The Ghost of Second Source Funding Has Lost a Desperate Court Battle

February 4, 2016The notorious company returned from the dead for one last final stand

For many veterans of the merchant cash advance business, the Second Source Funding name is something they’d rather forget. They were perhaps the largest funding ISO in the industry between 2006 and 2008. And as plenty of ex-employees will tell you, the story ends badly.

For many veterans of the merchant cash advance business, the Second Source Funding name is something they’d rather forget. They were perhaps the largest funding ISO in the industry between 2006 and 2008. And as plenty of ex-employees will tell you, the story ends badly.

Meir Hurwitz, a co-founder of NY based Pearl Capital, immortalized the Second Source years through a Bloomberg exposé about how his own company rose and sold for $40 million. In his tale, he claimed that Second Source founder Sam Chanin still owed him $2 million for the work he performed there. For Hurwitz, the falling out set the stage for the company he would go on to start. For other employees, it was the beginning of a grudge that would stick around for almost a decade.

Chanin has gone so far as to admit on his blog that he became known as “the guy who ripped them off and didn’t pay their residuals.” According to him, it wasn’t his fault. Court records do show Second Source Funding filing a complaint against Cynergy Data back in 2009 for $60 million in damages. Cynergy was the processor behind their lucrative merchant services operation and ultimately where the residuals they paid out to sales agents originated from. The case was dismissed in October of that year because Cynergy declared bankruptcy.

Effectively shuttered by the circumstances, the only reminder of what had once been, was another lawsuit filed by Second Source in September 2012 against a company (and more than 30 co-defendants) that acquired Cynergy Data’s assets. In October of 2009, Cynergy’s assets were reportedly sold to The Comvest Group for $81 million. In the complaint, Second Source sought at least $50 million from them in damages.

It has been approximately seven years since Second Source’s days ended, sources estimate. Users on industry forums were already speaking of the company in the past tense as far back as early 2009. The Second Source website no longer even exists. While ex-employees have long urged old peers to move on from those days, others have been forced to confront their demons.

THE GHOST OF MERCHANT CASH ADVANCE PAST

THE GHOST OF MERCHANT CASH ADVANCE PAST

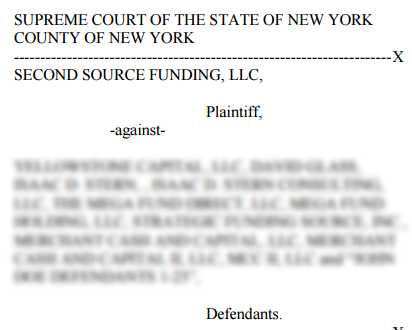

In September of 2014, the very same Second Source Funding emerged through a complaint filed in the Supreme Court of New York against Yellowstone Capital, LLC, 8 named co-defendants and 25 John Doe defendants. Seeking damages in the astounding amount of $360 million, Second Source alleged that Yellowstone’s co-founders stole their “revolutionary business model” of which they describe as using “Independent Sales Offices to leverage economies of scale in marketing and selling a bundle of financial services, including credit card processing and cash advances.” As a result of that and other claims, they were allegedly the reason for “Plaintiff SSF going out of business.”

The ensuing battle was probably one of the most contentious litigations the industry has ever experienced, at least from what can be seen on the docket. In one publicly filed exhibit introduced by Yellowstone, was the draft of a complaint that the plaintiffs had allegedly sent them that named more than 40 defendants. It reads like a yearbook of the merchant cash advance industry in 2009.

Other exhibits are packed with plenty of Second Source era nostalgia, including copies of the entrance exams given to new hires. One test question embodies the culture of the time, when it asked applicants:

What movie is this quote from, “Put the coffee down, coffee is for closers?”

While motions and cross motions at times appear to venture into the arena of insanity, especially considering Second Source went out of business a long time ago, deBanked has learned that Yellowstone was vindicated this week in a decision that dismissed all the claims with prejudice. That means they can’t have a do-over. The suit lasted 17 months.

deBanked has been quietly following the docket for over a year. We did not ask either party to comment on the decision for the reason being that Second Source may be considering an appeal, or at least they alluded to that in the court transcripts.

In the meantime, the ghost of Second Source reminded a few people in the merchant cash advance industry that the antics of 2006-2008 were more than just tall tales told by grey beard Wall Street guys. Back then the coffee was still for closers only. And back then, the game was so different that some people would still be feeling the effects of it a decade later.

In the meantime, the ghost of Second Source reminded a few people in the merchant cash advance industry that the antics of 2006-2008 were more than just tall tales told by grey beard Wall Street guys. Back then the coffee was still for closers only. And back then, the game was so different that some people would still be feeling the effects of it a decade later.

THEN AND NOW

Yellowstone Capital was one of the first merchant cash advance companies to experiment with the ACH payment method. Today, they originate nearly a half billion dollars a year in funded deals.

If you want to see just how much has changed since the Second Source days, check out this answer to the Second Source exam in 2008.

Q: If a merchant is getting an advance from MCA and can’t switch processors, what can the agent offer this merchant?

A: Lock box

It’s amazing to think that ACH was inconceivable at the time. Touched by ghosts indeed…

Industry Trade Group Coming of Age: The SBFA is Becoming More Political

February 1, 2016By hiring an executive director, the Small Business Finance Association hopes to achieve at least two goals – taking a step toward becoming a full-service trade group and providing a public voice for the alternative finance industry.

Stephen Denis, formerly deputy staff director of the U.S. House Committee on Small Business, went to work in the new role in mid-December, setting up shop with his cell phone and laptop in a Washington, DC, area coffee emporium. He’s the SBFA’s first full-time employee.

Hiring Denis, who also has association experience, represents “the next evolution” of the trade group, according to David Goldin, SBFA president and Capify’s founder, president and CEO.

The SBFA, which got its start in 2008 as the North American Merchant Advance Association, changed its name last year because members have added small-business loans to the their merchant cash advance offerings. Although the trade group’s not exactly new, it has plenty of room to grow and its leadership and members seem open to change.

The SBFA, which got its start in 2008 as the North American Merchant Advance Association, changed its name last year because members have added small-business loans to the their merchant cash advance offerings. Although the trade group’s not exactly new, it has plenty of room to grow and its leadership and members seem open to change.

“The goal is to start from scratch and take a look at everything the association is doing,” Denis told deBanked, “and to really build this out to a robust group that represents the interests of small businesses.”

Denis appears optimistic about pursuing that goal. He’s a native of the Boston area and a Harvard University graduate whose first job out of school was as an aide to Republican Sen. John E. Sununu of New Hampshire. After three years in that position, he took a job for two years with a UK-based trade association, traveling frequently to London to inform the group of Congressional action in the United States.

From there, Denis went on to become director of government affairs and economic development for the Cincinnati Business Committee, a regional association that included Fortune 500 companies among its members. After two years in that role, Denis joined the staff of Rep. Steve Chabot, R-Ohio, moving back to Washington and serving as the congressman’s deputy chief of staff during a five-year stint that ended when he joined the SBFA.

While working for Chabot, Denis also became deputy staff director of the House Committee for Small Business, the No. 2 position there, and he has held that job for the last three years. The committee’s tasks include learning as much as they can about small business, including financing, and using the information to advise members of the House on policy initiatives.

The experience Denis has amassed in government should serve the association well because his duties include briefing federal legislators and regulators on how the alternative-finance business works. With Denis as spokesperson, the industry can speak to government with a single voice, Goldin asserted.

“We are going to be aggressive in our outreach to legislators and regulators as well as be active reaching out to local, state governments,” Denis said. The SBFA will “work with other trade groups and small business groups to promote our mission to ensure small businesses have alternative finance options available to them.”

Until now, too many players from the alternative finance industry have been vying for lawmakers’ attention, Goldin said. To make matters worse, some of those seeking to influence government in hearings on Capitol Hill are brokers instead of lenders and thus may not have a perfect understanding of risk and other aspects of the business, he maintained.

“We’re hearing that there are people trying to be the voice of small-business finance that either don’t have a lot of years of experience or they’re not telling the whole story,” Goldin said. “We want to make sure the industry’s represented properly.”

Denis can draw attention away from the “noise” created by unqualified voices and focus on information that Congress needs to make reasonable decisions about the alternative finance business, Goldin maintained.

Besides getting the word out in Washington, the SBFA hopes to convey its message to the general public on “the benefits of alternative financing,” Goldin said. At the same time the group can help make small business owners aware of the finance options, Denis added.

Asked whether hiring Denis marks the beginning of an effort to lobby members of Congress for legislation the association deems favorable to the industry, Goldin said only that additional announcements will be forthcoming.

Asked whether hiring Denis marks the beginning of an effort to lobby members of Congress for legislation the association deems favorable to the industry, Goldin said only that additional announcements will be forthcoming.

Meanwhile, updated “best practices” guidelines might be in the offing to help industry players navigate the business ethically and efficiently, Goldin said. A set of six best practices the association released in 2011 included clear disclosure of fees, clear disclosure of recourse, sensitivity to a merchants’ cash flow, making sure advances aren’t presented as loans and paying off outstanding balances on previous advances.

Addressing other possible steps in the association’s growth, Goldin said the group doesn’t plan to publish an industry trade magazine or newsletter. However, a trade show or conference might make sense, he noted.

Denis said he and the board had not discussed the possibility of a test, credential or accreditation to certify the expertise of qualified members of the industry. However, associations often establish and monitor such standards, so it would be reasonable for the SBFA to do so, he added.

The association might establish a Washington office, Goldin said. “We’ll look to Steve for his thoughts and guidance on that,” he observed. Denis seems amenable to the idea. “Down the road, we would love to open an office and hire more people,” he said.

In Goldin’s view, all of those moves might help the rest of the world comprehend the industry. Understanding the industry requires taking into account the cost of dealing with risk and business operations, he said.

Placing a $20,000 merchant cash advance, for example, requires a customer-acquisition effort that costs about $3,000 and a write-off of losses and overhead of about $4,000, Goldin said. That’s a total of $27,000 even without the cost of capital, he maintained.

“Most people don’t understand the economics of our business,” Goldin continued. The majority of placements are for less than $25,000, he said, characterizing them as “almost a loss leader when you factor in the acquisition costs.”

While spreading that type of information on the industry’s inner workings, Denis will also conduct the day-to-day for the not-for-profit’s affairs. The association’s board of directors will continue to set policy and objectives.

Members elect the board members to two-year terms. Current board members are Goldin; Jeremy Brown of Rapid Advance, who’s also serving as the group’s vice president; John D’Amico, GRP Funding; Stephen Sheinbaum, Bizfi; and John Snead, Merchants Capital Access.

Member companies include Bizfi, BFS Capital, Capify, Credibly, Elevate Funding, Fora Financial, GRP Funding, Merchant Capital Source, Merchants Capital Access (MCA), Nextwave Funding, NLYH Group LLC, North American Bancard, Principis Capital, Rapid Advance, Strategic Funding Source and Swift Capital.

Companies pay $3,000 in monthly dues, which Denis characterizes as inexpensive for a DC-based trade association.

Membership could spread to other types of businesses, Denis said. “I’d like to expand the tent to other industries,” he noted. “The association is trying to represent the interests of small business and make sure they have every finance option available to them.”

But a key purpose of the trade association is to provide a forum for members to come together as an industry, Denis said. “We’re thinking big,” he admitted. “We hope that all members of the marketplace will want to become a part of it.”

January/February 2016 Cover Teaser

January 25, 2016The January/February 2016 issue of deBanked magazine is set to ship soon. Can you guess who is on the cover???

If you don’t already get the hard copy of our magazine, you can SUBSCRIBE HERE FREE. To review previous issues in HTML or PDF, click here.

Platinum Rapid Funding Group Sets Annual Funding Record

January 25, 2016Platinum Rapid Funding Group, a Long Island, NY based merchant cash advance provider, set a new personal-best funding record last year, according to company VP of Partner Relations Corey Cicero. Through direct and indirect channels, the company originated more than $100 million worth of funded deals during 2015.

The growth has led to what seems like a never-ending hiring spree at their Uniondale office. Cicero told deBanked that they plan to beat their 2015 figures this year by a wide margin. “We are still hiring,” he said.

deBanked visited their office back in September and as evidenced by the above photo, they are not a small shop.

Should Funders Pay Lifetime Renewals?

January 24, 2016OPINIONS ARE LIKE A-HOLES RIGHT?

We all know what they say about “opinions” right? They (opinions) are basically like a-holes and everybody has one. I’ve stated a lot of opinions here on deBanked over the last couple of months, while some might agree and others disagree, I always try to provide educated opinions to separate commentary from the generic pack of people blurting out comments across industry forums and media publications that might not have firsthand experience on the front lines.

With that being said, it’s in my sole opinion that every funder/lender should offer their independent brokers lifetime renewal compensation despite new deal volume.

BROKER AGREEMENTS SEEM TO CHANGE ON A WHIM

BROKER AGREEMENTS SEEM TO CHANGE ON A WHIM

I’ve been reselling the merchant cash advance and alternative business loan products since November 2009, however, the current program structures/agreements of my funders and lenders look totally different today than they did in the beginning.

It’s almost as if a new agreement is created every 12 – 18 months with similar conditions, but certain terms might have changed, including the compensation of renewals.

Some funders and lenders will start without any provisions related to renewals, basically as long as the client continues to renew, then you will be allowed to collect commissions off the client. But later on down the line, some funders and lenders will change provisions and require certain levels of new deal volume in order to be compensated on renewals going forward. Most broker agreements have terminology listed that states that the funder/lender can change the program at their discretion, however, I believe that at no point in time (other than for particular circumstances of fraud or ethics violations) should a funder take away a broker’s renewal compensation as whatever “good” it’s supposed to be doing (which I still can’t think of any), I believe it does far more damage in return.

YOU CAN’T CLOSE WHAT YOU CAN’T GET APPROVED

Sometimes a broker doesn’t fund a deal within 3 – 12 months because the funder can’t approve any of the submitted deals. If the broker is like myself, I’m going to pre-screen all new applications to see if it fits the underwriting criteria before submitting it, as submitting applications that are outside the criteria does nothing but waste valuable underwriting resources. If they are a somewhat conservative funder, a lot of times a broker just might get too few applicants to fit the box.

WHAT DID YOU ACTUALLY SPEND ON MARKETING?

Funders and lenders receive free marketing from brokers because they bring them the deals, so what is the big deal about continuing to pay renewal compensation despite new deal volume? They don’t have to worry about taking the risk of putting marketing capital up on the table with a potential of no return. The person who puts up the capital is the broker, and they should be compensated for the lifetime of the client regardless of new deal volume.

As an independent broker, the individual is a part of the Mom and Pop Network, which is just a group of random brokers who resell for free (100% commission). Not only are funders/lenders receiving the free marketing from the resellers, but they are also receiving free data to utilize in any potential “big data” valuations for sell-off, or “big data” analysis for better market segmentation. In addition, if the broker’s portfolio of merchants (even if it’s just one merchant) didn’t default or the default rate is very low, what is the justification for cutting off the broker just because there was no new deal funded?

RENEWALS ARE THE LIFEBLOOD OF THE BROKER’S INCOME

Once upon a time, during the very early days of MCA, the product was pretty much a one-off project. A merchant had an emergency, they sold off a percentage of their future credit card receivables in exchange for some upfront cash today, and used the cash to address whatever emergency they were facing. If the merchant renewed, it was usually one time (twice if you were lucky) and that was it. Today, it’s a different situation if you set up your merchant based on their proper Paper Grade. Merchants are renewing back-to-back, a lot of times for 3 to 5 years (or more) in a row, which means that the product is becoming more of an integrated portion of their business (similar to the MCA’s Kin A/R Factoring) rather than a one-off occurrence. This means for a broker, there’s a lot of money to be made off of their MCA portfolio going forward and the entire point is to build your portfolio up to a particular size, where you can just “sit back” and solely manage the renewals of the portfolio without being required to continually produce new deals by spending more on marketing.

Take a broker with a portfolio of 25 merchants who renew just about every 6 months (twice a year) with an average funding of $75,000 with 5 points commission per deal. That alone is $3.75 million a year in funding volume and almost $100,000 per year in income, solely off the renewal portfolio. If the broker maintains this portfolio for 10 years in a row, that’s almost $38 million in funding volume and close to $1 million in income. Why on Earth would you want to even threaten to cancel a broker out of the deal when again, it was their ingenuity, rapport building skills and sales skills that are the foundation of the clients coming to the funder to begin with, as well as continuing to renew back-to-back?

YOU ARE ASKING FOR YOUR MERCHANTS TO BE FLIPPED OR STACKED

The broker is the one who has the original relationship with the merchant, thus, the merchant more than likely has more rapport with the broker than they have with anyone in the funder’s organization. Thus, cutting off the broker from the renewal compensation might do nothing but just cause the merchant(s) to be stacked or flipped to another funder/lender.

TELL ME WHICH BROKER IS MORE VALUABLE? BROKER A OR BROKER B?

Okay, so tell me which Broker is more valuable? Is it Broker A or Broker B?

– Broker A: Over the course of one year, Broker A brings in 15 new merchants, with only 4 of those merchants renewing once because the broker didn’t price the merchants in their proper Paper Grade and thus, a competitor stole them away at renewal. This produces a total of 19 advances (new/renewal) and let’s say with the average funding being $50,000 you are looking at volume of $950,000.

– Broker B: Over the course of one year, Broker B brings you only 8 new merchants, but 3 of them renew 4 times back-to-back (12 additional advances), 2 of them renew 3 times back-to-back (6 additional advances), 2 of them renew 2 times back-to-back (4 additional advances), and 1 of them renew only once, for a total of 31 advances (new/renewal). Keeping the average funding at $50,000 you are looking at volume of $1,550,000.

Broker B supplied fewer new deals than Broker A, but Broker B provided an overall higher level of production based on the rapport and proper structure they established with their clients that produced more renewals and advances in total for the funder. Seeing as though in our industry, when funders count their “total volume funded” they include both new and renewal volumes, how can it be that Broker B is not more valuable to a funder than Broker A is? Not saying that Broker A isn’t valuable, but based on potentially cutting off renewal compensation due to a lower amount of new deal volume, they would potentially be cutting off the Broker that offers more value over time.

THE FINAL WORD

Why on Earth would a funder or lender want to kick out a competent broker by cutting off their renewal portfolio? What does it solve to cut off a competent broker, with a low (or no) default rate, just because they didn’t bring in newly funded deals during the previous 3 – 12 months? What does that solve? Does cutting them off somehow produce more margin for the funders? More market share? Savings in some sort of area? As mentioned, the broker is likely to flip the merchants or stack the merchants when this happens, which again, does nothing for the funder in terms of providing any type of benefits or value.

The only justification for cutting off a broker is when they are engaged in unscrupulous acts. But cutting off competent brokers just because they didn’t fulfill some insane new deal volume policy, makes absolutely no sense because at the end of the day, cutting off the brokers will be like cutting off the funder’s relationship with the merchants as well. With the parade of new funders looking to grab market share, what better way to gain it than to partner with competent but dejected brokers, who just got their renewal compensation cut off for not fulfilling some insane new deal policy?

To Syndicate or Not to Syndicate?

January 20, 2016 Someone once asked the question of, “To love or not to love?” But I believe soon every broker will have to ask the question of, “To participate or not to participate?” Is it time we all get into the game?

Someone once asked the question of, “To love or not to love?” But I believe soon every broker will have to ask the question of, “To participate or not to participate?” Is it time we all get into the game?

THE YEAR OF THE BROKER OR THE YEAR OF ROSY PROMISES?

Debanked writers such as Sean Murray, Ed McKinley and myself, referred to 2015 as the Year of The Broker, as a stream of new brokers continued to rush into our space to take advantage of the perceived opportunities.

THE YEAR OF PARTICIPATION?

For experienced brokers, I’ve written two pieces so far here on deBanked in relation to the broker’s future. I’ve talked about how I believe the future of our industry will be dominated by Strategic Networks and those who utilize these networks efficiently will not just be the dominant players going forward, but they will be pretty much the only “real” players going forward. I also talked about how success in our industry is based mainly on leveraged resources and networks, rather than having some sort of “superior” selling capability.

But with that being said, I wanted to use this article as a way to add to this discussion of the future by outlining my recommendation that experienced brokers “get into the game” when it comes to syndication and deal participation. DeBanked reported back in April of 2015 about how Strategic Funding Source’s syndication network of over 200 partners (at the time) invested over $260 million of their own capital into funded deals. This level of investment, according to the reporting, helped amass significant wealth for the 200 syndication partners that participated. If 2015 was the Year of The Broker, could 2016 be the Year of Participation?

IT’S NOT THE SAME ANYMORE

It’s no longer 2000 – 2013, when quite frankly a broker could amass great income by just strategically utilizing the Uniform Commercial Code (UCC) as a marketing model. But pretty soon the word got out and everybody rushed in to duplicate the methodology. What was once a great idea became a complete waste of marketing dollars.

UCCs are so bad today, that when you call a merchant and just mention the fact that you are from a funding company, they immediately hang up the telephone. Sometimes, I would call and before I would even have the chance to say a word, the staff member on the telephone would ask, “Are you calling about a cash advance?” Once I would reluctantly answer in the affirmative, they would of course immediately inform me to put them on the do not call list, never call again, and either in nice language or a language full of swearing, they would inform me that they aren’t interested and how I’m the 19th guy that has called them this week. This is the result of a merchant getting 20 calls a week from 20 different companies, about 20 different merchant cash advance products.

As a result, brokers are going to have to specialize in the Strategic Networks and leveraged resources that I have been discussing for nearly a year now on Debanked. We will also have to juggle the rising marketing costs and increasing pressures on pricing as our industry goes more mainstream. You might not want to operate as a full-fledged direct funder, as I understand that the investment outlay for such a task is significant. But I believe going forward, you aren’t going to be able to “make it” like you used to by solely relying on commissions from brokering deals. You are going to have to get into the game and put some money in deals not just to sustain the amount of income you were making in commissions historically, but to potentially make more money than you ever made before.

A SHOUT OUT TO WBL

Also back in April of 2015, there was a pretty popular online discussion that discussed World Business Lenders’ (WBL) new ISO/Broker acquisition program. I had a conversation by telephone with Lenny Steigman from WBL on April 21st of last year to discuss the program in detail.

One of the things that Lenny mentioned on that call was the notion of the broker’s office requiring a shift in structure in order to survive in the upcoming future. Lenny discussed that brokers who chose to continue to operate on the sidelines relying solely on commissions from brokering deals, without getting involved in some sort of equity or syndication participation, might find the future of their involvement in our space limited as continued growth through strategic networks drive the progression of the industry. I could not agree more with Lenny Steigman. It’s certainly time for a shift and one of those shifts I believe will require more experienced brokers to become syndication partners through putting up a portion of the capital to fund the merchants that they service.

GET YOUR DUCKS IN ORDER

As you prepare for this shift and look to get into the game, make sure that you have your ducks in order:

Legal Representation: This is important, you need an attorney to review your syndication agreements as well as review the legal structure of the funder you are partnering with, to make sure that all of the legal terminologies are outlined properly.

Understand The Deals You Are Funding: Know the type of client you are funding, such as if they are A Paper, B Paper, C Paper, D Paper or E Paper. Your level of risk on the deal in terms of default increases when you get into the higher risk paper grades, thus, make sure you are getting a significant enough “return” on said deals to accommodate the risk you are tolerating.

Examine Your Funder’s Finances: By syndicating, you are doing more than just investing in the merchants that you serve, you are also investing in the financial soundness of the funder you are syndicating with. Make sure your funder is not on the verge of bankruptcy, profitable, and will actually be around a year from now.

Examine Your Funder’s Operational Structure: I’ve talked about the importance of making sure you vet who you partner with in relation to being a broker. Now that you are syndicating, you most definitely make sure you are dealing with a funder that’s “proven.” The funder should have at least 2 years in business, have funded in the eight digits in terms of volume, have a proven and profitable underwriting formula, have an office full of employees, not have a significant amount of bad reviews, be in good standing with the BBB, having an actual online presence, and they should be running a professional and competent organization overall.

Round Up Your Capital: The secret of many of the wealthy has always been their unique ability to utilize the money of other people for their business investments. They find equity investors seeking a return on their capital, invest said capital with a high return and collect a management fee off of the transaction. Or, they borrow money from a creditor at a particular interest rate, invest the monies for a higher rate of return, then pay off the loan with interest and pocket the profits. Whichever way you prefer, how about you utilize OPM (other people’s money) to your advantage (leverage) as well for your participation efforts?

TO PARTICIPATE OR NOT TO PARTICIPATE?

I believe we might be entering the year of participation, which means it’s time for the experienced brokers to join in on the strategic networks which will dominate our space going forward. New entrants who don’t know the space and still can’t spell “merchant cash advance” will be in for a bumpy ride going forward, but those with the experience, it’s time to add to your industry influence by coming off of the sidelines as brokers solely, and becoming broker/syndicates in the truest form.

Me-Too Lenders Reject The Opportunity to be Unique

January 15, 2016 IMITATION IS THE BEST FORM OF FLATTERY

IMITATION IS THE BEST FORM OF FLATTERY

You know they say that the imitation is the best form of flattery, the only problem is that flattery is insincere praise, or praise only given to further one’s own selfish interests.

Surely new funders and lenders in our space are looking to further their own selfish interests by stealing away market share from existing players, which is perfectly fine seeing as though we operate in a free market society. However, what doesn’t make sense to me is thinking that you can steal away a competitor’s clientele by looking, sounding, and behaving exactly like he does.

THEY ALL SOUND THE SAME

I have no idea how many direct funders are present in our space today, but from what I’ve heard it’s well into the hundreds, and I receive recruiting emails along with invites on LinkedIn from these new players all of the time. What’s strange about just about all of these new players is that they all sound, specialize in, and operate the same as my current funders, leaving me scratching my head wondering why in the hell should I bring my volume over to you, if you do nothing different? I can hear them now:

– “John, we can consolidate your merchant’s balances as long as they net 50%!” (This isn’t anything new, the 50% net rule has been around for 17 years.)

– “John, we can approve some of your merchants for as low as a 1.12!” (This isn’t anything new, A+ and A Paper merchants have been receiving proper risk based pricing for years now.)

– “John, you will receive a dedicated account manager!” (This isn’t anything new, funders and lenders have been providing their broker houses with dedicated ISO Managers for around 17 years.)

– “John, we can fund just about every deal if the deal makes sense!” (This could be a new concept, the problem is that I have heard this before, only to submit a “restricted industry” merchant and it be declined just like it’s declined everywhere else.)

– “John, we fund deals as small as $5,000 to as high as $5 million!” (This isn’t anything new, this has been the standard funding range for years now. Plus, it’s rare that a broker in our space would get a merchant that needs $5 million, as those merchants would usually rely on the traditional lending system.)

– “John, we get deals done fast!” (Everybody says this, the reality is that unless a lender has automated the majority of their closing process as well as eliminated many portions of said closing process, then that means they are still doing a good chunk of it “manually”, which means it will always take 2 – 10 business days to complete everything.)

NOT EVERY “DIRECT FUNDER” IS A “DIRECT FUNDER”

There are a number of small firms that might market themselves as a direct funder, but the reality is that all they do is fund their deals through some type of syndication platform. My definition of a direct funder or lender is one that has built their own underwriting platforms and produced their own formulas to complete merchant cash advance transactions or alternative business loans. Thus, to be a direct funder (based on my definition), it’s going to “cost you something” in terms of real investment in your infrastructure, your people, as well as needing to raise millions of dollars in lending capital.

OUR TRUE PURPOSE IS DISRUPTION

Understand that our true purpose here on the alternative side of the debt financing space is to innovate how financing is underwritten, approved and delivered, seeking to steal market share away from traditional lending systems. The media calls this process “disruption.” Our system is so efficient, that with one of our industry’s most popular platforms, a small business owner can go online at 11:30 a.m. to apply for a loan, get an approval by 12:15 p.m., then complete their entire closing process online by 12:25 p.m. Within 60 minutes, a small business can start, sign for, and close their small business loan application for amounts including $25k, $75k, $150k, $200k, etc., and receive the funds in their bank accounts the next morning. The traditional lending system cannot underwrite, approve and deliver financing with this amount of efficiency, speed and proficiency.

IF YOU ARE GOING TO BE A DIRECT FUNDER, WHY NOT CONTRIBUTE TO CHANGING THE GAME?

Various reports on marketplace lending have estimated that the global lending size of our space is near $60 billion per the end of 2015, but it’s also estimated that by 2020 we will be near $300 billion of the total global lending market (includes lending on the consumer and commercial sides). Understanding this, what baffles me with new funders and lenders, is why in the hell are you going through the hassles of setting up your own platform, raising millions of dollars in lending capital, and setting up an experienced underwriting team, only to come into the market and do absolutely nothing different?

That makes absolutely no sense. You have the technology, the people, the capital and the formula behind you, so please add a unique contribution to our space to assist our industry as a whole (consumer and commercial side) in growing to this $300 billion in global lending metric by around 2020.

SPECIALIZATION RECOMMENDATIONS

When you enter the market and send brokers information on your program, it should be clear what separates you from everybody else and what your unique role will be going forward in helping our space achieve this $300 billion in global lending metric. Here are a couple of recommendations off the top of my head that you could utilize for specialization:

#1.) A True High Risk Funder/Lender

How about actually funding industries that nobody else will fund? I’ve seen this promoted before but I’m talking about going all the way by taking a look at our market’s standard underwriting practices across the board, then asking the question of, “What merchants are being pushed out and why? How can we start saying YES to these merchants rather than saying NO like everybody else is doing?” You could begin by putting together a list of industries on just about every funder or lender’s restricted list, then trying to figure out how to fund these categories with risk based pricing.

#2.) Bring Efficiency To Global Lending

How about funding in countries that other funders aren’t funding in? Basically, bringing the efficiency of the US market to the global markets in a way that currently is lacking? It’s hot over here in the US market with many players and competitors, but what about in the UK, Australia, China, etc.?

#3.) A Completely New Product

How about creating a new alternative working capital product that we’ve never heard of before?

#4.) Further Lowering Of Pricing

How about find a way to continue bringing down your cost of operations, administration and lending, so that brokers are able to have lower base pricing to increase profitability on lending to merchants, even those in A+ and A Paper categories? This can also help open up the market to attract higher credit grade merchants due to the lower pricing available, but still with “liberal” underwriting procedures.

#5.) A More Efficient Alternative Asset Based Lending Product

How about creating a more efficient alternative asset based lending product, that competes with the current crop of alternative asset based lenders? The current crop that we have today has a lot of inefficiencies within their product, such as having the merchant put up luxury items or even their house to obtain approval, but still charging the merchant rates that resemble traditional merchant cash advance factor rates or even higher. Shouldn’t the fact that a merchant is putting up tangible collateral lower the risk on the deal, which should also lower the pricing and extend the term? So I say, how about some innovation be done in this area so more of these products could be sold?

#6.) Innovation in Factoring, Purchase Order Financing and Equipment Leasing

How about providing accounts receivable factoring, purchasing order financing and equipment leasing, but finding a way to provide such services in an innovative fashion that’s different than the current crop of funders or lenders offering said services?

#7.) A Real Alternative Based Line Of Credit

There are certainly alternative line of credit programs out in our market today, but they are not as efficient as they should be. How about you create a real alternative based line of credit that would resemble something similar to a credit card line of credit, where the merchant can take it out and have it on the side, without it interfering with that of other financing programs such as a merchant cash advance or an alternative business loan?

#8.) Innovation In Consumer Lending

I know that regulations are much higher on this side, but could it be possible for you to find a way to create some innovative consumer lending products as well?

THE FINAL WORD

You have the technology, the people, the capital and the formula, so why in the world do you want to copy a current player instead of doing something different?

While I’m not saying that you shouldn’t also offer said programs of the current players to steal market share away from them, it’s just my opinion that the biggest opportunity today for new funders and lenders is to specialize in other niche areas that aren’t being catered to by our current market players.

Doing so should allow you to come in, specialize, make a name for yourself, and brand your organization as the “go to” funder/lender for (insert innovative concept here) for years to come. It might take you some time to “perfect” your unique brand and approach, but as long as you have investors that believe in your concept, you should be able to survive through the growing pains. To quote Herman Melville, always remember the following: It is better to fail in originality than to succeed in imitation.

Are You Weak, Or Are The Leads Weak?

January 13, 2016 A LOOK BACK AT A CULT CLASSIC

A LOOK BACK AT A CULT CLASSIC

The 1992 film, Glengarry Glen Ross, is a cult classic and one of my favorite movies of all time, with excellent writing, storyline and acting work done on behalf of the stars. In my opinion, the best part of the film was the beginning, when Blake (played by Alec Baldwin) was sent in from Mitch & Murray to fire up three of the office’s sales reps who were “low on the board” in terms of their sales performance. Blake’s “always be closing” speech has been glorified and imitated in sales offices across the United States since the movie’s release on Friday, October 2nd, 1992. I can hear the conversation between Blake and the late Jack Lemmon’s character, Shelley “The Machine” Levene, right now:

Blake: You laughing now? You got leads, Mitch & Murray paid good money, so get their names to sell them! You can’t close the leads you’re given?! If you can’t close sh*t, then you are sh*t! Hit the bricks pal and beat it because you are going OUT!

Shelley “The Machine” Levene: The leads…are weak.

Blake: The leads are weak?! F**king leads are weak?! You’re weak!

Blake was sent in to “fire up” The Machine as well as Dave Moss (played by Ed Harris) and George Aaronow (played by Alan Arkin), who were all struggling to meet sales numbers due to what they believed to be mainly their Office Manager’s fault (John Williamson who was played by Kevin Spacey) for supplying them bad, outdated and dead leads. The main character of the film was Ricky Roma (played by Al Pacino) and Roma wasn’t having the same struggles as his three counterparts, as he received the “premium leads” from Williamson for being number one on the board in terms of sales performance.

WAS ROMA’S SUCCESS MORE OF A RESULT OF HIS PERSONALITY OR THE GOOD LEADS?

Could Roma’s sales success have been based on the fact that he was just a “tad bit” more charismatic than The Machine, Moss and Aaronow? Or, could the bulk of Roma’s success be tied to the fact that he wasn’t sent out to sell to dead leads? Were the reps weak, or were the leads weak?

Moss believed it was all about the leads, even suggesting to Aaronow during the film that they start their own agency. Towards the end, Roma himself revealed that he believed it was all about the leads as well, as once someone broke into the office to steal the premium Glengarry leads out of Williamson’s office (which was later revealed to be The Machine and Moss), Roma was offered some of Williamson’s “dead leads” and Roma quickly rejected them, throwing them back into Williamson’s face and stating that he wasn’t going out until he got the Glengarry leads.

As mentioned, this movie is a cult classic, but often art imitates life as this movie displays one of the fundamental problems of the sales profession today as a whole, and it’s the fact that most Sales Managers are completely out of touch. As a result, for this article let’s take a deeper look into this topic to determine if you’re weak, or if the territory, market and leads you are being asked to “sell” or “sell into” are weak.

IT’S TIME TO DO AWAY WITH MOST SALES MANAGERS (THEY ARE USELESS)

As globalization and technology automation in the 21st century surely replaces the jobs of many retail salespeople, customer service agents, and low level brokers, what I’m really hoping for is that someway and somehow, we can get rid of most Sales Managers. They are one of the biggest problems in the sales profession today because:

- They are completely out of touch

- They promote sales strategies that don’t work

- They teach their reps to read off “scripts”

- They don’t equip their reps with research, trends and ground breaking solutions

- They don’t train their reps to become component professionals who can critically think

- They instead train their reps to become a robotic, script reading, mindless drone

On top of all of this, most Sales Managers do not understand the B2B Sales cycle, as they “train” their reps as if they are selling a box of girl scout cookies or a new music album, focusing on over the top personalities, how cute someone is or their level of charisma. Instead, they should be focusing on providing knowledge, research, trends and other information to build a competent critically thinking professional, to implement market solutions that fulfill unmet market demand.

The majority of Sales Managers need to be done away with. These incompetent fools believe that it’s mainly the personality of the sales rep that makes them successful, thus, they will throw their reps out in a bad territory, a bad market, and calling on dead leads because in their mind a “good sales rep” has the “personality” to sell fire to Hell. As a result, their belief is that the quality of the market, the territory, the leads, nor the competitiveness of the products they sell don’t matter!

DO NOT WORK UNDER A SALES MANAGER

I usually recommend that B2B sales professionals work on an independent basis so that they don’t have to be subjected to an out of touch Sales Manager, which does nothing but stop your career progression and limit your earning potential. This is especially true when these out of touch Sales Managers provide you with their “leads”, as a vast majority of the time, their “leads” are inefficient.

THEIR LEADS ARE REALLY JUST DATA RECORDS (BUT THEY DON’T KNOW THAT)

Most of the time the leads aren’t leads, they are data records. You are going to have a much lower conversion rate on data records than you would leads, but the out of touch Sales Manager (who thinks he just gave you “leads”) will think that your conversion should be a lot higher and thus, he might “inform you” that you just aren’t cut out for this business.

THEIR LEADS ARE OLD AS HELL AND THE SALES CYCLE IS OVER (BUT THEY DON’T KNOW THAT)

Or, they might supply leads that are aged, sometimes from 90 days ago or more, thinking that the sales cycle is still active with these leads when the fact is that for the vast majority of them, the sales cycle was over months ago. Aged leads are usually leads where a merchant requested financing, but there’s usually one of three issues with these types of “leads”. Number one, the merchant either received the funding they wanted two months ago, or number two, they were declined by everybody and gave up on speaking with anybody else about the topic. Or number three, it could have been the case where the merchant wasn’t truly serious about getting funded anyway, deciding not to move forward with anybody. The few leads that you do convert, because your Sales Manager believes these were “hot leads”, he will end up scolding you over the low conversion numbers.

THEY USE THE GLENGARRY GLEN ROSS MODEL (WHICH REVEALS HOW INSANE THEY ARE)

This is the biggest pet peeve right here, they might use the Glengarry Glen Ross model, which makes absolutely no sense. So here’s what they would do.

They would spend a lot of money on a marketing budget to produce a good stream of leads of merchants looking for financing assistance from an alternative basis. However, instead of dishing them out to their sales reps in equal number, they will give the majority of them to the reps “already high up on the board” and give hardly any of them to the reps at the lower end of the stick. All this does is causes the “rich to get richer” in that the reps getting the hot leads will just continue to stay up high on the board while those at the bottom can never move up.

What I don’t get is this, if you don’t believe in the reps at the bottom of the board, why not terminate them? Why the hell would you keep them on your staff, if you no longer believe in their abilities to perform and thus, aren’t going to provide them with the resources needed to move up on the board?

ARE THE LEADS WEAK, OR ARE YOU WEAK?

The truth is that in professional sales, it’s all about supply, demand, and solving complex problems with innovative solutions. It takes research, strategic planning and strategic market segmentation in terms of who we target, as the target of our prospecting has to be someone who is currently in a situation to utilize our services. This means that 90% of the job is that of finding the right territory, market and/or leads to sell to. Now, there are a lot of incompetent salespeople in the world, and you could equip them with the resources needed to succeed and they still fail to execute. That would indeed make those reps “weak” rather than the leads being weak. But in my opinion, far too often are competent salespeople at the mercy of a weak Sales Manager that provides them with weak training, weak products, weak markets, a weak territory, and weak leads. It’s based on this that my opinion stands, in that most of the time it’s the leads that are weak, rather than the competency of the sales professional.