RapidAdvance’s Mark Cerminaro is deBanked’s November/December Cover

December 14, 2016

It’s been a quick rise for Mark Cerminaro, who won the 2016 Commercial Finance Association’s 40 Under 40 Award and is the Chief Revenue Officer of RapidAdvance based in Bethesda, MD. He is featured in the November/December issue of deBanked magazine that is currently being delivered to subscribers nationwide. If you haven’t already subscribed, you can SIGN UP HERE FREE.

An excerpt from the story:

Early in Cerminaro’s tenure at Morgan Stanley, the company sent him for training with about 300 other new employees at 2 World Trade Center in Manhattan. The date was Sept. 10, 2001. When the trainees reported to the office the next day, they were in a 64th-floor conference room when they heard an explosion and saw shreds of paper floating past the windows. They didn’t realize yet that a terrorist controlled jetliner had hit next door at 1 World Trade Center.

deBanked interviewed Mark and several folks who know him professionally. He joined RapidAdvance in 2007, which gave him a front row seat to the financial crisis that forever shaped the company. “We went from a single-product company, to now being more of a solutions-based company,” he said.

If you want to know how the big players are succeeding, you’ll certainly want to hear what a day in the life of a chief revenue officer is like, and how Mark is making the sales hum at Rapid.

The digital version will be online next week, but you don’t want to miss deBanked magazines in print. Sign up FREE!

Alternative Funders Bid Adieu to 2016, Show Renewed Optimism for 2017

December 12, 2016

After getting pummeled in 2016, many alternative funders have licked their wounds and are flexing their muscles to go another round in 2017.

“The industry didn’t implode or go away after some fairly negative headlines earlier in the year,” says Bill Ullman, chief commercial officer of Orchard Platform, a New York-based provider of technology and data to the online lending industry. “While there were definitely some industry and company-specific challenges in the first half of the year, I believe the online lending industry as a whole is wiser and stronger as a result,” he says.

Certainly, 2016 saw a slowdown in the rapid rate of growth of online lenders. The year began with slight upticks in delinquency rates at some of the larger consumer originators. This was followed by the highly publicized Lending Club scandal over questionable lending practices and the ouster of its CEO. Consumers got spooked as share prices of industry bellwethers tumbled and institutional investors such as VCs, private equity firms and hedge funds curbed their enthusiasm. Originations slowed and job cuts at several prominent firms followed.

Despite the turmoil, most players managed to stay afloat, with limited exceptions, and brighter times seemed on the horizon toward the end of 2016. Institutional investors began to dip their toes back into the market with a handful of publicly announced capital-raising ventures. Loan volumes also began to tick up, giving rise to renewed optimism for 2017.

Notably, in the year ahead, market watchers say they anticipate modest growth, a shift in business models, consolidation, possible regulation and additional consumer-focused initiatives, among other things.

MARKETPLACE LENDERS REDEFINING THEMSELVES

Several industry participants expect to see marketplace lenders continue to refocus after a particularly rough 2016. Some had gone into other businesses, geographies and products that they thought would be profitable but didn’t turn out as expected. They got overextended and began getting back to their core in 2016. Others realized, the hard way, that having only one source of funding was a recipe for disaster.

“Business models are going to evolve quite substantially,” says Sam Graziano, chief executive officer and co-founder of Fundation Group, a New York-based company that makes online business loans through banks and other partners.

For instance, he predicts that marketplace lenders will move toward using their balance sheet or some kind of permanent capital to fund their loan originations. “I think that there will be a lot fewer pure play marketplace lenders,” he says.

Indeed, some marketplace lenders are starting to take note that it’s a bad idea to rely on a single source of financing and are shifting course. Some companies have set up 1940-Act funds for an ongoing capital source. Others have considered taking assets on balance sheet or securitizing assets.

“The trend will accelerate in 2017 as platforms and investors realize that it’s absolutely necessary for long-term viability,” says Glenn Goldman, chief executive of Credibly, an online lender that caters to small-and medium-sized businesses and is based in Troy, Michigan and New York.

BJ Lackland, chief executive of Lighter Capital, a Seattle-based alternative lender that provides revenue-based start-up funding for tech companies, believes that more online lenders will start to specialize in 2017. This will allow them to better understand and serve their customers, and it means they won’t have to rely so heavily on speed and volume—a combination that can lead to shady deals. “I don’t think that the big generalist online lenders will go away, just like payday lending is not going to go away. There’s still going to be a need, therefore there will be providers. But I think we’ll see the rise of online lending 2.0,” he says.

Despite the hiccups in 2016, Peter Renton, an avid P2P investor who founded Lend Academy to teach others about the sector, says he is expecting to see steady and predictable growth patterns from the major players in 2017. It won’t be the triple-digit growth of years past, but he predicts investors will set aside their concerns from 2016 and re-enter the market with renewed vigor. “I think 2017 we’ll go back to seeing more sustainable growth,” he says.

THE CONSOLIDATION EQUATION

Ron Suber, president of Prosper Marketplace, a privately held online lender in San Francisco, says victory will go to the platforms that were able to pivot in 2016 and make hard decisions about their businesses.

Prosper, for example, had a challenging year and has now started to refocus on hiring and growth in core areas. This rebound comes after the company said in May that it was trimming about a third of its workforce, and in October it closed down its secondary market for retail investors. Suber says business started to pick up again after a low point in July. “Business has grown in each of the subsequent months, so we are back to focused growth and quality loan production,” he says.

Not long after he said this, Prosper’s CEO, Aaron Vermut, stepped down. His father, Stephan Vermut, also relinquished his executive chairman post, a sign that attempts to recover have come at a cost.

Other platforms, meanwhile, that haven’t made necessary adjustments are likely to find that they don’t have enough equity and debt capital to support themselves, industry watchers say. This could lead to more firms consolidating or going out of business.

The industry has already seen some evidence of trouble brewing. For instance, online marketplace lender Vouch, a three-year-old company, said in June that it was permanently shuttering operations. In October, CircleBack Lending, a marketplace lending platform, disclosed that they were no longer originating loans and would transfer existing loans to another company if they couldn’t promptly find funding. And just before this story went to print, Peerform announced that they had been acquired by Versara Lending, a sign that consolidation in the industry has come.

The industry has already seen some evidence of trouble brewing. For instance, online marketplace lender Vouch, a three-year-old company, said in June that it was permanently shuttering operations. In October, CircleBack Lending, a marketplace lending platform, disclosed that they were no longer originating loans and would transfer existing loans to another company if they couldn’t promptly find funding. And just before this story went to print, Peerform announced that they had been acquired by Versara Lending, a sign that consolidation in the industry has come.

“I think you will see the real start of consolidation in the space in 2017,” says Stephen Sheinbaum, founder of New York-based Bizfi, an online marketplace. While some deals will be able to breathe life into troubled companies, others will merge to produce stronger, more nimble industry players, he says. “With good operations, one plus one should at least equal three because of the benefits of the economies of scale,” he says.

Market participants will also be paying close attention in 2017 to new online lending entrants such as Goldman Sachs’ with its lending platform Marcus. Ullman of Orchard Platform says he also expects to see more partnerships and licensing deals. “For smaller, regional and community banks and credit unions—organizations that tend not to have large IT or development budgets—these kinds of arrangements can make a lot of sense,” he says.

A BLEAKER MCA OUTLOOK

Meanwhile, MCA funders are ripe for a pullback, industry participants say. MCA companies are now a dime a dozen, according to industry veteran Chad Otar, managing partner of Excel Capital Management in New York, who believes new entrants won’t be able to make as much money as they think they will.

Paul A. Rianda, whose Irvine, California-based law firm focuses on MCA companies, likens the situation to the Internet boom and subsequent bust. “There’s a lot of money flying around and fin-tech is the hot thing this time around. Sooner or later it always ends.”

In particular, Rianda is concerned about rising levels of stacking in the industry. According to TransUnion data, stacked loans are four times more likely to be the result of fraudulent activity. Moreover, a 2015 study of fintech lenders found that stacked loans represented $39 million of $497 million in charge-offs.

Although Rianda does not see the situation having far-reaching implications as say the Internet bubble or the mortgage crisis, he does predict a gradual drop off in business among MCA players and a wave of consolidation for these companies.

“I do not believe that the current state of some MCA companies taking stacked positions where there are multiple cash advances on a single merchant is sustainable. Sooner or later the losses will catch up with them,” he says.

Rianda also predicts that the decrease of outside funding to related industries could have a spillover effect on MCA companies, causing some to cut back operations or go out of business. “Some companies have already seen decreased funding in the lending space and subsequent lay off of employees that likely will also occur in the merchant cash advance industry,” he says.

THE REGULATORY QUESTION MARK

One major unknown for the broader funding industry is what regulation will come down the pike and from which entity. The Office of the Comptroller of the Currency that regulates and supervises banks has raised the issue of fintech companies possibly getting a limited purpose charter for non-banks. The OCC also recently announced plans to set up a dedicated “fintech innovation office” early in 2017, with branches in New York, San Francisco and Washington.

There’s also a question of the CFPB’s future role in the alternative funding space. Some industry participants expect the regulator to continue bringing enforcement actions against companies. In September, for instance, it ordered San Francisco-based LendUp to pay $3.63 million for failing to deliver the promised benefits of its loan products. Ullman of Orchard Platform says he expects the agency to continue to play a role in the future of online lending, particularly for lenders targeting sub-prime borrowers.

Meanwhile, some states like California and New York are focusing more efforts on reining in online small business lenders, and it remains to be seen where this trend takes us in 2017.

MORE CONSUMER-FOCUSED INITIATIVES ON HORIZON

As the question of increased regulation looms, some industry watchers expect to see more industry led consumer-focused initiatives, an effort which gained momentum in 2016. A prime example of this is the agreement between OnDeck Capital Inc., Kabbage Inc. and CAN Capital Inc. on a new disclosure box that will display a small-business loan’s pricing in terms of total cost of capital, annual percentage rates, average monthly payment and other metrics. The initiative marked the first collaborative effort of the Innovative Lending Platform Association, a trade group the three firms formed to increase the transparency of the online lending process for small business owners.

Katherine C. Fisher, a partner with Hudson Cook LLP, a law firm based in Hanover, Maryland, that focuses on alternative funding, predicts that more financers will focus on transparency in 2017 for competitive and anticipated regulatory reasons. Particularly with MCA, many merchants don’t understand what it means, yet they are still interested in the product, resulting in a great deal of confusion. Clearing this up will benefit merchants and the providers themselves, Fisher notes. “It can be a competitive advantage to do a better job explaining what the product is,” she says.

CAPITAL-RAISING WILL CONTINUE TO POSE CHALLENGES

CAPITAL-RAISING WILL CONTINUE TO POSE CHALLENGES

Although there have been notable examples of funders getting the financing they need to operate and expand, it’s decidedly harder than it once was. Renton of Lend Academy says that some institutional investors will remain hesitant to fund the industry, given its recent troubles. “It’s a valuation story. While valuations were increasing, it was relatively easy to get funding,” he says. However, industry bellwethers Lending Club and OnDeck are both down dramatically from their highs and concerns about their long-term viability remain.

“Until you get sustained increases in the valuation of those two companies, I think it’s going to be hard for others to raise money,” Renton says.

Several years ago, alternative funders were new to the game and gained a lot of traction, but it remains to be seen whether they can continue to grow profits amid greater competition and the high cost of obtaining capital to fund receivables, according to William Keenan, chief executive of Pango Financial LLC, an alternative funding company for entrepreneurs and small businesses in Wilmington, Delaware.

These companies continue to need investors or retained earnings and for some companies this is going to be increasingly difficult. “How they sustain growth going forward could be a challenge,” he says. Even so, Renton remains bullish on the industry—P2P players especially. “The industry’s confidence has been shaken. There have been a lot of challenges this year. I think many people in the industry are going to be glad to put 2016 to bed and will look with renewed optimism on 2017,” he says.

Prior to this story going to print, small business lender Dealstruck was reportedly not funding new loans and CAN Capital announced that three of the company’s most senior executives had stepped down.

New deBanked Magazine Issue is On The Way

December 7, 2016

The Nov/Dec issue of deBanked magazine is on the way! Can you guess who is on the cover? Hint: his face is blurred out in this image so you can’t cheat!

This edition closes the end of 2016, celebrates the journey of an industry veteran, recaps late fall conferences, and reveals new clues and details into a former industry player’s devilish fall from grace.

Stay on top of the industry and finish out the year with our latest major stories that are released in print well before they’re online. If you’re not already subscribed to deBanked Magazine, register now for FREE!

Shakeup at CAN Capital – CEO and 2 other Execs Put on Leave of Absence

November 29, 2016Update 11/30 7:30 pm: CAN says they are still open for business and still providing access to capital for current customers and renewal business. They are not actively seeking new business at this time, but will evaluate it as it comes in.

CAN Capital has confirmed that CEO Dan DeMeo has gone on a leave of absence. The company’s chief financial officer Aman Verjee and chief risk officer Kenneth Gang have also reportedly stepped down. Parris Sanz, the company’s Chief Legal Officer, has been made acting head of the company, while Ritesh Gupta has been promoted to COO.

A statement from CAN Capital is below:

“As the board and our leadership team conducted our business reviews and looked at how we can best position the firm for future growth, we self-identified that some assets were not performing as expected and that there was a need for process improvements in collections. It became clear that our business has grown and evolved faster than some of our internal processes. As we work to improve these processes, the Board has named twelve-year CAN Capital veteran and senior executive, Parris Sanz acting head of the company and promoted Ritesh Gupta to COO, while Dan DeMeo, CEO, and two other members of his team are on a leave of absence. Over the past 18 years CAN Capital has consistently made decisions to position ourselves for growth and leadership in the industry and we look forward to helping small businesses succeed for many years to come.”

Some of CAN Capital’s referral partners have reported to us that the funding of new deals has been put on hold until January 2017. This could not be confirmed, however. (Update: This was later confirmed)

More than just an industry leader, CAN was founded in 1998 and is widely regarded as the first merchant cash advance company. A year ago, deBanked featured Dan DeMeo and CAN in a story to mark their success. As of April this year, they had funded more than $6 billion since inception. In August, they secured a coveted partnership with Entrepreneur Magazine.

Having secured a $650 million credit facility last year led by Wells Fargo, they are the second largest player in the alternative business finance industry behind OnDeck.

Sanz joined the company in 2004 with more than 12 years of experience as a corporate, securities, and transactional attorney. Before joining CAN Capital, he was a senior executive and General Counsel of a specialty pharmaceutical company, the successful sale of which he led in 2003. Prior to that, Sanz was an attorney in private practice at the law firms of Latham & Watkins in Los Angeles and Paul, Hastings, Janofsky & Walker in San Francisco, where he handled a wide variety of M&A transactions, securities offerings including IPOs, and other corporate transactions, and acted as outside general counsel to a number of technology start-ups.

Sanz received his J.D. from Harvard Law School in 1993 and a Bachelor of Arts degree from U.C. Berkeley, High Honors and Phi Beta Kappa, in 1990. Sanz is admitted to practice in California and Washington, D.C., is a registered In-House Counsel in New York, and is also admitted to practice before the United States Court of Appeals for the Federal Circuit.

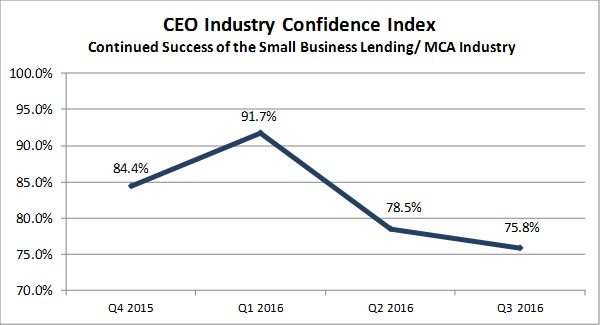

Q3 2016: Confidence in the Small Business Financing Industry’s Success Down Slightly

November 29, 2016Confidence in the industry’s continued success was down among small business financing CEOs in the third quarter, according to the latest survey conducted by Bryant Park Capital and deBanked. At 75.8%, it’s the lowest level recorded since surveying began late last year.

Respondents were not asked the reasoning for their confidence score, but the sentiment may have been influenced by what seemed like an impending Clinton presidency at the time and the 4 more years of regulatory pressure on financial services that would’ve continued as a result. The survey was conducted before the election. Also, the correction taking place in the consumer space with companies like Prosper and Avant have allowed a general feeling of pessimism to waft through the alternative financing universe.

Still, at 75.8%, which is still well into positive territory, the mood is probably best described as cautiously optimistic. The euphoria in Q1 at 91.7%, preceded the resignation of Lending Club’s founder and CEO, which symbolically burst alternative lending’s bubble.

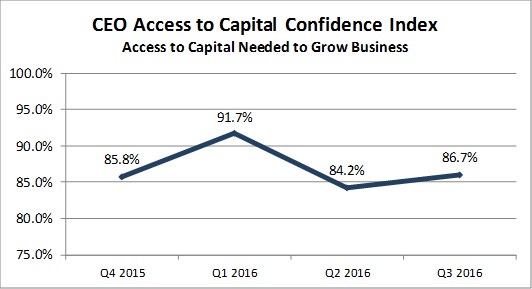

Curiously, industry CEOs were slightly more confident in their ability to access capital needed to grow their business. Respondents were not asked what their capital source options were or the respective costs, but it signals that there are still plenty of investors interested in the space.

Bryant Park Capital and deBanked also produce a comprehensive full-year industry report, available to anyone for $495. To purchase the 2015 report, you can contact me at sean@debanked.com

The History of Alternative Finance (As Told Through Memes)

November 21, 2016Exactly four years ago, I honored the Thanksgiving holiday by slightly exaggerating the industry’s history in a blog post. And every year around this time since, I’ve reposted it to the home page for all the newbies to enjoy. But in 2016, it just doesn’t seem as applicable. Too many things have changed, especially compared to when I first joined the industry.

The technological experience I remember as an underwriter back in 2006 might as well have been the 1700s. From my perspective, here’s how things have changed:

I don’t know about you, but I am afraid to see where we will be in 2026.

Happy Thanksgiving! 🙂

The Remedy For a Bad Industry Decision?

November 9, 2016 A recent disappointing New York trial court decision concerning merchant cash advances has been making the rounds over the past few weeks and a few industry players have been asking if there is cause to be concerned. While the case will likely have little precedential value, it should serve as a reminder to all funders and ISOs in the industry to invest resources where they matter; on employee education, contract review, legal representation, and customer service.

A recent disappointing New York trial court decision concerning merchant cash advances has been making the rounds over the past few weeks and a few industry players have been asking if there is cause to be concerned. While the case will likely have little precedential value, it should serve as a reminder to all funders and ISOs in the industry to invest resources where they matter; on employee education, contract review, legal representation, and customer service.

Failures or breakdowns in these areas can lead to consequential events. With so many products being offered in the marketplace to small business owners today, it is of great importance to be educated on what they all are and how they work. Sales reps, underwriters, and other staff should know what’s in the language of the contracts and be able to articulate it accordingly.

A starting point, of course, is getting your certificate in Merchant Cash Advance Basics, the online tutorial that covers the differences between the purchases of future sales and loans. It is worthwhile even for industry veterans to take considering how much MCAs have evolved over the years.

We’ve also got a list of several industry attorneys on our website, none of whom pay to be there.

Of note for contracts and legal compliance is Hudson Cook, LLP, who actually created the MCA Basics course.

Of note for litigation concerning the validity or enforcement of contracts in New York courts, is Christopher Murray of Giuliano McDonnell and Perrone, LLP, whose experience includes the VIP Limo case and several others.

It helps to have a system in place to try and resolve conflicts with merchants before they escalate. But that job is made far easier when the contractual expectations of all parties is understood from the beginning.

What’s the takeaway from a case that has gone wrong? That you should work hard to do everything right.

Merchant Cash Advances Are Not Loans – Take the Online Course to Learn Why (And Get a Certificate)

November 3, 2016

A New York Supreme Court decision in June was pretty deliberate when it said a purchase of future receivables was not a loan.

Essentially, usury laws are applicable only to loans or forbearances, and if the transaction is not a loan, there can be no usury. As onerous as a repayment requirement may be, it is not usurious if it does not constitute a loan or forbearance. The Agreement was for the purchase of future receivables in return for an upfront payment. The repayment was based upon a percentage of daily receipts, and the period over which such payment would take place was indeterminate. Plaintiff took the risk that there could be no daily receipts, and defendants took the risk that, if receipts were substantially greater than anticipated, repayment of the obligation could occur over an abbreviated period, with the sum over and above the amount advanced being more than 25%. The request for the Court to convert the Agreement to a loan, with interest in excess of 25%, would require unwarranted speculation, and would contradict the explicit terms of the sale of future receivables in accordance with the Merchant Agreement.

Lawyers around the country are pointing to this published decision and other similar ones as becoming the standard rule of law in New York State.

Finally, there are extracurricular steps you can take as a sales rep, underwriter, or other participant in the industry to educate yourself on what it means to buy future receivables at a discount versus a loan.

Finally, there are extracurricular steps you can take as a sales rep, underwriter, or other participant in the industry to educate yourself on what it means to buy future receivables at a discount versus a loan.

A new online course created by law firm Hudson Cook LLP, teaches the basic and unique characteristics of merchant cash advance contracts. New entrants and veterans alike can take the course and corresponding exams to brush up on the core fundamentals of MCA. Those that pass will receive a certificate of completion in “Merchant Cash Advance Basics” that is valid for two years. There are even video tutorials in case you don’t like to read.

Co-produced by deBanked as part of an effort to foster educational standards in the industry, the course just only recently went live. An educated sales force is no doubt integral to the success of the industry and the businesses it serves.

This in no way implies that company in-house training programs are currently insufficient. Instead, companies can use the course to supplement their own in-house training efforts with new hires or to test current employee education levels. More comprehensive versions of the course or new components of it may be developed in the future. We realize this can be evolved to cover more, but for now, it’s the basics.

Can YOU pass MCA Basics?

That’s a copy of my real certificate on the right (shrunken down to fit in this story). I got a perfect score.

Hosted on Counselor Library, you can sign up to purchase the course here.

Update 11/4: Link to the course in the story has been fixed: http://www.counselorlibrary.com/public/courses-mca.cfm