The Broker: How Gerald Watson Mixes Factoring with MCAs

December 3, 2019 Role?

Role?

I’m the owner of The Watson Group, a factoring broker company.

How did you end up in the industry?

I got started in what I call the contract financing industry about 35 years ago, kind of by accident. I had spent years working with a large management consulting company in Boston and we had some major contracts in the DC area. I was on an assignment there and my son was in school there with another kid, and I met the parents and the dad told me what he was doing and he said I needed to come by the offices to check it out.

I really had no intention of going at all, but finally to get this guy off my back, I went by one day and he showed me the business they were in. When I left I was totally on board. I had been working for several years in management consulting, but this was all new and I was excited because it was helping real businesses solve real problems and it was very hands-on.

I came on board and I’ll never forget my first day on the job: I didn’t know anything from anything – rights, factoring, contracts financing – this was years before the MCA industry even existed, and my boss said he just got a job, 911 call from a printer and they needed some funding help. “Can you help them? Why don’t you come ride with me? It’d be good on the job training for you.” And so we sat down with the guy and found a solution for him. And to this day he hasn’t had to close his business.

How were those early days?

Interesting because this was before the internet, almost before cell phones, in fact. I remember at one point when I was being hired, the Motorola flip phone was just coming out and they were like $1,500 around 25 years ago. And I said okay, I’ll take the job but you’ve got to give me one of these Motorola phones, so he did and it was great but this is before the internet and I didn’t really believe in traditional advertising or mailing out brochures, so the strategy I take is called “institutional referral-based marketing.”

In a nutshell, what that is, is working with various institutions that refer clients to use on a regular basis and as part of that process, I’d give talks or seminars and workshops and sit on panels and teach some of these referral groups how to assess deals and package them and get them ready for funding. You know, develop a pretty solid reputation in the industry for what we did and even today we’re 100% referral.

What can you tell me of the style in which you approach deals?

The approach that I’ve always taken is really a diagnostic approach, we kind of almost see ourselves as doctors. If you go to a doctor and you have pain, you may not know what’s causing that pain, you just want to feel better. And so what does the doctor do? They have to understand what’s going on in order to make you feel better.

Client’s got a pain: “I need money. I need working capital and I need it now.” And so we get a clear picture of what their objectives are and what they’re looking to accomplish: how much they need, what they need it for, timing, etc., and like a doctor, we go through a series of diagnostic tests, which can involve getting a list of documents – financials, bank statements, whatever it is – and going through them. You’re drilling down on where they’re at and coming up after that, coming up with what I call a treatment plan or funding strategy.

Here’s the key: you’ve got to ask the right questions, because if you don’t ask the right questions you’ll never get the right answer. All too often what a broker will do is they’ll get right into solutions and answers and talk about why what they offer is the best or why their funder is the best thing since sliced bread without having a picture of what their client’s true needs are in this situation. So I have a whole series of quizzes I’ve done a million times so I don’t need to write them down. I know what they are but I systematically go through ‘em, and we call that a preliminary underwriting interview.

What is the value of combining MCAs and factoring?

Funding solutions typically involve multi-funding products. And that’s where the advent of MCAs came in, and why they’re such a real asset. Because you meet a client today and it’s Wednesday, or Tuesday, hell maybe even Thursday, and the guy’s siting there with half a million dollars in receivables that we can convert into cash but we may need 3 days to do it, but he needs 2 days.

MCAs are a great product because we can step in, solve the problem, get him an immediate injection to stop the bleeding, and take it out from factoring proceeds a few days later. So it’s a great compliment and tool and this is something I’ve tried to educate on both sides. It’s not a threat it’s a complement. The key is how you use it. It’s like two medications. You go to a doctor, they’ll prescribe a list of meds, the key is to make sure they all complement each other.

Any advice for those looking to combine MCAs and factoring?

The first thing you want to do as an ISO who’s interested in developing a factoring brokering business is to understand the basics of factoring: what is factoring, how does it work, how do you qualify, how much does it cost?

The second thing you want to do is look internally to develop your customer base and the quickest customer base is what we call the low-hanging fruit. These are existing merchants that didn’t fund. Any merchant that is in B2B, whether they got funded or not, is a candidate for factoring. So go back through the files, look at the database and you may find out you probably have a lot more than what you ever imagined.

The third is to develop your database of funding resources – of funders.

And the last thing you want to have is a game plan. What’s your game plan and what’s your strategy for moving forward with your factoring broker business?

Broker Fair / Black Friday ONE-DAY ONLY Special Price

November 28, 2019

Broker Fair Returns to New York City on May 18, 2020. Take advantage of this special ONE-DAY only discount code and get 29% OFF THE EARLY BIRD PRICE. This incredible deal ends at 11:59pm EST on 11/29/19.

Broker Fair’s two previous annual events sold out in advance. Hundreds of brokers from the commercial financing, merchant cash advance, and small business lending industries will be in attendance this year. See you at Broker Fair!

Flender Makes BIG Mark in Ireland’s SME Lending Market

November 26, 2019 Ireland can seem like a small place, so much so that on my way to meeting with Colin Canny, Flender’s Head of Partnerships, I quite literally bumped into Flender’s co-founder & CEO Kristjan Koik who was walking through Dublin’s Silicon Docks. I recognized Koik from the who’s who catalogue of executives I had compiled before traveling abroad to explore the Irish fintech scene. He was cordial and polite. And yet through his demeanor I sensed there was more, that there was a story to be told even if it was not ready to be shared.

Ireland can seem like a small place, so much so that on my way to meeting with Colin Canny, Flender’s Head of Partnerships, I quite literally bumped into Flender’s co-founder & CEO Kristjan Koik who was walking through Dublin’s Silicon Docks. I recognized Koik from the who’s who catalogue of executives I had compiled before traveling abroad to explore the Irish fintech scene. He was cordial and polite. And yet through his demeanor I sensed there was more, that there was a story to be told even if it was not ready to be shared.

The following month Flender would reveal remarkable news, a new €75 million funding line, bringing their total to €109 million raised since the company’s founding in 2015. The company is backed by Eiffel Investment Group, Enterprise Ireland, entrepreneur Mark Roden and former Ireland rugby player Jamie Heaslip.

This large amount of funding, even by UK or US standards, makes Flender stand out, and so when I finally meet with Canny on that warm Fall day in September, I’m pretty thankful he afforded me the time.

Flender, Canny explains, is derived from Flexible Lender. The pamphlet he produces and hands to me says that their idea is simple, to provide businesses with the funding they need and ensure the application process is fast, easy, and transparent.

Application details for products like term loans and merchant cash advances require the usual stips like historical bank statements, a profit & loss statement, and a balance sheet. But there’s also a section quintessentially Irish, that is that it can be beneficial to submit your last 2 years herd numbers if you’re a farmer, complete with your last 12 months Milk Reports and property acreage figure.

Canny explains that Flender is not a high-risk fall-back lender, but rather the opposite. “Our credit process is extremely tight,” he says, “in line with banks.” And with good rationale, seeing that the company is still somewhat reliant on a peer-to-peer funding model. More than half of individual peers on the platform are Irish but Canny says that it’s not unusual for non-residents including Americans to lend on the platform as well.

Canny explains that Flender is not a high-risk fall-back lender, but rather the opposite. “Our credit process is extremely tight,” he says, “in line with banks.” And with good rationale, seeing that the company is still somewhat reliant on a peer-to-peer funding model. More than half of individual peers on the platform are Irish but Canny says that it’s not unusual for non-residents including Americans to lend on the platform as well.

Canny says the Irish market is very “community based.” The transparency of the marketplace aligns with that characterization. Like other peer-to-peer small business lenders in Ireland, borrower identity is publicly accessible on the platform, as are the terms of the loan. Anyone can view the business name of a prospective borrower on the website, the address, a bio, and even their “story.”

Flender taps several marketing channels like Google Adwords, radio, direct sales, and even brokers. Canny says they generate an underwriting decision in as quick as 4-6 hours and fund a business in as little as 24 hours. Borrowers like the product so much that many renew. Seventy percent of the SMEs in the country are peer-to-peer bankable, Canny explains, creating a wide playing field to target.

Meawnwhile, CEO Kristjan Koik told the Irish Times that the top 3 banks in Ireland have 92 percent of the SME lending marketshare so there is still a ton of opportunity for non-banks like Flender to grab hold of.

As for how the massive credit line impacts them going forward? Koik told the Times that they would be cutting interest rates by up to 1 percent across their various loan products. Interest rates now start as low as 6.45% and terms range up to 36 months.

As Canny and I part ways I present one final question, will Flender be expanding abroad? I get no definitive answer. He was cordial and polite, and yet I sensed through his demeanor that there was more, perhaps even a story in the works that was not yet ready to be shared.

Merchant Cash Advance Valuation Dynamics

November 20, 2019Understanding the differences in cashflow dynamics between small business loans and MCAs is crucial for investors when valuing these alternative investments. A small business loan usually has familiar terms such as a principal amount that is paid back with interest over time, typically with a monthly payment schedule. An MCA agreement does not have these terms. Instead, the merchant agrees to sell a certain percentage of future revenues generated by the business, up to a specified “Purchased Amount,” to the funder in exchange for a lump sum of cash (the “Funded Amount”). MCAs often have an initially agreed-upon dollar amount that is debited daily by the funder via ACH. However, merchants have the ability to reconcile the total debited at the end of each month based on their actual sales activity and the agreed-upon percentage. If the merchant’s sales are slower than projected, the MCA company owes the merchant back a portion of the month’s debits to be in line with the contractual percentage of sales, and the daily ACH amount may be adjusted.

The preferred approach for valuing MCAs is discounted cashflow analysis. Given the nuances of MCA cash flow dynamics, modeling should be done individually for each MCA. Projections should be modeled using assumptions that are supportable from historical data and the methodologies used should be transparent. This modeling should incorporate not only the cash flow from the merchant, but also the cash flows arising from deal mechanics such as commissions paid, origination fees and ongoing fees as well as expected charge-offs. Since the funder cannot know for certain which merchants will realize revenues higher or lower than projected or default when underwriting the MCA, any attempt at an accurate projection of future cash flows must incorporate probabilities for scenarios where the timing and amount of cash flows is different than the underwritten scenario. Because businesses in a particular sector may have similar historical cash flow behavior, each MCA should be analyzed based on the historical experience of MCAs with similar characteristics such as business type, advance amount and purpose for taking out the MCA. A smaller but related issue is incorporating the probability that the merchant chooses to pay off the Purchased Amount via a lump sum payment and negotiates a discount to the Purchased Amount.

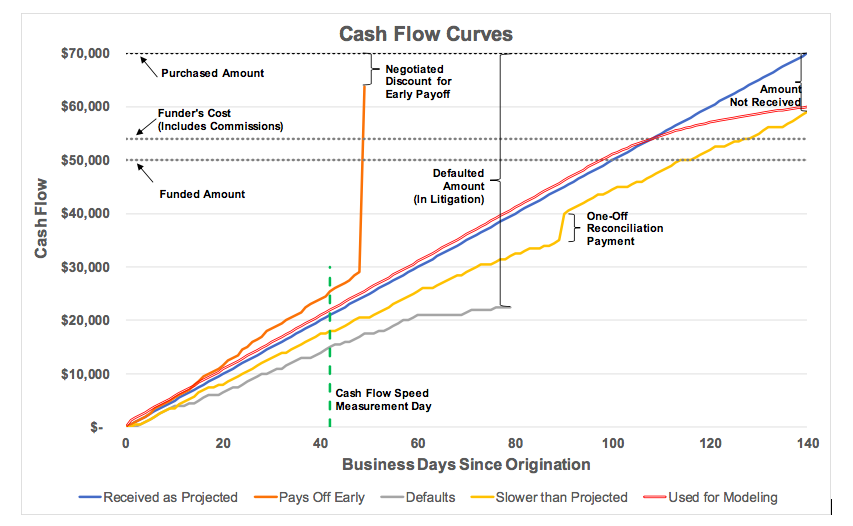

Examining payment behavior involves creating payment curves that compare the cash flow received at each point in time, expressed as a percentage of the Purchased Amount, to the cash flow projected to have been received at that time during underwriting. This curve is the “Cash Flow Curve,” and its steepness is the “Cash Flow Speed.” More specifically, the Cash Flow Speed is the cash flow received to date divided by the cash flow projected to be received as of that date during underwriting. A perfectly underwritten MCA would be one on which no reconciliations are made and each daily ACH goes through without issues, meaning that all of the Purchased Amount was received exactly as originally projected, and its Cash Flow Speed would be 100.0% every day. As with most things, this does not work in practice like it does in theory. Some merchants will have ACHs which fail, make additional payments to make up for failed ACHs, renegotiate the daily ACH amount as part of a reconciliation or after a failed ACH, turn off ACH completely or have other issues. Analyzing the Cash Flow Curve for each MCA and comparing it to its cohort is essential to understanding performance drivers when projecting future cash flows.

To illustrate a possible MCA agreement, assume a merchant sells $70,000 of future sales (the Purchased Amount) to the funder for $50,000 (the Funded Amount). The Purchased Amount is to be received via ACH daily, with $500 debited per day for the next 140 business days based on projected revenues. In this example, the Gross Factor is 1.40, i.e. $70,000 divided by $50,000. Assuming that the funder pays a commission of 8% of the Funded Amount, the Funder’s Cost is $54,000, and the Net Factor is 1.30, i.e. $70,000 divided by $54,000. The graph below illustrates some possibilities of what the actual Cash Flow Curves might be.

Received as Projected: depicts an MCA where debits via ACH are received each day, and the ACH is unchanged until the full Purchased Amount is received. Its Cash Flow Speed at the measurement day (and every day) is 100.0%.

Pays Off Early: depicts an MCA where the merchant elects to send additional cash flow to the funder, eventually negotiating to pay off the MCA early after 49 business days with a discount to the Purchased Amount negotiated with the funder. Its Cash Flow Speed at the measurement day is 121.4%.

Defaults: depicts and MCA where the ACH debit fails with increasing frequency until the bank account is closed and the funder takes the merchant into litigation for the remaining Purchased Amount (the “Defaulted Amount”). Note that the funder may be entitled to recoup amounts beyond the Defaulted Amount in litigation. Its Cash Flow Speed at the measurement day is 71.4%.

Slower than Projected: depicts an MCA where ACH fails sometimes, but the merchant does not shut down and the funder receives cash flow slower than projected. An example of a one-off reconciliation payment is included, assuming the merchant had not been paying in accordance with the contract and agreed to make a “catch-up” payment. After 140 days only $59,000, or 84.3% of the $70,000 Purchased Amount, has been received, although the funder would likely still expect to recoup most or all of the remaining Purchased Amount. Its Cash Flow Speed at the measurement day is 85.7%.

Used for Modeling: When analyzing this MCA on day 0, before any cash flow behavior is known, each of these possibilities (as well as others) would be incorporated into the analysis on a probability-weighted basis. An example of a probability-weighted average Cash Flow Curve is shown. After 140 days 85.7% of the Purchased Amount has been received, although cash flow is assumed to continue to be received until 210 days (150% of the underwritten projection), with 90.3% of the Purchased Amount received by then. Its Cash Flow Speed at the measurement day is 104.6%.

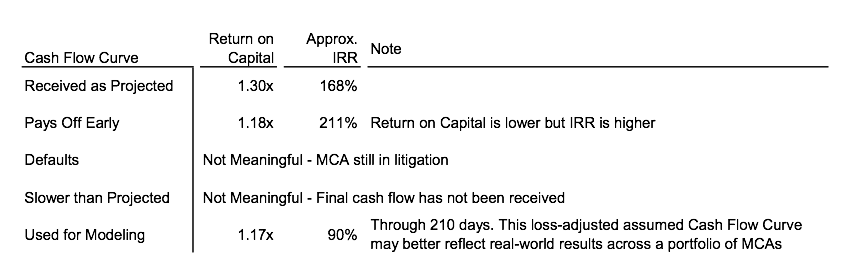

Based on the Funder’s Cost, the chart below shows some return metrics based on these Cash Flow Curves.

As the industry matures and attracts more capital from institutional investors, it is increasingly important to have clearly defined metrics in place to evaluate underwriting effectiveness, assess relative credit performance of originators or cohorts of MCAs, and to perform valuations. Standardizing on terms such as Funded Amount, Purchased Amount, Gross Factor, and Net Factor and concepts such as Cash Flow Curve and Cash Flow Speed should ease the understanding of MCAs by eliminating ambiguity amongst various participants in the industry.

Merchant Infamous For Safari-Themed Home, Has Died

November 18, 2019 The saga of Michael Willhoit has come to an end. deBanked wrote about Willhoit in December 2018 when we learned he defaulted on nearly half a million dollars in merchant cash advance transactions and was sued by banks over $4.5 million in bad loan deals. This past June he was also indicted on 36 counts of bank fraud.

The saga of Michael Willhoit has come to an end. deBanked wrote about Willhoit in December 2018 when we learned he defaulted on nearly half a million dollars in merchant cash advance transactions and was sued by banks over $4.5 million in bad loan deals. This past June he was also indicted on 36 counts of bank fraud.

But on Sunday, Willhoit passed away of natural causes, the Springfield News-Leader reported. He was 66.

Willhoit’s local notoriety gained somewhat national interest thanks to his fully-customized multimillion dollar safari-themed home, dubbed “The African Queen.” Willhoit told a News-Leader reporter in 2016 that he spent $3 million renovating the Sprinfield, MO property including $400,000 for a 900-square-foot wood floor and $300,000 for landscaping. Other notable items on the property included:

- Two roaring lion masks

- Two 7-foot tall hand-carved wooden tusks

- An eight-legged genuine impala horn zebra-hide chair

- A 15-foot African warrior statue

- A 3,000-pound (approximately) bronze rhino

- Four gazelle taxidermy mounts

- A baboon, full-body mount

Willhoit’s criminal trial was scheduled for July 2020.

You can still view a virtual video tour of his home below:

For ISOs Only — How To Develop Your Factoring Brokerage Business (Part 1)

November 17, 2019 Let me ask you a question; If you were walking down the street and saw a $100 bill on the sidewalk, would you stop and pick it up? Of course you would, unless you didn’t see it. Or would you say, “I’m in a hurry and it’s ONLY $100. I’ll make a lot more money on that big MCA deal I’m heading into the office to work on, so I’ll just leave it on the sidewalk.” Really?!

Let me ask you a question; If you were walking down the street and saw a $100 bill on the sidewalk, would you stop and pick it up? Of course you would, unless you didn’t see it. Or would you say, “I’m in a hurry and it’s ONLY $100. I’ll make a lot more money on that big MCA deal I’m heading into the office to work on, so I’ll just leave it on the sidewalk.” Really?!

Well, Here’s a rude awakening. For any of you who haven’t added Factoring to your financing product mix, that’s EXACTLY what you’re doing RIGHT NOW! And get this, you’re doing it with some of the SAME merchants you’re doing deals with RIGHT NOW! Here’s why; A percentage of your merchants sell Business-To Business (B2B), and get paid in 30 to 45 days, and in some cases, even longer.

Many of these are the SAME merchants who come to YOU for an advance to help cash-flow due to delayed invoice payments, so you provide an MCA, right? Right! That’s what we do. But here’s the problem: Next month they come back again, and then again, and then sometimes they get wise, secure another position somewhere else, and before long, well, we all know the story. After all that, while the last advance may have solved their immediate problem, they will ALWAYS have a continuing and on-going need for cash because they’re ALWAYS waiting to get paid. And the FASTER they grow, the BIGGER the problem! Sound familiar?

So, what does that tell us? In most cases, while an MCA may help stop the bleeding, it’s not designed to heal the wound. More specifically, the “wound” that needs to be healed is the un-predictable timing of customer payments on outstanding invoices. So while an MCA provides immediate relief, factoring solves the timing problem. Here’s how it works: The factoring funder provides an advance against approved invoices, typically 70% to 90%. Once the invoice is paid, the funder deducts the advance, along with their fee, and wires the balance to the merchant. So the advance essentially pays itself off, working much like a revolving Line of Credit (LOC). In other words, no payments! The term I use to describe this is called Self-Liquidating.

Here’s how I see it: when structured properly, factoring and MCAs can often complement each other and work well together. Factoring provides predictable cash flow because advances are based on predictable billings to their customers, whether it be monthly, weekly, or even daily. The predictable cash-flow from factoring advances is what the merchant can rely on to cover their continuing and on-going business expenses, i.e. payroll, materials, etc. MCAs can also be used to provide a lump sum injection to cover interim cash needs on a short-term basis, while factoring is being put in place.

Here’s how I see it: when structured properly, factoring and MCAs can often complement each other and work well together. Factoring provides predictable cash flow because advances are based on predictable billings to their customers, whether it be monthly, weekly, or even daily. The predictable cash-flow from factoring advances is what the merchant can rely on to cover their continuing and on-going business expenses, i.e. payroll, materials, etc. MCAs can also be used to provide a lump sum injection to cover interim cash needs on a short-term basis, while factoring is being put in place.

Here’s an actual example of a real client situation we recently funded using this approach. Client is a large importer of Spanish wines selling to one of the largest spirits distributors in the country. They typically get paid in 45 to 60 days, so we established a factoring facility, which would take about a week. However, they had a container from Spain that needed to be paid for and shipped IMMEDIATELY to help fill holiday orders. We secured an MCA to pay for the container and negotiated an aggressive early pay-off discount. Once the factoring LOC was in place, the MCA was satisfied using a portion of the proceeds from the first factoring advance. We are now putting a purchase order funding facility in place to cover the upfront costs on all future container shipments from overseas.

This combined approach, enables YOU to provide FUNDING SOLUTIONS for your merchants, much like Ed McKinley described in the September/October, 2019 issue of deBanked Magazine where he talks about Consultative Selling. A true professional focuses on solving financing problems and building a relationship with their merchants, versus simply funding a transaction. You then have the opportunity of becoming a “trusted financing resource” versus a broker simply interested in what I call “hit and run” selling. In addition, this approach can have a multiplier effect on your income, enabling you to get paid on a continuing and on-going basis.

Speaking of getting paid, you may ask, “So how much money can I make with factoring?”

I’m so glad you asked that question. Maybe now is a good time to introduce myself. For over the past 25 years, I have specialized in arranging factoring/PO and contract financing for hundreds of growing business owners all over the country, providing millions of dollars in financing. Over the years I have earned in excess of a seven-figure income, primarily as a broker. I’m sharing this information with you to make a point; there’s a LOT of money which YOU can make too with factoring, IN ADDITION TO what you’re already making with MCAs.

So, then you say, “Well that’s great for you Watson, but how much money can I make?” Good question. Let’s take a look at how it’s structured. With factoring, you’re paid by the funder, just like an MCA. Two major differences. The first is that broker commissions for factoring typically range between 10% to 15% of the fee income earned by the funder per month. Fee income is earned once the outstanding funded invoices have been paid by the merchant’s customers. Broker commissions are then paid by the funder the following month. As an example, if the fee income earned by the funder was, say, $10,000 per merchant, per month, you would be paid $1,000 to $1,500 per merchant, per month. Ten merchants would pay you $10,000 to $15,000 per month and so on. Broker commissions will continue to be paid for the life of the factoring relationship and provide you with residual income, or what many refer to as, mail-box money, because it’s actually like getting a renewal every month from the same merchants, and you don’t even have to get out of bed!

A second source of income which is OPTIONAL, is to establish a fee agreement with the client to pay a success fee or origination fee based on the size of the facility. It is a one-time fee paid at closing and funding, either from the first factoring advance or over several advances based on what you work out with your merchant. Success fees are much like points in a closing on a real estate loan and typically range from 1% to 5% of the facility size. The fee is paid to you directly by your merchant once they have been funded. It is designed to provide you with IMMEDIATE INCOME. As an example, a $250,000 facility at 2% will pay you $5,000 or $10,000 at 4%. And that’s just for one merchant. How many could you do per month? For large contracts, we’ve established factoring facilities up to $5 million. I’ll let you do the math to see the potential.

Combining these two income streams can potentially provide a significant increase to your existing MCA income base, and in some cases from your EXISTING book of merchants. These are what we refer to as the low hanging fruit. They include your construction contractors, service and supply companies, transportation, manufacturing, medical and professional services firms, or anyone else who invoices B2B. Some retail merchants also sell B2B, while others, like restaurants, may have catering contracts. Take a look through your files. For many of these merchants you are already asking for A/R Aging Schedules as a stip, right? Now that aging schedule takes on a whole new meaning! And if they’re not factoring now, my friends, THAT’s the $100 bill you “didn’t see” laying on the street, and potentially THOUSANDS more you are leaving on the table! To be sure, close the MCA they need right now, make the money, and set them up with Phase II by establishing a factoring facility on their behalf. Then continue to provide MCAs as needed to cover unexpected problems or take advantage of opportunities. Make sense?

The next article will be what I call Factoring 101 and will focus on 4 major areas: (1) What is Factoring? (2) How does it work? (3) What are the costs? and (4) How do you qualify? We will also talk about identifying and selecting potential factoring funders, HOW TO deal with UCC filing issues, Subordination Agreements, and Fee Agreements with your merchants. We will also touch on Purchase Order Funding as well.

The last article will be designed to bring it all together and talk about HOW TO establish a game plan and options for getting started with your factoring brokerage business and a few key tips on maximizing success in the business.

Clearbanc Offering Funding to Combat US-China Tariff Costs

November 16, 2019 Clearbanc, the Toronto-based funding company co-founded by Dragons’ Den’s Michele Romanow, has announced this month that it will be expanding its funding options to support those small businesses who need assistance purchasing inventory from Chinese suppliers.

Clearbanc, the Toronto-based funding company co-founded by Dragons’ Den’s Michele Romanow, has announced this month that it will be expanding its funding options to support those small businesses who need assistance purchasing inventory from Chinese suppliers.

Specializing in funding businesses who require capital for digital adverts, the Canadian firm decided to expand its offerings after Chinese suppliers started to require inventory payments upfront as a response to the pressure caused by President Trump’s trade war with China. “This isn’t really about the tariffs,” explained Romanow. “This is really about the fact that now all of the Chinese suppliers, because of the uncertainty, are asking for upfront payments for inventory.”

With the Black Friday-Cyber Monday weekend approaching, vendors are looking to be as well stocked as possible, especially when estimates are saying shoppers will spend more than $136 billion in Q4 2019. Most notably affected will be those merchants who deal in electronics. And with worries of the spending extravaganza weekend being affected by the tariffs having persisted for months, Clearbanc is aiming to step in and soothe some of the uncertainty.

With the Black Friday-Cyber Monday weekend approaching, vendors are looking to be as well stocked as possible, especially when estimates are saying shoppers will spend more than $136 billion in Q4 2019. Most notably affected will be those merchants who deal in electronics. And with worries of the spending extravaganza weekend being affected by the tariffs having persisted for months, Clearbanc is aiming to step in and soothe some of the uncertainty.

Not being limited to goods coming from China, funding is also available to all businesses looking to secure capital for inventory purposes, regardless of the supplier’s location; with a charge of 9% of the total amount funded, and funds available being between $10,000 and $10 million.

Speaking on the company’s strategy, Romanow had to say that “every political change can certainly breed new business, but these are all fairly new so we’re just listening and figuring out what our founders are looking for.”

“Predatory Lenders” Slammed as Bill to Ban Confessions of Judgment Nationwide Advances

November 14, 2019

(Bloomberg is majority owner of Bloomberg News parent Bloomberg LP)

Rep. Nydia Velázquez (D) celebrated the advancement of a bill on Thursday that aims to outlaw confessions of judgment (COJs) in commercial finance transactions nationwide. HR 3490, dubbed the Small Business Lending Fairness Act, made its way through the House Financial Services Committee on a vote of 31-23. The next step will be a floor vote.

Velázquez made direct references to a Bloomberg News story series published last year about “predatory lending” and a NY Times article about Taxi medallion loans as her basis for supporting it. Velázquez said that New York had become a breeding ground for “con artists” that relied on COJs to prey on mom-and-pop businesses. The congresswoman singled out New York because of recent taxi medallion loan outrage and the state’s alleged reputation as a “clearing house” for obtaining fast easy judgments against debtors nationwide. New York took a major step to change that practice earlier this year through a new law that only allows COJs to be filed in the state against New York residents. HR 3490 seeks to prevent them from being filed in every state, including New York.

Ironically then, the bill is at odds with the new New York law in that Velázquez’s bill, if it became federal law, would go so far as to prevent New York’s own courts from entering a COJ against New York’s own residents, if it resulted from a commercial finance transaction.

Ironically then, the bill is at odds with the new New York law in that Velázquez’s bill, if it became federal law, would go so far as to prevent New York’s own courts from entering a COJ against New York’s own residents, if it resulted from a commercial finance transaction.

While momentum in the House could be perceived as a partisan initiative unlikely to survive the Senate, the bill has in fact garnered a degree of Republican support, recently through Rep. Roger W. Marshall, a co-sponsor of the bill, and originally by Senator Marco Rubio who initially sparked the call to action in the Senate last year.

The Financial Svcs Committee approved my bill to end "Confessions of Judgment", contracts that allow for unfair, predatory small business loans & that have been linked to #taximedallion crisis in NYC.

On to the House floor!

Read More: https://t.co/xHaYnLKme4@NYTW @FSCDems

— Rep. Nydia Velazquez (@NydiaVelazquez) November 14, 2019

A co-author of the COJ-centric Bloomberg News stories was quick to take the credit for the advancement of Velázquez’s bill.

the bill was drafted in response to our series Sign Here to Lose Everythinghttps://t.co/lrfIW3P0yi

— Zeke Faux (@ZekeFaux) November 14, 2019