Loans

CFPB (and others) Not Amused By Quicken’s Push-Button Mortgage Ad

February 9, 2016Is Quicken in the right place at the wrong time?

Imagine a world where you could get a mortgage at the push of a button. And then imagine like literally pushing that button while you’re sitting in a dark auditorium watching a magic show. As the magician saws a woman in half, you agree to a $400,000 loan payable over 30 years. That pivotal moment, according to Quicken’s vision for American prosperity, will lead to a “tidal wave of ownership” that will flood the country with new home owners.

Consider the implications of that commercial on its own merits (or watch it below of course) and then imagine watching it after you’ve just seen The Big Short in theaters. Given that the movie is a true story about the build-up of the housing and credit bubble in the 2000s that led to a near catastrophic global collapse, a mortgage “tidal wave” might not be the best way to describe your new mobile app.

After Quicken’s push-button mortgage commercial aired during the Super Bowl, the Consumer Financial Protection Bureau responded on twitter:

When it comes to #mortgages, take your time, ask questions and #knowbeforeyouowe. https://t.co/UUaGyWDbzk

— consumerfinance.gov (@CFPB) February 8, 2016

While the mortgage process shown on TV looked overly ambitious, a Quicken customer service rep who I chatted with while posing as a borrower, said that it really can be all done online, even if the mortgage was for like $600,000. When I inquired about what documents I’d need to provide through that process, I was told all I needed to do was state the address of the home.

A no-doc process?

According to the Wall Street Journal, “borrowers can authorize Quicken to access their bank and other financial information directly, eliminating the need for sending pay stubs, bank statements and tax returns back and forth.” So there’s still documents, they’re just electronic and retrieved via APIs.

Having scanned the process, there is clearly more than just one button to push (I counted 9 steps), but it may actually be possible to get a mortgage while watching a magic show. Apparently a lot of people on twitter don’t think that’s a good thing:

Thanks Rocket Mortgage for thinking the '08 housing crisis needed a sequel

— Wyatt Rasmussen (@Wyatt_Rasmussen) February 8, 2016

Let's start another financial collapse. #RocketMortgage https://t.co/7CkBTGJRPD

— Turney Duff (@turneyduff) February 8, 2016

My kid was playing with my phone and bought 7 houses. I can return those right? #RocketMortgage #SB50

— Tim Murphy (@TimMurphy104) February 8, 2016

Rocket Mortgage: explaining the 2008 financial crisis in one commercial

— Rahul Vedantam (@RahulVedantam) February 8, 2016

This commercial is making an excellent case for a massive real estate bubble. It worked awesome in 2007. #RocketMortgage

— Ben Shapiro (@benshapiro) February 8, 2016

Meanwhile, Rana Foroohar, Assistant Managing Editor and Columnist for Time and Global Economic Analyst for CNN, argued that the backlash is unfounded. “No, the Rocket Mortgage Ad Is Not the Sign of Another Financial Apocalypse,” was the headline of her Time story published on Monday. Her evidence? Nobody can afford a mortgage anyway so there’s nothing to worry about, she basically says.

Private equity firm Blackstone has become the largest buyer of single family homes in the country over the last few years. […] Most ordinary Americans need mortgages to buy real estate; at current housing prices and incomes, it would take a typical family more than twenty years to save even a 10% down payment for a home plus closing costs. But they can’t get the loans, because in our post-crisis world, banks are still keeping credit tighter than usual. Besides, many individuals simply don’t have the secure employment, nest egg, and increasingly high credit scores needed to obtain a mortgage these days.

– Rana Foroohar

http://time.com/4212259/rocket-mortgage-super-bowl-ad/

See? There can’t be a bubble brewing because nobody can possibly qualify.

So when Quicken makes wildly provocative sales pitches like this:

Push Button. Get Mortgage. https://t.co/UzOXYFF25C#RocketMortgage 🚀🚀🚀

— Quicken Loans (@QuickenLoans) February 8, 2016

What they’re really apparently trying to say is that the process for those that qualify is supposedly more transparent and therefore better for borrowers:

.@CFPB We agree. No better way than #RocketMortgage for full transparency into mortgage options & info needed to make the right decision.

— Quicken Loans (@QuickenLoans) February 8, 2016

Of course, it probably doesn’t help when their legal help page is titled “legal mumbo jumbo.”

Quicken CEO Bill Emerson tried to clarify the message of the commercial to the WSJ. “What we’re saying is that a strong housing market filled with responsible homeowners is important to the economy,” he said.

Don’t worry about the mumbo jumbo folks, just push button, get mortgage.

—

What do you think? Is Quicken walking down a slippery slope?

Bernie Sanders Poses Bad Lending Question

December 27, 2015Two loans: one with collateral, the other without any. All else being the same, which one do you think would have the higher interest rate?

Given his tweet, Socialist (Democrat) candidate Bernie Sanders might not understand the question.

You have families out there paying 6, 8, 10 percent on student debt but you can refinance your homes at 3 percent. What sense is that?

— Bernie Sanders (@SenSanders) December 26, 2015

The twitterverse was quick to pounce on him for it:

@SenSanders I like you but you have to understand collateralized debt

— Greg Wissinger (@gwiss) December 26, 2015

@SenSanders

A bank can repossess a house. They can't repossess your brain if you quit paying student loans. Though, you make me wonder.

— Smittie (@smittie61984) December 26, 2015

@SenSanders Collateralized vs non collateralized loan. But you knew that already.

— enargins (Neil) (@enargins) December 26, 2015

@SenSanders it makes perfect sense. A 'home' is collateral which the bank can take possession of in case of default. m/t @KurtSchlichter

— All-American Male (@chrisbraly) December 26, 2015

@SenSanders astonishing how you can run president and not understand this basic understanding of collateral.

— Wittorical (@Wittorical) December 26, 2015

@SenSanders I'm generally on your side, but mortgages are secured debt whereas student loans are unsecured and don't always increase income.

— Don Edwards (@DMEdwards) December 26, 2015

@SenSanders wow, big display of stupidity here. The house has resale value. Can we sell people now if they don't pay?

— Ms. Parker (@CaseyParksIt) December 26, 2015

To be fair, student loans might be unsecured debt but they can’t be discharged in bankruptcy. There’s also ways for debt collectors to garnish a paycheck to pay them back. That’s entirely dependent on the borrower generating income though and likely means a substantially longer repayment period. In a famous op-ed by Lee Siegel in the NY Times titled, Why I Defaulted on My Student Loans however, it is apparently possible to just avoid the debt altogether (and apparently feel okay about it).

With stories like that it’s easy to understand why a loan secured by a home would cost less than a loan secured by someone’s willingness and ability to pay. And in the case of Bernie Sanders, a candidate who believes college should be free for everyone, it’s tough to say if his question was really just rhetoric meant to stir up his base or a serious one in which he really doesn’t understand how the underwriting of loans work.

Either way, many people are worried:

.@SenSanders doesn't understand why having collateral would account for a lower interest rate. And people want to make him president?

— Caleb Cassel (@CalebCassel) December 27, 2015

Debt Settlement: A Partner to Alternative Lenders?

August 23, 2015 Call it the flip side of the coin, the part of the universe that helps consumers get out of debt, rather than take more on. Debt settlement, as it’s called, has a bit of a murky reputation thanks to a number of unscrupulous players that operated prior to the implementation of the Telemarketing Sales Rule in 2010.

Call it the flip side of the coin, the part of the universe that helps consumers get out of debt, rather than take more on. Debt settlement, as it’s called, has a bit of a murky reputation thanks to a number of unscrupulous players that operated prior to the implementation of the Telemarketing Sales Rule in 2010.

On October 27th, five years ago, for-profit companies that sold debt relief services over the phone could no longer charge a fee before they settled or reduced a customer’s unsecured debt.

“That law forever changed the industry for the better,” said a company representative at National Debt Relief (NDR), a New York City-based debt settlement firm.

Located right in front of the Bull at 11 Broadway, NDR occupies two floors and employs over four hundred people. And while it may seem that their business model is at odds with the dozens of loan brokers that operate in the neighborhood, they’re actually finding ways to work together.

“We’re monetizing their declines,” said a company representative. Indeed, alternative lenders like to talk about the amount of loans they can issue, but thousands of consumers are ultimately declined.

What those consumers do next and where they go is a storyline that doesn’t get much attention. NDR offers to the consumer an alternative route to become debt free in 36 months.

“NDR is enrolling thousands of consumers per month,” said a company representative. The A+ BBB rating and firm regulatory compliance has enabled them to land several strategic partnerships in this industry ranging from merchant cash advance com- panies to peer-to-peer lenders.

“NDR is enrolling thousands of consumers per month,” said a company representative. The A+ BBB rating and firm regulatory compliance has enabled them to land several strategic partnerships in this industry ranging from merchant cash advance com- panies to peer-to-peer lenders.

“We’ve found that 36% of declines from alternative lenders fit our criteria,” said a company representative. Too much debt is one obvious reason that applicants are getting declined from some of these companies in the first place. And to that end, NDR strives to provide them relief. One condition however is that the client not use credit while in the program.

NDR operates in 42 states and requires a minimum of $10,000 of unsecured debt to be eligible. They are also an accredited member of the American Fair Credit Council, a consumer credit advocacy association that touts the strictest code of conduct in the industry.

At the 2015 LendIt Conference in NYC, NDR stood out as a Gold Sponsor.

“Everybody wanted to know what we did,” said Michael Drehwing who was there as the company’s representative. “I told them we want to monetize your declines. How simple is that?”

Search Engine Lead Generation Is Probably Rigged

March 21, 2015 Hoping to do some nifty SEO to boost your site to the top of search results for valuable keywords? Don’t bother. In August, 2014, I presented six signs that alternative lending is rigged, at least as far as search was concerned.

Hoping to do some nifty SEO to boost your site to the top of search results for valuable keywords? Don’t bother. In August, 2014, I presented six signs that alternative lending is rigged, at least as far as search was concerned.

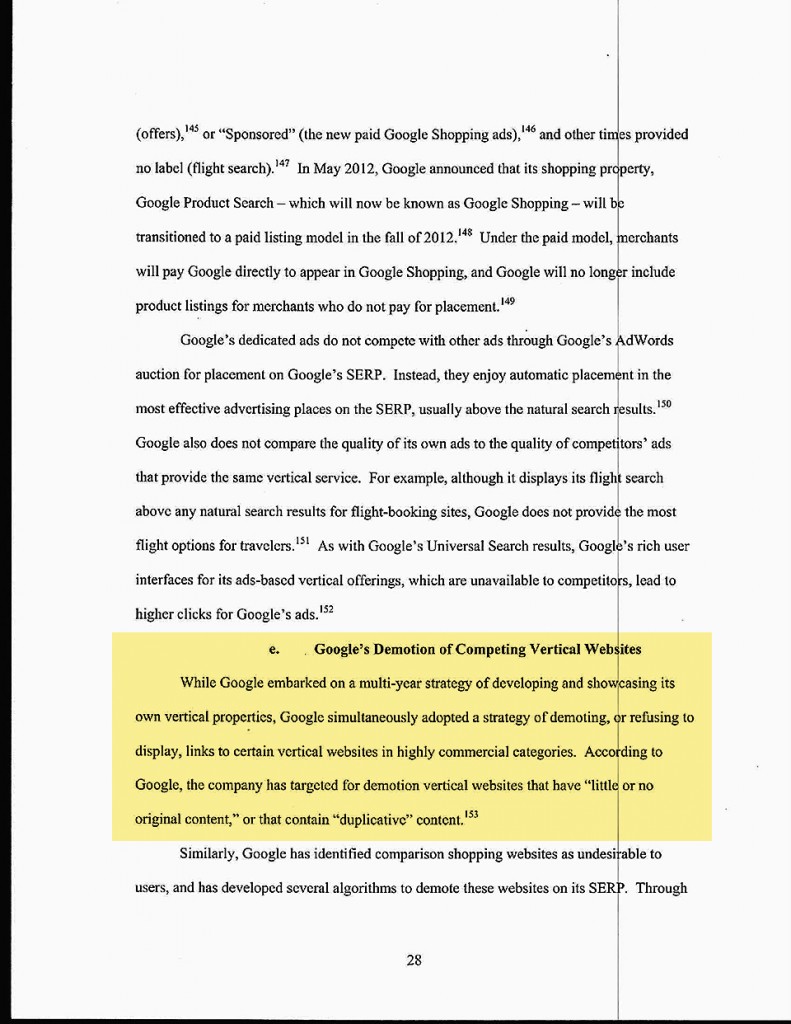

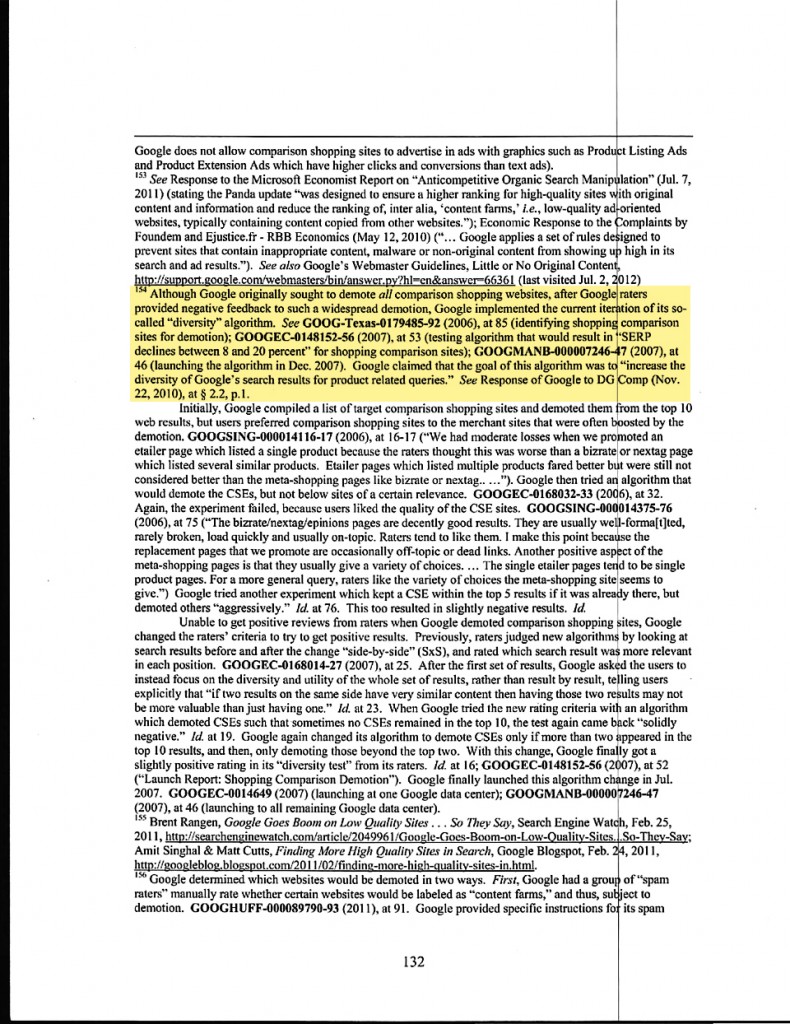

Two days ago, the Wall Street Journal ran a story that exposed a confidential FTC report on Google. The article opens with, “Officials at the Federal Trade Commission concluded in 2012 that Google Inc. used anticompetitive tactics and abused its monopoly power in ways that harmed Internet users and rivals, a far harsher analysis of Google’s business than was previously known.”

The conclusion? Google indeed skewed search results to favor its own services.

The 160 page report that the WSJ draws its analysis from was not supposed to be made public. Only a handful of pages are presented on the WSJ’s website in their entirety. Below are two of them:

Though I cannot find the specific comment anymore on LinkedIn, one of the responses I received on my August post regarding Google’s search results came from a former Google employee. They informed me that my suspicion was preposterous and that Google would never ever manipulate results.

While I made no effort to assert my evidence as anything more than circumstantial, the outright dominance of Google-owned lending companies for high value lending keywords was impossible to ignore. The WSJ story adds fuel to this fire.

Admittedly, the WSJ story doesn’t mention lending, nor do I think lending keywords were a subject of the FTC report (There are 156 pages the WSJ didn’t share). What I think is compelling here is a conclusion that Google did indeed manipulate results and penalized competitors to favor its own financial goals.

Despite the findings, the FTC ultimately did not bring any action against Google.

Is the game rigged? I feel a little bit better about saying, yes. Don’t put all your eggs in the SEO basket.

More Red for OnDeck (ONDK)

February 24, 2015 Back in the red?

Back in the red?

It looked like the tide had finally turned. After 8 years and just in time for their IPO, OnDeck had pulled off their first quarterly profit, a meager amount of $354,000. But it was a start right? After their debut on the NYSE, the price swung heavily from a high of $28.98 to a low of $14.52. It closed at $19.37 right before the report was released.

OnDeck reported a $4.3 million loss for the 4th quarter and an $18.7 million loss for the year. Despite this, their margins are definitely improving.

The company issued $369 million in loans last quarter, bringing the 2014 total to $1.2 billion. Sales and marketing expenses doubled in 2014 over the prior year with CEO Noah Breslow and CFO Howard Katzenberg acknowledging on the call they’ve made a big go at TV and radio advertising.

Competition? What competition?

Noticeably, the average APR of loans originated in the fourth quarter was 51.2%, down from over 60% in Q4 of 2013.

One analyst asked if competitive pressures were leading to the reduction in interest rates but Breslow said that wasn’t the case. If anything their closing rate or “booking rate” has been improving and rates coming down is an initiative they’ve taken up on their own. Merchants are actually shopping less according to them.

“Overall this market is still characterized by extreme fragmentation,” Breslow said. “The behavior that we see with our customers is that they might research other competitive options online but then when they actually apply to OnDeck and receive that offer, they kind of have this bird in hand dynamic, and there’s so much search cost associated with going out and looking at other places and so much uncertainty around that, they typically just take that offer that OnDeck has provided to them.”

With their cost of capital down, closing rate up, and defaults steady, a net loss should arguably be a tough pill to swallow. In response to a question about potential regulatory threats, Breslow said there wasn’t really anything on the horizon.

With their cost of capital down, closing rate up, and defaults steady, a net loss should arguably be a tough pill to swallow. In response to a question about potential regulatory threats, Breslow said there wasn’t really anything on the horizon.

So was it just a weird quarter? Under Guidance for First Quarter 2015 and Full Year 2015 in their quarterly report, they suggest another long year of losses ahead.

To infinity and beyond!

The economic and regulatory environments couldn’t be any more favorable to a company that now has almost a decade worth of data under its belt. But unfettered growth still seems to be the number one priority on the agenda. Breslow and Katzenberg spoke optimistically about their recent entry in the Canadian market and the potential to set up shop in other countries. As for the OnDeck Marketplace… surprisingly they claimed its only real purpose is to diversify their funding sources. They are not aiming to become a marketplace but rather they view the OnDeck Marketplace as just one of many vehicles to sell off loans.

So when does the profit part come in? None of the analysts on the line asked about profit. They mostly all offered their congratulations on a “great quarter”. Coincidentally they were almost all from companies that originally underwrote their stock offering.

Six months ago I wrote that OnDeck’s lack of profits has been intentional. In An Insider’s Perspective, I wrote, “What scares their competitors though, is that this strategy has been intentional. Very few if any players in the industry have had the luxury, guts, or the purse to lose money for seven years as part of a coup to conquer the market.” Nothing has changed.

As long as they have cash in the bank, they’re going to keep pursuing growth. They had $220 million in cash and cash equivalents as of December 31st. So for now that means continuing to turn up the marketing heat to increase volume domestically while planting seeds in other markets like Canada.

But the question remains, at what point does profitability become important? Sure it’s tempting to be lending $2 billion or $3 billion a year instead of the $1.2 billion size they’re at now because it would mean they’ll be that much bigger right? Heck, maybe they can be a $10 billion a year lender. But if they are running in the red at a moment where their cost of capital is low, the credit markets are liquid, the economy is favorable, regulatory threats are nil, defaults are static, there is supposedly no competition, and their margins are at their peak, then what happens when one or two of those things change? What if all those things change at once?

But the question remains, at what point does profitability become important? Sure it’s tempting to be lending $2 billion or $3 billion a year instead of the $1.2 billion size they’re at now because it would mean they’ll be that much bigger right? Heck, maybe they can be a $10 billion a year lender. But if they are running in the red at a moment where their cost of capital is low, the credit markets are liquid, the economy is favorable, regulatory threats are nil, defaults are static, there is supposedly no competition, and their margins are at their peak, then what happens when one or two of those things change? What if all those things change at once?

Those rates are too high low

OnDeck’s price jumped in afterhours trading. The market is chalking up the results as a positive. It’s just another losing quarter in a long line of losing quarters for OnDeck and they’ve promised more of the same in the year ahead. Nothing to see here folks, business as usual.

OnDeck may have made it easier for small businesses to get a loan, but they have yet to prove since 2006 if their methodology can actually make money. That should be a wake up call to critics that complain their interest rates are too high.

It is quite possible that their interest rates are actually too low. At an average of 51.2% APR, that’s a heck of a theory to consider.

But it looks like it’s true.

OnDeck 4th Quarter Earnings Call

February 21, 2015 OnDeck Capital (ONDK) will report Q4 and 2014 earnings on Monday, February 23rd at 5pm EST. If you’d like to view the live webcast, you can register here. You can log in as early as 15 minutes before it starts.

OnDeck Capital (ONDK) will report Q4 and 2014 earnings on Monday, February 23rd at 5pm EST. If you’d like to view the live webcast, you can register here. You can log in as early as 15 minutes before it starts.

This is a surprisingly crucial moment for OnDeck who has recorded losses every quarter since inception except for the one just prior to the IPO. Since then the company has been confused as a Lending Club for businesses. The companies differ in that OnDeck’s core business is lending and Lending Club’s is servicing fees.

Critics have called out OnDeck’s high interest rates which top out at 99% APR.

In just a couple months, OnDeck has bounced from a high of $28.98 per share to a low of $14.52. It closed Friday at $18.37.

Despite FinTech Disruptions, Many Thing Stay The Same

January 5, 2015 2014 was an unbelievable year!

2014 was an unbelievable year!

I kicked off last year by opening an account with Lending Club so that I could understand their product. Today I have tens of thousands of dollars invested on their platform and picking up new loans has become part of my daily routine. You could say I’m not surprised they went public a few weeks ago.

I also launched the industry’s first trade publication and ran it as both publisher and chief editor. We produced 6 issues and distributed more than 20,000 print copies combined. Unfortunately the publication will not be continuing further. It is wild to think that it both started and concluded in 2014 as the magazine had a cult-like following.

7 conferences in 4 cities. Las Vegas (twice), San Francisco, New Orleans, and here in New York. I spoke at two of them. Hoping for at least 1 Miami conference this year. Please??? It’s so cold here right now.

OnDeck Capital took a lot of flak in 2014 from both industry insiders and the media. They shrugged it all off and went public on December 17th. Considering they’ve operated on the fringe of the merchant cash advance industry for so long, it was one of those things you had to see to believe. I didn’t get inside the building but I saw the IPO was real from the outside.

I started off 2014 not knowing what a Bitcoin was. Now I have a copy of the entire blockchain, operate a full node (don’t worry I have port 8333 open), have 10 dedicated mining devices running 24/7, have made purchases with bitcoin, conducted countless transfers, and just finished coding a working prototype application using Coinbase’s API. And when I realized that bitcointalk.org and my cryptography books weren’t enough to satisfy my appetite, I found myself talking about bitcoin on IRC; #bitcoin and #bitcoin-pricetalk on irc.freenode.net. I also know who Satoshi Nakamoto really is now too but he made me promise not to tell anyone.

I rebranded Merchant Processing Resource to deBanked, retiring a name I’ve used for 4 years.

I interviewed former Congressman Barney Frank, one of the two architects of the Dodd-Frank Wall Street Reform and Consumer Protection Act (it was only a few questions).

I got asked by a credible movie producer if I would help him on a storyline for a script about Wall Street and the alternative business lending industry. Don’t worry I turned it down!

I jumped on the payment disruption bandwagon and used Square to process credit card transactions all year. You should know that I previously did merchant account sales. I could’ve boarded my own account and set my own fees but I went with Square anyway.

I finally got set up to syndicate on merchant cash advances.

I ran my first 5k in Central Park.

I moved to a different part of Manhattan.

Of course a whole lot more happened. It was a roller coaster year which leads me to believe that 2015 will be impossible to predict. There’s a lot more room to grow in FinTech but it might be time for fresh ideas. Everyone and their mom built an online lending marketplace platform in 2014.

Similarly, it’s also a tough time to become a loan broker or MCA ISO especially if you’re undercapitalized. The easy profit ship has sailed. Press 1s and UCCs aren’t winning business models, at least not ones that will invite outside capital or ensure survival long term.

2014 changed finance but in many ways it stayed the same.

It still takes 2-4 days to confirm an ACH didn’t reject! This is annoying all around. If I add funds to Lending Club on a Monday, it’s not accessible until Friday evening. If you debit a merchant on Monday, you won’t really know if you have it until a few days later. Believe it or not I actually mailed out more checks in 2014 than in any other year of my life. The ACH system appears to be fine until you use something that is far more advanced, something I will probably write about over the next month. Instantaneous payments, low transaction fees, no bank involvement. Yeah, it’s time for ACH to go away…

And with banks, well… I have opened business bank accounts over the last few years with 3 different banks. The one I opened in 2014 required a two hour in-person interview, a process that involved filling out forms by hand and being threatened that the government would shut everything down in a heartbeat if they found out that I so much as breathed wrong on an ATM. It was a repeat of prior account opening experiences. Although I’ve never had an account closed for doing anything wrong (because I’m not actually doing anything wrong), it is easy to see how much regulatory pressure banks are under. Swiping your debit card upside down could cause the entire bank to get an Operation Choke Point subpoena. They want your business but they’re scared to death of anything you might do with a bank account.

All the major peer-to-peer platforms of 2014 became centralized. Lending Club and Prosper don’t even fall in the p2p category anymore. The market trend has been to create a platform designed for the little guys and then hand it over to a bank or institutional money to do all the funding. In some ways it’s easier to deal with a handful of big players instead of thousands or millions of retail investors. But with the regulatory environment uncertain on so many new investment products, it’s probably also safer to deal with institutional investors, lest the regulators claim they violated a consumer protection law they thought up this morning.

Banks continue to be the biggest obstacle to innovation because at the end of the day, all payments flow through them. How can one deBank and truly disrupt?

Hopefully we’ll find out in 2015. Happy belated New Year.

With OnDeck IPO, Strangers Walk Among Us

December 18, 2014The future isn’t ours to make anymore. Not ours alone anyway. Last week the industry was a group of insiders. Today the outsiders walk among us.

$ONDK looking good, but surely this will fall by tomorrow.

— Nealio (@IpoBandwagonTagAlong) Dec. 17 at 11:07 AM

I don’t know who IpoBandWagonTagAlong is but he’s now an influencer in the industry. Almost 13 million shares of OnDeck Capital traded today, its very first day on the NYSE.

$ondk new ipo watching this..seems similar business to $lc

— kunal desai (@kunal00) Dec. 17 at 01:59 PM

It hurts to see “seems similar business to [Lending Club]” as the information being gleaned about OnDeck. I could spend an entire week contrasting the differences but it doesn’t matter anymore. Opinions about OnDeck and the industry they’re part of are about to be formed in tweet-sized pieces at rapid fire pace. Anything longer and the opportunity presenting itself on a trade might pass. Wild.

If you’re in the merchant cash advance business, you’re about to learn that describing the purchase of future sales in anything more than 140 characters is going to work against you. You will inevitably be asked if you do what OnDeck does and you better be concise.

Exactly 140:

“We provide working capital to small businesses by leveraging their future sales. It’s not a loan but it is in some ways similar to OnDeck :)”

Or you could simplify it further and just write:

“Seems similar”

Proud to have OnDeck join the NYSE’s community of the world’s leading, most-recognized companies (NYSE: $ONDK ) pic.twitter.com/ReozilWjbR

— NYSE (@nyse) December 17, 2014

The most striking thing I experienced on opening day was watching so many OnDeck bears transform into OnDeck bulls. Lots of buy orders were placed by those that have been chugging hater-ade for years.

I think that despite reservations with their business model, there was a desire to touch the company in some way, to feel like they were a part of the industry’s milestone. I totally get it. But that brings up an interesting question, how much of the stock can you touch until you start to hold some sway?

I mean shareholders are owners right?

Theoretically, could a terminated ISO buy up shares and then start making demands about re-establishing a partnership? What is the protocol here? Can OnDeck’s ISOs buy OnDeck? Or OnDeck’s competitors? I don’t mean a controlling stake but enough to make some noise. Imagine OnDeck being a funder for the ISOs by the ISOs! If a huge ISO is terminated, does that have to be announced to the public at the same time that the ISO community finds out?

This is a very gossipy industry and coincidentally, I run practically all the industry gossip websites so people like me want to know.

What if a merchant owns shares of the company it is applying to? Is that a positive underwriting data point?

With an office close to the New York Stock Exchange, I was able to at least snap off a few pics of the big banner displayed outside.

And if you’re wondering if I bought stock in OnDeck, I did not. I didn’t buy Lending Club either. It has nothing to do with how I feel about either company.

According to Crain’s, OnDeck’s “$1.32 billion market cap at its debut was the biggest for a venture capital-backed New York City tech company since 1999.” The stock exploded upward almost 40% from its open today. A lot of folks in the industry bought in and the rest is history.

Congratulations OnDeck Capital.