Loans

Amazon and Wells Fargo Shake Hands on Student Loans. Who is Surprised?

July 22, 2016Some might have seen this coming eventually but Amazon is dipping its feet into student loans with Wells Fargo.

Through Amazon Prime Student, the online retailer will offer discounts on student loans when they apply for a Wells Fargo private student loan. The bank will shave half a percentage point off the interest rate for referrals from Amazon.

“We are focused on innovation and meeting our customers where they are – and increasingly that is in the digital space,” said John Rasmussen, Wells Fargo’s head of Personal Lending Group.

Wells Fargo is banking on this multiyear agreement to reach millions of potential borrowers. Five of the largest private student lenders, including Sallie Mae, Wells Fargo and Discover Financial Services Inc., distributed $6.46 billion in loans between July 2015 and March 2016, up 7% from the same period a year earlier, the Wall Street Journal reported.

While the federal government is still the primary student loan lender, banks and other private lenders are steadily increasing their market share. Earlier this week, New York-based private student loan lender CommonBond raised $30 million in equity and $300 million in debt and acquired a startup that opens the gate to employers. San Francisco-based lender SoFi also has similar partnerships with employers for their student loan refinancing product.

“Over 99.99 percent of the student loan market is driven by the federal government and private banks and the tiny piece of the market is made up by CommonBond and SoFi,” said David Klein, CEO of CommonBond to deBanked earlier. “And as big as that sounds, relative to the largesse of the market, we don’t even make up a percent of that.” The ilk of alternative lenders are tilling away at establishing such partnerships to widen their net but will the banks let them?

Online Consumer Lenders Stumble, While Online Business Lenders Stay On Their Game

July 8, 2016

Something is happening in the land of marketplace lending, painful setbacks. And it’s mostly on the consumer side.

Avant, for example, plans to cut up to 40% of its staff, according to the Wall Street Journal. Prosper is cutting or has cut its workforce by 28%. For Lending Club it’s by 12% and for CommonBond by 10%. And then there’s Kabbage, whose consumer lending division playfully named Karrot, has been wound down altogether.

Kabbage/Karrot CEO Rob Frohwein told the WSJ that Karrot was put to sleep about three or four months ago, right around the time that it became obvious to industry insiders that the temperature had changed.

Ironically, the person who best summed up the problem is the chief executive of a lender that rivals the ones that are suffering, but has announced no such job cuts of his own. In March, SoFi CEO Mike Cagney told the WSJ “In normal environments, we wouldn’t have brought a deal into the market, but we have to lend. This is the problem with our space.” And that is a problem indeed because the success of these businesses becomes entirely dependent on making as many loans as possible so they can raise more capital to make as many more loans as possible so they can raise more capital. Perhaps the end game of that dangerous cycle is to go public, but the market has gotten a glimpse now of what that might look like, and they’re not very impressed with Lending Club.

The pressure of living up to the expectation of eternal loan growth manifested itself when Lending Club manipulated loan data in a $22 million loan sale to an investor, but it was a problem all the way back to their inception. In 2009, the company founder made $722,800 worth of loans to himself and to family members, allegedly to keep up the appearances of continuous loan growth. It was never found out until last month, seven years later.

That is a perfect example of the vulnerability that SoFi’s CEO spoke of months ago when he said, “we have to lend.” Because if they don’t lend or investors won’t give them money to lend, well then we’d probably see things like massive job cuts, falling stocking prices, and a loss of investor confidence. And that’s what we’re seeing now.

This wave of cuts is not affecting much of the business lending side

Despite the rush to the exits on consumer lending, Kabbage’s CEO is still very bullish on their business lending practice, so much so that they intend to increase their staff by more than 25%.

And in the last month alone, four companies that primarily offer merchant cash advances, have announced new credit facilities to the aggregate tune of $118 Million, one of whom is Fundry which landed $75 Million. Meanwhile, Fora Financial secured a $52.5 Million credit facility in May. Fora offers both business loans and MCAs.

And here’s one big difference between the consumer side and the business side. While online consumers lenders have found themselves trapped on the hamster wheel of having to lend, there is very little such pressure on those engaged in business-to-business transactions. Sure, their investors and prospective investors want to see growth, but only a handful are following the Silicon Valley playbook of always trying to get to the next venture round fast enough, lest they self destruct.

Avant’s latest equity investment, for example, was a Series E round. Prosper and Lending Club also hopped from equity round to equity round, progressing on a track with evermore venture capitalists that were likely betting on the companies going public.

But over on the business side, they’re much less likely to involve venture capitalists. Equity deals tend to be one-offs, major stakes acquired by private equity firms or private family offices, sometimes for as much as a majority share. These deals tend to be substantially bigger, are harder to land, and are less likely to be driven by long-shot gambles. In other words, the motivation is less likely to be driven by the hope that the company can simply lend just enough in a short amount of time to land another round of capital from another investor.

Examples:

- RapidAdvance was acquired by Rockbridge Growth Equity

- Fora Financial sold an undisclosed but “significant” stake to Palladium Equity Partners

- Strategic Funding Source sold a large stake to Pine Brook Partners

- Fundry sold a large stake to a private family office

Business lending behemoth CAN Capital has raised all the way up to a Series C round but they’ve been in existence for 18 years, way longer than any of their online lending peers. Several other of the top companies in the business-to-business space have relied only on wealthy investors that did not even warrant the need for press.

The upside is that these companies are less vulnerable to the whims of market interest and confidence. Having a down month would not trigger an immediate death spiral, where a downtick in loans means less investor interest which means a further downtick in loans, etc.

The margins in the business-to-business side tend to be bigger too, which means it’s the profitability that often motivates investments, rather than pure origination growth potential.

There are outliers, of course. Kabbage, which has raised Series A through E rounds already, admitted to the WSJ that they still aren’t profitable. Funding Circle, which also raised several rounds, disclosed that at the end of 2014, they had lost £19.4 Million for the year, about the equivalent of $30 Million US at the time.

These facts do not mean that either company is in trouble. Kabbage is not limiting themselves to just making loans for instance, since they also have a software strategy to license their underwriting technology to banks like they have already with Spain’s Banco Santander SA and Canada’s Scotiabank. And Funding Circle enjoys government support at least in the UK where they primarily operate. There, the UK government is investing millions of dollars towards loans on their platform as part of an initiative to support small businesses.

Business lenders and merchant cash advance companies may not necessarily be on the same venture capital track as many of their consumer lending peers because it is a lot more difficult to perfect and scale small business loan underwriting. Even the most tech savvy of the bunch are examining tax returns, verifying property leases, reviewing corporate ownership documents, and scrutinizing applicants through phone interviews. While this process can be done much faster than a bank, there’s still a very old-world commercial finance feel to it that lacks a certain sex appeal to a Silicon Valley venture capitalist who may be expecting a standalone world-altering algorithm to do all the risk related work so that marketing and volume becomes all that matters. Maybe on the consumer side something close to that exists.

Instead, a commercial underwriting model steeped in a profitability-first mindset makes online business lenders better suited to be acquired by a traditional finance firm, rather than a venture capitalist that is probably hoping to hitch a ride on the join-the-fintech-frenzy-and-go-public-quickly-so-I-can-make-it-rain express train.

Consumer lenders who had to lend and are faltering lately, will now have to figure out something more long term beyond just making as many loans as possible. It might not be something that excites their venture capitalist friends, but it is crucial to building a company that will last a long time.

Skintech? Fintech Lenders in China Accept Nude Photos As Collateral

June 14, 2016 Some online lenders in China are taking an invasive application process to a whole new level, according to People’s Daily, a Chinese state-owned newspaper. To increase the likelihood of repayment, applicants may be required to upload a nude photo of themselves while holding an ID card, along with contact information for their friends and family members. And if they don’t pay, they’ll threaten to distribute it to all of them accordingly.

Some online lenders in China are taking an invasive application process to a whole new level, according to People’s Daily, a Chinese state-owned newspaper. To increase the likelihood of repayment, applicants may be required to upload a nude photo of themselves while holding an ID card, along with contact information for their friends and family members. And if they don’t pay, they’ll threaten to distribute it to all of them accordingly.

People’s Daily wrote that the borrowers tend to be educated university students and they are willing participants to these harsh terms if it means they can get the loan they seek. After all, they actually have to take the photos and upload them to the lender in the first place. Insiders reportedly said that naked IOUs have been a practice for a long time.

A reporter for Sixth Tone, a hip media company overseen by the Chinese government, was able to find a student lender online during their journalistic investigation that indeed requested a nude photo and family contact information. The ability to actually repay the loan was not assessed by the lender.

Fu Jian, a lawyer at Yulong Law Firm based in Zhengzhou that was interviewed by Sixth Tone said that the use of a naked photo as collateral is not forbidden by law, even if it does raise ethical questions. Were the photo to be leaked, only then would the law have been broken. “The online lending industry is like a food chain with some huge financial groups on the top, followed by the platforms, then the middlemen,” Fu said to Sixth Tone. “Students, sadly, are just the prey.”

The highly predatory practice is obviously carried out by unscrupulous players and is not representative of the fintech industry in China.

Midland Funding Gets Mentioned in John Oliver’s HBO Show

June 6, 2016The infamous Midland Funding you might know from the Madden v Midland case, was mentioned on John Oliver’s Last Week Tonight and not in the best context. Midland is a subsidiary of Encore Capital Group, the largest publicly traded debt buyer in the United States and the episode was about the not-always-peachy world of debt buying and debt collection.

Oliver referenced Midland just to provide background on an industry as a whole, not to imply that they were involved in anything negative.

More background was added by Jake Halpern, the author of Bad Paper: Chasing Debt from Wall Street to the Underworld, who explained that the sale of debt from one party to another is not always done using the most sophisticated means, with it often being simply a list of fields on an Excel spreadsheet.

Oliver, who took his research to the extreme, actually set up his own debt collection company in Mississippi and purchased $15 million worth of debt that was aged beyond the statutory collections period for the bargain price of $60,000. Rather than try to collect on the debt, which he mentioned would not have been illegal, he decided to forgive the debt entirely and set the record for TV’s largest monetary giveaway in the process.

Oliver was careful to remind viewers throughout that while there are a few bad seeds and horror stories, the industry itself is regulated and is not illegal. You can watch the episode below:

Throwback to 2008? Credit Card, Auto Debt Soars to $1 Trillion

May 20, 2016Subprime borrowing is back, this time with auto loans.

Vehicle loans and leases held by subprime consumers increased by 11 percent in Q1 this year and the for the first time since the recession, balances on auto loans hit the $1 trillion mark, up from $905 billion last year.

Non-bank finance companies and credit unions saw the largest spike in loan growth market share with 26 percent and 16 percent respectively.

“With more and more consumers relying on financing, it is important for lenders to keep a close eye on delinquency trends to ensure the market remains healthy,” said Melinda Zabritski, senior director of automotive finance for Experian, which conducted the study.

However there is some respite in the overall percentage of total delinquent loans remains relatively low when compared to pre-recession levels.

And it’s not just auto loans that are soaring, credit card debt is also pushing the $1 trillion mark inching scarily close to recession peak of $1.2 trillion in 2008. According to Federal Reserve numbers, outstanding balances touched $952 billion in the first quarter, up 6 percent last year, and the highest level since August 2009.

Here’s How Much an American Household Owes in Credit Card Debt

April 8, 2016 US credit card debt equals debt of Canada, France, Japan, Mexico, Russia and China put together.

US credit card debt equals debt of Canada, France, Japan, Mexico, Russia and China put together.

62 percent of Americans are under credit card debt they cannot pay off.

A study by Fifth Third Bank revealed that 70 percent Americans are under debt and financial hardship.

Alarmingly enough, an average American household owes $7,879 in credit card debt alone, the highest since the recession. If that sounds worrisome, there’s more. Yet another survey revealed that recent college graduates choose to remain ignorant about the student loan they owe. Nearly half of them (45 percent) didn’t know what percentage of their salary goes to paying loans and 15 percent of them are unaware of how much they owe.

Key numbers:

- In 2015 alone, credit card debt rose by $71 billion.

- Americans spent $52 billion in the fourth quarter of 2015, mostly due to holiday shopping and this equaled credit card debt during the entire years of 2009, 2010 and 2011 combined.

- The delinquency rates on credit card debt is 2.17 percent, the lowest since 1991.

Some experts might argue that rising credit card debt is a healthy sign of consumer spending. However, that needs to be consistent with wages. America added 242,000 jobs in February but wages took a hit. According to Labor Department statistics, average hourly earnings dropped by 0.1 percent, declining for the first time since December 2014.

Does this portend a warning signal for investors buying loans?

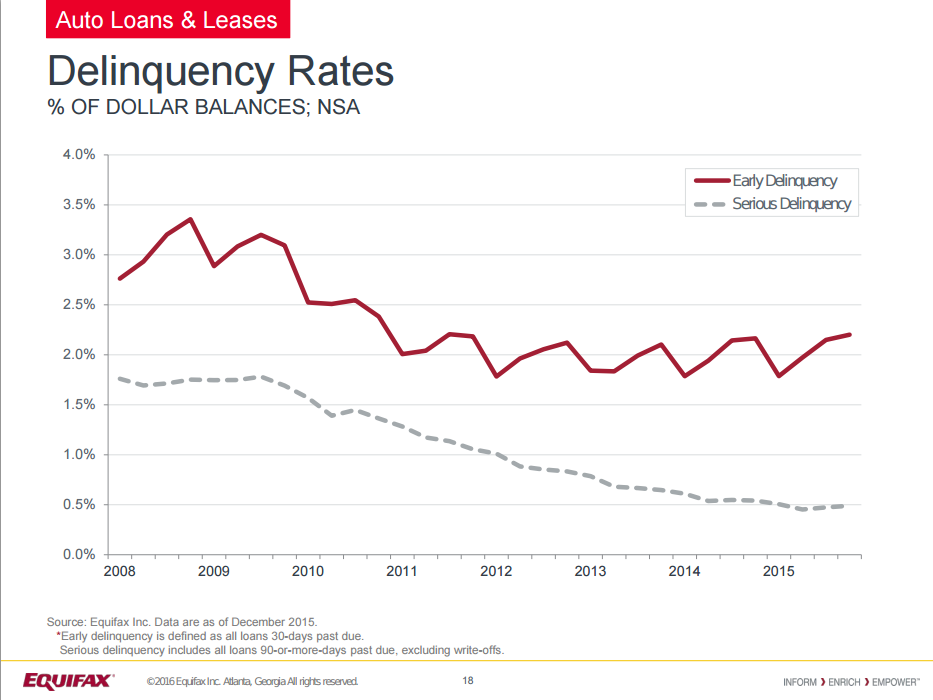

Are Subprime Auto Loans Showing Cracks or Not?

March 19, 2016 Subprime auto delinquencies are even higher now than they were during the height of the most recent recession, according to Fitch Ratings. The 60-day-plus delinquency rate of the subprime loan group that Fitch evaluates reached 5.16% last month, compared to 5.09% in January, 2009.

Subprime auto delinquencies are even higher now than they were during the height of the most recent recession, according to Fitch Ratings. The 60-day-plus delinquency rate of the subprime loan group that Fitch evaluates reached 5.16% last month, compared to 5.09% in January, 2009.

Fitch attributed this to weaker underwriting standards as well as sharp origination growth and increased competition.

The prime sector is mostly stable, they say. Further weakness is anticipated across all credit categories, though the outlook is stable.

But while Fitch spoke of weaker underwriting and nearly unprecedented delinquencies, consumer credit reporting agency Equifax spun a different picture just four days later when they announced the results of their own auto lending study.

“Lenders are making more informed lending decisions and the underwriting process has been strengthened as a result of new data and technology that is available to the marketplace,” said Amy Crews Cutts, chief economist at Equifax.

Indeed, the rates of both early delinquency and serious delinquency as a percentage of dollar balances are nowhere near recession levels, at least according to Equifax’s data set.

Both Fitch and Equifax agree there has been an increase in auto loan originations.

In a WSJ interview, hedge fund manager Ben Weinger said that demand for auto debt has led lenders to systematically loosen underwriting standards.

Equifax’s Cutts recently said however that “credit performance is still excellent, showing that lenders are prudently extending credit to well-underwritten borrowers.”

Who’s right?

Here’s How Much the American Credit Card Addiction is Worth

February 9, 2016 Of all the addictions Americans could have, credit card debt is one which is measurable monetarily. And as of December 2015, it was $936 billion.

Of all the addictions Americans could have, credit card debt is one which is measurable monetarily. And as of December 2015, it was $936 billion.

A recent study by the Federal Reserve of Boston revealed that a majority of Americans roll over their debt paying high amounts of interest. Americans racked up $103 billion in debt since April 2011, still less than the $1.02 trillion owed in 2008, Bloomberg reported.

The credit card frenzy that hits people in their 20s is hard to get rid of and as they get older, the reliance on debt only increases. ‘While 20-year-olds use more than half their available credit on average, 50-year-olds use almost 40 percent,’ the article noted.

The study revealed that credit card usage on an individual level doesn’t change much during the course of their life but banks constantly adjust the credit available. ‘The average credit-card limit rose about 40 percent from 2000 to 2008, then plunged about 40 percent during 2009.’ The study also found that when offered a 10 percent increase in credit limits, people who take on revolving debt subsequently increase their debt by 9.99 percent.