Legal Briefs

Madden vs. Midland Funding, LLC: What does it mean for Alternative Small Business Lending?

August 13, 2015 On Friday, May 22, 2015, while the rest of us were gearing up for the long Memorial Day weekend, three judges of the United States Court of Appeals for the Second Circuit quietly issued their decision in Madden v. Midland Funding, LLC. Though issued to little fanfare, the decision, if upheld on appeal—may lead to significant changes in consumer and commercial lending by non-bank entities.

On Friday, May 22, 2015, while the rest of us were gearing up for the long Memorial Day weekend, three judges of the United States Court of Appeals for the Second Circuit quietly issued their decision in Madden v. Midland Funding, LLC. Though issued to little fanfare, the decision, if upheld on appeal—may lead to significant changes in consumer and commercial lending by non-bank entities.

Loans that were previously only subject to the usury laws of a single state may now be subject to more restrictive usury laws of multiple jurisdictions. Commercial transactions that could be affected include short-term loans by a number of alternative small business lenders.

The Case

The plaintiff, Saliha Madden, opened a credit card account with a national bank in 2005. Three years later, Madden’s account was charged off with an outstanding balance. The account was later sold to Midland Funding, LLC, a debt purchaser.

In November 2010, Midland sent a collection letter to Madden’s New York residence informing her that interest was still accruing on her account at the rate of 27% per year. In response, Madden filed a class action lawsuit against Midland and its servicer. In her complaint, Madden alleged that Midland had violated state and federal laws by attempting to collect a rate of interest that exceeded the maximum rate set by New York State’s usury laws. Midland countered that as a national bank assignee, it was entitled to the preemption of state usury laws granted to national banks by the National Bank Act (the “NBA”). The district court agreed with Midland and entered judgment in its favor. Madden appealed to the Second Circuit.

After reviewing the record, the Court of Appeals reversed the district court’s decision. The appellate court found that the NBA’s preemption provision did not apply to Midland as a mere bank assignee. Instead, the court held that in order “[t]o apply NBA preemption to an action taken by a non-national bank entity, application of state law to that action must significantly interfere with a national bank’s ability to exercise its power under the NBA.”

The court explained that the NBA’s preemption protections only apply to non-bank entities performing tasks on a bank’s behalf (e.g. bank subsidiaries, third-party tax preparers). If a bank assignee is not performing a task on a national bank’s behalf, the NBA does not protect the assignee from otherwise applicable state usury laws. Therefore, as Midland’s collection efforts were performed on its own behalf and not on behalf of the national bank that originated Madden’s account, the appellate court found that New York’s usury laws were not preempted and that Midland could be subject to New York’s usury restrictions.

Usury Law Compliance

The Madden decision undermines a method of state usury law compliance that I’ll refer to as the “exportation model”. In a typical exportation arrangement, a non-bank lender contracts with a national bank to originate loans that the lender has previously underwritten and approved. After a deal has been funded, the bank sells the loan back to the lender for the principal amount of the loan, plus a fee for originating the deal.

1F.3d —, 2015 U.S. App. LEXIS 8483 (2d Cir. N.Y. May 22, 2015).

The exportation model allows non-bank lenders to benefit from the preemption protections granted to banks under the NBA. Specifically, the NBA provides that a national bank is only subject to the laws of its home state. This provision allows a bank to ‘export’ the generally less restrictive usury laws of its home state to other states where it does business. As bank assignees, lenders that have purchased loans from a bank are only subject to the laws of the originating bank’s home state. This exemption saves these non-bank lenders from having to engage in a state-by-state analysis of applicable usury laws.

The Madden decision, however, casts doubt on the ability of these non-bank assignees to benefit from the NBA’s preemption protections. The Second Circuit’s decision makes clear that non-bank assignees that are not performing essential acts on a bank’s behalf—which would seem to include alternative small business lenders—are not entitled to NBA preemption and are subject to the usury laws of the bank’s home state as well as any otherwise applicable state’s

usury laws.

Aftermath

While the Court of Appeals’ decision foreclosed Midland’s preemption argument, other issues remained unresolved. Specifically, the circuit court did not decide whether the choice-of-law provision in Madden’s cardholder agreement—which provided that any disputes relating to the agreement would be governed by the laws of Delaware—would prevent Madden from alleging violations of New York State usury law.

In the district court proceeding, both parties had agreed that if Delaware law was found to apply, the 27% interest rate would be permissible under that state’s usury laws. The district court, however, did not address the choice-of-law issue because the court had found that the NBA’s preemption protections were sufficient grounds upon which to resolve the case. As the issue had not been addressed, the circuit court remanded the case back to the district court to decide which state’s law controlled.

In the district court proceeding, both parties had agreed that if Delaware law was found to apply, the 27% interest rate would be permissible under that state’s usury laws. The district court, however, did not address the choice-of-law issue because the court had found that the NBA’s preemption protections were sufficient grounds upon which to resolve the case. As the issue had not been addressed, the circuit court remanded the case back to the district court to decide which state’s law controlled.

But before sending the case back down, the appellate court made two points worth noting. First, the court stated that “[w]e express no opinion as to whether Delaware law, which permits a ‘bank’ to charge any interest rate allowable by contract…would apply to the defendants, both of which are non-bank entities.” The court’s statement suggests that it may not have completely agreed with the parties that 27% would be a permissible interest rate under Delaware law.

Second, the court highlighted a split in New York case law on the enforceability of choice-of-law provisions where claims of usury are involved. Generally, courts will refuse to enforce a choice-of-law provision if the application of the chosen state’s law would violate a public policy of the forum state. As usury is sometimes considered an issue of public policy, the enforceability of such clauses is commonly a point of contention in usury actions. The cases cited by the Court of Appeals show that some courts in New York have enforced choice-of-law provisions—even where the interest rate permitted by the chosen state would violate New York’s usury laws—while other New York courts have refused to enforce such provisions in light of public policy concerns.

New York, however, is by no means the only state with usury laws that are less than straightforward. The general complexity of state usury laws is evidenced by the circuit court’s hesitation to agree with Madden’s concession that a 27% interest rate would be permissible under Delaware law. The court made clear that an argument could be made that the rate was usurious under both New York and Delaware law.

Madden’s Impact

An important legal principle that was not addressed in either the district or circuit court proceedings is the ‘valid when made’ doctrine of assignment law. The ‘valid when made’ doctrine provides that a loan that is valid at the time it is made will remain valid even if the loan is subsequently assigned. This doctrine may have led to a different outcome in the case had Midland argued it before the district or circuit court. Midland is now appealing the Second Circuit’s decisions and many expect a ‘valid when made’ argument to be a primary point of Midland’s appeal (SEE NOTE BELOW). If this argument is successful, the practical impact of Madden would be greatly diminished.

NOTE: The Second District Court rejected a request to rehear the case. Read that decision here.

In the meantime, the Madden decision will likely increase the importance of choice-of-law analysis in relation to usury law. Assignees that previously relied on the NBA’s preemption provision as a method of state usury law compliance will now need to address the enforceability of their contractual choice-of-law clauses where claims of usury may become an issue. This analysis is often a complex undertaking because states take varying views of what constitutes usury as well as whether or not usury is an issue of public policy.

While the Madden decision may have been published before the long Memorial Day weekend, analyzing its consequences will likely keep many non-bank lenders (and their attorneys) busy, even on their days off.

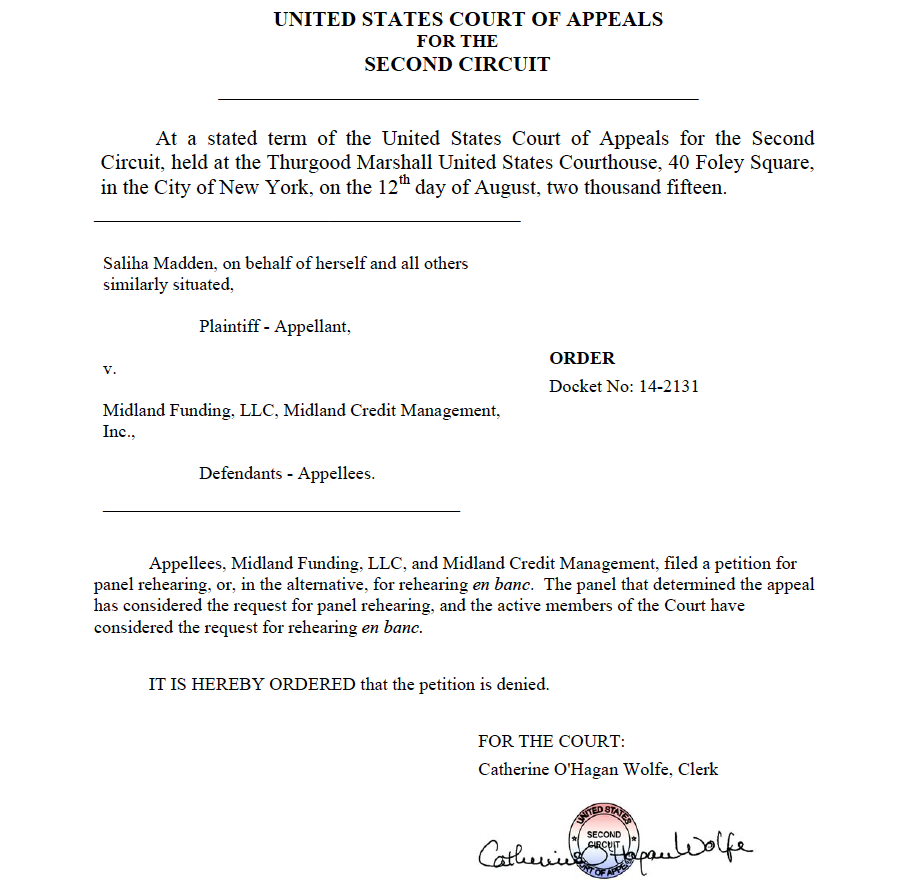

Madden v. Midland Appeal Rejected

August 13, 2015Alternative lenders might have reason to lose a little bit of sleep going forward. The United States Court of Appeals for the Second Circuit shot down a request for a rehearing of Madden v. Midland. The original ruling stated that third party debt buyers are not covered under National Bank Act pre-emption. That decision had major ramifications for alternative lenders who often rely on banks to issue the loans and then immediately sell them to the “lender” to book and service.

You can read a legal brief of the case here.

Lending Club’s CEO recently addressed this case and he explained that he believed his company would be unaffected because of their choice of law provision.

And Patrick Siegfried, Esq, the author of the Usury Law Blog, has previously said that Madden v. Midland may be the start of new usury Litigation.

Decision below:

Ignoring Cease and Desist Letters – Just Don’t Do It

August 12, 2015 Usury law is complex. It is an area of law heavily burdened with obscure exceptions and antiquated nuances. Yet, one point is clear.

Usury law is complex. It is an area of law heavily burdened with obscure exceptions and antiquated nuances. Yet, one point is clear.

No matter how clear the case law, sophisticated the compliance program or lax the regulator, when a business receives a cease and desist letter from a state or federal authority it must be addressed. To do nothing risks litigation and worse. Case in point is the recent complaint filed by the CFPB against payday lender NDG Financial Corp. and its affiliates.

According to the complaint, NDG received cease and desist letters regarding its lending practices from Michigan (2014), California (2012, 2013, and 2014), Virginia (2013), New Hampshire (2011), Maine (2011), Oregon (2011), and Pennsylvania (2010). And though NDG stopped lending in some of these jurisdictions, it apparently felt confident enough to continue its operations in a number of these states even after receiving the letters. Partly as a result, the Bureau filed suit.

Now, I am in no way suggesting that CFPB will prevail in its claims against NDG or that merely receiving a cease and desist letter is evidence of wrongdoing. As a recent post of mine shows, regulators are often incorrect in their interpretation of usury law. That being said, the number of previous warnings NDG received from state regulators prior to being sued is stunning. So it seems to me that NDG is somewhat responsible for the targeting it has received from the CFPB.

If a lender has received 8 cease and desist letters within a 4 year period, there is a problem. It doesn’t mean it must immediately stop all lending. But it would be wise to undertake a greater review of its operations and, hopefully, generate a plan to address the regulators’ concerns.

Placing one’s head in the sand just won’t cut it.

Renaud Laplanche on Madden v. Midland

August 8, 2015 In case you missed the comments by Lending Club’s CEO regarding the Madden v. Midland decision, we’ve got the transcript of it from the Q2 earnings call below. A brief of that case was published on deBanked back on June 11th by lawyers from Giuliano McDonnell & Perrone, LLP.

In case you missed the comments by Lending Club’s CEO regarding the Madden v. Midland decision, we’ve got the transcript of it from the Q2 earnings call below. A brief of that case was published on deBanked back on June 11th by lawyers from Giuliano McDonnell & Perrone, LLP.

Smittipon Srethapramote – Morgan Stanley

And do you have any comments on the Madden versus Midland funding case that’s going through the court system right now in terms of how it potentially impacts your business?Renaud Laplanche – Founder & CEO

Yes, so we’ve seen that case that came out a couple of months ago. I think the –our take there is obviously the particular circumstances of the case are different from what we’re seeing on our platform. But in general what really helps us apply Utah law to most of our loans is really a couple of things. One is for the all preemption. And the second is choice of law provision in our contract. The Madden case really challenged the federal preemption but did not challenge the choice of law provision, so that’s really the – and we don’t need both, we need one of them. So we continue to operate in the Second Circuit district where that decision was rendered exactly as we did before and are relying on our choice of law provisions.Note that this particular case is getting challenged by a lot of players in the banking industry, including the American Banking Association. And I think it’s an unusual case, but certainly that doesn’t come back to us in that the sense that we continue to rely on choice of law provision. If we were to see that the choice of law provision was getting challenged elsewhere which there’s no reason to expect at this point, we could also think of a different issuance framework than the one we’re using now where we would switch to a series of state licenses. And that’s in [indiscernible] we provided in our slide deck that shows that using the current mix we have about 12.5% of our loans that would exceed the state interest rate caps.

So that certainly would be [indiscernible] demand and we’d have to revise our pricing in certain states, but that certainly would be another option available to us if our choice of law provision and federal preemption was getting challenged in other states.

On July 28th, Attorney Patrick Siegfried pointed out that the Madden case could be the start of a chilling trend after a subsequent ruling in Blyden v. Navient Corp. In that brief, he wrote, “Blyden also demonstrates that debtors that become aware of subsequent assignments of their loans may be inclined to use the assignment event as a way to invalidate otherwise legitimate debts.”

Florida Court of Appeals Finds Usury Does Not Violate Public Policy, Denies Temporary Injunction

August 8, 2015 The Florida Office of the Attorney General was granted a temporary injunction against CashCall, Inc. The Attorney General’s action was based on alleged violations by CashCall of Florida’s Deceptive and Unfair Trade Practices Act related to loans CashCall had issued to Florida residents that charged rates in excess of Florida’s usury law. The injunction required CashCall to pay all loan proceeds it received during the pendency of the underlying litigation into the court registry and to establish a reserve of one million dollars. CashCall appealed to the Court of Appeals.

The Florida Office of the Attorney General was granted a temporary injunction against CashCall, Inc. The Attorney General’s action was based on alleged violations by CashCall of Florida’s Deceptive and Unfair Trade Practices Act related to loans CashCall had issued to Florida residents that charged rates in excess of Florida’s usury law. The injunction required CashCall to pay all loan proceeds it received during the pendency of the underlying litigation into the court registry and to establish a reserve of one million dollars. CashCall appealed to the Court of Appeals.

In its review, the Court explained that “[a]s a matter of law, in order to obtain a temporary injunction the Attorney General must demonstrate that ‘it has a clear legal right’ to the injunction…” and that “the viability of the Attorney General’s action is dependent on its ability to avoid the choice of law provision in the loan agreements.” The provisions provided that the loans at issue would be governed under the laws of Cheyenne River Sioux Tribe which permitted the rates charged.

The Attorney General argued that the choice of law provision was unenforceable because it violated Florida’s strong public policy against usury. CashCall disagreed. It countered that Florida had no such policy against usury and the provision should be upheld.

CashCall’s argument prevailed. The appellate court cited two cases where the Florida Supreme Court had declined to apply the public policy exception to set aside a choice of law provision in a usury context. In those cases, the Supreme Court held that Florida has no strong public policy against usury as long as there is a reasonable relationship between the chosen jurisdiction and the transaction.

The Court of Appeals highlighted that the Attorney General had essentially agreed with this finding during the lower court proceedings. The Court quoted a portion of the Attorney General’s statement:

Hey, that money you’re getting from Floridians, let’s put it into the Court Registry until we can hear your Motion to Dismiss from all of your hundreds of attorneys and we can talk about hundreds of years’ worth of tribal authority. And you know what, they might win. There’s good case law I think as Brian said on both sides. It is an interesting argument. But I would like to ask the Court to focus on what we asked for and are we entitled to it.

Based on the Attorney General’s statement and Supreme Court precedent, the Court of Appeals found that the Attorney General had failed to demonstrate a clear right to the injunction and reversed the lower court’s decision.

Cashcall, Inc. v. Office of the AG, 2015 Fla. App. LEXIS 11559 (Fla. Dist. Ct. App. 2d Dist. July 31, 2015)

Is This OnDeck Class Action Lawsuit a Sham?

August 7, 2015Update: The lawsuit was withdrawn on September 28, 2016

If you haven’t actually read the class action complaint filed against On Deck Capital on August 4th for an alleged violation of securities laws, you can download it here. Reactions throughout the industry are generally mixed, but the big surprise is that anyone would actually be surprised about who OnDeck is or what they are doing.

If you haven’t actually read the class action complaint filed against On Deck Capital on August 4th for an alleged violation of securities laws, you can download it here. Reactions throughout the industry are generally mixed, but the big surprise is that anyone would actually be surprised about who OnDeck is or what they are doing.

The company sourced 68.5% of its loans from commercial finance brokers in 2012 and 45.6% of its loans from them in 2013. By the second quarter of this year, that percentage had drifted down to 20.6%.

To OnDeck, this gradual shift has been part of an overall strategy to control their sales process, costs, and reputation. While it might impede origination growth in the short term, it would be a heck of a lot harder to explain to investors in the future that the company’s fate was in the hands of unknown salespeople who may or may not be swayed to work with their competitors at any moment.

Understandably, many brokers were not happy when OnDeck suddenly terminated them. Angry feelings spilled out on to DailyFunder, an online message board, and were eventually cited in a Seeking Alpha article, the very same article the lawsuit opens up with to make its case.

“THE TRUTH BEGINS TO EMERGE,” the complaint states. “On February 11, 2015, less than two months after the IPO, SeekingAlpha.com published an article entitled “On-Deck Capital: Bad Loans, Bad Interest Rates, Bad Business Plan.”

But the author of the article, TheStreetSweeper, which describes itself as as “a publisher of news and opinion,” placed a disclaimer that they held a short position in OnDeck’s stock. And notably, TheStreetSweeper website is run by Hunter Adams, a convicted felon who makes no effort to hide his past. His website bio says, “his career ended in 2001, when government investigators accused him of manipulating worthless penny stocks.” And continues, “he pled guilty to two conspiracy charges — for securities fraud and money laundering — and served time in prison for his crimes. Years later, he pled guilty to racketeering charges, fully cooperated with the government and accepted full responsibility for his actions.”

Today, his opinion on a stock for which he holds a short position in, has somehow become credible enough for lawyers to make the case that the “truth” had come out about OnDeck. But it’s no small oversight by the Pomerantz law firm, the attorneys that brought the suit on behalf of plaintiff Carl A. Stitt. A cursory glance at the law firm’s past press releases and filed complaints show that the firm regularly relies on TheStreetSweeper’s stories to solicit plaintiffs as well as to bolster class action complaints.

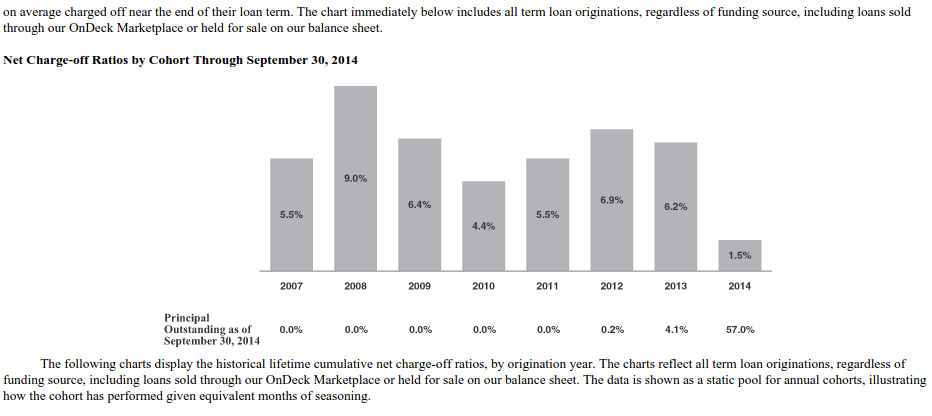

Notably, TheStreetSweeper’s analysis (overseen by convicted mob associate pumper dumper Hunter Adams), which Pomerantz accepts at face value and offers as evidence of misleading default rates, calculates a loan loss rate 24.8%. That formula is unfortunately incorrect. $26.7 million in charge offs divided by $107.6 million in gross revenue might return 24.8% but that’s not how one assesses a loan loss rate. $107.6 million is the interest income, not the aggregate loan principal.

OnDeck had an aggregate unpaid principal balance on loans outstanding of $422.1 million for the nine months ending September 30, 2014. $26.7 million was charged off during that time period.

Some quick math: $26.7 million/$422.1 million = 6.3% lost.

This is decent considering the company generated $107.6 million worth of interest income, not to mention consistent with what company management has both said and reported. TheStreetSweeper’s math and the plaintiff’s reliance on it is unsurprisingly wrong.

Reading through the rest of the suit, the plaintiff’s complaint hinges almost entirely on the phony calculation.

OnDeck might not be popular with the commercial finance brokers these days, and I myself have published several posts about their progress (good and bad), but if anything is garbage, it’s probably this lawsuit.

—-

Note: I do not and have never had a financial position in OnDeck.

Blyden v. Navient Corp: A Glimpse of a Post-Madden Future?

July 28, 2015 A recent US District Court decision out of California offers a rough idea of the usury litigation that may begin to occur if the decision in Madden vs. Midland Funding, LLC ultimately stands.

A recent US District Court decision out of California offers a rough idea of the usury litigation that may begin to occur if the decision in Madden vs. Midland Funding, LLC ultimately stands.

The case involved a student loan that the plaintiff had received that had been originated by a national bank. The loan charged an interest rate of 10.25% which the plaintiff believed to be lawful because the loan had been made by a bank.

When the plaintiff later learned that her loan had been assigned to a non-bank entity, she instituted a usury class action arguing that the assignee was not been permitted to charge more than 10% interest under California law. She sought to represent a class of borrowers whose loans had been made by the national bank and later assigned.

In an effort to represent the largest class possible, the plaintiff named as defendants various investment trusts that had purchased loans from the bank despite the fact that most of the trusts had never had any interest in her specific loan. While the court ultimately dismissed the case because of pleading deficiencies, it granted the plaintiff leave to amend her complaint and the case seems likely to continue.

What’s noteworthy about the Blyden case is that it is illustrative of some of the possible consequences of the 2nd Circuit’s decision in Madden. In particular, it shows that a large number of unrelated entities may be drawn into extended litigation by a plaintiff that is unable (because of a lack of information) or unwilling (because of a desire to represent the largest class possible) to limit its claims to those specific entities that have had or presently maintain an interest in the loan at issue. While this desire to cast the widest net possible is common to most class action plaintiffs, it seems likely to prove especially true in cases involving securitized products that have passed through numerous investment vehicles.

Blyden also demonstrates that debtors that become aware of subsequent assignments of their loans may be inclined to use the assignment event as a way to invalidate otherwise legitimate debts. The plaintiff in Blyden conceded that she was unable to pursue a usury action against the national bank that had originated the loan because of NBA preemption. She also acknowledged that the original transaction had been legal. Only when the plaintiff later learned of the assignment of her loan to a non-bank entity did she seek to recover the allegedly usurious interest charges.

What may be most disconcerting for assignees about the Blyden case is that it only demonstrates some of the complex consequences that may result from the Madden decision.

Blyden v. Navient Corp., 2015 U.S. Dist. LEXIS 96824 (C.D. Cal. July 23, 2015)

Failure to Prove Damages Dooms Usury Claim

July 27, 2015 A recent decision in an adversarial bankruptcy proceeding demonstrates how important it is to prove each and every element of a claim of usury. In the case, the court refused to award relief–despite the rate being conceded as usurious–because the debtor had failed to plead all of the required elements of the claim.

A recent decision in an adversarial bankruptcy proceeding demonstrates how important it is to prove each and every element of a claim of usury. In the case, the court refused to award relief–despite the rate being conceded as usurious–because the debtor had failed to plead all of the required elements of the claim.

The litigation involved long standing business partners whose relationship had soured. When one partner filed bankruptcy, the other filed a plethora of proof of claims for money allegedly owed.

The debtor countered with usury as a defense. While the creditor conceded that the rate alleged in its proof of claims exceeded the maximum rate in Texas, it argued that the filing of a proof of claim did not constitute a “charge” under Texas’ usury statute. Therefore, the creditor believed it was not subject to the usury penalties.

The court rejected the creditor’s contention and cited to a number of cases that had construed proof of claims as “charges” under Texas’ usury statute. These holdings, coupled with the creditor’s admission, led to a quick finding of fact that the alleged rate was usurious.

The court then turned to the element of damages. The Texas code provides that:

A person who violates this subtitle by contracting for, charging, or receiving interest or time price differential greater than the amount authorized by this subtitle is liable to the obligor for an amount equal to:

(1) twice the amount of the interest or time price differential contracted for, charged or received; and

(2) reasonable attorney’s fees set by this court.

Texas Finance Code § 349.001(a).

Despite the finding of a usurious rate, the court held that the debtor had failed to present any evidence or testimony to prove the amount of interest that was usurious under Texas law. Rather, the debtor had merely made conclusory statements that the interest rate charged was usurious. The court held these statements to be insufficient evidence to justify an award of damages.

Ali v. Merchant (In re Ali), 2015 Bankr. LEXIS 2443 (Bankr. W.D. Tex. July 23, 2015)