Legal Briefs

Court Refuses to Apply Federal Preemption to Loan Servicer Despite Bank’s Continued Interest in Loan

January 20, 2016 In November 2014, the Pennsylvania Office of Attorney General (“OAG”) filed a complaint against a number of companies that did business with a group of payday lenders. The payday lenders were a Delaware bank and three tribal entities. The defendants provided marketing services and operational support to the lenders and in some instances purchased portions of the loans. In its complaint, the OAG alleged that the defendants, and not the bank or tribes, were the de facto lenders and that their partnership with the bank and tribes were constructed to circumvent Pennsylvania usury laws.

In November 2014, the Pennsylvania Office of Attorney General (“OAG”) filed a complaint against a number of companies that did business with a group of payday lenders. The payday lenders were a Delaware bank and three tribal entities. The defendants provided marketing services and operational support to the lenders and in some instances purchased portions of the loans. In its complaint, the OAG alleged that the defendants, and not the bank or tribes, were the de facto lenders and that their partnership with the bank and tribes were constructed to circumvent Pennsylvania usury laws.

In their motions to dismiss, the defendants argued that, in regards to the loans issued by the Delaware bank, federal law preempted the OAG’s state usury claims. They explained that the Depository Institution Deregulation and Monetary Control Act (“DIDA”) allows state-charted federally insured banks to charge the same interest rate in any state as they are legally permitted to charge in the state in which they are located. The DIDA mirrors the language of section 85 of the NBA.

The defendants argued that because the Delaware bank was a state-charted federally insured bank, the DIDA preempted the causes of action in the OAG’s complaint as they pertained to the defendants’ partnership with the bank. As additional support for their preemption argument, the defendants highlighted the fact that the bank not only originated the loans but also retained them wholly, or at least in part.

Despite the bank’s origination and retention of the loans, the District court rejected the defendants’ arguments. It held that federal preemption only applied to the bank. In support of its holding, the court cited to the Third Circuit’s decision in In re Community Bank of Northern Virginia, 418 F.3d 277, 295 (3d Cir. 2005). In that case, the Circuit court held that state law claims against a non-bank were not preempted by the DIDA or the NBA.

The District court refused to apply federal preemption to the defendants even though the bank retained ownership of all or part of the loans. The court noted that the complaint alleged that the defendants, and not the bank, were the real parties in interest and therefore reasoned that preemption should not apply.

Pennsylvania v. Think Fin., Inc., 2016 U.S. Dist. LEXIS 4649 (D. Pa. 2016)

When it Comes to Usury Law, Be Careful What You Ask For

January 8, 2016 In a previous post, Creditor Fails to Navigate Usury Law “Minefield”, Ordered to Refund $1.3 Million to Debtor, I discussed a recent bankruptcy case in California. In the case, a lender had filed a claim in the borrower-debtor’s bankruptcy case. The debtor objected to the claim and brought a usury claim against the lender for allegedly usurious interest that it claimed it had paid.

In a previous post, Creditor Fails to Navigate Usury Law “Minefield”, Ordered to Refund $1.3 Million to Debtor, I discussed a recent bankruptcy case in California. In the case, a lender had filed a claim in the borrower-debtor’s bankruptcy case. The debtor objected to the claim and brought a usury claim against the lender for allegedly usurious interest that it claimed it had paid.

After a two day trial on the debtor’s objection to the lender’s bankruptcy claim, the court found in favor of the debtor and ordered the lender to refund the usurious interest it had charged the debtor. The court also ordered post-trial briefing on a number of issues, including:

Are the debtors barred by the two year statue of limitations on usury actions from recovering usurious interest paid prior to the 2 years before the date of the bankruptcy petition?

In its post-trial brief, the lender argued that the California statute of limitations provides that a borrower that commences an usury action against a lender may only recover the amount of usurious interest paid to the lender in the preceding two years prior to filing the complaint. Therefore, the lender argued, the amount that the debtor could recover should be limited to those payments that the debtor had made within the two years preceding the filing of the bankruptcy petition. The court disagreed.

The court first noted that California usury claims generally must be filed within two years of the payment at issue. However, if the lender brings an action on the debt, the borrower may cross complain for recovery of all usurious interest paid, regardless of the two year statute of limitations. The court found that this was also true where a lender files a claim for usurious interest in a bankruptcy proceeding. As support the court cited a recent ninth circuit which explained:

The filing of a proof of claim is analogous to filing a complaint in the bankruptcy case… And a claim objection by the debtor is analogous to an answer… In re Cruisephone, Inc., 278 B.R. 325, 330 (Bankr. E.D.N.Y. 2002) (“In the bankruptcy context, a proof of claim filed by a creditor is conceptually analogous to a civil complaint, an objection to the claim is akin to an answer or defense and an adversary proceeding initiated against the creditor that filed the proof of claim is like a counterclaim.”).

Based on the Ninth’s Circuit holding, the court found that the lender had “‘brought an action’ by filing its proof of claim and actively and aggressively pursuing its remedies in the course of the bankruptcy case, and the usury defenses and claims of the Debtors are in the nature of counterclaims, thus rendering the two-year statute of limitations inapplicable here.” As a result, the debtor was permitted to recover all of the usurious interest that the court had awarded it at trial.

In re Arce Riverside, LLC, 2015 Bankr. LEXIS 4380 (Bankr. D. Cal. 2015)

Getting a California Lender’s License

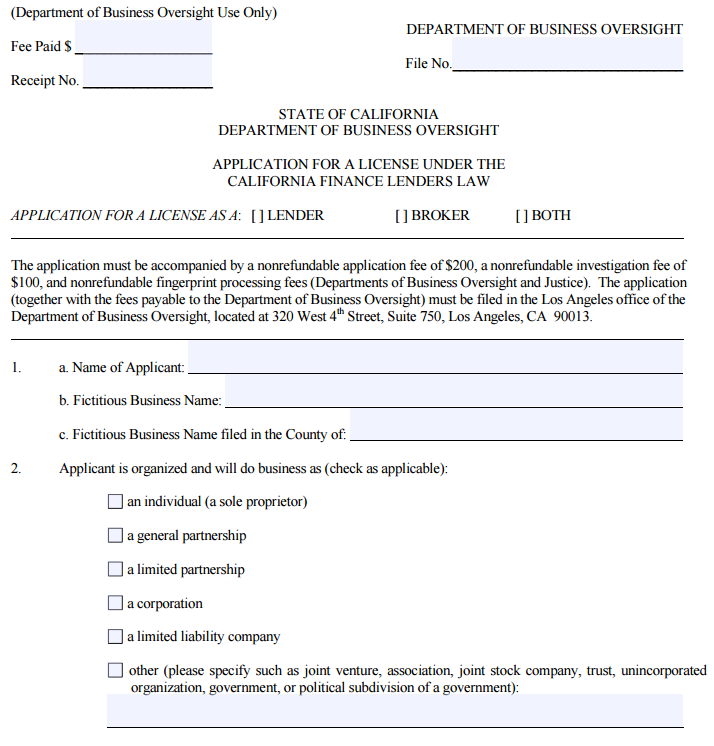

December 17, 2015Given the fact there have been a number of successful lawsuits against cash advance companies in California, many cash advance companies have decided to take a different route and get a lending license to provide loans to merchants in the state. If done correctly, this can allow companies to provide loans to merchants in California at roughly the same profit margins one could expect from a cash advance. Below I will discuss the process for obtaining a California lender’s license and some tips for making that process less painful.

To start, go to the California Department of Business Oversight and get the form titled “Application for a License Under the California Finance Lenders Law.” The application is long and detailed but don’t let that scare you. Most of the information you provide is really more related to letting the State know about your company and the main people that will be responsible for managing the lending operations. As you complete the form, one thing you do need to do is make sure you are very careful and meticulous as any small mistake will cause the application to be rejected making the process much longer.

To start, go to the California Department of Business Oversight and get the form titled “Application for a License Under the California Finance Lenders Law.” The application is long and detailed but don’t let that scare you. Most of the information you provide is really more related to letting the State know about your company and the main people that will be responsible for managing the lending operations. As you complete the form, one thing you do need to do is make sure you are very careful and meticulous as any small mistake will cause the application to be rejected making the process much longer.

The first part of the application requests basic information about your company and its officers. In filling out this and other parts of the application, it is essential to respond to all the questions. If you fail to miss just one response the application will be rejected. To that end, even if a question does not apply to you I find it better to respond “N/A” or “not applicable” rather than just leaving a blank. By doing that you force yourself to fill in every blank and therefore reduce the chances for missing a response resulting in a rejection of your application.

Also, you need to be very precise in your responses. I have experienced a situation where the examiner rejected an application because the name of the company was incorrectly spelled on the application. The name of the company was submitted on the application with “Inc” instead of the complete “Inc.” at the end of the company’s name. The examiners are very good at what they do and very thorough. You need to make sure the packet you submit is perfect and also that there are no inconsistencies in the document.

Another important point to remember is that the application requires you to name the person that will be responsible for running the location where the lending is occurring. The main requirement is that the person running the location must be physically present at the location. As a result, you could not manage a California office remotely from New York for instance. In another twist, if your principal location is out of state, you will need to get the license and fill out the main application for that out of state address. For the California location, you will need to fill out the short form application in addition to the main application and submit the short form application as part of the packet to allow the license to apply to the location in the state of California.

There are a number of exhibits you also have to provide as part of the process. Some of them are simple like a balance sheet for the company. It is acceptable that the company is new and has little in the way of assets. You just have to make sure you attach a balance sheet and that it is prepared in compliance with generally accepted accounting principles. I have seen times when the balance sheet was rejected because there was no line items for liabilities for instance, even though the company was new and therefore had none. It is probably wise to engage your accountant to make sure you submit a balance sheet that complies with those guidelines.

You also have to get a surety bond in the amount of $25,000. There are readily available bonding companies that specialize in providing these bonds. In addition, you need some other exhibits like a statement of good standing for your company, authorization for financial disclosure, social security number (on a separate exhibit), organizational chart and a few other documents. As with the rest of the application the key is to make sure you include everything they are asking for exactly as requested.

The most involved exhibit is the “Statement of Identity and Questionnaire.” That exhibit has to be filled out for each owner, officer and manager listed on the application. It requests detailed information going back 10 years for each person for items like residence address and work history.

In addition, there are a series of questions on topics such as whether the person has been involved in lawsuits, had any licenses revoked or declared bankruptcy. Fingerprints are also taken as part of the process. This part of the application is trying to vet the various people working for the company to make sure they are suitable to be in the lending business.

Once you have all the documents prepared, you need to put them together in a packet to send off to the Department of Business Oversight to be reviewed. Again, I cannot overemphasize how important it is to completely and accurately answer the questions and put the packet together. You need to make sure things are in the proper order and complete. Triple check the application for errors and to make sure that packet is presented in the best manner possible. You also need to determine the amount of fees to submit with the application. Then, send the package by overnight delivery to make sure you have proof of delivery.

So what happens next? Well there is usually a bit of a wait. Typically it takes 3 months or more to get a reply. If you have done your homework, you might get lucky and successfully get your license on the first try. If there are any deficiencies, you will get a response letter from the State detailing the items that need to be corrected in the application and a time frame in which you have to respond or the application is abandoned.

On the first go round, you are usually given at least 2 months so you should have plenty of time. Digest the things they want and provide the required information. The deficiency letters are very detailed so it should be easy to make the requested changes. Resubmit the requested items and wait for the next response. It could be in the form of another deficiency letter but it could be an approval of the license. Just keep on trying until you are finally successful.

That’s it, you are finally a licensed lender in California! But that is where the fun begins. You are subject to many laws in California and audits by the State. To get the right to operate as a licensed lender, you need to make sure you prepare your application correctly. Once you have done that, you need to get all your loan documents drafted in compliance with California law. Make sure you have adequate experience and professional help to take on those tasks.

Can California Lenders Pay Referral Fees to Unlicensed Brokers?

December 15, 2015 A new California law is drawing attention to a much-misunderstood issue – whether California Finance Lenders can pay referral fees to unlicensed ISOs. Effective January 1, 2016, the answer is yes, but only for commercial loans with an annual percentage rate of less than 36% where the lender reviews documents to verify the borrower’s ability to repay. These restrictions benefit non-profit lenders making business development loans, and shut out their higher-cost commercial lender competitors from paying referral fees to unlicensed ISOs.

A new California law is drawing attention to a much-misunderstood issue – whether California Finance Lenders can pay referral fees to unlicensed ISOs. Effective January 1, 2016, the answer is yes, but only for commercial loans with an annual percentage rate of less than 36% where the lender reviews documents to verify the borrower’s ability to repay. These restrictions benefit non-profit lenders making business development loans, and shut out their higher-cost commercial lender competitors from paying referral fees to unlicensed ISOs.

Existing regulations under California’s Finance Lender’s Law (“CFLL”) prohibit paying any compensation to unlicensed persons or companies for “soliciting or accepting applications for loans.” 10 CCR 1451(c). This prohibition does not apply to referrals for merchant cash advances or referrals to banks, which are not subject to the CFLL. A number of not-for-profit CFLL lenders offering business development loans complained that it was unfair that they could not pay referral fees to an unlicensed ISO while their higher-cost competitors, the merchant cash advance companies, could.

California SB 197, supported by Opportunity Fund, California’s largest not-for-profit commercial lender, and the California Association of Micro-Enterprise Organizations, a group of more than 170 organizations, agencies, and individuals dedicated to furthering micro-business development in California, aimed to remedy this perceived problem. According to an information sheet on SB 197 available on the Opportunity Fund’s web site:

Often, merchant advance companies offer less favorable terms to small businesses than commercial lenders; however, small businesses never learn about the commercial lenders that offer more favorable terms, because those lenders cannot compensate entities to refer business to them.

http://www.opportunityfund.org/media/blog/introducing-sb-197-(block)!/ (last accessed on December 9, 2015)

The legislature approved SB 197 and Gov. Jerry Brown signed it last October. Starting on January 1, 2016, a CFLL lender can pay a fee to an unlicensed person in connection with a referral of a prospective borrower if:

- The referral by the unlicensed person leads to the consummation of a commercial loan (defined as a loan with a principal amount of $5,000 or more the proceeds of which are intended by the borrower for use primarily for other than personal, family or household purposes);

- The loan contract provides for an annual percentage rate that does not exceed 36%; and

- Before approving the loan, the lender:

- Obtains documentation from the prospective borrower documenting the borrower’s commercial status. Examples of acceptable forms of documentation include, but are not limited to, a seller’s permit, business license, articles of incorporation, income tax returns showing business income, or bank account statements showing business income; and

- Performs underwriting and obtains documentation to ensure that the prospective borrower will have sufficient monthly gross revenue with which to repay the loan pursuant to the loan terms. The lender cannot make a loan if it determines through its underwriting that the prospective borrower’s total monthly expenses, including debt service payments on the loan for which the prospective borrower is being considered, will exceed the prospective borrower’s monthly gross revenue. Examples of acceptable forms of documentation for verifying current and projected gross monthly revenue and monthly expenses include, but are not limited to, tax returns, bank statements, merchant financial statements, business plans, business history, and industry-specific knowledge and experience. If the prospective borrower is a sole proprietor or a corporation and the loan will be secured by a personal guarantee provided by the owner, the lender must consider a credit report from at least one consumer credit reporting agency that compiles and maintains files on consumers on a nationwide basis.

The licensee must also maintain records of all compensation paid to unlicensed persons in connection with the referral of borrowers for a period of at least 4 years.

SB 197 also provides that a lender that pays compensation for a referral to an unlicensed person is liable for “any misrepresentation made to that borrower in connection with that loan.” It is not clear whether the lender is liable only for misrepresentations made by the unlicensed person who receives compensation for the referral, or if the regulator will interpret this provision more broadly. Further, lenders must provide such prospective borrowers this specific written statement in 10-point font or larger at the time the licensee receives an application for the loan:

You have been referred to us by [Name of Unlicensed Person]. If you are approved for the loan, we may pay a fee to [Name of Unlicensed Person] for the successful referral. [Licensee], and not [Name of Unlicensed Person] is the sole party authorized to offer a loan to you. You should ensure that you understand any loan offer we may extend to you before agreeing to the loan terms. If you wish to report a complaint about this loan transaction, you may contact the Department of Business Oversight at 1-866-ASK-CORP (1-866-275-2677), or file your complaint online at www.dbo.ca.gov.

Lenders must require prospective borrowers to acknowledge receipt of the statement in writing.

SB 197 defines “referral” to mean either the introduction of the borrower and the lender or the delivery to the lender of the borrower’s contact information. The following activities by an unlicensed person are not authorized:

- Participating in any loan negotiation;

- Counseling or advising the borrower about a loan;

- Participating in the preparation of any loan documents, including credit applications;

- Contacting the lender on behalf of the borrower other than to refer the borrower;

- Gathering loan documentation from the borrower or delivering the documentation to the lender;

- Communicating lending decisions or inquiries to the borrower;

- Participating in establishing any sales literature or marketing materials; and

- Obtaining the borrower’s signature on documents.

Many for-profit CFLL licensees may find the narrow exemption that permits CFLL licensees making commercial loans to accept referrals from non-licensed entities impractical. The industry may instead choose to focus on the existing prohibition against paying non-licensees for “soliciting or accepting applications for loans” to avoid the limitations on the loan terms.

California Finance Lenders Push Legislative Agenda in Response to Growth of Alternative Small Business Finance Industry

December 8, 2015On October 10, 2015, California Governor Jerry Brown signed into law SB 197, a bill that allows licensed California finance lenders to pay commissions to unlicensed persons that refer prospective commercial loan borrowers to licensees that offer certain types of lower cost loans. The bill was co-sponsored by Opportunity Fund and the California Association for Micro Enterprise Opportunity. The stated purpose of the bill was to “remove a competitive disadvantage that applies to C[alifornia Finance Lender Law (“CFLL”)] licensees making commercial loans.” As the bill’s legislative background explains,

Existing CFLL regulations prohibit CFLL licensees from paying any compensation to any person or company that is unlicensed, in exchange for the referral of business. This places CFLL licensees who make commercial loans at a competitive disadvantage relative to their direct competitors, who are not required to hold CFLL licenses and are thus not subject to this restriction. Two types of direct competitors that are not required to hold CFLL licenses include merchant advance companies (not required to be licensed under the CFLL, because they are advancing, rather than lending money) and companies that partner with banks (not required to be licensed under the CFLL, because the loans are made under the banks’ charters).

Prior to the passage of SB 197, a CFLL licensee was prohibited from paying a commission to an unlicensed person that referred a potential commercial loan borrower to the licensee. The California Code of Regulation states that “no finance company shall pay any compensation to an unlicensed person or company for soliciting or accepting applications for loans…” 10 CCR § 1451.

The new legislation overrides the regulatory restriction and permits licensees to pay compensation to unlicensed persons if certain conditions are met. A CFLL licensee may pay a commission to an unlicensed person if:

- The loan made to the borrower does not charge an annual interest rate in excess of 36%.

- The lender conducts an underwriting and obtains sufficient documentation to ensure that the borrower has the ability to repay the loan.

- The lender maintains records of all compensation paid to unlicensed persons for at least 4 years.

- The lender submits annual reports to the California Commissioner of Business Oversight.

While the bill permits an unlicensed person to refer potential borrowers to commercial lenders in exchange for compensation, it limits the activities in which the unlicensed person can engage. Under the new legislation, unlicensed persons that refer borrowers for compensation may not:

- Participate in any loan negotiation.

- Counsel a borrower about a loan.

- Prepare any loan documents, including credit applications.

- Contact the lender on the borrower’s behalf, other than to refer the borrower.

- Gather documentation of the borrower or obtain the borrower’s signature.

- Participate in the development of any sales or marketing materials.

To be clear, the purpose of SB 197 was not to prohibit licensees from paying compensation to unlicensed persons in exchange for borrower referrals (licensees have been prohibited from paying commissions to unlicensed persons since the CFLL was enacted). Instead, the bill allows certain lenders that charge annual rates under 36% to do something that they were previously prohibited from doing, i.e. pay commissions to unlicensed persons for commercial loan referrals.

CFPB Officially Begins Work on Small Business Data Collection Rule

November 23, 2015 On Friday, the CFPB issued its semiannual update to its rulemaking agenda. The agenda lists the Bureau’s major current and long-term initiatives. Long listed as a long-term item, the Small Business Data Collection rule required by section 1071 of Dodd-Frank is listed on the update as a current initiative.

On Friday, the CFPB issued its semiannual update to its rulemaking agenda. The agenda lists the Bureau’s major current and long-term initiatives. Long listed as a long-term item, the Small Business Data Collection rule required by section 1071 of Dodd-Frank is listed on the update as a current initiative.

The move is unsurprising given the number of lawmakers that have publicly called for implementation of the rule. CFPB director Richard Cordray also recently mentioned that the Bureau would begin its initial work on the rule early next year.

In the update, the Bureau states that it plans to build off of its recent revision to the home mortgage data reporting regulations as it develops the new Small Business Data Collection rule. The first stage of the CFPB’s work will focus on outreach and research. This will be followed by the development of proposed rules concerning the type of data to be collected as well the procedures, information safeguards, and privacy protections that will be required of the small business lenders that will report information to the Bureau.

Madden v. Midland Appealed to the US Supreme Court

November 15, 2015The Madden v. Midland decision has been appealed to the US Supreme Court and the future of non-bank lending potentially hangs in the balance. The introductory statement reads as follows:

This case presents a question which is critical to the operation of the national banking system and on which the courts of appeals are in conflict. The National Bank Act authorizes national banks to charge interest at particular rates on loans that they originate, and the Act has long been held to preempt conflicting state usury laws. The question presented here is whether, after a national bank sells or otherwise assigns a loan with a permissible interest rate to another entity, the Act continues to preempt the application of state usury laws to that loan. Put differently, the question presented concerns the extent to which a State may effectively regulate a national bank’s ability to set interest rates by imposing limitations that are triggered as soon as a loan is sold or otherwise assigned.

Several attorneys have said off the record that the likelihood the US Supreme Court would actually hear the case is about 100 to 1, because the issue lacks sex appeal. Gay Marriage, Obamacare, these are the type of things that make their way through the system.

Nevertheless, the petition argues the matter at hand:

The Second Circuit vacated the judgment, holding that the National Bank Act ceased to have preemptive effect once the national bank had assigned the loan to another entity. App., infra, 1a-18a. In so holding, the Second Circuit created a square conflict with the Eighth Circuit, and its reasoning is irreconcilable with that of the Fifth Circuit. The Second Circuit also rode roughshod over decisions of this Court that provide broad protection both for a national bank’s power to set interest rates and for its freedom from indirect regulation. And it cast aside the cardinal rule of usury, dating back centuries, that a loan which is valid when made cannot become usurious by virtue of a subsequent transaction.

The Second Circuit, of course, is home to much of the American financial-services industry. And if the Second Circuit’s decision is allowed to stand, it threatens to inflict catastrophic consequences on secondary markets that are essential to the operation of the national banking system and the availability of consumer credit. The markets have long functioned on the understanding that buyers may freely purchase loans from originators without fear that the loans will become invalid, an understanding uprooted by the Second Circuit’s decision in this case. It is no exaggeration to say that, in light of these practical consequences, this case presents one of the most significant legal issues currently facing the financial-services industry. Because the Second Circuit’s decision creates a conflict on such a vitally important question of federal law, and because there is an urgent need to resolve that conflict, the petition for a writ of certiorari should be granted.

Brian Korn, a partner at Manatt, Phelps and Phillips, told the LendAcademy blog in an interview that the Court could rule on the motion at any time and that it takes 4 out of 9 justices to agree to accept the case.

The plaintiff, Madden, has until December 10, 2015 to file a response to the petition.

Legal Brief: Kalamata v. Biz2Credit and Itria Ventures

October 20, 2015 The typical merchant cash advance contract contains language that prohibits the merchant from stacking multiple merchant cash advances. Some cash advance companies, however, induce merchants to stack. This is where the legal concept of “tortious interference with contract” comes in. Tortious interference places legal liability on a person who wrongfully causes another person to breach an existing contract. In the merchant cash advance industry, these lawsuits usually involve disputes over whether a stacking cash advance company intentionally caused a merchant to stack additional cash advances, thereby breaching an existing contract. This is an evolving area of the law and what conduct constitutes tortious interference is a hot topic in the legal field.

The typical merchant cash advance contract contains language that prohibits the merchant from stacking multiple merchant cash advances. Some cash advance companies, however, induce merchants to stack. This is where the legal concept of “tortious interference with contract” comes in. Tortious interference places legal liability on a person who wrongfully causes another person to breach an existing contract. In the merchant cash advance industry, these lawsuits usually involve disputes over whether a stacking cash advance company intentionally caused a merchant to stack additional cash advances, thereby breaching an existing contract. This is an evolving area of the law and what conduct constitutes tortious interference is a hot topic in the legal field.

Tortious interference is one of several claims that came up in Kalamata Capital’s recent lawsuit against Biz2Credit Inc. and Itria Ventures, LLC, and the court has already issued its first ruling on what conduct might constitute tortious interference with cash advance agreements.

Kalamata sued Biz2Credit and Itria for, among other things, stacking. One of Kalamata’s arguments was that Biz2Credit and Itria tortiously interfered with Kalamata’s contract. Biz2Credit and Itria filed a motion to dismiss. They argued that Kalamata failed to allege facts that would support a claim of tortious interference with contract. The court denied their motion because Kalamata alleged that 1) it had a business relationship with a merchant, 2) that Biz2Credit and Itria knew of that relationship and intentionally interfered with it, 3) that Biz2Credit and Itria acted solely out of malice, used improper means, illegal means, or means amounting to an independent tort, and 4) that the interference caused injury to Kalamata.

Kalamata alleged that, under its contract with Biz2Credit, Kalamata paid Biz2Credit commissions for referrals and for managing all of Kalamata’s accounts, including the referrals, on Biz2Credit’s online platform. Kalamata also alleged that the contract with Biz2Credit prohibited Biz2Credit from soliciting Kalamata’s merchants. The crux of the lawsuit is Kalamata’s claim that Biz2Credit secretly referred Kalamata’s merchants to Biz2Credit’s closely related company, Itria, and intentionally induced those merchants to stack additional cash advances in breach of the merchants’ contracts with Kalamata, despite an alleged agreement between Kalamata and Biz2Credit that prohibited Biz2Credit from doing so. Biz2Credit and Itria disputed Kalamata’s claims and argued that they were permitted to solicit any account that Biz2Credit referred to Kalamata or serviced for Kalamata.

Ultimately, the court found that if Biz2Credit was, solely for malicious purposes, sharing Kalamata’s confidential customer information with Itria, Kalamata’s competitor, and, if Itria and Biz2Credit were knowingly inducing Kalamata’s customers to breach their merchant agreements with Kalamata, then such conduct would rise to the level of tortious interference.

As this was a decision on a motion to dismiss, the motion focused on the legal sufficiency of Kalamata’s claims and did not address the merits of either party’s factual assertions.