Business Lending

OnDeck Expands Canadian Business with Merger

December 5, 2018 OnDeck announced today that it has entered into an agreement to merge its Toronto-based Canadian business with Evolocity Financial Group (Evolocity), an online small business funder headquartered in Montreal. OnDeck will have majority ownership of Evolocity and the combined entity will be rebranded as OnDeck Canada.

OnDeck announced today that it has entered into an agreement to merge its Toronto-based Canadian business with Evolocity Financial Group (Evolocity), an online small business funder headquartered in Montreal. OnDeck will have majority ownership of Evolocity and the combined entity will be rebranded as OnDeck Canada.

“The combination of OnDeck’s Canadian operations with Evolocity will create a leading online platform for small business financing throughout Canada and represents a significant investment in the Canadian market,” said Noah Breslow, Chairman and CEO of OnDeck. “There is an enormous need among underserved Canadian small businesses to access capital quickly and easily online.“

According to the announcement, “the transaction will combine the direct sales, operations, and local underwriting expertise of the Evolocity team with the marketing and business development capabilities of the OnDeck team.”

As part of the merger, Neil Wechsler, who is the CEO of Evolocity, will become the CEO of OnDeck Canada. And the management team will include Evolocity co-founders David Souaid as Chief Revenue Officer and Harley Greenspoon as Chief Operating Officer. OnDeck Canada will be governed by a Board of Directors chaired by Breslow and composed of existing OnDeck and Evolocity management.

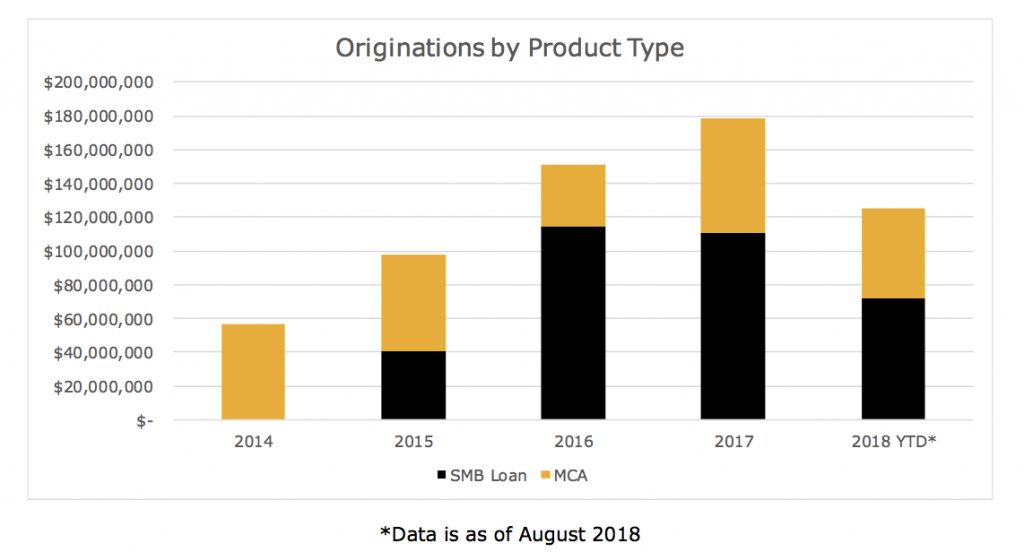

Currently, OnDeck offers a variety of loans up to $500,000 and lines of credit up to $100,000. Evolocity offers small business loans and an MCA product, from $10,000 to $300,000. deBanked inquired with OnDeck to see if OnDeck Canada will retain the MCA product from Evolocity, but has yet to hear back. Since OnDeck entered the Canadian market in 2014, it has originated over CAD $200 million in online small business loans there. Evolocity has provided over CAD $240 million of financing to Canadian small businesses since 2010.

Currently, OnDeck offers a variety of loans up to $500,000 and lines of credit up to $100,000. Evolocity offers small business loans and an MCA product, from $10,000 to $300,000. deBanked inquired with OnDeck to see if OnDeck Canada will retain the MCA product from Evolocity, but has yet to hear back. Since OnDeck entered the Canadian market in 2014, it has originated over CAD $200 million in online small business loans there. Evolocity has provided over CAD $240 million of financing to Canadian small businesses since 2010.

Investment in online small business lending in Canada is growing. IOU Financial, a Montreal-based small business funder that primarily funds American small businesses, told deBanked last month that they made a concerted marketing effort in the third quarter to reach Canadian small business owners. Meanwhile, Thinking Capital, a Canadian online small business funder, announced in July the launch of BillMarket, a service that provides Canadian small businesses with a credit grade (A through E), making it easier for them to get funded.

“BillMarket represents a cash flow revolution for the Canadian small business market,” said Jeff Mitelman, CEO of Thinking Capital, which has roughly 200 employees between its Toronto and Montreal offices.

According to a recent Canadian government report cited by OnDeck in its announcement today, there are 1.14 million small businesses in Canada that represent 97.9 percent of all businesses in the country. Also, small businesses employed over 8.2 million people in Canada, or 70.5 percent of the total private workforce.

According to a recent Canadian government report cited by OnDeck in its announcement today, there are 1.14 million small businesses in Canada that represent 97.9 percent of all businesses in the country. Also, small businesses employed over 8.2 million people in Canada, or 70.5 percent of the total private workforce.

Evan Marmott, founder of Canadian small business funder, Canacap, told deBanked earlier this year that unlike the saturated small business market in the U.S., the Canadian small business market is still ripe for growth. Not only this, he said that while the market is smaller in Canada, the default rates are generally lower and he found that Canadian merchants do less shopping around. He also said he has seen less fraud in Canada than in the U.S.

“For brokers, while commissions are lower, you could actually speak to business owners who are not being bombarded with calls [as they are in the U.S.] and have a much higher closing rate,” Marmott said.

Evolocity has 70 full-time employees and offices in Montreal, Vancouver and Marham, in the Toronto area. OnDeck has funded over $10 billion to small businesses and became a public company (NYSE: ONDK) in 2014. OnDeck is headquartered in New York.

“We are excited to join forces with OnDeck…to enhance our best in class digital financing solutions to small businesses across Canada,” said Wechsler, Evolocity CEO. “Additionally, this transaction will augment our data science and analytics capabilities to help deliver an unparalleled merchant experience.”

Popular Business-Lending Marketplace Dealstruck Restructures

December 3, 2018VALLEY STREAM, N.Y., Dec. 3, 2018 — Innovative online business-lending marketplace Dealstruck.com (which has been featured in CNBC, The New York Times, Forbes and many other publications) has reorganized. A private investment group of fintech experts acquired the company. “This acquisition represents a significant strategic opportunity for our client base,” said Dealstruck CEO Anthony Porrata.

Dealstruck is a leader in the alternative lending space. The company provides small and medium-sized business owners with seamless access to capital. Advances in technology make the process quick and efficient with minimal paperwork.

During the restructuring process, the company paused providing loans. “Recently, many people have asked, ‘What happened to Dealstruck?’ There were rumors that Dealstruck shut down but that was not true,” noted Porrata. “We’re happy to announce the Dealstruck news that a group of private investors has created a new ownership coalition that is leading a bold evolution for the company.” The new investment group combines a portfolio of existing small business capital providers with the highest technological advances in the field of online business loans.

Company leaders expect the change will help small businesses immensely. “Clients will see quicker approval turnarounds and a more streamlined process,” said Porrata. “This will also help clients who would not otherwise have equal access to growth opportunities.”

Vice President Chris Jones expects small business owners will be excited about the Dealstruck news. “This restructuring will allow us to approve more clients than ever before,” he smiled. “I’m looking forward to joining many new business ribbon-cutting ceremonies. Nothing gives us more pride than a grand opening.”

The reorganization allows Dealstruck to expand its mission while maintaining the personalized service that makes it so well known. The new management team has access to more capital and creative financing terms for Dealstruck clients.

About Dealstruck: As a leading online capital facilitator, Dealstruck connects small and medium-sized businesses with access to a variety of working capital options. These options help business owners find custom-tailored loans, so they can better manage their time and achieve their goals. For more information, visit dealstruck.com.

Contact:

Anthony Porrata – CEO

855-610-5626

info@dealstruck.com

What We Learned About Credibly From Credibly’s Securitization

November 29, 2018Today, Credibly CEO Ryan Rosett told deBanked that the company’s October securitization will be used, in part, to roll out its new Market Expansion Product (MXP), which will allow Credibly to service merchants with FICO scores as low as 500 and those that have been in business for less time.

“We believe the MXP will open up the funnel by allowing us to serve business owners that we previously couldn’t,” Rosett said.

Kroll Bond Rating Agency assigned preliminary ratings to three classes of notes as part of Credibly’s first securitization. Rosett said this securitization follows a large warehouse line of credit from SunTrust Bank which is also the primary underwriter, of the securitization.

In addition to the new MXP product, Rosett said that Credibly intends to launch a line of credit product in 2019. Currently, Credibly provides merchant cash advances up to $150,000, business expansion loans up to $250,000, with terms up to 24 months, and working capital loans up to $250,000 with terms up to 17 months. Rosett said that the company’s working capital loan is its most popular product.

In an interview yesterday with Benzinga, Rosett said that he has seen a strong increase in demand for Credibly’s products and that they are currently evaluating over 10,000 applications per month.

2017 net revenue before provisions: $33 million

2017 earnings: $1.4 million

Total shareholder equity: $18.7 million

Lifetime funding volume: $700+ million

Raw # of fundings: 17,000+

Majority owned by: Flexpoint Ford

# of employees: 140

Notable deal: Acquired the rights to service BizFi’s $250 million MCA portfolio in August 2017

Provides: Small business loans (in 37 states and D.C.) and merchant cash advances

Founded: 2010 by co-CEOs Edan King and Ryan Rosett

Generates deals via: Brokers and inside sales

Patriot Bank Expands SBA Lending

November 28, 2018 Connecticut-based Patriot Bank announced today the overall expansion of its small business lending operation. At the beginning of the month, it added to it board of directors Brent Ciurlino, a former SBA official who served as Director of the Office of Credit Risk Management for the SBA. There, he supervised the $105 billion SBA 7(a) and 504 loan debenture and portfolio programs.

Connecticut-based Patriot Bank announced today the overall expansion of its small business lending operation. At the beginning of the month, it added to it board of directors Brent Ciurlino, a former SBA official who served as Director of the Office of Credit Risk Management for the SBA. There, he supervised the $105 billion SBA 7(a) and 504 loan debenture and portfolio programs.

“As a banking executive and former federal regulator overseeing small business loan programs, Brent brings substantial expertise and value that will benefit Patriot Bank, its customers and its shareholders,” said Michael Carrazza, chairman and CEO of the bank. “As we build our small-business lending portfolio and look ahead to the goals we have set, Brent’s active involvement will bring a heightened dimension of operational, regulatory and risk management oversight.”

Patriot Bank became an approved SBA lender at the end of 2017, obtained “preferred lender” status with the SBA in September, and is currently opening SBA Business Development offices in the southeast, according to a story on the bank’s website. Additionally, according to the story, the bank signed a definitive purchase agreement in February of this year with Hana Small Business Lending Inc. for its $490 million SBA portfolio. Carrazza said at the time that this would help the bank become one of the country’s leading SBA 7(a) lenders.

Patriot Bank’s Director of SBA Lending Kevin Ferryman, himself a new hire this year, said that the bank’s goal is to enhance its traditional lending programs.

“We’re in a position now where we can approve loans for a lot more customers than we could do with our own internal policies,” he said.

Ferryman also acknowledged that having “preferred lender” status with the SBA allows the bank to process, close and service most SBA-guaranteed loans without prior SBA review.

“As a result, entrepreneurs and small community businesses can obtain their loans more quickly and efficiently,” Ferryman said.

Founded in 1994, Patriot Bank is a consumer and commercial bank with branches in affluent communities in Connecticut and one in Scarsdale, NY.

IOU Partners with FINSYNC to Fuel Growth

November 27, 2018 Montreal-based IOU Financial announced yesterday that it is partnering with FINSYNC in an effort to improve their customers’ experience and broaden access to new customers. FINSYNC is a cash flow management software and platform that allows businesses to collect income, pay bills, process payroll, automate accounting, and access financing through FINSYNC’s Lending Network.

Montreal-based IOU Financial announced yesterday that it is partnering with FINSYNC in an effort to improve their customers’ experience and broaden access to new customers. FINSYNC is a cash flow management software and platform that allows businesses to collect income, pay bills, process payroll, automate accounting, and access financing through FINSYNC’s Lending Network.

“FINSYNC’s innovative cash flow management solution helps business owners better assess the opportunity to access working capital based on past and projected cash flow,” said Christophe Choquart, VP of Strategic Partnerships at IOU Financial. “This is a totally new way to [support] growing businesses.”

FINSYNC provides almost all financing-related services except for the actual financing. According to its website, FINSYNC has partnerships with a number of other alternative funders, including OnDeck, Breakout Capital, BFS Capital and The Business Backer.

“This partnership greatly enhances the convenience of applying for working capital,” said Robert Gloer, President and COO of IOU Financial. “It gives merchants insight into what a cash infusion would look like [before they take out a loan.”

Through this partnership, IOU Financial’s marketing efforts will introduce potential merchants to FINSYNC’s payment, payroll and accounting services, while FINSYNC will offer IOU Financial an enhanced user experience, according to IOU Financial CEO Philip Marleau. He said that, for now, neither company is exchanging money with one another. It is purely a mutually beneficial partnership.

IOU Financial offers business loans of up to $300,000 to small business merchants in the U.S. and Canada. The company, which is traded publicly on the Toronto Stock Exchange, had a strong third quarter, with $36.1 million in originations, an 85% increase from the prior year. The lender’s average loan is $100,000 with a 12 month term, although they do offer terms up to 18 months.

Founded in 2009 by Gloer and CEO Phil Marleau, the company also has an office in Atlanta and has a total of about 40 employees.

SBA Loans Increase Slightly in 2018

November 26, 2018SBA total loan volume exceeded $30 billion with more than 72,000 approved loans for FY18 (October 1, 2017 through September 30, 2018), according to the SBA. The total volume is about the same as last year and there were approximately 4,000 more SBA loans issued this year compared to FY17.

Of the 72,000 SBA loans approved this year, 60,353 of them were 7(a) loans, totaling $25.37 billion. And 5,874 of the loans were 504 loans, totaling over $4.75 billion. This year, the SBA launched the 25-year Debenture, which offers an additional 60 months of financing at a fixed rate for small businesses. Since its introduction in April, over 1,000 debentures had been sold in FY18.

“The 25-year Debenture is designed to help free up cash flow and offer fixed rates in a rising interest rate environment for 504 borrowers and we are pleased to see over $1 billion has been disbursed in less than six months,” Associate Administrator for SBA’s Office of Capital Access William Manger said.

In FY18, there was notable growth in the SBA’s Microloan and Community Advantage Programs. In particular, over 5,000 loans were approved for over $72 million in the Microloan program and over 1,000 loans were approved for over $150 million in the SBA Community Advantage program.

Study Shows Small Business Loan Demand Highest Since 2012

November 26, 2018 A study released today reveals that American small businesses are eager to take business loans, with 48% planning to take out a loan in the next year, the highest level of demand since 2012. The study, called “Gimme Credit: Faster, Simpler, Safer Credit Main Street America,” was conducted by PayNet, which provides small business credit data, and Raddon, a research provider to financial institutions.

A study released today reveals that American small businesses are eager to take business loans, with 48% planning to take out a loan in the next year, the highest level of demand since 2012. The study, called “Gimme Credit: Faster, Simpler, Safer Credit Main Street America,” was conducted by PayNet, which provides small business credit data, and Raddon, a research provider to financial institutions.

According to the study, almost 65% of small businesses anticipate an increase in sales, the highest percentage in over 14 years. And 43% of small businesses have overall confidence in the economy.

“Small businesses are in full-on growth mode,” said PayNet President William Phelan. “They’re looking to banking partners for reasonable capital infusions, but are discouraged by slow reviews, impersonal processes and denials. This creates a huge opportunity for nimble community banks, credit unions, and alternative lenders to fill the void.”

Already, some larger banks like Chase and PNC have partnered with OnDeck’s ODX to enhance speed and fill this void.

Still, small business loan demand is often met with uncertainty from banks that remain wary of lending to small businesses in the wake of the financial crisis, according to the study. But Bill Handel, Chief Economist at Raddon, believes that lenders can change their ways, while still being fiscally responsible.

“It’s a recurring cycle,” Handel said. “Cumbersome underwriting practices increase the likelihood that lenders are either unwilling or unable to extend favorable terms to small businesses, which in turn discourages applications. Fortunately, lenders can take steps to improve their efficiency and profitability in this area.”

What are some of these steps? The study recommends the following:

- Segment applications by loan request size and reviews by loan risk profile.

- Deploy technology to assist in preparing applications, collecting data, and analyzing the business/loan.

- Optimize procedures by leveraging industry intelligence to improve their “decision engines.”

Selling a Home, Selling Commercial Financing – What’s the Difference?

November 16, 2018 Alternative funding brokers come from all different backgrounds, but for many them, being a broker is not their first job in sales. Some sold equipment, some sold cars and others sold homes. They were realtors. deBanked found two alternative funding brokers with a background in residential real estate and we asked them to compare the similarities and differences between selling a home and selling money.

Alternative funding brokers come from all different backgrounds, but for many them, being a broker is not their first job in sales. Some sold equipment, some sold cars and others sold homes. They were realtors. deBanked found two alternative funding brokers with a background in residential real estate and we asked them to compare the similarities and differences between selling a home and selling money.

Alex Alpert is the owner and CEO of Philadelphia-based Solomon Commercial Lending, which provides clients with a wide variety of funding from SBA loans, equipment leasing, factoring and some MCA. Before starting his company, he had worked as a residential realtor for about five years. When asked about his approach to selling a home versus selling money, he sees them as very different.

“When I consider non-investment home ownership, it is 100% emotional,” Alpert said. “If you think about it, the most expensive and most intimate and emotional purchase that you’re ever going to make is going to be your home. As people, we pour ourselves into our homes. Our homes speak so much about our personalities – what we like, what we don’t. It’s literally like a biography [of someone.]”

Alpert spoke about the intangibles involved in residential real estate, how a lot of it is about the feel of a home, which is highly subjective.

“Instead of you manipulating what they want, it’s just guiding them to reach that ‘ah-ha’ moment,” Alpert said. “I didn’t walk around the house with them and say ‘This is the bedroom and this is the bathroom.’ I would stay back and just say ‘Take a walk around, see how it fits, jump in the bed if you want to, and see how you feel.’ And when they came back down, one of my common first questions would be, ‘Can you picture yourself living here?’ Because that question makes you visualize yourself waking up there. If you can pick up on what the person is showing at that moment, you can guide them better…I think I’m successful because I’m honest, I’m transparent, and I will tell you things you won’t expect. And at the end of the day, that’s how you build referrals and address the needs of an emotional transaction.”

On the other hand, Alpert sees non-primary home deals as more transactional.

“When it comes to business, it’s much less personal,” Alpert said. “People will certainly do their research on who they engage with. Most all of my business comes from referrals. But still, you don’t know me from Adam, and you’re sending me over everything…With [business transactions,] it’s based on need and your ability to serve that need. The emotional part, just from the start, is not that present. It’s a need and solution type of approach.”

Alpert will work with clients with tens of millions of dollars in revenue. But he acknowledged that for some of his smaller “mom and pop shop” clients, transactions can be emotional, like with a small town dance studio client he is helping to secure a 7(a) SBA loan for.

James Celifarco, President of Horizon Financial Group in Brooklyn, which offers mostly small business loans and MCA, currently works as a realtor as well. He doesn’t see much of a difference in the way he approaches residential real estate clients versus small business merchants.

“I think they’re very similar in that if [people] are buying or selling a home, it’s their most coveted possession,” Celifarco said. “It’s what they’ve worked the hardest to obtain. It’s their biggest asset. And it’s the same thing when dealing with a business owner. Business owners are probably more passionate than a homeowner. Either way, if you’re dealing with a business owner or a homeowner, it’s their prized possession.”

While not using the word “emotional,” Celifarco seemed to suggest that non-residential real estate deals are just as emotional.

“[For both homeowners and business owners,] you really have to deal with kid gloves in that they play very close to the vest,” Celifarco said. “You have to have a certain approach where they feel comfortable speaking with you about their home and their finances or their business and their finances. They want to know that their information is protected.”

Celebrity residential real estate agent Ryan Serhant, who spoke at Broker Fair 2018, said that he lives be three rules to successful in real estate: Follow up, Follow through and Follow back. The last refers to following back a client on social media. This part might not always apply, but Celifarco said that the same persistence is required regardless of the sales client.

“It’s all sales,” he said. “You eat what you kill. You close a deal, you make money. You sell a house, you make money. If you don’t, if you’re not reaching out to your clients, you’re not going to make any money. It’s the same in that you get paid for how hard you work.”