Business Lending

Shopify Issued $93M in MCAs and Loans in Q2, Has Begun Offering Funding to Non-Shopify Payment Customers

August 4, 2019 Shopify, a publicly traded e-commerce platform, is quickly growing its merchant cash advance and loan originations through its Shopify Capital brand. The company issued $93M in Q2, up 36% year-over-year and an increase from the prior quarter of $5.2M. Shopify’s loan product is only available in Arizona, Idaho, Illinois, Indiana, Iowa, Kansas, Louisiana, Maine, North Carolina, South Carolina, Utah, Washington, Wisconsin, and Wyoming.

Shopify, a publicly traded e-commerce platform, is quickly growing its merchant cash advance and loan originations through its Shopify Capital brand. The company issued $93M in Q2, up 36% year-over-year and an increase from the prior quarter of $5.2M. Shopify’s loan product is only available in Arizona, Idaho, Illinois, Indiana, Iowa, Kansas, Louisiana, Maine, North Carolina, South Carolina, Utah, Washington, Wisconsin, and Wyoming.

The company also recently began offering funding to merchants who don’t use Shopify Payments but still use the Shopify platform.

On the quarterly earnings call, Shopify CFO Amy Shapero said in doing so “we still have significant visibility into their operations, we see their orders, we see the engagement with the platform. And so, we are very comfortable moving in that direction.” The move provides an opportunity to expand their eligible market by 10%, she added.

Furthermore, Shopify’s deals are performing well, the company claims. Shapero said “we’ve actually managed our loss ratio in a very, very tight range. In fact, it’s lower than the top of the range where we think we could go with this, which says the power of our algorithms are working.”

Shopify Capital has originated more than $180M in 2019 so far, indicating they may be surpass many competitors in the rankings this year. The company originated $277.1M in 2018.

Import/Export SMBs Introduced to Fintech Lending Options

August 2, 2019 Early this week TangoTrade announced its partnership with the online lender Fundation. TangoTrade, which deals primarily in payment assurances for US small business importers and exporters, will now offer alternative financing to SMBs with the help of Fundation.

Early this week TangoTrade announced its partnership with the online lender Fundation. TangoTrade, which deals primarily in payment assurances for US small business importers and exporters, will now offer alternative financing to SMBs with the help of Fundation.

The development is a reaction to the struggles faced by small businesses who engage in global trade. Sam Hayes, Co-founder and President of TangoTrade, said that “If you’re an SMB and a transaction goes south, it causes major problems for cash flow. There’s very little recourse you can have as a small business.”

Explaining that about one-third of all US imports and exports originate from small businesses (roughly 200,000 small businesses import and 300,000 export), Hayes notes that this is a large portion of the American economy that is potentially at risk. Especially when they are being left out to hang by banks whose debit and credit facilities come attached with lengthy approval wait times and complex application processes that are often too inconvenient for SMB owners.

The partnership with Fundation, which is backed by both Goldman-Sachs and SunTrust Bank, will enable TangoTrade to fund SMBs up to $1 million. As mentioned, TangoTrade also offers payment assurance for importers and exporters, which reduces payment risks by managing the entire payment process for both parties involved and offering imbursement via 130 currencies. As well as this, the option to wire funds globally is available through TangoTrade’s partnership with TempusFX.

These services have been centralized by TangoTrade, being made accessible through the business’s site, a decision that is key to the company’s vision of offering services through a platform, Hayes told deBanked. “We’ve seen innovations in cross-border payments and global sourcing, but not a whole lot in this particular area,” which is why TangoTrade is pushing to incorporate fintech in their dealings.

And this impetus has attracted attention. With a diverse set of investors ranging from Hard Yaka, which has ties to Square, Ripple, and Twitter; to Village Global, a venture capital network that is backed by Bill Gates, Jeff Bezos, and Mark Zuckerberg, TangoTrade has links to large names. Such diverse connections are mirrored in the company itself, with their team bringing together experience from MasterCard, Payoneer, NASDAQ, and Oracle.

A cabal of tech heads to be sure, Fundation CEO Sam Graziano says that this approach will “enable small businesses to access low-cost capital through an integrated user-friendly digital experience on their platform.”

Spotlight on deBanked CONNECT Toronto

July 30, 2019 As the heat of the Toronto sun split the stones outside, the crowd inside the Omni King Edward’s seventeenth-floor Crystal Ballroom mingled and munched as part of deBanked’s most recent CONNECT event.

As the heat of the Toronto sun split the stones outside, the crowd inside the Omni King Edward’s seventeenth-floor Crystal Ballroom mingled and munched as part of deBanked’s most recent CONNECT event.

The first of its kind to be held in Toronto, the CONNECT series are half-day events that take place in both San Diego and Miami as well. Despite not being as established as the latter two, Toronto proved just as eventful, with a variety of speakers and topics broached, as well as a host of attendees from differing backgrounds making an appearance. It was par for the course for an inaugural deBanked show with the attendance figures being reminiscent of deBanked’s first ever event in the USA, a market that’s 10x the size.

The day was kicked off by entrepreneur, a dragon on the Canadian Dragons’ Den series, and co-founder of Clearbanc, Michele Romanow, whose anecdotes detailed the adventures that accompany the beginning of a startup. Regaling the audience with the story of Evandale Caviar, Romanow began with telling the room of a post-college venture that saw her working tooth and nail to secure a fishing license, studying YouTube fish gutting tutorials that were exclusively in Russian, and getting her hands dirty with the other co-founders when the time came to put their time spent online to use.

But it wasn’t all blood and glory for Romanow, as the tale shifted from one of youthful expansion to one of reflection and acceptance of the unknown. Speaking on the effect of tech giants in various fields, Romanow explained that “we have no idea of how these industries will shape out.” The likes of Uber and AirBnb never planned change the world, just to change a product and thus solve a problem, and their meteoric rises are unpredictable as a result. Iteration, rather than innovation, is what drives a company forward according to Romanow.

But it wasn’t all blood and glory for Romanow, as the tale shifted from one of youthful expansion to one of reflection and acceptance of the unknown. Speaking on the effect of tech giants in various fields, Romanow explained that “we have no idea of how these industries will shape out.” The likes of Uber and AirBnb never planned change the world, just to change a product and thus solve a problem, and their meteoric rises are unpredictable as a result. Iteration, rather than innovation, is what drives a company forward according to Romanow.

And this sentiment was brought further along with the following panel, which featured Vlad Sherbatov of Smarter Loans, Paul Pitcher of SharpShooter Funding, and SEO expert Paul Teitelman, speaking on the trials and novelties of the sales and marketing scene. Offering wisdom on various aspects of the field, the three men covered the need to go beyond the traditional forms of advertising, instead looking outward towards unorthodox methods of marketing; the hardships that come with the grind of a sales job; and the role that SEO can play when raising public awareness of your company; respectively.

“It’s a matter of spreading the word,” one conference goer noted when asked about the sales panel afterwards. “Businesses have to know who we are, and we’re working on that.”

“It’s a matter of spreading the word,” one conference goer noted when asked about the sales panel afterwards. “Businesses have to know who we are, and we’re working on that.”

Similarly, Martin Fingerhut and Adam Atlas discussed the existing legal topics of note to Canadian alternative financing companies, as well as those incoming rulings that may be worth knowing about. Covering both the English-speaking provinces and Quebec, the duo gave a comprehensive crash course on the legal landscape of the industry, highlighting laws unique to the regions. Aaron Iannello of Top Funding considered the talk to be particularly engaging, commending it for relaying information that might otherwise be unknown to American companies.

Following this, Kevin Clark, President of Lendified, took to the stage to talk about the importance of the Canadian Lenders Association (CLA). Saying that in the absence of a regulatory body, the CLA seeks to offer guidance to those companies who are looking for it. Clark asserted that “it’s a good thing for our industry to have oversight from a regularly body,” and that he looks forward to the day when one is established.

Following this, Kevin Clark, President of Lendified, took to the stage to talk about the importance of the Canadian Lenders Association (CLA). Saying that in the absence of a regulatory body, the CLA seeks to offer guidance to those companies who are looking for it. Clark asserted that “it’s a good thing for our industry to have oversight from a regularly body,” and that he looks forward to the day when one is established.

And before wrapping up the speakers for the day, Clark was joined by IOU Financial’s President, Robert Gloer, to discuss contemporary risk management. Covering everything from the next recession to the emergence of AI, the pair, which accumulatively have been in the industry for decades, offered knowledge learnt from years of experience in both the pre- and post-crash eras.

And the prophesizing of what will be the next big episode to shake the industry continued beyond the day’s scheduled agenda as many attendees continued on well into the evening at smaller networking functions offsite.

As the sun started to touchdown on the tips of Toronto’s skyscrapers, the salvo of excited conversation briefly harmonized to produce a singular axiom, that there was an abundance of opportunity in Canada.

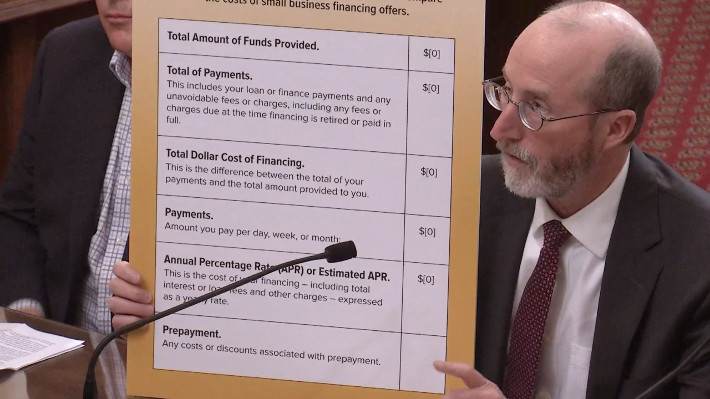

California DBO Making Progress On Finalizing Rules Required By The New Disclosure Law

July 29, 2019 Last October, California Governor Jerry Brown signed a new commercial finance disclosure bill into law. The bill, SB 1235, was a major source of debate in 2018 because of its tricky language to pressure factors and merchant cash advance providers into stating an Annual Percentage Rate on contracts with California businesses. The final version of the bill, however, delegated the final disclosure format requirements to the State’s primary financial regulator, the Department of Business Oversight (DBO).

Last October, California Governor Jerry Brown signed a new commercial finance disclosure bill into law. The bill, SB 1235, was a major source of debate in 2018 because of its tricky language to pressure factors and merchant cash advance providers into stating an Annual Percentage Rate on contracts with California businesses. The final version of the bill, however, delegated the final disclosure format requirements to the State’s primary financial regulator, the Department of Business Oversight (DBO).

The DBO then issued a public invitation to comment on how that format should work. They got 34 responses. Among them were Affirm, ApplePie Capital, Electronic Transactions Association, Commercial Finance Coalition, Fora Financial, Equipment Leasing and Finance Association, Innovative Lending Platform Association, International Factoring Association, Kapitus, OnDeck, PayPal, Rapid Finance, Small Business Finance Association, and Square Capital.

On Friday, the DBO published a draft of its rules along with a public invitation to comment further. The 32-page draft can be downloaded here. The opportunity to comment on this version of the rules ends on Sept 9th.

You can review the comments that companies submitted previously here.

Chase Ends Partnership With OnDeck, OnDeck Stock Tanks On Bucket of Mixed News

July 29, 2019 The market didn’t take too kindly to OnDeck’s Q2 earnings announcement on Monday. The stock price set a new all time intraday low of $3.01, down 24% from Friday’s close.

The market didn’t take too kindly to OnDeck’s Q2 earnings announcement on Monday. The stock price set a new all time intraday low of $3.01, down 24% from Friday’s close.

First, JPM Chase ended their partnership with OnDeck, the company said, bringing a 3-year relationship to a close. “We can’t speak for Chase and their change in priorities,” OnDeck CEO Noah Breslow said during the Q&A with analysts. “I don’t think it was specific to us.”

It was subsequently revealed that the relationship was never a significant moneymaker for their business to begin with. “On a standalone basis, it was a positive contributor,” the company said, but that it was “not a contributor to the bottom line profit.”

Breslow called the Chase deal a one-off that had some costs involved with it, but that they were optimistic about other deals with banks through their subsidiary ODX. “We do believe the drivers of this are not some fundamental readout on the ODX model,” he explained. “Again, we had a product that performs very well from an underwriting perspective. Customers loved it. We can’t speculate on why Chase made this particular decision. We just know it was specific to them.”

OnDeck also announced plans to pursue a bank charter and believed that the timing was right. Although they were “far along in [their] thinking,” they had not actually applied for a charter and they left the door open to possibly acquiring a chartered bank to achieve that goal. “I think the next logical milestone would be to look for some kind of either application for such a charter, but we’re not prepared to talk about a timeframe over which that would occur,” the company said.

Originations shrank to $592M, down from $636M in the previous quarter. “We do expect a return to sequential originations growth in the third quarter,” Breslow said.

The company also plans to buy back up to $50 million worth of stock to boost the share price.

PayPal Begins Offering Business Loans in Canada

July 28, 2019 PayPal has extended its popular working capital business loan program to Canada, according to company CEO Dan Schulman.

PayPal has extended its popular working capital business loan program to Canada, according to company CEO Dan Schulman.

“This quarter, we began offering our PayPal business loan product to PayPal merchants in Canada, allowing them to access financing to build and sustain their businesses,” he said during the Q2 conference call. “This follows the expansion of our business financing solutions to Germany in Q4 2018 and in Mexico earlier this year in partnership with Mexican lending platform Konfio.”

deBanked ranked PayPal as the leading alternative small business finance company by originations in 2018. They are followed by OnDeck, Kabbage, Square, and Amazon.

Become: The Who, What, and Why of a Rebrand

July 23, 2019Last week Lending Express rebranded to Become. Founded in 2016, the company, which educates businesses looking for loans on how to appear more attractive to funders, was spearheaded by CEO Eden Amirav in Australia originally, with an eventual expansion to the US. Three years in, the company has over 50 lending partners across its two markets, a record of having facilitated over $150 million in funding, and more than 150,000 members on their platforms. As indicators of progress go, these are far from undesirable. So, when things were going so well, what led Amirav to decide to rebrand?

In short, the company had evolved into something different from what it was in 2016, and its name, logo, and stylized website fonts had to reflect that. Thus, Lending Express became Become.

Gone are many of the aesthetic features of Lending Express, replaced with fresher counterparts, but beyond the brand, much of the company has remained. Amirav, the ex-pro gamer who was national champion of Israel in Warcraft 3 when he was a teenager, is still around; their AI-powered funding odds calculator, LendingScore, continues to be used; and their offices in both the US and Israel remain open.

Gone are many of the aesthetic features of Lending Express, replaced with fresher counterparts, but beyond the brand, much of the company has remained. Amirav, the ex-pro gamer who was national champion of Israel in Warcraft 3 when he was a teenager, is still around; their AI-powered funding odds calculator, LendingScore, continues to be used; and their offices in both the US and Israel remain open.

Rather than being hoarded remnants of times past, what Become has brought with it from Lending Express were deemed necessary by Amirav when discussing what was required to execute the rebrand. Explaining that before planning for the future of the rebrand even begun, Lending Express worked for months to comprehensively take stock of itself, and Amirav noted that all hands were needed and the entire company pitched in. Whether it was ensuring that URL links which once directed people to Lending Express now went to Become, or the drafting up of the new name, much of the work that went into the business’s metamorphosis came from within the company. Of course, Become specializes is helping small businesses get approved for loans, so not everything could be done by themselves, which is where a marketing firm came in to aid them with the crafting of the company’s new image.

As to the motives of the rebrand, the brief explanation given above doesn’t cut it. A blog post on Become’s website explains the origins of both names. With Lending Express having a ‘do-what-it-say-on-the-tin’ aspect to it, Become is much more abstract in how it reflects the company. Noting that Become originates from both within the company and without, Amirav explains the name owes itself to Lending Express’s development into a “no human-touch, all-tech based” company, following LendingScore’s creation; as well as the business’s ability to help its customers achieve their goals, enabling them to become what they wish.

Rebranding comes at a massive financial cost, with no guarantee of an immediate large payout upon launch, but as Amirav asserted, the switch to Become was necessary in his long-term plan for the company, as the “stress [of the rebrand] is offset by the goal of where they want to go.” “We’re well equipped with people, resources, and vision,” Amirav went on to say, and as well as this, he believes in the importance of a strong brand, regardless of industry, claiming that it “becomes a power to work with.”

And with their new logo and four-tone color palette sure to catch eyes, perhaps Amirav’s gamble will pay off. For now, he’s content with his rebrand going public, the continued business of Become, and the “shareholders [being] happy.”