Business Lending

Fintech Small Business Lender Origination Volume Snapshot

January 16, 2026It was full speed ahead in 2025. Here’s how the origination volume stats were trending among the biggest fintech small business lenders for the first nine months of last year.

| Lender | First Three Quarters 2025 | All of 2024 |

| Square Loans | $5 billion | $5.7 billion |

| BHG Financial | $4.4 billion | $3.7 billion |

| Enova | $4 billion | $3.98 billion |

| Shopify Capital | $2.8 billion | $3 billion |

| PayPal | $1.6 billion | $3 billion |

deBanked tracks fintech small business lenders that publicly report (or privately report to us) their origination volumes. Square Loans became the largest in 2021 and has held on to the top spot ever since. Their advantage (and limitation) is that they lend only to merchants in their POS payments ecosystem.

A dark horse not listed, because precise origination volumes are not available, is Parafin, an embedded lender that works through partnerships with DoorDash, Amazon, Walmart, TikTok and more. At last report, the company said it had made more than $14 billion in offers.

California Partnered With a Revenue Based Financing Provider

January 13, 2026On the California Small Business Loan Match website operated by The California Infrastructure and Economic Development Bank (IBank), is a list of vetted partner small business lenders that the state guarantees loans for. One of those lenders is AltCap California which actually offers revenue based financing.

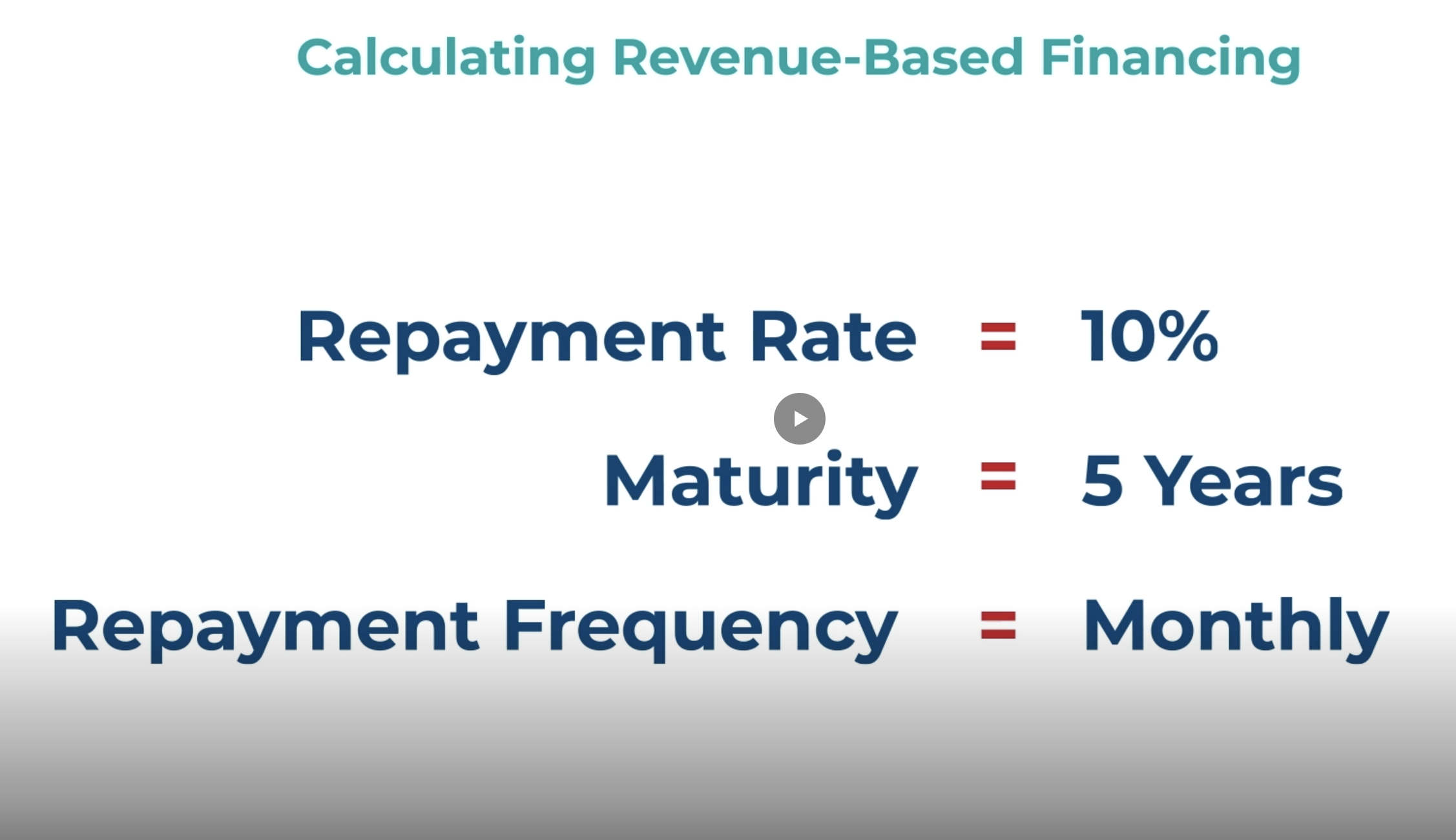

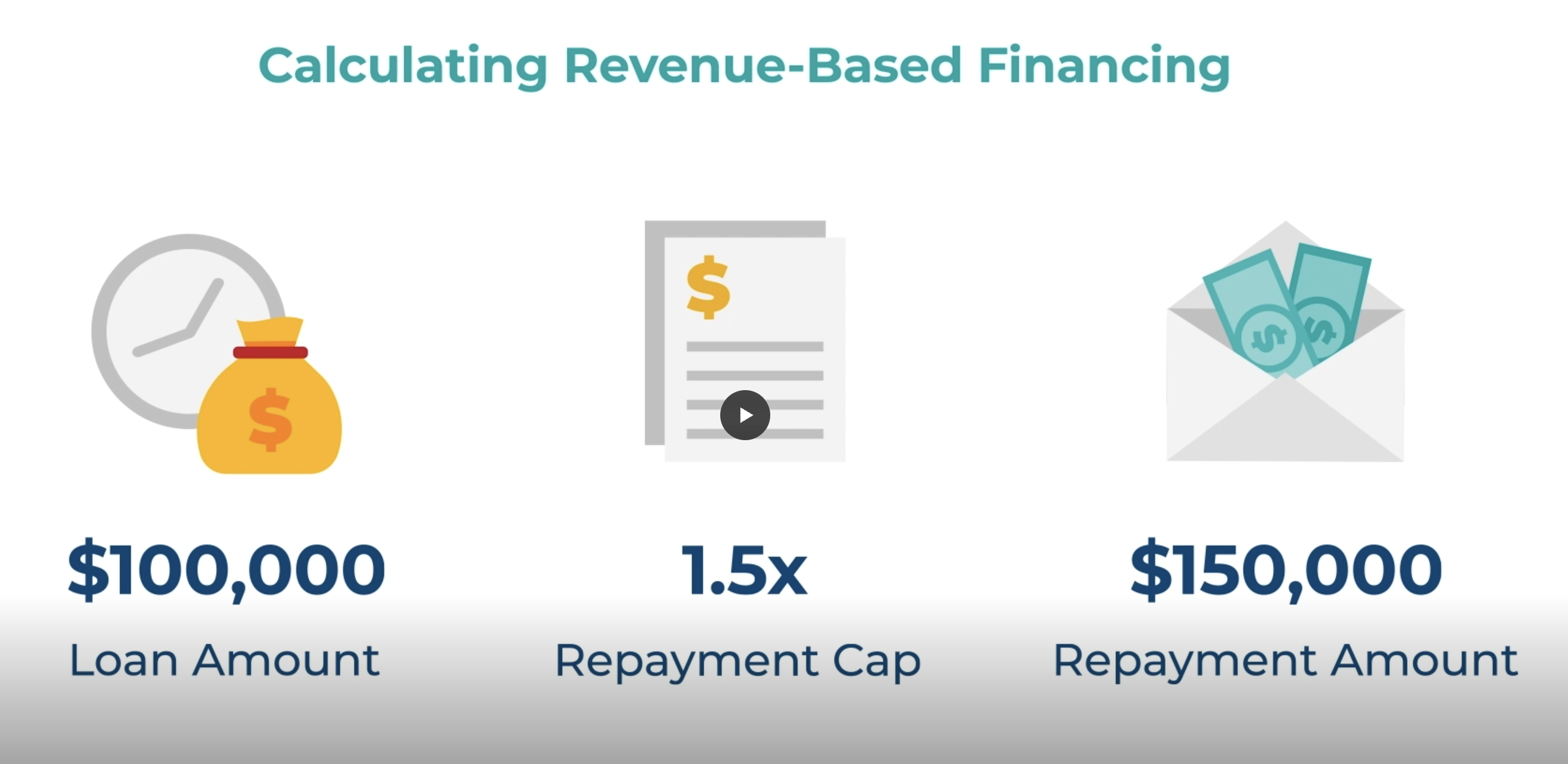

At face value, AltCap describes the cost of its revenue based financing as having to pay up to 7.5% of monthly revenue with a total cost of 1.4x to 1.5x. Its multi-part video education series describes revenue based financing costs as working in the following way:

Repayment Cap: Multiple of the total loan amount used to calculate the set dollar amount to be repaid. (Total Cost of Capital)

Repayment Rate: Share of revenue taken to repay the loan. (Holdback %)

It reinforces this in its Case Study example of Juice Boost (the 2nd video) where it explains that the metrics used to calculate the cost of Revenue Based Financing are the Repayment Cap (factor rate) and Repayment Rate (holdback %).

In its final video, the 4th video, it tells borrowers to inquire about APRs to make comparisons against companies like Square, Amazon, Stripe, and Shopify.

“Revenue-Based Financing allows small businesses to raise funds by pledging a percentage of future, ongoing revenues in exchange for capital provided by a lender,” the website says. “Revenue-Based Financing is different than debt financing. Interest is not paid on an outstanding loan balance and there are no fixed payments. Instead, payments are proportional to a firm’s performance, offering a flexible, patient source of financing.”

New Year, New Lenders?

January 5, 2026There’s a couple new lenders on the block to keep an eye on.

One of them is named Slope. Backed by both JPMorgan and OpenAI CEO Sam Altman, Slope offers revolving lines of credit up to $5 million. And they’re already out there. Seemingly overnight they’ve become capital providers for a number of large e-commerce platforms including Amazon and Walmart and are now listed alongside Parafin on both. When they announced their deal last year with JPM, they said that the US embedded financing market was worth $20 billion and that the B2B economy was $125 trillion. Slope is also offering a new AI underwriting tool.

Another is named Uncapped. Walmart says that Uncapped offers term loans while Amazon says that Uncapped offers lines of credit. The Uncapped website says that they offer loans from $10,000 to $2 million and that they accept business from business loan brokers. The company was technically founded in 2019, but in the UK.

Success and Lessons Learned From Small Business Finance Industry Vets

December 11, 2025 “In October, the company did $23 million+ and it was our best month ever,” says Eddie DeAngelis, founder and CEO of QualiFi, a full-service business loan brokerage.

“In October, the company did $23 million+ and it was our best month ever,” says Eddie DeAngelis, founder and CEO of QualiFi, a full-service business loan brokerage.

Talk to anyone in the industry and it always seems to be their best month, quarter, or year, but that’s just happenstance since those same people will also tell you—if they’ve been in it long enough—that success is not a straight shot up. They’ll also say that success is defined on their own terms, not by other people’s measures.

In DeAngelis’ case, for example, the origination figure, which comprised a mixture of LOCs, term loans, HELOCs, SBAs, and equipment financing, is all the more celebratory because the company accomplished it with just 13 funding reps at the time.

“It just shows how efficient our business model is,” DeAngelis says, “so that’s the number that I’m really proud of, which is 13 reps.”

Jared Weitz, CEO of United Capital Source, a small business finance marketplace, had a similar perspective, sharing that at one point he had 27 employees and now operates with 17—but the 17 are producing the same output as the 27.

“Ten less people, less expenses, same numbers, higher net margin and profit,” Weitz says. He explained that he spent time dissecting his P&L, structures, and systems to maximize efficiencies to get where he wants to be.

“I’ve always viewed it as ‘am I profitable every year?’” Weitz says. “‘Do I have concentration where, if 3,4, 5, [lenders] in my portfolio go out, am I screwed? Can I grow without body count? Can I create more efficiencies in my business through automations, technologies, different marketing and grow without body count?’ I’ve done that very well.”

Zach Ramirez, CEO of Calldrive, a pay-per-call marketing and consulting company, also has experience running brokerage shops.

“I found that my skillset, I was great at sales. I still am good at sales, but I think my real skill is building operations. I’ll be honest, one of my weaknesses is I’m not really that great at managing big groups of people,” Ramirez says.

In this regard, Ramirez also thought deeply about maximizing efficiencies rather than maximizing headcount, and says that “I found that what I do enjoy doing is building the infrastructure, the marketing, the sales processes, all the metrics and KPIs, and building the CRM and all the automations.”

Between that and his mountain of firsthand experience working at and operating brokerages, Ramirez is often called upon these days as a consultant for ISOs to help fix or improve all of those things.

Chad Otar, CEO of Lending Valley, a revenue-based financing provider, shrugs at the milestone benchmarks some of his competitors tout and explains that it’s not a race for publicity but rather a marathon of good economics. Otar, for example, says his company funds from its own self-funded balance sheet and has no incentive to be anything less than prudent.

“I’m not looking for market share,” Otar says. “I’m just looking for, you know, a calm, collected life at the end of the day.”

Through all the years Otar has been working in the industry, he says he’s seen the cycle of jaw-dropping deals that, while they may still be more expensive than a bank loan, are unlikely to yield a financial incentive for him to risk participating in.

“And I’m like, no, no. I’ll just stick to what I know, stick to what I like,” he says.

All four executives have the benefit of experience under their belts. Otar has worked in the industry for 19 years, Weitz for 20, Ramirez for 16, and DeAngelis for 12.

What they all have in common is a deep love for the game.

“It’s a delight, I love this #$@&*!-ing industry,” Ramirez says.

“I wouldn’t trade it for the world. I love this industry a lot,” echoes DeAngelis.

Weitz and Otar expressed similar sentiments.

DeAngelis, who had a couple of decades’ worth of experience as a traditional business owner in screenprinting and designer fragrance wholesaling, says that he loves talking to business owners, overseeing operations, and building relationships with partners.

Weitz says it’s been a joy to watch long-term members of his team go through their own life milestones, like going from an apartment to marriage to a home to kids.

“They’ve seen growth also, which really also means we’ve shown growth to not just our clients but our staff,” Weitz says. “These are really good recognition signs that we’re doing pretty good, which is also how I define success.”

If you’re earlier on in your career or entrepreneurial journey, know that there are going to be rough times—especially in this industry.

“My very first job selling finance was for [a mentor],” says Ramirez. “I was probably 19 or something, or 20, and he always said, ‘when you build your business, put your blinders on and only focus on your business and you’ll be instantly rich in 20 years.’”

Ramirez says that the march toward success is kind of like going to the gym. There are people who give up on a routine after three months because they think they’ve put in enough time to judge the final outcome and never truly follow through. And then there are those who stick with a routine, realize that they’re incrementally moving toward their goal, and eventually get there. Ramirez says he has been guilty of surrendering too soon in the past and has also fallen victim to shiny object syndrome. In one example of the latter, he said his previous ISO became overly caught up with selling Employee Retention Tax Credits (ERTC/ERC) during COVID, to the point where it overwhelmed and negatively impacted what had been a well-run business.

“It was a waste of time and energy more than anything, but also cash, because I didn’t remain true and focused to my major core expertise or my core area of competency,” Ramirez says. “I think we lost probably over a full year. We went the wrong direction.”

Otar, meanwhile, says he has felt the pressure as a funder in an increasingly competitive environment with demanding brokers. In one example, he says that while he normally sticks to his principles about not doing same-day fundings, he became convinced to make an exception—and it came back to bite him.

“I did a same-day funding and the next morning on the first Decision Logic, there’s four different positions in there already.”

In his view, that completely changed the risk profile of the deal and produced immediate regret. “That’s why I’m not advocating for same-day funding. I am not advocating for [online] checkouts,” he says. “I’m not doing any of that. I’m still sticking to what I know best, and it’s the reason why I have longevity in this industry.”

Otar adds that he is still employing automation, tools, and systems, and running a modern operation, but he thinks very carefully about each decision.

For Weitz, one of the big defining moments in his business was realizing that concentration risk can be existential. In an industry that prides itself on strong relationships, putting too many eggs in one basket can produce unforeseen consequences if a lender or funder disappears. And what are the odds? High enough that it happened to him. In the early days of United Capital Source, two large funding partners ceased operations at the same time, one of which comprised nearly half of his company’s entire portfolio. That not only jeopardized renewals but also the valuable volume bonus relationships he had with both.

“I know plenty of large brokers who make their profits solely from volume bonuses,” Weitz says. Fortunately, he recovered—and it gave him the chance to refactor his strategy to mitigate future fallout.

DeAngelis says that things can go from great to not good at all in a very short time. In one example, he said that six months after being featured positively in a deBanked story in early 2023, his company QualiFi hit such a snag that he had to temporarily take himself off payroll.

“We just ran into this down spurt where we had a really bad month,” DeAngelis says. “We’ve been there before, right? Another month, another really bad month. ‘Okay, so now back-to-back months. What’s going on? June, July, another bad month. Now it’s a bad quarter,’ and we just were spiraling down, like revenues dropping 30%, we’re starting to stress with the bills, like, ‘what the hell’s going on?’”

They knew they didn’t forget how to execute, but they made tweaks where they could. Like Ramirez’s gym analogy, DeAngelis said they didn’t completely change what they were doing—they stayed the course.

“Our answer was to just keep our heads down, just keep pushing, make some changes and start watching what we’re spending and just barrel through and push through,” DeAngelis says. “And then when we got to October [2023], is when things started to turn for us.”

Two years later, that recent $23 million funding month is a milestone that arose from going through the bad to get to the good. The last several months have also come in at over $15 million.

Some founders try to leverage milestones into additional growth before they’re ready, but DeAngelis—who has been down this road before, including with a previous company he started that was acquired by Nav—says it’s become important to look at each portion of the business as its own business. Hiring and onboarding, for example, has become its own structured operation.

“Before when we lost a rep or we needed to hire someone, we’d hire like the first two to come through the door and just put them on the phones, right?” DeAngelis says. “Those days are done. So the hiring process, we’re super selective. We want to make sure it’s a really good fit for the candidate, as much as this is for us, for long-term sustainability.”

DeAngelis has added a few more reps since the earlier-mentioned 13 and is being cautious about how they approach growth from here.

Ramirez, meanwhile, says that sometimes it helps to look at a problem in reverse. A common gripe these days is that the small business finance market is getting too crowded and squeezing margins (and ethics).

“If I look at everything from the perspective of, ‘I’m an ISO, and there’s more ISOs coming in,’ I understand why they would feel threatened,” Ramirez says. “Because… we’re all fighting for the same pool of merchants, essentially. I would respond with, ‘well, why don’t you help them?’ Instead of being fearful, then why don’t you help them? Why don’t you find these other smaller ISOs and help them do business the right way. Consult with them, charge them for that.”

Ramirez’s outlook embraces the spirit that success in the industry is not limited to being the best broker or the best lender, but about spotting opportunities and being brave enough to capitalize on them.

For Weitz, that meant diversifying early on beyond just one product. United Capital Source offers LOCs, HELOCs, SBA loans, term loans, revenue-based financing, equipment financing, and more. The result is long-term client relationships that shift between products as needs evolve—some going back to the company’s inception 15 years ago. Weitz also notes that not all new competition is real competition: his team conducts themselves with a level of expertise and best practices that they believe clearly distinguishes them.

For Otar, seeing a crowd rush into something doesn’t necessarily indicate a real opportunity, at least not economically. Unless the play is for market share or another specific objective, he considers patience and vigilance his advantages.

“I’ve been through the ringer,” Otar says. “I started this a long time ago. I was an opener, I was an originator, I was a collection guy, I was an underwriter, I’ve seen it all. I don’t think there’s one area in this industry that I haven’t been able to cover yet.”

“I’m here for the long run, not overnight,” Otar adds. As part of that, he prides himself on relationships not only with brokers but with every merchant he funds.

“My mom, when I first started, she had said this, ‘there’s three things that you don’t mess around with in people’s lives: their money, their spouse, and their car.’”

Realizing that his business involves one of those three, he has made it his mission to manage it with care.

“If you look at Lending Valley’s reviews, we’re at 5.0 right now, every single one of them. You could give them a call and they’ll be like, ‘Chad is amazing,’ because I try to keep them on with me.”

For DeAngelis, part of success is giving back. For example, they recently started a charity drive in the office where each month a different employee selects a charity and the company donates to it.

“We started with a small donation of like $500 a month,” DeAngelis says. “And it started really catching on, and I loved it, and got everybody involved. And we talk about it every month. Somebody picks a charity, tells us why it’s special to them, and then they give us some updates on it.”

“I just want to say that ever since we started doing that, even when we were struggling, our business just literally made a skyrocket transformation,” DeAngelis adds. “Over the last year, we’ve doubled and tripled and almost quadrupled our fundings and our revenues.”

For Ramirez, he says that “Last year was one of the best financial years of my life.” He used some of the earnings from it to acquire a small telecom company, which has become another valuable component of his overarching strategy. For younger people entering the space, he’s certain that this business is here to stay.

“The industry is not going anywhere,” he says. “Is it going to fluctuate? Is it going to change? Absolutely.”

Weitz, now two decades in, also concludes that by any rational measure, this business will continue to provide opportunities—as long as one evolves with the times.

“People are always going to need homes,” Weitz explains. “People are always going to borrow against assets. Businesses will never go away, ever, ever, ever, and they will also never, ever, ever have enough capital to grow themselves. They’re always going to need an outside source. This is the way the world has worked for a thousand years. So that won’t change. How people access it will change. The cost will change. The products will change. The need will not. So as long as you’re shifting with that, you’re in an industry where that need is still abundant.”

Otar says, “At the end of the day, I’m very happy with what I do every day. It makes me excited to wake up and actually want to go to work. It’s like I don’t have a job per se. They say, ‘if you have something that you love to do every day, it’s not a job.’ It just becomes a habit at this point. And I enjoy my habit.”

QuickBooks Capital Originates $1.3B in Latest Fiscal Quarter

December 10, 2025Intuit’s QuickBooks Capital is growing tremendously. The company originated $1.3B in term loans to small businesses for the fiscal quarter ending October 31, 2025, a 100% increase over the same period last year.

For the company’s previous full 2025 fiscal year which ended on July 31, 2025, the company had originated $3.5B in term loans, up from $1.8B in FY 2024. The figures put them near the top of all online small business lenders that deBanked tracks.

Intuit hardly mentions its term loan business in its quarterly earnings since other business lines including the QuickBooks software, TurboTax, and Mailchimp dominate. The term loans are marketed inside the QuickBooks software in a style of marketing known as embedded lending. The loans are technically issued by bank partners and Intuit buys the loans back from them.

‘Face-to-Face is a Must In This Industry’: How Julian Hernandez of Idea Financial Earned a Trophy Along The Way

November 24, 2025

“Face-to-face interactions are a must in our industry, and not only through conferences but even though we’re based out of Miami, I’m very familiar with the Long Island Railroad,” said Julian Hernandez, Director of Revenue at Idea Financial.

On multiple occasions, Hernandez has gone from New York City to eastern Long Island and then back again to meet with referral partners. It’s part of his job, meeting face-to-face with ISOs, and working with them to maximize the spread of Idea’s business line of credit products. He says through this experience he’s actually become “best buddies” with the LIRR.

“It’s good for morale, it’s good for relationships. It’s good not only for the reps internally on my end, but I’m sure for the reps on [the ISOs’] end to see and put a face to the lender that they’re always working with,” he said.

Hernandez will go wherever it’s necessary. Just last month that initiative placed him on the opposite side of the country, in a room full of ISOs and competitors that had gathered to play poker on the eve of the big B2B Finance Expo at the Wynn in Las Vegas. For Hernandez, who was born and raised in Colombia and only ever plays poker in a casual setting with friends, he had not gone in with any expectation of winning the friendly tournament. He wanted to network.

“That’s probably one of the main reasons why I wanted to join the tournament,” Hernandez said. “It’s just an opportunity for us, for anyone really that goes to the conference, to connect with either people that they know from the industry, or branch out or meet with new faces in an environment that isn’t so corporate.”

As the cards were dealt and the hands played, Hernandez found himself at the final table of the night and walked away with 2nd place overall, a title that garnered him a trophy and a small prize.

As the cards were dealt and the hands played, Hernandez found himself at the final table of the night and walked away with 2nd place overall, a title that garnered him a trophy and a small prize.

While he was happy to earn the rank of #2, it was the social setting of it all that he felt was the best part.

“It’s more of a relaxed environment where people are just having a good time, playing a game, having a drink, and really just getting to know each other on a personal level,” Hernandez said. “That’s the best kind of way to make relationships, right? It’s kind of like when people always say the best kind of business is made on a golf course.”

But in the two days that followed at B2B Finance Expo, Hernandez and the Idea team that was there along with him were in business mode.

“97% of our business is through ISO channels and through all the relationships we’ve established with brokers in our industry, and we’re looking to expand that further,” Hernandez said, noting that there are big growth plans in the works for 2026.

Idea’s line of credit is not like an MCA or the term loans commonly found around the industry. It’s a true revolving line. After every payment made, it replenishes the line. The process to get approved is quick and easy. Hernandez said that some brokers are shocked by how good it is and that larger businesses, ones that tend to be the most rate sensitive, find it very attractive.

Idea’s line of credit is not like an MCA or the term loans commonly found around the industry. It’s a true revolving line. After every payment made, it replenishes the line. The process to get approved is quick and easy. Hernandez said that some brokers are shocked by how good it is and that larger businesses, ones that tend to be the most rate sensitive, find it very attractive.

When deBanked first covered Idea Financial in 2019, Hernandez had not yet joined the company. He came on board the following year during covid and started in an entry level position. He’s since moved up the ranks and now oversees the entire sales and marketing department, which includes anything from ISO relations to marketing. He cites the team and the structure of how it operates as being the key to success. One of the things he first learned when he started was that Idea Financial was always looking to help businesses one way or another.

“I found my way to Idea Financial and have loved it ever since,” Hernandez said.

And while business and networking are important parts of the job, regardless of where that takes him, he is proud of how well he did in that poker tournament at B2B Finance Expo.

“I was happy with my 2nd place trophy,” Hernandez said. “It’s actually right there,” he exclaimed while pointing at it. “It’s back in my office!”

B2B Finance Expo 2025 Recap

November 12, 2025B2B Finance Expo 2025 was a tremendous success! This conference featured a larger number of attendees, exhibitors, and speakers from across the spectrum of commercial finance and small business lending than the previous inaugural year.

B2B FINANCE EXPO 2025 PHOTOS HERE

VIDEO INTERVIEWS FROM THE RED CARPET HERE

If you want a copy of your interview video file, email events@debanked.com.

To learn more about the Small Business Finance Association, contact Stephen Denis or visit: https://sbfassociation.org

A special shout out to the Diamond and Platinum Sponsors: Rapid Finance, Kapitus, Bitty, and Ocrolus.

Also a shout out to Nexi (WiFi Sponsor), AMA Recovery Group (Breakfast Sponsor), Shoreham Bank (Lanyard Sponsor), and Vox Funding (Key Card Sponsor).

NerdWallet: Organic Search Result Leads for SMB Financing Still Down, LLM-Generated Leads Converting Better

November 7, 2025This quarter, NerdWallet repeated that its SMB financing deal flow continues to lag significantly below last year’s levels because of changes in organic search. Similarly, the company reiterated that the conversion rate of leads coming from LLMs has looked very promising. During the Q3 earnings call, analysts finally asked if LLM traffic meant ChatGPT.

“I’d say the primary driver to think about is actually AI overviews within Google Search,” said NerdWallet CEO Tim Chen. “So because search is becoming more useful, people are searching a lot more. And so we are seeing traffic come through from AI overviews. ChatGPT and Gemini are also driving an increase there. So those are kind of the 2 major drivers in terms of the LLM traffic. When people come through that way, they’re really high intent typically, they’re really held in on finding something in a marketplace, for example. So I think that’s what’s driving some of the higher transaction rates there.”

Though, LLM conversions are promising, they are currently not enough to replace the organic search conversions they were previously generating. CFO John Lee said they expect a continued degradation in SMB in Q4.