Business Lending

Quickbooks Capital: Another $1.3B Funded to Merchants, Has Protective Moat from AI

March 2, 2026Intuit’s Quickbooks Capital originated $1.3B in business loans to its customers for its fiscal Q2 2026. The number was a repeat of the previous quarter but still puts them on a trajectory to surpass yet another rival (Shopify Capital) on originations in 2026.

Quickbooks users are presented a “button” in their Quickbooks software to obtain funding.

“We are switching that conversation from being a sales pitch to helping address a customer need,” said Intuit CFO Sandeep Singh Aujla during the latest quarterly earnings call. “As an example, our customer could have a payroll due tomorrow, but the invoice is not going to get paid till next week. With a click of a button, they can access the Capital loans. Payroll is done. The employees are paid. Employees are happy. Next week when the customers pay the invoices, the agent automatically pays down the debt.”

When an analyst raised a concern about their partnership with LLMs, Intuit said there was nothing to worry about because their data is not shared with the LLMs.

“Our moat comes from being the core of the flow of funds, whether it is access to capital, whether it is hours worked by the employees, whether it is money flow—that is not being touched by these LLMs,” said Aujla.

Square Loans: $7 Billion Funded in 2025, Block Lays Off 40% of All Staff Due to AI

February 26, 2026Square Loans finished 2025 with a whopping $7 billion funded to merchants. And just as has been the case previously, payment performance on these loans has been so good that “the amount of loans that were identified as nonperforming loans was immaterial,” according to the year-end report.

Despite Square Loans being the largest originator of online business loans in the country that deBanked tracks, the product is merely a value-add to its parent company’s (Block) merchant processing and point-of-sale business. Block’s year-end figures were overshadowed by the announcement that it was laying off 40% of its staff on the basis that AI has unlocked new efficiencies that no longer require such a high headcount. Layoffs amounted to more than 4,000 employees in a single day.

“We’re not making this decision because we’re in trouble,” Company CEO Jack Dorsey wrote on X following the news. “Our business is strong. gross profit continues to grow, we continue to serve more and more customers, and profitability is improving. but something has changed. we’re already seeing that the intelligence tools we’re creating and using, paired with smaller and flatter teams, are enabling a new way of working which fundamentally changes what it means to build and run a company. and that’s accelerating rapidly.”

Biggest Challenge of Low Cost Business Lending: The customers couldn’t distinguish the difference

February 26, 2026In a podcast between Ballard Spahr attorney Alan S. Kaplinsky and Executive Director of the Responsible Business Lending Coalition Louis Caditz-Peck, the latter revealed one of the biggest revelations he had while previously working in the small business lending division of LendingClub. Winning on price doesn’t work if your customers don’t realize your product is actually a lower price.

“[…] part of that strategy [LendingClub] was to be the lowest cost financing that a small business could get online while properly managing risk and be as fast and easy as some of the fastest and easiest financing a business could get online,” said Caditz-Peck. “And what I found was that strategy of being lower cost really had challenges because customers could not tell that our products were lower cost and that was our biggest challenge.”

Caditz-Peck gave an example of how a quoted “rate” might have different meanings or reflect a different aspect of a deal:

“What was a challenge to our business was losing deals over and over again to competitors that were offering a much worse product, because the customer can’t tell. So this is a San Francisco open floor plan. And I can hear all the conversations happening of our folks that are talking to the small business owners, the kind of loan officer type folks, and they were having this conversation just constantly where they would say, ‘hey, Alan, congratulations, you’re pre-approved. We can lend to you at ________.’ The average APR at the time was about 22% that we were charging. ‘So we can get you financing at 22%’ and the small business borrower would often say, ‘Well, such and such company is offering me 10%’ and then our loan officer would say, ‘okay, but when they say 10%, what is that? Is that an APR? is it an interest rate?’ Usually it was bullshit. It just meant it was a percentage number that had no relationship to how we compute a real interest rate, and was probably equivalent to an interest rate of—in some cases if they’re saying 10% maybe it was like 40%, maybe it was like 300%, but this business owner didn’t know who to trust, and so that was squelching innovation, and that is what continues to be squelching innovation.”

Stripe Capital Originated 81,000 MCAs and Business Loans in 2025

February 25, 2026 Stripe, currently in the news for its $159 billion valuation and its potential interest in acquiring PayPal, originated 81,000 merchant cash advances and business loans in 2025 through its subsidiary Stripe Capital. Stripe didn’t say what that equated to in total funding volume but when compared to a rival’s (Square Loans) historical data, it puts it in the likely range of $800 million to $1.2 billion.

Stripe, currently in the news for its $159 billion valuation and its potential interest in acquiring PayPal, originated 81,000 merchant cash advances and business loans in 2025 through its subsidiary Stripe Capital. Stripe didn’t say what that equated to in total funding volume but when compared to a rival’s (Square Loans) historical data, it puts it in the likely range of $800 million to $1.2 billion.

Stripe recently conducted a study to measure the impact of Stripe Capital on its customers and found that “businesses that accepted Capital offers grew 27 percentage points faster over the following year than comparable businesses that didn’t.”

“The averages conceal a wide spread,” the company said. “The fastest-growing decile of financed businesses grew more than 3× faster than comparable peers; the next decile grew nearly 100 points faster. A representative example: Xirsys, a server hosting business based in California, used financing from Stripe Capital to set up additional servers in China, India, and Japan, subsequently doubling its revenue. Notably, even businesses with low credit scores grew 11 to 18 percentage points faster after receiving financing.”

Stripe’s rumored interest in PayPal is also notable in the fact that PayPal also has a business loan program. Last year PayPal funded $2.2 billion to small businesses, down from $3 billion in 2024.

BHG Financial Originations Surge to $6.1B in 2025

February 20, 2026“With regards to BHG, that team down there just continues to deliver, you can see that with their performance in 2025,” said Pinnacle Financial Partners CFO Jamie Gregory on the company’s recent Q4 earnings call. Pinnacle owns 49% of BHG Financial. BHG’s average business loan is between $20,000 to $250,000. It also does personal loans. Combined they originated $6.1B in 2025, up from $3.7B in 2024.

Pinnacle has been very impressed with BHG’s performance and outlook going forward.

“I mean we’re talking 25% to 35% growth for the company,” said Gregory. “So they continue to perform. And I go through all that because it just shows that they are focused on their core business. They’re focused on growing it, adding value.”

In the earnings presentation, it says that BHG targets borrowers through direct mail and “other sophisticated marketing techniques using a wide range of proprietary marketing tools.”

Shopify Capital Finishes 2025 With $4.2B in MCAs and Business Loans

February 18, 2026Shopify revealed its full year MCA & business loan origination figures. $4.2 billion. That’s $1.2 billion over the previous year. Only 91.9% of these deals were considered “current” as of December 31, 2025. That’s down slightly from last year when 93.7% of deals were considered current at year-end.

For clarity, Shopify Capital offers funding in 8 total countries. The product is considered a value-add to its e-commerce platform and only offered to merchants who use it. Shopify Capital is in the same league as Square Loans and Enova in terms of origination volume.

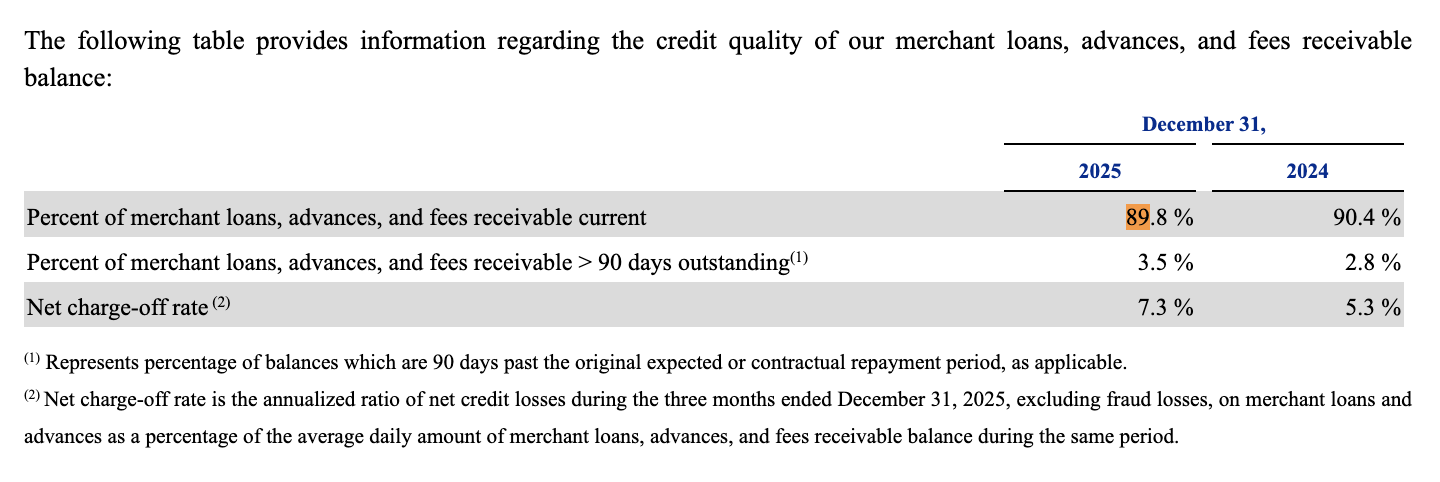

PayPal: > 10% Business Loans Not Current

February 4, 2026PayPal finished 2025 with ~$2.2B in business loan originations, down from $3B the prior year. As of December 31, 2025, only 89.8% of their portfolio was current, down slightly from the prior year.

Charge-offs, however, are up significantly. The percentage excludes “fraud losses.”

PayPal’s CEO was replaced this week after the Board was disappointed by the company’s overall trajectory. Enrique Lores, the former president and CEO of Hewlett Packard, is now in the top spot. The upheaval was enough to prompt commentary from PayPal’s former president of the 2012-2014 era, David Marcus. On PayPal’s lending business specifically, Marcus offered this critique:

“On lending, PayPal missed the opportunity to turn it into a platform weapon. Products like Working Capital were conservative, short-duration, and optimized for loss minimization. Lending never became programmable, never became identity-driven, and never became a reason for merchants or consumers to choose PayPal over something else.”

Enova: On the Ground, Small Businesses Optimistic

January 28, 2026Enova reported $1.6B in small business loan originations for Q4 2025, a big jump from the $1.4B in the prior quarter.

“There’s been a lot of noise over the year of 2025 around the impacts of tariffs and the macro economy and where we are,” said Enova CEO Steve Cunningham during the earnings call. “But I think what I wanted to highlight in my commentary is that it’s not quite as gloomy as it seems on the ground. It seems that small businesses are looking forward positively. And I think it’s reflecting in the demand that we’re seeing.”

On the ground that they see, credit quality and net charge-offs have also remained stable.

“Our internal and external data highlight that SMBs continue to express confidence in the economy and expect favorable operating conditions during 2026,” Cunningham said.

In its latest study and report it published with Ocrolus, they found that “Overall, growth expectations amassed an all-time high with 94% of small businesses projecting growth over the next 12 months.”

Enova also expects to close its acquisition of Grasshopper Bank in the 2nd half of this year and said that both companies are business as usual until that happens.