Business Lending

Why OnDeck and CAN Capital Nailed Their Treasury RFI Responses

October 1, 2015 A congressional staffer once told me that if you want your input to have any meaningful impact, you better bring hard statistics and numbers.

A congressional staffer once told me that if you want your input to have any meaningful impact, you better bring hard statistics and numbers.

Both CAN Capital and OnDeck accomplished that in their comprehensive responses to the Treasury RFI.

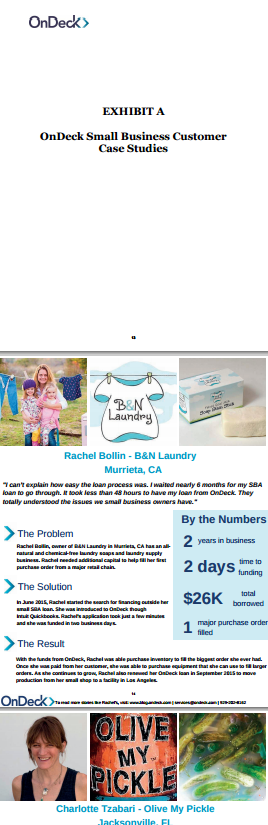

OnDeck went a step further and even attached case studies that included photographs of actual small business owners they’ve helped. They also put to bed the notion that their business model is unregulated:

At the federal level, we are regulated by the SEC and subject to US securities laws. We further satisfy applicable lending requirements under, among others, the Fair Credit Reporting Act, the Servicemembers Civil Relief Act, the Equal Credit Opportunity Act, and sanctions programs administered by the Office of Foreign Assets Control (OFAC).

They also clue us in to the size of the potential market they’re in. “It is estimated that there is $80-$120 billion in unmet demand for small business lines of credit,” they wrote.

Notably, they support the logic that a short term high APR loan can make more financial sense than a long term low APR loan. “With respect to loan cost, by matching a loan’s term with the estimated investment payback (or ROI) period, a small business can minimize total overall interest expense. For example, a loan used to purchase inventory can have a payback term that corresponds to the expected sale of the inventory — in this way, a borrower may pay less in total interest expense on a higher-rate, short-term loan than on a lower-rate, long-term loan (which may take weeks or months to procure).”

Meanwhile, CAN Capital explained just how time consuming the process can be for small business owners. “On average, a small business owner might spend over 30 hours applying for credit from a traditional lender and wait weeks or longer for the underwriting process to run its course and the funds to be disbursed, assuming the loan request is approve,” they wrote.

CAN’s response at time reads like an S-1 registration form (could there be a reason for that?). “Our approach to assessing the risk of small businesses and their ability to pay has been very effective, as manifested by our lifetime weighted average net write off rate of 7.2% over 17 years and more than $5.3 billion in funding transactions,” they say. “For returning customers that access capital through our platform more than once, we see an increase in their gross sales of approximately 7% on average between their first and last funding transaction.”

And if you don’t want your data sources to be questioned, the easy thing to do is cite governmental studies which both companies did often. “Traditional lenders are not serving the capital needs of small businesses. This is especially true when small businesses need $100,000 or less, which accounts for 90% of small business loans,” CAN wrote while citing a report published by the SBA’s Office of Advocacy.

Sam Hodges on Fox Business

September 30, 2015Funding Circle’s Sam Hodges appeared on Fox Business on Monday, September 28th. One of the things he said is that loans under $1 million are still out of reach for most small businesses.

He also mentioned that his company has the lowest loss level of any digital small business lender anywhere in the world.

Details about Funding Circle disclosed:

- $1 billion lent to more than 10,000 businesses

- 40,000 investors globally

- $25,000 to $500,000 small business loans

Watch the full video below:

Mr. Merchant: Help ME, Help YOU

September 25, 2015 As we close the 3rd Quarter in the Year Of The Broker, I thought that it might be imperative to blow off some steam. Industry forums, commentators and media reporters often rant on Brokers and Lenders by disclosing the inefficiencies of such parties. But I have yet to see (or hear) of anyone making a particular “rant” on the most crucial element in our industry, The Merchant. So if you would allow me the liberty to do so, I would like to take a couple of moments to provide these rants as many of you might have the same “pet peeves” with the merchants you are currently assisting (or trying to assist).

As we close the 3rd Quarter in the Year Of The Broker, I thought that it might be imperative to blow off some steam. Industry forums, commentators and media reporters often rant on Brokers and Lenders by disclosing the inefficiencies of such parties. But I have yet to see (or hear) of anyone making a particular “rant” on the most crucial element in our industry, The Merchant. So if you would allow me the liberty to do so, I would like to take a couple of moments to provide these rants as many of you might have the same “pet peeves” with the merchants you are currently assisting (or trying to assist).

Help ME, Help YOU

Mr. Merchant please Help ME, Help YOU. We all know the situation of why you returned my call, email, etc., you are in need of some working capital for your business because conventional sources are either not lending to you altogether, or they can’t work within the time frame that you need the capital in.

But I can’t help YOU, unless you first help ME in the process by being as efficient as you can in terms of your level of organization. You operate a $350k – upwards to $10 million business, why is it that you are so unorganized to the point where you can’t seemingly tell your head from your rear? Below are just “some” of things that Mr. Merchant, YOU need to work on.

Not Meeting Basic (Elementary) Deadlines

We would be at the very end of the closing process only for you to send over an expired driver’s license because you never updated it, or your SOS filing is inactive because you didn’t pay the $50 annual filing fee, or you are late filing your taxes and didn’t put in an extension. These are basic (elementary) deadlines Mr. Merchant, how is it that you are not staying on top of them?

Bank Statements Are Out Of Order

We need your bank statements to analyze your sales, cashflow, balances, etc. to determine approval terms/conditions. Why is it that your fax has pages that are totally out of order, pages missing, etc.? Why is it that many times you don’t even know where your bank statements are and we have to wait 3 or 5 days for you to “find” them? We are in the Year of 2015 Mr. Merchant, have ever heard of a tool called “Online Banking”? You can easily log in and forward your statements over in PDF format by email within 5 minutes.

Can’t Find Financials

So Mr. Merchant, you are requesting $200,000 plus from my platform and the Underwriter needs to take a look at last year’s Tax Return, Prior Year Financials and YTD Financials. But similar to your Bank Statements, you have no clue where these documents are. Mr. Merchant, how can you run a $5 million plus business, but not know where your Company’s Financials are?

Bad Credit

Bad Credit

The average FICO score in the country is about 693, yet Mr. Merchant, your FICO score is under 500, or 520, or 575. As an entrepreneur, you know that you are supposed to keep your credit clean as much as possible, yet you routinely tell me that you haven’t pulled your credit in a while and you don’t know what’s on your report. There are free sources like Credit Karma, Credit Sesame and your Credit Card Issuer to get your credit score/reporting ranges for free, yet you don’t use them?

Running The Business On Overdraft Protection

Mr. Merchant, my financing is based on a daily or weekly fixed payment, how can I approve you when you have no money in your business bank account and you run the business on overdraft protection?

Not Disclosing Liens, Bankruptcies, Or Landlord/Mortgage Issues

During my pre-qualification, I asked you if you had any prior liens or bankruptcies, I also asked if you were behind on your landlord or mortgage payments. You flat out said no. Did you not think we were going to find late in the 11TH Hour of the closing process, that you have a $150,000 tax lien without a payment plan on it? Which means we just did all of this work, for nothing?

Excessive Cash Advance Stacking

Mr. Merchant, tell me how does this make sense? Why would you take out excessive advances on top of one another without calculating the fact that you would be paying 25% to sometimes 40% of your gross monthly revenue in cash advance payments? Then after doing so, you come to me complaining about why no one will help you get from under these “evil” Cash Advance companies?

Sending Fake Statements and Financials

And this is the ultimate pet peeve! So Mr. Merchant, you are in such desperate need of a high priced Cash Advance, that you are willing to go to prison for it by sending over fake bank statements and financials? Why on Earth would you risk your freedom in such a manner?

Final Word

As Brokers and Lenders, we are always hammered in the media about our inefficiencies, but nobody says anything about the flat out (sorry to say) stupid behavior of merchants that we serve.

Mr. Merchant, please help ME, help YOU, or should I say help US as an industry help YOU, by just doing the basic (elementary) of things that will assist us in securing the best alternative financing deals in the marketplace, all designed to help grow, develop and sustain your business.

Dodd-Frank and More Paperwork Make Lending Harder

September 19, 2015 It’s not just alternative lenders that have concerns about Dodd-Frank, Section 1071 and the CFPB. Several community bankers recently testified in front of The House Committee on Small Business Subcommittee on Economic Growth, Tax and Capital Access to explain just how detrimental regulations have been to their lending operations.

It’s not just alternative lenders that have concerns about Dodd-Frank, Section 1071 and the CFPB. Several community bankers recently testified in front of The House Committee on Small Business Subcommittee on Economic Growth, Tax and Capital Access to explain just how detrimental regulations have been to their lending operations.

While the discussion encompassed all types of lending including consumer mortgages, B. Doyle Mitchell Jr, the CEO of Industrial Bank said that, “Dodd-Frank was intended for maybe 50 to 100 institutions. It was not intended for mainstream institutions, minority banks around the country.” Mitchell was speaking on behalf of the Independent Community Bankers of America (ICBA).

While repeatedly making the case about how important community banks were to local communities, he explained that Dodd-Frank had not helped them achieve their goals. “It has only increased our costs,” he testified.

Mitchell also expressed a feeling of perpetual anxiety over the loans they make, worrying that a regulator will not like them.

Dixies FCU CEO Scott Eagerton, who was there speaking on behalf of the National Association of Federal Credit Unions (NAFCU) said, “I really feel like we’re getting away from helping people and making sure that we make the loans that Washington agrees with and I think that needs to change.”

While alternative lenders were not on the agenda, the subject of government mandated transparency and its intent to help make things easier for borrowers is both timely and relevant. Referencing some of the new disclosures required in loan documents by Dodd-Frank and/or the CFPB, Congressman Trent Kelly asked if all the added pages to loan agreements make it easier for their customers to understand.

“Do they understand what they’re signing?” he asked.

Mitchell responded that they do not. “It is not any more clear,” he answered. “In fact it is even more cumbersome for them now.”

Regulators should pay special attention to this especially in light of a Federal Reserve study that came to the same conclusion. In Alternative lending: through the eyes of “Mom & Pop” Small-Business Owners, small business owners were asked if they understood financing terms offered by typical online lenders. The feedback was overwhelmingly positive that they did. But when asked a trick question about annual percentage rates, most got confused. While some advocacy groups interpreted this to mean that small business owners are confused by online lenders, it actually offers pretty compelling evidence to the contrary. A future standard of government mandated transparency as it relates to annual percentage rates would only serve to make it harder for small businesses to understand contracts, not easier.

Both Eagerton and Mitchell made the case that increased compliance costs undermined the ability of community banks to grow the economy. “You cannot expect a trillion dollar institution to focus on hundred thousand dollar loans,” Mitchell said. And Subcommittee Chairman Tom Rice said, “the burdens created by Dodd-Frank are causing many small financial institutions to merge with larger entities or shut their doors completely, resulting in far fewer options where there were already not many options to choose from.”

Both Eagerton and Mitchell made the case that increased compliance costs undermined the ability of community banks to grow the economy. “You cannot expect a trillion dollar institution to focus on hundred thousand dollar loans,” Mitchell said. And Subcommittee Chairman Tom Rice said, “the burdens created by Dodd-Frank are causing many small financial institutions to merge with larger entities or shut their doors completely, resulting in far fewer options where there were already not many options to choose from.”

Eagerton argued that,”lawmakers and regulators readily agree that credit unions did not participate in the reckless activities that led to the financial crisis, so they shouldn’t be caught in the crosshairs of regulations aimed at those entities that did. Unfortunately, that has not been the case thus far. Accordingly, finding ways to cut-down on burdensome and unnecessary regulatory compliance costs is a chief priority of NAFCU members.”

But Congressman Donald Payne, Jr wondered why the ICBA was objecting to Section 1071 of Dodd-Frank, the part that grants the CFPB authority to collect certain pieces of data from financial institutions. Regulation B of Section 1071, for those that aren’t aware, was intended to study gender, racial and ethnic discrimination in small business lending.

Payne likened the law to The Home Mortgage Disclosure Act (HMDA), pronounced HUM-DUH, in which raw data is disclosed to the public but no penalties are specifically imposed if the data leans one way or another.

Mitchell responded to that by saying HMDA was a good example of something that was already very burdensome and another reason why Section 1071 was a bad idea. “While there is a clear need to outlaw discrimination at any level, I don’t think [this law is] necessary for community institutions,” he said. He pointed out that his bank could suffer reputational damage in the community by disclosing the gender and racial statistics of their business loans to the public at large.

While he did not expand on what he meant by reputational risk, one could fill in the blank that he meant the context that such data would lack. For example, if 75% of Hispanic-owned businesses were declined for business loans while only 25% of African-American-owned businesses were declined for business loans, one might infer from that raw data that there is potential discrimination taking place. Since small business loans are less FICO driven than consumer lending and focused more on the story of the business and the projected financial future, it is impossible to infer anything from raw data as it relates to discrimination.

“Simply put, Dodd-Frank needs to be streamlined,” said Marshall Lux, Cambridge, MA, John F. Kennedy School of Government, Harvard University.

And “the problem with Dodd-Frank,” Mitchell voiced, “is you cannot outlaw and you cannot regulate a corporation’s motivation to drive profit at all costs so while it had a lot of great intentions in over a thousand pages it has not helped us serve our customers any better.”

You can watch the full hearing below:

Is The Small Business Administration An Ally to Alternative Lenders?

September 16, 2015 Add the Small Business Administration (SBA) to the list of organizations likely to understand the rise of tech-based business lending. Miriam Segal, a research economist for the SBA, recently published a report titled, Peer-to-Peer Lending: A Financing Alternative for Small Businesses. In it, she opens with a line that is all too familiar in the merchant cash advance and non-bank lending industry. “Imagine that you own a small bakery and you need $15,000 to buy a new oven,” she writes. She later adds, “Data suggest that peer-to-peer lending may be a viable financing alternative for small businesses, particularly given the post-recession credit market.”

Add the Small Business Administration (SBA) to the list of organizations likely to understand the rise of tech-based business lending. Miriam Segal, a research economist for the SBA, recently published a report titled, Peer-to-Peer Lending: A Financing Alternative for Small Businesses. In it, she opens with a line that is all too familiar in the merchant cash advance and non-bank lending industry. “Imagine that you own a small bakery and you need $15,000 to buy a new oven,” she writes. She later adds, “Data suggest that peer-to-peer lending may be a viable financing alternative for small businesses, particularly given the post-recession credit market.”

After having read the recent Federal Reserve study that essentially concluded that small business owners are just too confused to make sound financial decisions, the SBA report is a welcome sign that there is little to fear from “alternative lending.”

While the SBA is sometimes cast as a villain to the private sector, what with their ability to assuage banks into making small business loans at very low interest rates with the assurance of default guarantees, a practice viewed by some economic ideologues as anti-free market, there hasn’t actually been much competition with alternative lenders. The average SBA loan is about $371,000, much higher than the average merchant cash advance transaction of about $30,000. And although they are a government agency, the SBA is scrutinized far more than today’s alternative lenders are. Politicians have sought to shut the agency down for decades but it has managed to survive. If any small business lending group knows what it’s like to be a political football, it’s the SBA. They’ve even been accused of similar antics, like being a participant to predatory lending.

Chris Hurn, Fountainhead Commercial Capital’s CEO, offered his opinion on such in the Huffington Post when he wrote, “I realize that calling some behaviors ‘predatory’ will raise some hackles, but what else would you call a virtually systemic practice of convincing small business owners to accept an inferior loan program on commercial real estate transactions, which almost certainly puts these borrowers in future harm’s way, only so a bank can maximize its income?”

Where have we heard this viewpoint before?

In the SBA report, Segal acknowledges a wide array of working capital options including merchant cash advance products. “P2P lending may fill a gap in small business lending for entrepreneurs seeking small amounts of capital when existing options are not suitable or available (e.g., bank loans, credit cards, and merchant cash advances),” she states.

She also gets to the heart of the issue that those touting the superiority of long term loans seem to be missing and that is that, “the majority of small business borrowers appear to be interested in relatively short-term loans in relatively small amounts.” Using data made available by Lending Club, 56% of small business owners applied for loans of $15,000 or less. Although the SBA will guarantee really small loans, it’s uncommon for banks to spend time and effort underwriting these, not to mention that many small businesses lack collateral and other minimum requirements for eligibility.

The reality is that alternative lending is for the most part the world outside of the SBA’s scope. “For some small businesses, an expensive loan may be better than no loan,” Segal concludes.

Given the variations in application process, interest rate, loan amount, and term length across loan products, it is apparent that each option presents a unique set of pros and cons. Peer-to-peer loans offer the benefits of expedited application processing, smaller loan amounts, and shorter terms, but borrowers pay for these conveniences in the form of higher interest rates.

– Miriam Segal

Research Economist, SBA

From the perspective of small business advocacy, the report gets it right. “Peer-to-peer lending to small businesses is rising while the origination of small business bank loans is decreasing. Micro businesses are interested in borrowing small amounts of money, although their credit applications are the most likely to be rejected. Therefore, the financial regulatory environment in which P2P lending exists is particularly important to small businesses.”

And it concludes, “Peer-to-peer lending has the potential to change the landscape of small business financing for the better. In order for this to happen, financial regulations must reflect the need for investor protection and simultaneously allow small businesses to access the capital that many individuals are willing to provide—no small task.”

As the wider industry is being researched by regulators, it is an especially important time to discover who shares the same understanding of the facts. Although not an immediately obvious choice of ally, the SBA is undoubtedly qualified to communicate the needs of small business. That makes them an especially good candidate to help explain the story about the what, why, and how of the changing landscape.

SBA Offers Balanced Review of Alternative Small Business Lending

September 15, 2015 In response to the Treasury’s RFI, I expect many industry commentators to encourage potential government regulators to engage in a careful review of the small business finance market before deciding on a course of action. As an example of the type of review necessary, these commentators could highlight the recent issue brief published by the SBA Office of Advocacy entitled “Peer-to-Peer Lending: A Financing Alternative for Small Businesses“.

In response to the Treasury’s RFI, I expect many industry commentators to encourage potential government regulators to engage in a careful review of the small business finance market before deciding on a course of action. As an example of the type of review necessary, these commentators could highlight the recent issue brief published by the SBA Office of Advocacy entitled “Peer-to-Peer Lending: A Financing Alternative for Small Businesses“.

While the scope of the paper is limited to P2P loans used for business purposes, it explains how alternative small business lenders are expanding access to capital:

Compared to traditional loan products, marketplace loans feature decreased search costs; this is a result of the proprietary credit scoring algorithms that the lending platforms use. This decrease in costs makes it economical for lenders to provide smaller and/or shorter-term loans to firms on which less information is available. Such firms may include those that are younger, less established, have a shorter credit history, lack collateral, or may be in acute financial distress (e.g., imagine that you own a bakery and your only oven stops working).

The paper recognizes that alternative lenders are able to offer financing to small businesses that previously had no way of obtaining working capital, a fact that is often misunderstood or disregarded by industry critics. The paper also explains some of the reasons why alternative small business loans charge higher rates when compared with other types of loans:

[E]ven controlling for observable borrower characteristics, loans for small businesses were more than 250 times more likely to perform poorly than loans for other purposes, which may give some insights into why such loans are charged a higher rate. Put simply, investors require a higher payoff in order to fund these riskier loans, and for some small businesses, an expensive loan may be better than no loan.

Overall, the paper is a evenhanded assessment of a complex topic. It highlights how alternative lenders have increased credit availability for small business owners while explaining the economics behind the rates charged. And as the policy discussion regarding marketplace lenders begins, explaining these facts will become increasingly important.

Major Business Lending Fraud Has Consequences

September 15, 2015 It appears that commercial financing fraud is not limited to just the average $40,000 transactions typical in the merchant cash advance and non-bank business lending sector. Four executives for a small business named Projuban, LLC, DBA G3K Displays, Inc., were sentenced last week to serve time in prison for their role in an $18 million loan fraud.

It appears that commercial financing fraud is not limited to just the average $40,000 transactions typical in the merchant cash advance and non-bank business lending sector. Four executives for a small business named Projuban, LLC, DBA G3K Displays, Inc., were sentenced last week to serve time in prison for their role in an $18 million loan fraud.

G3K was a New Jersey-based company that provided in-store displays for retailers. According to a report published by the FBI, the execs “engaged in a scheme to falsely inflate G3K’s revenue and accounts receivable, and as part of the scheme, made and caused to be made materially false and misleading statements about G3K’s financial condition. To create the false impression of sales, the defendants created phony documents, including fake and falsely inflated purchase orders purporting to reflect sales to G3K’s customers.”

One of the lenders that fell victim to the fraud is Veritas Financial Partners LLC. Veritas is no stranger to the merchant cash advance industry, having financed at least one merchant cash advance funder themselves just a few years ago. They are regularly involved in multi-million business financing transactions, deals that are typically considered too large for merchant cash advance companies and other non-bank lenders.

In addition to the prison sentences which ranged from 4 months to 40 months, The FBI report says that, “STEVEN KAITZ, 56, of Jersey City, New Jersey, was ordered to forfeit $1,382,427 and pay $18,687,518 in restitution; LATCHMEE MAHATO, a/k/a “Robbie,” 50, of Jamaica, Queens, was ordered to forfeit $2,215,417 and pay $18,687,518 in restitution; JONATHAN WHEELER, 46, of Southport, Connecticut, was ordered to forfeit $957,435 and pay $18,687,518 in restitution; and ZACHARY KAITZ, 32, of Brooklyn, New York, was ordered to forfeit $100,000 and pay $18,687,518 in restitution.”

Perhaps the lenders working on really large transactions should heed the advice of those working on small transactions, and that’s to stop relying on paper statements. In this case, the perpetrators heavily relied on the use of fake documents.

“ZACHARY KAITZ, who was skilled in graphic design, helped carry out the fraud by creating fraudulent documentation, such as fake invoices, purchase orders, and bills of lading, to support the false representations to the lenders about G3K’s business,” the FBI report states.

Financing Not Really an Issue for Small Business According to the NFIB

September 11, 2015 Small businesses need money right? Well according to an August 2015 survey conducted by the National Federal of Independent Business, 21% of respondents said that taxes were the single most important problem facing their business today. That ranked highest on a list of ten issues. Only a minuscule 1% said that financing and interest rates were the most important problem. Even inflation was ranked as more important than financing.

Small businesses need money right? Well according to an August 2015 survey conducted by the National Federal of Independent Business, 21% of respondents said that taxes were the single most important problem facing their business today. That ranked highest on a list of ten issues. Only a minuscule 1% said that financing and interest rates were the most important problem. Even inflation was ranked as more important than financing.

Thirty-three percent of all owners reported borrowing on a regular basis and similarly, thirty-three percent reported all credit needs met. 49 percent however, explicitly said they did not want a loan. This data is based on a sample of 3,938 small-business owners/members that translated into 656 usable responses received for a response rate of 17%.

20% of respondents said that government requirements and red tape were the single most important problem they face, second to taxes.

One could infer from the data that access to capital is not a challenge for small business right now, which would make sense given how many non-bank alternatives are currently available. It also raises the question as to why regulations for non-bank alternatives would be considered a priority when small businesses seem to be pretty content with the way things are. If anything, the message here is that the best solution to grow small business is to lower their taxes. With that remedy being unlikely, a potential takeaway from this study then is that non-bank financing companies should consider ways to address their prospects’ two biggest pain points, taxes and government requirements. And if not those two, then the third issue that respondents said was the single most important problem, poor sales.

How can non-bank financing companies help small businesses address poor sales? This may be the key to long-term mutual success.