Business Lending

The First Ever Comprehensive Industry Report is Now Available

December 29, 2015 Months ago, investment bank Bryant Park Capital teamed up with us to conduct the first ever industry CEO survey of its kind. A sample of the initial findings were distributed at Money2020 in Las Vegas. Eligible participants that disclosed their identities to the surveyors have already received a complementary copy of the full anonymized report.

Months ago, investment bank Bryant Park Capital teamed up with us to conduct the first ever industry CEO survey of its kind. A sample of the initial findings were distributed at Money2020 in Las Vegas. Eligible participants that disclosed their identities to the surveyors have already received a complementary copy of the full anonymized report.

Today, those that either weren’t eligible to take the survey or missed the deadline to participate, can buy a copy of it.

With a sample size of small business funding companies that originate more than $2 billion annually, the final report reveals the industry’s Compound Annual Growth Rate, Average Annual Revenues, Average Annual EBITDA, Portfolio Loss Rates, Approval Rates, M&A Expectations, Valuation Expectations, Syndication Data, and much more.

This report is highly recommended for all funders and ISOs seeking to raise capital or for those that want to eventually sell their company. It’s also a must-have for any company that seeks to set short-term or long-term goals, that wants to compare themselves against the industry, or is creating a realistic business plan.

Investors in the industry also stand to benefit from this data.

If you are interested in buying the full report, e-mail sean@debanked.com.

The original report sample for public distribution

Mentioned in Forbes

Bryant Park Capital’s professionals have completed approximately 400 assignments representing an aggregate transaction value of over $80 billion.

Funding Brokers: Critical Thinking is Greater Than Positive Thinking

December 28, 2015 THE NEW THOUGHT MOVEMENT HAS TAKEN OVER THE SALES PROFESSION

THE NEW THOUGHT MOVEMENT HAS TAKEN OVER THE SALES PROFESSION

Somewhere between the 19th and the current 21st century, the profession of sales as a whole integrated the concepts of the New Thought Movement, going so far as to actually shape the mantras, slogans and thought processes of salespeople everywhere.

In my opinion, the New Thought Movement has the potential to do far more harm than good, because it does not emphasize the importance of individuals learning how to critically think. It has an over-reliance on positive thinking and positive faith, with a complete disregard for critical thought and analysis. When a person fails to critically think, they can easily fall prey to scams, manipulation, brain-washing, etc. and even mismanage their finances through various forms of impulse (emotional-based) spending. As a result, for whatever amount of good that the movement does, in my opinion, it has the potential to do far more damage, such as the damage that I believe it has done to the sales profession.

THE HISTORY OF THE NEW THOUGHT MOVEMENT

It started in the 19th century with the promotion of ideals by philosophers such as Napoleon Hill, that life begins in the mind and that the quality of your life would be based on your level of positive thinking and positive faith. The mantra of the movement is that if you maintain the right level of positive thought processes as well as keep high levels of positive faith, then you can “attract” to you whatever you desire, which usually centers around materialistic items like fancy cars, shallow things like very attractive mates, significant wealth, or good health and wellness.

By the 20th century, the movement would eventually spread to various religious denominations in the form of the prosperity gospel (the word of faith movement), promoted through television evangelists and the vast majority of mega churches throughout the country.

By the 21st century, the movement would spread to even more authors and even film producers with the 2006 film “The Secret” which also included a book version of the ideals promoted during the film.

It was also by the 21st century that the movement had been fully ingrained into the vast majority of sales training material, which would serve as the foundation for a lot of what I deem to be “issues” of the sales profession today. These being the utter lack of critical thinking and critical analysis which leaves too many sales people as mindless, robotic, and routine order-takers, rather than strategic thinkers, innovators, and business developers.

NEW ENTRANTS TO THIS INDUSTRY ARE INSPIRED BY TECHNIQUES FROM THE NEW THOUGHT MOVEMENT

Since this year’s March/April edition of deBanked Magazine, we have talked about the Year of The Broker as it relates to the surge of new brokers coming into the space. These new entrants are inspired by funders, lenders and large brokerages using techniques from the New Thought Movement.

The rah-rah sales motivational speech that’s provided to these new brokers is founded mainly on the New Thought Movement. The people recruiting these new brokers into the space get them to dream about:

- Getting out of debt

- Moving out of their mother’s basement

- Living in a big/fancy house

- Having a very attractive mate on their arm

- Driving a Mercedes Benz S-Class

- Making $25k, $40k, or $50k per month

- Being “the man” in the nightclub, buying up all of the drinks and being the life of the party

They would sum up their rah-rah sales motivational speech with simply, “As you think, so shall you become,” quoting the great Bruce Lee.

Thoughts that arise of a critical nature that look for more market research, market planning, trends, innovative solutions, ROI analysis, and other forms of foresight are either quickly shunned as “over-thinking” or “negative thinking”. You might flat out be kicked out of the room where the rah-rah sales motivational speech is being conducted, with accusations of having “stinking thinking.”

THIS ISN’T ROCKET SCIENCE, IT’S CRITICAL THINKING

The New Thought Movement’s over-reliance on positive thinking and positive faith can be detrimental to personal growth. Being a part of the Mom and Pop Network isn’t necessarily a bad thing, as I have operated within the Mom and Pop Network, but what’s shortsighted is not giving brokers all the tools they need to think critically and truly be successful.

For you to survive, you are going to need to have resources that the vast majority of other brokers don’t have access to. Relying on UCC records and Aged Leads (that every other broker is calling on), isn’t going to cut it. You are going to need resources that provide you with a significant market competitive advantage which includes but isn’t limited to: having better data so you can produce your own exclusive internal leads, having “center of influence” partnerships with banks, credit unions, and other professionals, having access to creative financing in the form of either equity or debt, among other advantages. These advantages will not just give you a leg up over other brokers in the market, but they are truly the key to your long term survival.

A FINAL WORD

In my opinion, The New Thought Movement does more harm than good, by not emphasizing the importance for individuals to learn how to critically think.

We are living in the day and age where to survive in any professional sales environment, you are going to have to be more of a critical thinker and do things outside of “the box”, versus being the stereotypical smiley faced, overly optimistic, robotic, sales guy, that’s incapable of true “independent thought.” You want to be the sales guy that thinks and operates outside of the box, which is basically this bubble in which everybody else is operating and thinking within. You can’t achieve this unless you first embrace cynicism by taking a long hard look at this box, poke holes in it, discover new ways to profit, and then blaze your own trail.

Being cynical, pessimistic and “negative” are the first steps towards becoming an excellent critical thinker, even though they will not make you feel as “good” as compared to that of being optimistic and positive. But in that regard, I must quote Dave Ramsey in that: Children do what feels good. Adults make a plan and follow it.

Critical thinking doesn’t feel good, but you can’t properly plan without it.

Brokers: It’s Okay To Delay Starting A Family

December 25, 2015 WE HAVE NO “MINIMUM” GUARANTEE

WE HAVE NO “MINIMUM” GUARANTEE

The debate to increase the minimum wage across the board in the US to $15 per hour has been going on for quite some time now, with marches in the street from fast food workers, people protesting by walking off the job, and strong political debate with passionate views on both sides.

What’s been strange to me about this debate, in relation to the argument of those that are in favor of increasing the minimum wage, is their reference to workers being “slave labor” by working excessively hard and long, but not making enough in a lot of cases to support a household. The reason this has been strange to me is because for close to 9 years, I operated on a 1099, independent, 100% commission basis, as a solopreneur managing my own one man show sales office. I received no salary, base pay, hourly pay, “floor”, nor company benefits (even though I am fully insured individually). The Harvard Business School report from July 2014 by Karen Gordon Mills and Brayden McCarthy, said that there’s 23 million businesses in the country that do not have any employees and are classified as Solopreneurs.

So, should myself and the other 23 million Solopreneurs in this country all be marching and protesting as well? And if so, marching and protesting against who? I work for 1ST Capital Loans, LLC, but I’m also the sole managing director, member and employee of said entity, so as a result, I should be marching and protesting against myself? We as independent brokers have no minimum guarantee or minimum wage, which not only makes the minimum wage debate strange, but it also points to another reality in that adding a family to our chaotic situation might not be optimal at this time.

RUNNING YOUR OWN SHOP IS VERY DIFFICULT

Running your own show is probably the hardest job you will ever have in your life. Having to juggle the various components of it with no established “minimum wage” just chokes out far too many independent brokers. Some of those various components include but surely aren’t limited to:

- Having to manage regulations, laws and other legal aspects

- Having to manage accounting, insurance and tax related aspects

- Having to design your own business plan and ROI formulas

- Having to come up with your own way of creative financing

- Having to manage your vendor, supplier along with partner negotiations and agreements

- Having to design your market strategy, solutions and spend time actually selling them

On top of this, you might have to deal with pet peeves of your Funder and Lender Partners, which could include them cheating you out of commissions, clawing back commissions after 45 days, cutting you off from your renewal and residual portfolios, among other things. These things rob you out of the hard earned commissions for deals that you fought for in one of the most competitive markets in the country (using your own capital, creativity, time and energy) to win.

MAKE A FAMILY NOW, OR DELAY DOING SO JUST A LITTLE BIT LONGER?

With all of the aspects of building your broker office that must be managed on your own, with no minimum guaranteed wage, benefits or true assistance, the next question becomes, how do you manage a family through the very early stages of all of this chaos? The reality is that there’s only so much time in the day. If you are just starting out your own shop and if you don’t currently have a present family to take care of, putting the creation of a family on hold might be your best bet. I once expressed that it was okay to be a piker, then I expressed that it was okay to be a minimalist, today I’m telling you that it’s okay to delay starting a family.

THE MILLENNIAL GENERATION FACES A LOT OF STRUCTURAL CHALLENGES

It seems as though most of the newer brokers in our space are a part of the Millennial Generation.

Generation Y (The Millennial Generation) begins usually around 1981 and lasts until about 1995, the Generation that follows (Generation Z) are those that were born just after 1995. Being a Millennial myself, I tend to keep abreast of many of the issues facing my generation, and while I currently do not have a family that I’m responsible for, I believe that many Millennials would agree that it’s seemingly more difficult today than ever before to manage a family:

- We Are Over-Educated and Under-Employed: We are in fact the most educated Generation, but some reports state that over 50% of us are under-employed, which means we are mainly a Generation of the over-educated and under-employed, saddled with student loan debt.

- Lack Of Security and Stability: Prior Generations had the luxury of working for one company, in one location and in one city, for the vast majority of their working career, and be able to retire with a pension, 401k, and strong retirement benefits from Social Security. Our Generation has no such securities, as many of us will have to change careers and work locations often during our working career, making it nearly impossible to seemingly ever purchase a home because purchasing a home only makes sense when you can estimate “staying put” in one area for at least 10 years. Also the lack of pensions, strong 401k plans, and the fact that we might not receive strong Social Security benefits further complicates the security issue.

- Our Cost Of Living Continues To Sky Rocket: From food to energy, from property taxes to rent, from insurance premiums to healthcare costs, from college tuition to day care expenses, our cost of living continues to skyrocket.

- Our Opportunities Are Being Stolen Away: Wages and business opportunities are either stagnant or flat out decreasing due to the rise of global competitive forces and IT/robotic automation stealing away our opportunities for income advancement.

So while you are trying to juggle the issues of building your broker office, you are also having to deal with competitive global forces and IT automation, along with the rising cost of living, along with deficiencies in job/income security and stability. So how in the world do you add a family of let’s say two kids on top of this chaos? Regardless of whether or not you are married or a single parent, the costs and risks of managing a family within this chaotic situation are significant.

IT’S OKAY TO DELAY STARTING A FAMILY

If you already have a family, obviously you can’t “give them back” and start over, so if you are seeking to enter this space and build your broker office, you are just going to have to find a way to juggle all of the chaos that’s present. However, if you are like me (a Millennial and Broker within this space), that hasn’t yet created a family, if you are still in the early stages of constructing your office, renewal and residual portfolios, then I would say that it’s “okay” to delay starting a family considering all of the chaotic issues that you would be facing today.

How long to delay such a very important choice is a personal one that you would have to manage, but for some of us, the choice might come down to opting out of creating a family altogether.

BizBloom Lights Up Times Square

December 24, 2015BizBloom’s “Yes, we’re local” campaign produced by industry veteran Thomas Costa is making its debut in New York City’s Times Square. Its mission, according to Costa, is to tell the story of the American Dream, particularly the struggles and accomplishments of entrepreneurs.

To do that, BizBloom intends to rely on the help of college students to interview small business owners all over the country. The stories that garner the largest social media responses will be featured in their slot airing over 43rd and Broadway. Additionally, for each story a student collects, BizBloom will donate to a special scholarship fund.

The campaign is already live and includes supporting endorsements from Quick Bridge Funding and deBanked:

Got a Ferrari or Fine Art? If So, You May Have More Leverage Than You Think

December 23, 2015If you own a Ferrari, fine art or expensive wine, getting access to capital may be easier than you think.

Although it’s still a niche market, luxury asset-backed lending has been gaining traction lately, particularly with small and mid-size business owners. These executives are enticed by the ability to use certain high-priced valuables as a means of getting large amounts of cash quickly and often at a lower cost than other funding sources.

“People are increasingly learning that this is another option. It’s not for everybody, but it’s another option,” says Tom McDermott, chief commercial officer at Borro, a New York-based asset-backed lender that deals exclusively with luxury asset-based loans.

It’s notable that luxury asset-based lending by alternative funders is gaining ground at a time when unsecured money is so easy to come by. There are several reasons business owners are attracted to the idea of leveraging their valuables to attain cash. First off, they don’t need stellar credit or a proven track record in business to qualify. Secondly, they can typically get larger sums of money and at better rates than they might through other financing channels. A third reason is that many of them have already tapped out other funding options and leveraging their assets allows them to obtain additional funds quickly.

“A lot of small business owners have assets, so it’s something else for them to utilize in getting access to attractive small business financing,” says Steven Mandis, chairman of Kalamata Capital LLC, an alternative finance company in Bethesda, Maryland.

Here’s how the process typically works at most luxury asset-based lenders. Say a business owner wants to borrow against a high-priced item such as a top-of-the-line car, fine art or wine, jewelry or a luxury watch. First the luxury-based lender hires a third-party to appraise the item. Generally, depending on the asset and its marketability, lenders will lend 50 percent to 70 percent of the asset’s value. If the owner moves forward, the item or items are held and insured in a lender’s secure storage area until the loan is paid back. Default rates on these types of loans are relatively low, lenders say.

“People don’t want to put their house at risk when they need capital,” says McDermott of Borro. “They’d rather lose the Maserati or a lovely piece of art than the house,” he says. And even then, it doesn’t happen very often, he says. Borro clients only default on their loans about 8 percent of the time, McDermott says.

Barriers to Entry

To be certain, luxury-based lending is not a business that every funder wants to be in. For starters, there are a lot of regulatory hoops a funder has to jump through in order to do it. You need a pawnbroker’s license and a second-hand dealer license. You also need a secure facility or facilities to house the collateral, have secure ways of transporting the valuables, and you need to carry large amounts of insurance for the transfer of the items as well as during the holding period.

Indeed, keeping the items secure is critical. PledgeCap, a Lynbrook, New York-based funder, says on its website that it uses “cutting edge technology, top of the line bank vaults and armed guards” to keep a customer’s items safe. What’s more, all items are insured during transit and storage. All items are shipped through secured and insured FedEx shipping vendors for pickups and drop-offs.

“There aren’t a lot of players in the market because there are a lot of operational and legal requirements to adhere to. There are a lot of barriers to entry,” says Gene Ayzenberg, the company’s chief operating officer.

Putting Things in Perspective

Luxury asset-based lending is only a small subset of the overall asset-based lending market, which as a whole has been gaining ground in the past few years. After getting badly burned in the most recent recession, many lenders have come to appreciate the security blanket that collateral offers. According to the Commercial Finance Association’s quarterly Asset Based Lending Index, U.S. ABL loan commitments rose 7.2 percent in the second quarter, compared with the year-earlier period. In addition, new ABL credit commitments were 6.3% higher than the same period a year ago.

“Asset-based lending at one time used to be the lending of last resort. Now it’s the type of lending that it is accepted globally,” says Donald Clarke, president of Asset Based Lending Consultants Inc., a Hollywood, Florida-based company that provides due diligence services for lenders. “Today, everybody wants an asset.”

There’s not a lot of public data to gauge the size of the luxury market within the broader asset-based lending market. But a 2014 report that focuses on art lending gives more perspective to at least one facet of luxury asset-based lending.

Thirty six percent of the private banks polled said they offer art lending and art financing services using art and collectibles as collateral. That’s up from 27 percent in 2012 and 22 percent in 2011, according to the report by consulting firm Deloitte and ArtBanc, a company that provides art sales alternatives, valuations and collections management services.

Meanwhile, 40 percent of private banks said this would be a strategic focus in the coming 12 months, up considerably from the 13 percent who named this as a priority in 2012.

These market changes are likely driven by client demand. The Deloitte/ArtBanc survey found that 48 percent of establishes art collectors polled said they would be interested in using their art collection as collateral for a loan, up from 41 percent in 2012.

Many big banks won’t touch asset-based lending deals unless they are worth north of $5 million. Some community banks will do smaller deals, but many don’t have the necessary infrastructure or skill sets, explains Clarke, of Asset Based Lending Consultants. This, of course, leaves an opening for alternative funders to capture market share.

Luxury asset-based lending expected to experience growth

Some lenders say they expect demand for luxury asset-based loans to continue to increase over time as more people accumulate big-ticket items and they become more aware that they can satisfy their capital needs by leveraging those assets. “A lot of times they don’t even know they have this option available to them,” says Ayzenberg of PledgeCap.

He says most of his company’s customers are small and mid-size business owners. Often they have temporary cash flow issues, but bank loans aren’t necessarily an option for them for any number of reasons. For instance, some may have bad credit. Others may have excellent credit but not enough of a business track record to qualify for a bank loan. Others may not have the cash flow to secure the amount of money they need, or they may need the money very quickly. Asset-based lenders can generally make the money available within a day, whereas bank loans require a lot of paperwork and can take months to obtain.

Mandis, of Kalamata Capital, says his company has seen an increased willingness by business owners to put up their luxury assets as collateral in order to get larger amounts of money at more favorable terms. Many times business owners have a high-priced asset that they don’t want to sell and pay a tax or can’t easily unload within a short-time frame. By borrowing against the luxury asset, they will get the capital to take advantage of a short-term opportunity and make an attractive return quickly without having to worry about finding a buyer or paying taxes on the sale of the asset, he explains.

Certainly luxury asset-based lending is not for every customer. Not only do you have to have a valuable asset to be used as collateral, but you also have to be willing to part with the item while the loan is outstanding. The risk of default and not getting the item back may also be a barrier for some people.

“I would be very hesitant to put up my wife’s diamond ring for my business. I don’t think it’s typically someone’s first choice,” says Ami Kassar, chief executive and founder of Multifunding LLC, a company in Ambler, Pennsylvania that helps small businesses find the best loan for their business. He remembers considering this option for a client only once in the past several years and the client ultimately chose another funding source.

But companies that focus on luxury asset-based lending say there is a viable market for their services that will continue to grow as more people hear about it and use it successfully to fulfill their funding needs. People have been taking their small items to pawn shops for many years. Working with a licensed lender to leverage their larger and often more expensive items gives them an option they may not have had previously. “You can’t just drive a tractor into a local pawnshop and say, ‘Here just put this in your safe,’” says Ayzenberg of PledgeCap.

Also, unlike pawn shops, luxury asset-based lenders say they aren’t looking to sell the items to make a quick buck and will only sell the item as a last resort if a customer defaults and they can’t reach agreeable terms. “We want them to keep their items,” says Ayzenberg whose company has been in business since 2013. For every 100 loans, there are only a small percentage of customers that default and lose the items, he says.

Every lender runs their business slightly different. At Borro, for example, loans typically range between $20,000 and $10 million and span in time frame from three months to three years. Rates start in the mid-teens and are based on the size of the loan, the time frame and how easy the asset would be to sell. In order to work with Borro, the asset typically has to be worth more than around $40,000, McDermott says.

Borro, which has been in business since 2009, deals with customers directly. But it also gets a good number of referrals from other lenders. Let’s say a customer needs $500,000 and a particular lender can only offer a maximum of $350,000. That lender might refer the client to Borro, which kicks in $150,000 based on the value of a leveraged asset. The referring company gets a commission based on the loan value and doesn’t lose the whole deal. “It’s a way to keep your customers tied in with you,” McDermott says, adding that Borro has no intention of getting into other types of lending. “We complement each other. We don’t compete.”

PledgeCap also focuses exclusively on asset-based lending. The company typically funds loans between $1,000 and $5 million. The length of each loan is four months. Customers don’t have to pay every month, though most do. For every month the loan is outstanding customers pay a rate of 3 percent on average. Other fees, payable at the end of the loan, are assessed based on costs PledgeCap incurs and depend on factors such as the cost of insurance, the appraisal fee and the cost of transporting the item to the secure facility.

PledgeCap also focuses exclusively on asset-based lending. The company typically funds loans between $1,000 and $5 million. The length of each loan is four months. Customers don’t have to pay every month, though most do. For every month the loan is outstanding customers pay a rate of 3 percent on average. Other fees, payable at the end of the loan, are assessed based on costs PledgeCap incurs and depend on factors such as the cost of insurance, the appraisal fee and the cost of transporting the item to the secure facility.

By contrast, Kalamata Capital, which has been in business since 2013, offers asset-backed loans in connection with several other small business financing options—such as working capital loans, SBA loans, lines of credit, merchant cash advance and invoice factoring—to give customers more flexibility in terms of rates.

In Kalamata’s case, it will evaluate the cash flow and other assets of a small business for financing options. Kalamata then combines both the amount it would lend against an asset and the amount it would lend to the small business, possibly giving the business a lower rate—and more options—in the process.

While it’s not a type of funding that works for everyone, Mandis, the chairman of Kalamata, expects to see continued growth in this area. “I don’t think the loan market for luxury assets is as large as many of the traditional small business finance areas, but it is something that can be helpful to small business owners,” he says.

Brooklyn Eyeglass Merchant Defrauds Business Lenders

December 22, 2015 It’s another case of bad merchants. In this instance, Maksim Grinberg, the owner of D&M Optical and 9th Street Vision in Brooklyn have been charged with defrauding lenders out of $3.4 million. According to an article in the New York Times, Grinberg, along with two co-defendants, used false documents and guarantors to obtain numerous business loans over the last five years. He then used those funds to gamble, shop with his girlfriend, and pay his rent. The charges have resulted in a 148-count indictment filed by the Brooklyn district attorney’s office.

It’s another case of bad merchants. In this instance, Maksim Grinberg, the owner of D&M Optical and 9th Street Vision in Brooklyn have been charged with defrauding lenders out of $3.4 million. According to an article in the New York Times, Grinberg, along with two co-defendants, used false documents and guarantors to obtain numerous business loans over the last five years. He then used those funds to gamble, shop with his girlfriend, and pay his rent. The charges have resulted in a 148-count indictment filed by the Brooklyn district attorney’s office.

Brooklyn District Attorney Ken Thompson is quoted in the official report as saying, “this long-running scheme allegedly took advantage of banks and leasing companies as well as of hard-working doctors whose identities were stolen so they could be listed as loan guarantors. We investigated this brazen scam, put an end to it and will now hold those responsible accountable.”

The roster of victim lenders which included names like Wells Fargo, noticeably did not list any alternative lenders. While a UCC search revealed his D&M Optical Store used a merchant cash advance 10-years ago, Grinberg’s scam was directed at what was apparently an easier target, traditional lenders. “To secure the loans,” according to the DA’s report, “the defendants submitted fraudulent documents, including applications, lease agreements and delivery acceptance forms as well as forged signatures of loan guarantors, according to the indictment.”

It is perhaps another sign that lenders need to move away from paper statements and to tools that can be verified electronically through third parties in an automated fashion. According to the Times, the scheme only began to unravel once a guarantor whose identity had been stolen was contacted to make a payment on their $1 million loan.

World Business Lenders Rings in 2016

December 18, 2015On December 8th, World Business Lenders (WBL) wrapped up 2015 and prepared for the coming new year at their annual shareholder meeting hosted at the Waldorf Astoria in New York City. The event, which was mostly restricted to company employees, referral partners and shareholders, featured some out-of-town guest speakers including BFS Capital CEO Marc Glazer and RapidAdvance Chairman Jeremy Brown.

On a panel moderated by WBL Managing Director Alex Gemici, Brown and Glazer expressed their optimism for the industry’s future, but to some extent heeded caution. Brown specifically made reference to his prediction of a bursting bubble but conceded that he might have been off by a year or two. Glazer reminded the audience that both executives had weathered the financial crisis so that they had witnessed firsthand how a recession can affect their businesses, and made them stronger because of it.

WBL CEO Doug Naidus made a similar admission in his presentation, in that he thought that the bubble of unsecured lending would burst in 2015 but that it hadn’t happened yet. Still, he thinks it’s right around the corner. One of their primary hedges against a correction is that they secure their loans against real estate. Naidus has a background in mortgage lending so it’s a market they’re familiar with.

Another one of their key strategies is the franchise model. Over the last two years, WBL has acquired commercial finance brokerages and converted them into originating houses for their collateralized loan program. It has had a really positive impact on their growth and on their margins, according to information disclosed at the event. It’s expected that they will continue to pursue more acquisitions.

The sentiment of the event was rather festive and optimistic, with WBL enjoying a positive trajectory of growth and success.

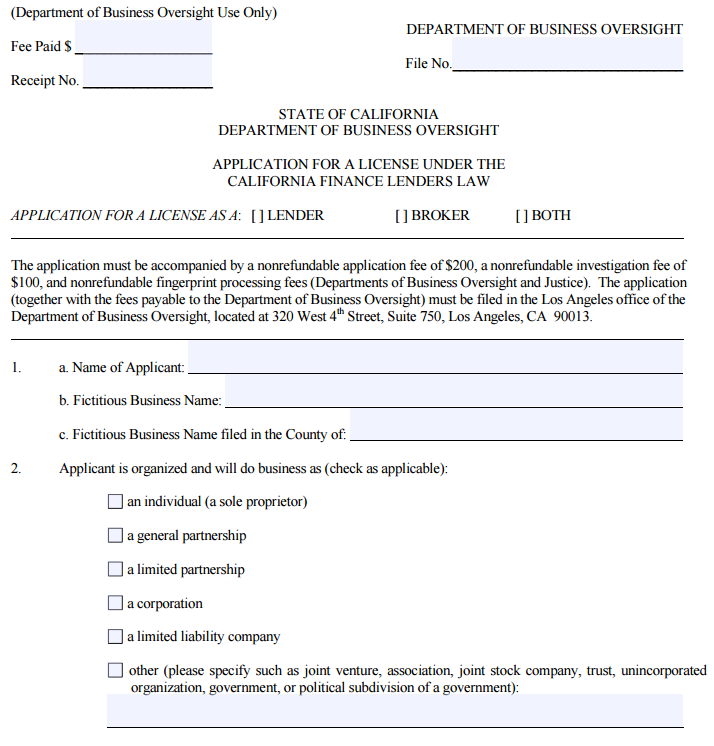

Getting a California Lender’s License

December 17, 2015Given the fact there have been a number of successful lawsuits against cash advance companies in California, many cash advance companies have decided to take a different route and get a lending license to provide loans to merchants in the state. If done correctly, this can allow companies to provide loans to merchants in California at roughly the same profit margins one could expect from a cash advance. Below I will discuss the process for obtaining a California lender’s license and some tips for making that process less painful.

To start, go to the California Department of Business Oversight and get the form titled “Application for a License Under the California Finance Lenders Law.” The application is long and detailed but don’t let that scare you. Most of the information you provide is really more related to letting the State know about your company and the main people that will be responsible for managing the lending operations. As you complete the form, one thing you do need to do is make sure you are very careful and meticulous as any small mistake will cause the application to be rejected making the process much longer.

To start, go to the California Department of Business Oversight and get the form titled “Application for a License Under the California Finance Lenders Law.” The application is long and detailed but don’t let that scare you. Most of the information you provide is really more related to letting the State know about your company and the main people that will be responsible for managing the lending operations. As you complete the form, one thing you do need to do is make sure you are very careful and meticulous as any small mistake will cause the application to be rejected making the process much longer.

The first part of the application requests basic information about your company and its officers. In filling out this and other parts of the application, it is essential to respond to all the questions. If you fail to miss just one response the application will be rejected. To that end, even if a question does not apply to you I find it better to respond “N/A” or “not applicable” rather than just leaving a blank. By doing that you force yourself to fill in every blank and therefore reduce the chances for missing a response resulting in a rejection of your application.

Also, you need to be very precise in your responses. I have experienced a situation where the examiner rejected an application because the name of the company was incorrectly spelled on the application. The name of the company was submitted on the application with “Inc” instead of the complete “Inc.” at the end of the company’s name. The examiners are very good at what they do and very thorough. You need to make sure the packet you submit is perfect and also that there are no inconsistencies in the document.

Another important point to remember is that the application requires you to name the person that will be responsible for running the location where the lending is occurring. The main requirement is that the person running the location must be physically present at the location. As a result, you could not manage a California office remotely from New York for instance. In another twist, if your principal location is out of state, you will need to get the license and fill out the main application for that out of state address. For the California location, you will need to fill out the short form application in addition to the main application and submit the short form application as part of the packet to allow the license to apply to the location in the state of California.

There are a number of exhibits you also have to provide as part of the process. Some of them are simple like a balance sheet for the company. It is acceptable that the company is new and has little in the way of assets. You just have to make sure you attach a balance sheet and that it is prepared in compliance with generally accepted accounting principles. I have seen times when the balance sheet was rejected because there was no line items for liabilities for instance, even though the company was new and therefore had none. It is probably wise to engage your accountant to make sure you submit a balance sheet that complies with those guidelines.

You also have to get a surety bond in the amount of $25,000. There are readily available bonding companies that specialize in providing these bonds. In addition, you need some other exhibits like a statement of good standing for your company, authorization for financial disclosure, social security number (on a separate exhibit), organizational chart and a few other documents. As with the rest of the application the key is to make sure you include everything they are asking for exactly as requested.

The most involved exhibit is the “Statement of Identity and Questionnaire.” That exhibit has to be filled out for each owner, officer and manager listed on the application. It requests detailed information going back 10 years for each person for items like residence address and work history.

In addition, there are a series of questions on topics such as whether the person has been involved in lawsuits, had any licenses revoked or declared bankruptcy. Fingerprints are also taken as part of the process. This part of the application is trying to vet the various people working for the company to make sure they are suitable to be in the lending business.

Once you have all the documents prepared, you need to put them together in a packet to send off to the Department of Business Oversight to be reviewed. Again, I cannot overemphasize how important it is to completely and accurately answer the questions and put the packet together. You need to make sure things are in the proper order and complete. Triple check the application for errors and to make sure that packet is presented in the best manner possible. You also need to determine the amount of fees to submit with the application. Then, send the package by overnight delivery to make sure you have proof of delivery.

So what happens next? Well there is usually a bit of a wait. Typically it takes 3 months or more to get a reply. If you have done your homework, you might get lucky and successfully get your license on the first try. If there are any deficiencies, you will get a response letter from the State detailing the items that need to be corrected in the application and a time frame in which you have to respond or the application is abandoned.

On the first go round, you are usually given at least 2 months so you should have plenty of time. Digest the things they want and provide the required information. The deficiency letters are very detailed so it should be easy to make the requested changes. Resubmit the requested items and wait for the next response. It could be in the form of another deficiency letter but it could be an approval of the license. Just keep on trying until you are finally successful.

That’s it, you are finally a licensed lender in California! But that is where the fun begins. You are subject to many laws in California and audits by the State. To get the right to operate as a licensed lender, you need to make sure you prepare your application correctly. Once you have done that, you need to get all your loan documents drafted in compliance with California law. Make sure you have adequate experience and professional help to take on those tasks.