Banking

Small Businesses Rank Online Lenders More Transparent Than Big Banks

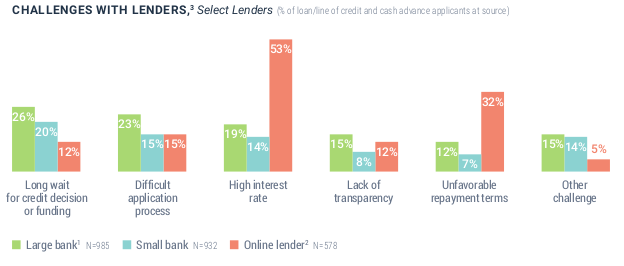

April 16, 2019When it comes to business loans, small businesses say online lenders are more transparent than big banks.

Specifically, 15% of respondents to a Federal Reserve survey reported challenges with transparency experienced at big banks versus only 12% with online lenders. Small businesses also ranked big banks worse on credit decision wait times, application process difficulty, and other unspecified challenges.

The Federal Reserve survey examined small businesses with less than 500 employees.

Small banks fared the best on transparency, payment terms, and interest rates.

Lyft IPO Follows a Foray into Finance Business

March 29, 2019 Lyft had its IPO today in the same week it announced that it was offering a debit card to its drivers. The company announced the launch of “Lyft Driver Services,” a suite of services for Lyft drivers including Lyft Direct, a no-fee bank account and debit card. The Lyft Direct debit card will allow drivers to instantly access their earnings after each ride, according to a company statement on its Medium page. This is an extension of Express Pay, which allows drivers to cash out on their earnings right away, rather than wait for the pay cycle to end.

Lyft had its IPO today in the same week it announced that it was offering a debit card to its drivers. The company announced the launch of “Lyft Driver Services,” a suite of services for Lyft drivers including Lyft Direct, a no-fee bank account and debit card. The Lyft Direct debit card will allow drivers to instantly access their earnings after each ride, according to a company statement on its Medium page. This is an extension of Express Pay, which allows drivers to cash out on their earnings right away, rather than wait for the pay cycle to end.

“The traditional biweekly paycheck falls short of serving today’s workers, and the rising costs of maintaining a bank account disadvantage them further,” Lyft COO Jon McNeill explained in a statement. “Americans pay an average of $163/year in banking fees. Minimum balances are often greater than what many people can save, and most cash-back programs require an above-average credit score. We’re fixing that for our drivers.”

The Lyft Direct debit card has 4% cash-back on select restaurant purchases, 2% on gas, and 1% on groceries. Additionally, Lyft will offer its drivers a no-fee bank account with access to over 20,000 fee-free ATMs. Lyft is working with Oklahoma-based Stride Bank on this program. Stride Bank will manage all of the drivers’ bank accounts.

Last April, Uber released the Uber Visa debit card with Go Bank which also allows drivers to get paid instantly. Like the Lyft Direct debit card, the Uber debit card also gives users cash-back, like 3% on Exxon and Mobil gas, 2% on Walmart purchases and 8% on your Sprint bill.

Uber is no stranger to finance. In fact, the company once offered a product akin to an MCA where drivers were offered money up front in exchange for a percentage of their future fares, according to a deBanked story from 2016. That arrangement was made by Clearbanc. Uber also got into the leasing business with its leasing program, Xchange Leasing. But that was phased out beginning in 2017 due to myriad problems, including losses, an FTC lawsuit that dealt with misrepresenting the program, and an FTC complaint, according to a December 2018 post on The Simple Dollar, a personal finance website. The complaint accused Uber of connecting its drivers with subprime auto companies and dealers that provided interest rates significantly higher than industry averages.

So while Uber offers its drivers a debit card, it has backed away from other financing. With Lyft a step behind, will Lyft stop with this new debit card? Or perhaps learn from Uber’s mistakes and expand into the lending space?

The Lyft stock (NASDAQ: LYFT) started at $72 and closed its first day of trading at $78.29, up 8.7 percent.

Two Cultures Collided, Gently

March 25, 2019

Banks are heavily regulated. Factoring companies are not. The two don’t always mix. So it was interesting last July when Axiom Bank, a regional bank in Florida, acquired Allied Affiliated Funding, a factoring company based in Texas.

Fast forward nine months and the merger of the two companies has been surprisingly easy, according to Axiom CEO Daniel Davis.

“Banking and factoring are two different worlds, two different cultures,” Davis said. “[But] the challenges that we expected didn’t occur.”

Davis explained that the biggest challenge with a bank acquiring a factor is reconciling a bank’s credit risk with a factor’s, which are different because banks are more or less governed by regulatory standards while factors are not.

“Good factoring shops have guidelines too,” Davis said, “and we’re lucky to be involved with Allied which does share that high level of policies, procedures and internal controls.”

Regardless of how well a factor self-regulates, factoring companies have virtually no regulations compared to a bank, and this may give regulators a little pause to see a bank mixing with a factor.

“It is a challenge,” Davis said about merging a factoring company with a bank regarding regulations. “What the regulators want to see you do, whether you’re acquiring a factoring company or entering into a new product or service…what they’re most concerned with is that you’ve put the policies and procedures and risk management in place to actively manage and monitor that business.”

But so far, so good, according to Davis, who said that the factoring business has grown 30% in receivables since the July 2018 acquisition. Allied Affiliated Funding, which has retained its name, is now known as the factoring division of Axiom Bank. The bank has 24 branches throughout Florida, 22 of which are located inside Walmart stores. As far as marketing the relatively new factoring product, Davis said that while they do some brand marketing, the Allied factoring division gets most of its business from referrals, including attorneys and accountants.

He said that they also get referrals from banks. For instance, if a bank’s underwriting standards makes it such that it cannot keep a loan, the bank might send the loan to Axiom for it to be restructured as a factoring deal.

Small Community Banks Power Fintech Revolution

February 15, 2019 “A few years back there was a lot of disruption talk about how the fintechs were going to destroy the banks,” said Jo Ann Barefoot, co-founder of Hummingbird Regtech and a former deputy U.S. Comptroller of the Currency, which regulates national banks. “There’s much more talk in the last few years about the need for banks to partner [with fintechs].”

“A few years back there was a lot of disruption talk about how the fintechs were going to destroy the banks,” said Jo Ann Barefoot, co-founder of Hummingbird Regtech and a former deputy U.S. Comptroller of the Currency, which regulates national banks. “There’s much more talk in the last few years about the need for banks to partner [with fintechs].”

This quote was cited in a CNBC story published today and judging from the recent bank partnerships with some of the largest fintech companies – including Square, Stripe and Robinhood – this could not be more evident. The CNBC story points out that most of these fintech/bank partnerships are not with household name banks, but rather with small community banks that welcome the business. These banks, including Sutton Bank, headquartered in Attica, OH, Cross River Bank, headquartered in Fort Lee, NJ, and Celtic Bank, headquartered in Salt Lake City, UT, are handling the banking activities for these growing fintechs – activities like holding customer deposits and underwriting consumer and business loans. And significantly, making sure that everything is up to snuff with government regulations.

A number of fintechs, including Square and SoFi, have tried to take the banking component of their businesses into their own hands by applying to become an ILC bank. But they have been met with tough resistance, much of it coming from, interestingly, community banks.

“No one envisioned when they wrote the ILC charter that we would have fintech companies that finance mortgages and student loans from private equity capital and not deposits,” President and CEO of the Consumer Bankers Association told deBanked last year. “It’s a new world. Like with all rules and regulations, federal regulators should periodically review longstanding policy.”

So far, the opposition has been relatively successful but time will tell if it keeps up. Square and SoFi withdrew their ILC loan their applications, but Square eventually reapplied. At the 2018 Money 2020 conference in Las Vegas, SoFi CEO Anthony Noto said he would entertain seeking ILC bank status.

Fintech Inevitable, But Petrou Says Risks Abound

February 12, 2019 At the end of last week, two large regional banks, BB&T and SunTrust announced that they are merging. The entity will be the sixth largest U.S. bank and the largest bank merger since the 2008 financial crisis. A MarketWatch story yesterday indicated that large bank mergers are part of a somewhat recent trend, citing the mergers of Chemical Bank with TCF Bank, and Key Bank with First Niagara, both in 2016. (The number of bank acquisitions have been static in 2017 and 2018, with 252 and 253 banks, respectively, according to American Banker.)

At the end of last week, two large regional banks, BB&T and SunTrust announced that they are merging. The entity will be the sixth largest U.S. bank and the largest bank merger since the 2008 financial crisis. A MarketWatch story yesterday indicated that large bank mergers are part of a somewhat recent trend, citing the mergers of Chemical Bank with TCF Bank, and Key Bank with First Niagara, both in 2016. (The number of bank acquisitions have been static in 2017 and 2018, with 252 and 253 banks, respectively, according to American Banker.)

If large bank mergers are a trend, Managing Director of Federal Financial Analytics Karen Petrou told MarketWatch that this is in part because banks realize that they can combine resources to develop mobile banking capabilities to compete with online banks.

“If banks don’t come up with ways to innovate, they die,” Petrou told MarketWatch yesterday. “Then consumers are left to do their banking with nonbanks.”

Federal Financial Analytics, where Petrou is the managing director, is a Washington, D.C.-based consulting firm and Petrou is a highly regarded voice in the financial regulation space.

While Petrou acknowledges that online banking is the only alternative if traditional banks don’t innovate, she sees serious problems in fintech which she outlined in a paper published earlier this month, according to American Banker.

For instance, she wrote about the danger of a company like Amazon getting into banking and being able to charge individuals different amounts for the same item based on its knowledge of how much money the customer has. Or, the implementation of better banking policies for people who exercise and eat healthier. Petrou says this favors wealthier people with more time for exercise and greater access to more expensive, healthier food.

“I am all for technology,” Petrou said. “But I spent a lot of time when I was a student at MIT studying tech policy, and there is one after another example of seemingly promising technologies with terrible, unintended consequences.”

Joust Launches Banking Platform for Entrepreneurs

January 17, 2019 Lamine Zarrad, CEO, Joust

Lamine Zarrad, CEO, JoustThis week marked the launch of the Joust iOS app, a platform for freelancers and small businesses that provides banking, payments, collections and invoice factoring solutions. The Android App is scheduled for release on February 1, 2019.

“We straddle three different domains: payments, merchant processing, and factoring, all in one app,” said Joust co-founder and CEO Lamine Zarrad. “Most freelancers have a bank account, then add a payments account using Stripe or Paypal, or both.Then you need an invoicing tool. Now you’ve accumulated three or four different tools to bill your customers. What Joust did, in partnership with [our banking partner], is we were able to consolidate all of these tools.”

Zarrad said that Joust has three categories of customers: traditional small businesses, part-time freelancers, and full-time freelancers, or “solopreneurs” – people who dedicate all of their efforts to their entrepreneurial endeavors.

Some of the most common financial problems among solopreneurs that Joust aims to fix are stabilization of cash flows, gap financing, and integration of payments and banking.

In conjunction with an online banking platform, called Cambr, Joust provides customers with a bank account as well as a merchant account, which gives them the ability to accept credit cards directly into their account, Zarrad said. Cambr was created by StoneCastle, a technology enabled financial services company managing over $15 billion on behalf of its clients. It stores cash within a network of 850 community banks in all 50 states.

Another significant pain point for freelancers is collection of unpaid receivables. Zarrad said that entrepreneurs in general lost 14% of their receivables to non-paying or extremely delayed paying clients in 2018. The Joust platform/app also includes a collections service, which is a series of five emails strategically spaced out.

“Most bills don’t get paid not because people don’t want to pay, but because it’s been de-prioritized,” Zarrad said, “and having a third party act on behalf of a freelancer is immensely more powerful.”

If there is no response after the fifth email, Joust then outsources the collections. Having a Joust bank and merchant account is completely free, with the exception of credit card processing fees, which Joust passes on to the customer. Joust anticipates making money in part by bringing business accounts to StoneCastle and primarily from its factoring capabilities. Zarrad said they make 1 to 6% on guaranteeing invoices.

Trained at OnDeck, LendingFront Founders Help Banks Lend to Small Businesses

January 9, 2019 Yesterday LendingFront announced that it has raised $4 million to help deliver its white label software designed to help banks and other financial institutions lend to small businesses. The company was founded in 2015 by two former OnDeck employees, Jorge Sun and Dario Vergara.

Yesterday LendingFront announced that it has raised $4 million to help deliver its white label software designed to help banks and other financial institutions lend to small businesses. The company was founded in 2015 by two former OnDeck employees, Jorge Sun and Dario Vergara.

Sun was the Chief Credit Officer at OnDeck from 2007 to 2012 and said he was the company’s third hire. Vergara joined OnDeck as its Chief Technology Officer in 2008 and was also among the first to join the company, Sun said. They both left before OnDeck went public in 2014 and took other jobs before reconnecting to create LendingFront together. Sun said that it is very difficult to create a technology company inside a large bank, which is what he tried to do in his job at Capital One, following his time at OnDeck. Vergara was working as VP of Technology at Bonobos, an online clothing company.

As Sun began talking with Vergara about going out on their own, he recalled telling Vergara: “There are no platforms in this space directly created to help lenders become more efficient…We’ve built this once [at OnDeck], let’s build it again. But the difference now is it’s strictly a technology company. We take no risk, we don’t lend. All we’re doing is powering other lenders.”

Sun said that LendingFront is “lender agnostic,” in that they license out their proprietary lending platform to any financial institution, including banks, community banks, leasing companies and Community Development Financial Institutions.

Their customers pay them a licensing fee and the customer, say a bank, sets its own parameters with regard to underwriting. The platform simplifies the underwriting process, but completely allows for customization and design of the customer experience, Sun said.

The idea of helping banks become better online lenders is not completely unique. In fact, the founders’ former employer, OnDeck, recently launched a separate entity called ODX, with the mission of making banks better lenders to small businesses.

But Sun said that while ODX and LendingFront both help banks, there is a difference between the two. He said the difference is that ODX is more of a full service shop acting on behalf of a bank.

“With us, a bank is using our platform like using Excel…versus [using] Excel and then giving it to a different company and saying ‘use Excel on our behalf.’”

Sun said that customers have funded $150 million through the LendingFront platform since they started licensing it out in 2016. They previously raised $1.6 million in 2016 and they employ 24 people in an office in New York.

Square Renews Effort to Become a Bank

December 19, 2018 Square has plans to refile paperwork with state and federal regulators to open a wholly owned bank in Utah, according to a report in The Wall Street Journal today. In 2017, the company applied with the Federal Deposit Insurance Corp (FDIC) for a licence to become an Industrial Loan Company (ILC) bank, but it withdrew the application at the beginning of July 2018.

Square has plans to refile paperwork with state and federal regulators to open a wholly owned bank in Utah, according to a report in The Wall Street Journal today. In 2017, the company applied with the Federal Deposit Insurance Corp (FDIC) for a licence to become an Industrial Loan Company (ILC) bank, but it withdrew the application at the beginning of July 2018.

An ILC bank can take deposits and can be owned by a non-bank. It is also exempt from certain regulations that traditional banks must follow, making the ILC bank structure highly controversial. Critics say that ILC banks are very risky because they can engage in commercial activity outside of banking, which could lose money and jeopardize the bank.

“ILC banks were meant to serve a certain type of industrial worker [in the early 1900s] that had trouble finding a commercial bank they could bank with,” said Chris Cole, Senior Regulatory Counsel at Independent Community Bankers of America (ICBA), a trade group.

“Now we don’t have that problem anymore…this [ILC bank] charter is completely outdated [and is] a loophole that should be closed so that the owners of these bank-like institutions are restricted in the same way that commercial banks are restricted,” he said.

Proponents of ILC banks, like the fintechs that seek ILC status, say that becoming a bank can better serve their customers. Under the 2010 Dodd-Frank Act, which came in response to the Great Recession, there was a moratorium on establishing ILC banks because they were deemed to be a risk to the U.S. banking system. That moratorium was lifted in 2013 and over the last several years, a handful of fintechs have applied to get an ILC bank charter license.

SoFi applied for a license and later withdrew its application in 2017 amid a scandal related to its former CEO. But its current CEO, Anthony Noto, mentioned the possibility of pursuing ILC status again at the Money 20/20 conference in October.

NelNet, which services student loans, applied for an ILC license in June of this year and later withdrew its application in October.