Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Is The Marketplace Lending Apocalypse Upon Us?

May 3, 2016

Days after rumors leaked that Prosper Marketplace had planned to lay off staff, the WSJ is now reporting that the company is indeed eliminating 171 jobs, closing their Utah office and letting go of their chief risk officer. CEO Aaron Vermut’s salary has also been cut to zero.

The timing for the industry they’re a part of couldn’t be worse. OnDeck’s stock closed down 34% today after Q1 losses and revised projections took analysts by surprise. The source of the pain? OnDeck’s “Marketplace.” The institutional investors typically willing to pay a high premium for loans disappeared, according to OnDeck executives on the earnings call.

Unsurprisingly, Prosper’s “Marketplace” has historically relied on institutional buyers for their loans too, as much as 92% of all loans on the platform in fact. Prosper’s roots as a peer-to-peer lender don’t make it an ideal candidate to just shift loans to their balance sheet like OnDeck, which could make the changing capital markets landscape even more painful for them.

Two months ago, Prosper raised the interest rates they charge, citing a “turbulent market environment.” And just weeks ago, Citigroup announced that they would no longer buy loans from Prosper to package into bonds. Now, signs of stress are finally starting to show.

And then there’s Lending Club, a “marketplace” rival to both Prosper and OnDeck, who experienced a 10% decline in its stock price today. The company’s model is under fire through a class action lawsuit that alleges among other things that they along with WebBank are Racketeer Influenced Corrupt Organizations. Lending Club plans to release their Q1 earnings on May 9th.

And it’s not just the capital markets and lawsuits shaking up the landscape. Half a dozen trade associations have been formed over the last few months to quell some of the negative rhetoric surrounding online lending in Washington and to educate policymakers on the positive aspects of these services.

In the Illinois State Senate for example, a pending bill has the potential to outlaw all nonbank business lending altogether.

Some of those that broker business loans have already fallen on hard times due to things like the cost of leads skyrocketing.

“Anybody can fund deals – the talent lies in collecting the money back at a profitable level,” said Capify CEO David Goldin in deBanked’s most recent magazine. “There’s going to be a shakeout. I can feel it.”

The early signs of that prediction may finally be starting to unfold.

After the Lendit Conference last month, I speculated that marketplace lending euphoria ended because the relationship between investors and platforms was in some ways based on lust, not love. The breakup is now starting to manifest itself in the form of missed earnings and layoffs.

Is the apocalypse upon us? Probably not yet, but these foreshocks are a good sign that we’ll soon be separating the wheat from the chaff.

Make sure to wear your hazmat gear as you enter the marketplace.

OnDeck Disappoints: “Marketplace” in Jeopardy?

May 3, 2016

OnDeck finally bombed an earnings report and marketplace lending (at least their marketplace anyway) is being seriously questioned. The company is now predicting a full-year adjusted EBITDA loss of between $41 million and $49 million, down from the projection they made just three months ago of full-year positive EBITDA of $10 million to $14 million. They had a GAAP net loss in Q1 of $12.6 million.

Any positive details were disregarded by analysts who hammered away at the shifting dynamic of the OnDeck Marketplace. The premium earned on selling off loans to major investors through this channel shrank to a measly 5.7% Gain on Sale Rate during the first quarter. Bank of America’s Nat Schindler pointed out on the call that back when OnDeck was getting a 9% Gain on Sale Rate, that they believed even that number to be undervalued, but that they had said it was worth selling them at a discount to “seed the marketplace.” With the margins now compressed to a point where “seeding the marketplace” is no longer a rational excuse, he wondered why they still sold $123 million worth. “Why not just keep it all? What would happen if you just stopped the marketplace?” he asked.

Stop the marketplace

Stopping the marketplace quickly became the underlying theme of the Q&A session. Previously, 35-45% of their term loans were sold off through Marketplace but they now predict that only 15%-25% will be sold through it in 2016.

David Scharf with JMP Securities asked if and when the company could ever break even assuming there was no marketplace.

Vasu Govil with Morgan Stanley asked “if the risk premiums were to continue to rise, at what point does marketplace funding go to zero? At what point do you decide that it’s not worth doing it and that you want to keep all the risk on the balance sheet?”

OnDeck CFO Howard Katzenberg explained the decreasing margins as a retreat from one type of buyer. “Our marketplace buyers fall into two counts,” he said. “The first is those that buy and want to hold ’til maturity and the other segment buys with the plan on securitizing the loans and selling off the residual position of the portfolio. Given the inherent leverage in the securitization transactions, those buyers historically have been willing to pay higher premiums versus the kind of the more traditional hold ’til maturity investors.”

The appetite from those that plan to securitize the loans has dropped off, the ones that are typically willing to pay more.

Losses today instead of income

OnDeck did book more loans on their balance sheet than they had expected and as a result GAAP rules require them to book a provision expense for them. “So as our loan book grows, we will have a mismatch of the provision expense upfront versus earning interest income over the lifetime of the loan,” Katzenberg said. “Moreover, when we sell a loan through marketplace, we book a gain on sale upfront, which had the affect of accelerating the recognition of income.”

Translation: Booking a loan on balance sheet means recording a loss today while selling a loan through marketplace means booking income today. The first might be more profitable over time but transitioning from marketplace to balance sheet makes the books look worse in the short term.

Originations down

Actual originations grew by 37% year-over-year, missing the 40-50% range projected. OnDeck CEO Noah Breslow was unapologetic about that. “We’re not going to do anything unnatural because of those growth numbers,” he argued. “If we conclude that growing at a slower rate is best for our business then we will grow slower.”

The stock was down 3.82% on the day prior to the earnings release but plunged by nearly 30% in after hours trading.

Online Small Business Lending Task Force Initiated by the ETA

April 30, 2016 The Electronic Transactions Association (ETA) is now advocating on behalf of online small business lenders.

The Electronic Transactions Association (ETA) is now advocating on behalf of online small business lenders.

Though you might not have suspected it last week at Transact16, the ETA very much plans to involve themselves in the affairs of marketplace lending. That might not have been obvious from a Bloomberg article that reported that OnDeck, Kabbage and PayPal were forming a splinter organization as an “extension” of the ETA known as the Online Small Business Lending Task Force. Referred to as a new initiative in the announcement, the group’s mission is described as striving to “prevent hasty or overly restrictive regulations.”

But the group’s named lobbyist, Scott Talbott, is also the ETA’s lobbyist. And the three lenders named, were already members of the ETA. When Talbott was asked by deBanked to clarify the relationship between the “task force” and the ETA, he said that the two weren’t separate. The “ETA organized its members to lobby on the issue. It’s what we do every day,” he wrote.

The “task force” merely highlights members in the trade group that share a common interest.

Formed in 1990 and comprising of over 550 companies across 7 countries, the ETA has served the payments industry well. OnDeck, Kabbage and PayPal therefore find themselves in good company and led by advocates with well-established government relationships.

Along with the ETA, the online small business lending industry has found support from the Marketplace Lending Association, the Small Business Finance Association, the Commercial Finance Coalition and the Coalition for Responsible Business Finance.

Why Does Lending Club Set The Interest Rates If It’s A “Marketplace”?

April 29, 2016 A new user on the LendAcademy forum asked a good question.

A new user on the LendAcademy forum asked a good question.

“If Lending Club is merely creating a marketplace for borrowers and investors, why does LC set the price? Why not let them determine it independently? The external credit models are fundamentally about finding loans with the highest expected return relative to their risk.”

Here are some of the summarized responses that were given:

– Individual investors are not as able to price risk on their own

– It would be inefficient, much more time would be needed to investigate each loan

– Prosper started out doing it this way and the results were poor

– Lending Club doesn’t disclose all the data points to investors for proprietary reasons and to avoid releasing information that could lead to borrower discrimination, i.e. violations of the Equal Credit Opportunity Act (ECOA) and Consumer Credit Protection Act (CCPA). It’s better to have a third party manage these legal risks.

Today, many investors use automated programs like LendingRobot to do their investing for them, which means the hassle of trying to price a loan in a dutch auction with limited information would likely become an obstacle in the marketplace. It would also become a race to the bottom. Underpricing risk would be great for borrowers because they’d benefit from very low interest rates but it would be a disaster for investors that would likely experience losses as a result. If investors were all institutional and accredited, then maybe that would be fine. But since Lending Club has a substantial amount of unaccredited investors, the kind legally presumed to be unsophisticated, putting the onus of pricing risk on their shoulders would quickly lead to the collapse of the system entirely.

Lending Club might not be a marketplace in the purest sense, but given the legal complexities and investor/borrower protection considerations, it comes pretty close.

You can read the original thread on the LendAcademy forum here.

BlueVine a Serious Player After Citigroup Investment (And it Could Land Them Citigroup Referrals)

April 27, 2016

When BlueVine announced raising $40 Million from Menlo Ventures three months ago, they raised eyebrows in the marketplace lending community but they didn’t steal the spotlight. That’s because BlueVine’s core focus, invoice factoring, is arguably the least sexy segment of small business finance. Just hearing the phrase invoice factoring is enough to induce one into a coma. That of course is what made the age-old practice ripe for disruption. But even so, BlueVine isn’t limiting themselves to just that.

The company now offers business lines of credit with interest as low as 6.9%, according to their website. That makes them a competitor of OnDeck, Lending Club, Funding Circle and many others in a crowded field.

A new investment from Citigroup however could change everything for them. While the terms from Citi Ventures (the banks’s investing arm) were not disclosed, Arvind Purushotham, told CNBC that it’s possible that Citigroup forms a referral arrangement with BlueVine to help small business customers of the bank find attractive credit. That’s significant because Purushotham is a managing director at Citi Ventures.

Two weeks ago, OnDeck CEO Noah Breslow, told the crowd at the LendIt conference that partnering is a company’s only chance now to gain a real foothold in the industry. Breslow could speak from experience since OnDeck currently has a unique arrangement with JPMorgan Chase.

While the sources interviewed by CNBC stressed that the BlueVine-Citigroup investment did not constitute a commercial partnership, the stage seems to have been set for that to be possible in the future.

Even though BlueVine just started making loans 3 months ago (they have been factoring since 2013), loans already make up 15% of their overall business. This is one invoice factoring company that rival small business lenders won’t want to sleep on.

Transact 16 Photos

April 26, 2016Did you miss Transact 16? It was a little bit different this year for a particular group of regular attendees that have historically relied on credit card processors to “split” transactions. Merchant cash advance as it is known (or was known) has officially evolved into something else. You can read more about that here.

In the meantime, here’s a few photos from the show:

Don't forget to stop by Booth 564 @ETATRANSACT #TRANSACT16 & ask TJ/Maria/Jim how we can help you do great things! pic.twitter.com/Gixc6WJNfV

— RapidAdvance (@Rapid_Advance) April 21, 2016

Where are the rest of the pictures you ask? You should know by now that what happens in Vegas stays in Vegas.

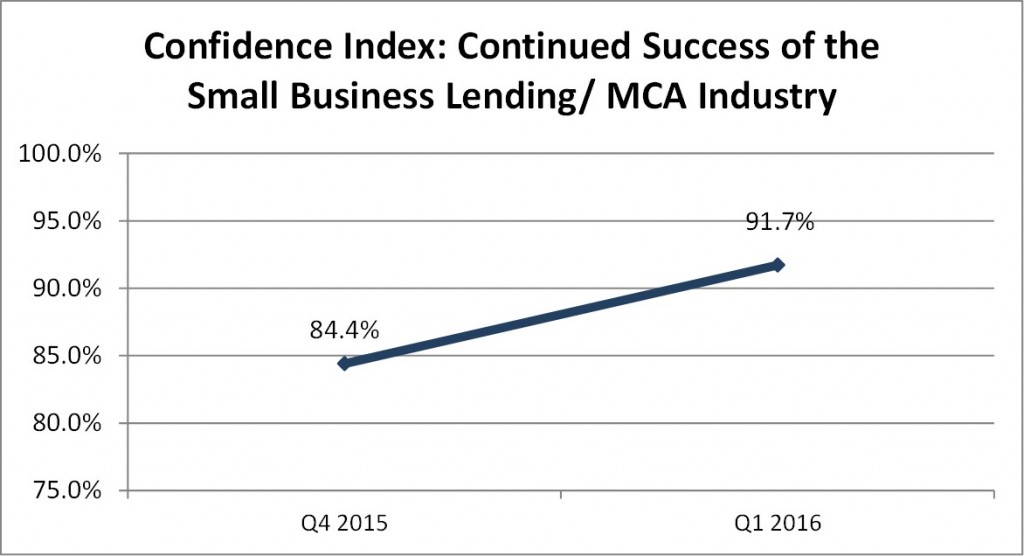

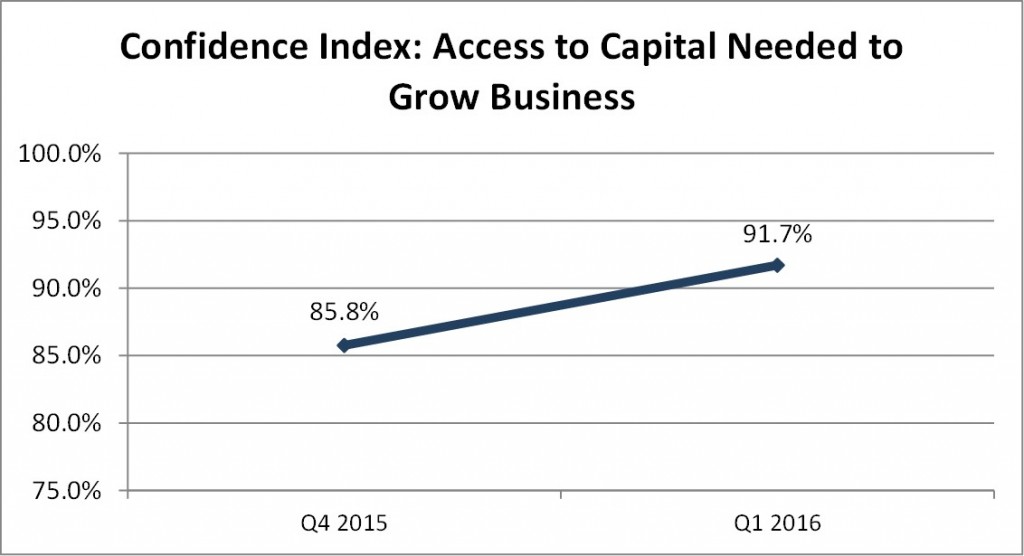

Small Business Lending and Merchant Cash Advance Industry Confidence On The Rise

April 25, 2016A fresh survey of industry captains revealed that their confidence is actually increasing.

Late last year, deBanked and Bryant Park Capital teamed up to produce the first ever comprehensive industry report on merchant cash advance and small business lending. More recently, eligible participants took a narrower survey to gauge their confidence in Q1 2016 and that was compared to results measured in Q4 2015.

The results were striking. Despite the apparent end of a euphoric love affair between investors and marketplace lenders earlier this month at LendIt, those on the small business side are still feeling very optimistic.

Confidence among industry captains increased from 84.4% in Q4 2015 to 91.7% in Q1 2016.

Confidence among industry captains in their ability to access capital needed to grow their business increased from 85.8% to 91.7%.

The 2015 comprehensive report is available for $495. Please contact sean@debanked.com for more information.

Splits Glitz or Fritz? – Transact 16 highlighted strange chapter in merchant cash advance history

April 21, 2016

It’s Opposite Day in the alternative business funding industry. Lenders are splitting card payments and merchant cash advance companies are doing ACH debits.

Jacqueline Reses was not an odd choice for Transact 16’s Wednesday morning keynote. Square, the company she works for, has continued to be a hot topic in the payments world for years. But what was striking is that Reses heads the lending division, the group that allows merchants to pay back loans through their future card sales. If that sounds very merchant-cash-advance-like, it’s because that’s exactly the product they used to offer before changing the legal structure behind them.

Split-payments, not ACH payments, have literally propelled Square and PayPal to the top of the charts of the alternative business funding industry. One individual on the exhibit hall floor posited that Square’s ability to originate loans through their payments ecosystem was the company’s real value; Payments itself was secondary. It’s a testament to the opportunities that split-payments affords to (as I argued 3 years ago on the ETA’s blog) a company well positioned to benefit from it.

Meanwhile, the companies at Transact that one would have historically described as merchant cash advance companies have mostly transitioned away from split-payments to ACH. Essentially, Square and PayPal embraced splits as an incredible strength while yesterday’s merchant cash advance companies viewed splits as a handcuff that limited scalability. The payment companies became merchant cash advance companies and the merchant cash advance companies became something else entirely, a diverse breed of loan and future receivable originators operating under a label people are now calling “marketplace lenders.” But even Square and PayPal, arguably the two companies at Transact doing the most split-payment transactions, claim to make loans, not advances.

Merchant Cash Advance as anyone knew it previously is dead

Ten years. That’s the average age of the small business funding companies that exhibited at Transact this week. They are but the last remaining players that probably considered the debit card interchange cap imposed by the Durbin Amendment of Dodd-Frank as being among the most significant legislation that affected their businesses.

A senior representative for one credit card processor told me at the conference that their biggest gripe with new merchant cash advance ISOs today is that they know almost absolutely nothing about merchant accounts. It’s not that they know less, they know nothing, he said.

One company was notably absent from the floor this year, OnDeck. They’ve since embraced the marketplace lending community as their home, just as many others have.

Nine years ago, I overheard a very influential person say that the first company to be able to split payments across the Global, First Data and Paymentech platforms would be crowned the “winner” of the merchant cash advance industry and by extension the wider nonbank small business financing space.

If one were to define the winner as the first company from that era to go public, well then those 3 platforms played no role. OnDeck was the first and they relied on ACH payments the entire way. They also refer to themselves these days as a nonbank commercial lender. If that doesn’t sound very payments-like, it’s because it’s not.

What cause is being Advanced?

At least four coalitions are currently advocating on the marketplace lending industry’s behalf, the Coalition for Responsible Business Finance, the Marketplace Lending Association, the Small Business Finance Association, and the Commercial Finance Coalition. The Transact conference is put on by the Electronic Transactions Association whose tagline is “Advancing Payments Technology.” In an age where new merchant cash advance ISOs know nothing about payments, it’s no wonder there’s a growing disconnect.

Could Transact now be one of the best kept secrets?

A few people from companies exhibiting say that they believed they stood a better chance to land referral relationships from payment companies by being there and that there was still a lot of value in landing those deals. Partnerships like these may be why the average exhibitor has been in business for 10 years while today’s new companies relying solely on pay-per-click, cold calling, or handshakes are falling on hard times.

Some payment processors acknowledged that merchant cash advance companies were still a good source to acquire merchant accounts, though the process by which that happens is not the same as it used to be. A lot of it is referral based now, according to one senior respresentative for a card processor. The funding company funds a deal via ACH and then refers them to the payment guy to try and convert that as an add-on. The residual earnings may not be as good as they used to be but that’s because they don’t have to do any work in this circumstance. In a sense, funders are still leading with cash but instead of the boarding process being mandatory, it’s an entirely separate sale that sometimes works and sometimes doesn’t. In that way, small business funding companies can be a good lead source for payments companies.

When I asked the senior representative if they really had success closing merchant accounts just off of a referral from a funding company, he looked at me incredulously, and said, “you used to do this, of course we do. that’s how this whole industry started.”

“What industry?” I asked.

What industry indeed…