Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

CFPB Rebuts its Unconstitutionality

October 21, 2016

The CFPB does not agree with the D.C. Circuit’s ruling that its leadership structure is unconstitutional, according to a reply filed in a separate case in the District of North Dakota. Believing itself constitutionally exempt from oversight by the President of the United States and any checks on its power whatsoever, the CFPB argued that the D.C. Circuit “based its decision on (a) the lack of sufficient historical precedent for the Bureau’s structure, and (b) a policy judgment that multi-member commissions are superior to single agency heads.”

It also suggested that it will be appealing the decision to the U.S. Supreme Court.

Remarkably, the D.C. Circuit Court’s ruling did not even call for the CFPB to be dismantled or have its funding reassigned to Congress, but instead ordered that it fall into line with the structure of other executive agencies where a reasonable system of checks and balances be implemented at the top. As originally created, CFPB Director Cordray was granted unilateral power that neither his agency colleagues or the President of the United States could check. Now, the CFPB appears unwilling to cede such authority.

“The CFPB’s concentration of enormous executive power in a single, unaccountable, unchecked Director not only departs from settled historical practice, but also poses a far greater risk of arbitrary decision-making and abuse of power, and a far greater threat to individual liberty, than does a multi-member independent agency,” the D.C. Circuit Court asserted.

Despite that, in CFPB v. Intercept Corporation, et al., the CFPB argued that “decision was wrongly decided and is not likely to withstand further review.”

A Glimpse into Square Capital’s Marketing

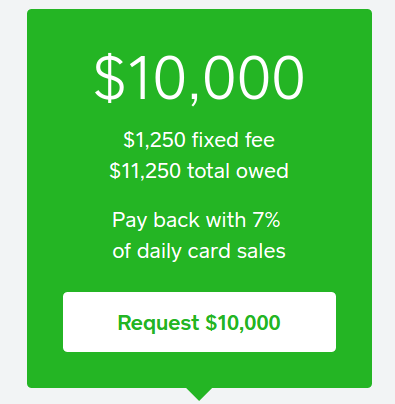

October 20, 2016As a merchant, Square has marketed their Square Capital program to me before. But this is the first time I’ve received direct mail marketing from them. Here’s a snapshot of what that looks like:

To view the potential offers, merchants are directed to log in to their Square accounts where they will see multiple terms. Even though their particular product is a loan made possible through Celtic Bank, all of the proposed loan offers are presented using the Total Cost of Capital method. That means cost is disclosed as a precise dollar amount so that potential borrowers will know exactly how much they will have to pay. Several studies have indicated that this is the easiest to understand, though it has been subject to some debate.

“There are no ongoing interest charges for your loan, only the one-time upfront fee that is listed as a dollar amount,” the Square Capital FAQ page states. “The total cost of the loan is a fixed fee and the total amount owed never changes.”

“There are no ongoing interest charges for your loan, only the one-time upfront fee that is listed as a dollar amount,” the Square Capital FAQ page states. “The total cost of the loan is a fixed fee and the total amount owed never changes.”

One of the defining features that makes Square Capital’s loan product different from a merchant cash advance or a purchase of future sales, is that Square enforces a fixed 18 month term. “If the loan hasn’t been repaid in full at the end of 18 months, the remaining loan balance will be due in full,” they state. That is completely unlike a purchase transaction in which there is no deadline or term. Even MCA purchase transactions that stipulate fixed daily payments do not actually have fixed terms. That’s usually because if a merchant’s sales activity rises or falls, they have the contractual right to request an adjustment to those payments to effectuate the basis of the agreement, that future sales be delivered in accordance with the unpredictable ebb and flow of business. That makes the date in which delivery will be satisfied in full unknowable. It’s that unknowable that can cause MCA transactions to be more expensive than their loan counterparts, though that is absolutely not always the case.

For Square, unknowable contract satisfaction dates likely made it difficult to bundle these deals up to sell off to institutional investors. Square Capital head Jackie Reses articulated this challenge during her appearance on an April 2016 LendIt stage. “From an investor side, that’s really where the savings are between the form of an MCA and the form of a loan, in that there’s an actual repayment date,” she said.

Even institutional investors recognize and understand that MCA purchase agreements do not have fixed terms.

Where a Non-Bank Falls, a Bank May Rise

October 19, 2016 Last week, CircleBack Lending disclosed that they were no longer originating loans, making them one of the first major casualties in the alternative lending industry. While even optimists projected that some platforms would eventually fail, the fact that this one coincided with Goldman Sachs’ announced kickoff into consumer lending, made their demise feel all too fatalistic.

Last week, CircleBack Lending disclosed that they were no longer originating loans, making them one of the first major casualties in the alternative lending industry. While even optimists projected that some platforms would eventually fail, the fact that this one coincided with Goldman Sachs’ announced kickoff into consumer lending, made their demise feel all too fatalistic.

Lending Club too, the symbolic leader of the online lending movement, announced some setbacks last week with their riskiest borrowers, which caused their stock price to plummet. In the background, banks such as Discover appear to be patiently waiting to swoop in on them should they stumble.

Even the recent announcement by JPMorgan Chase to double their commitment to Small Business Forward, a program meant to help small businesses access capital, suddenly feels a bit more threatening. Especially so given the bank’s partnership with OnDeck, an alternative business lender.

Goldman Sachs’ lending platform Marcus is offering borrowers no origination fees, no late fees, and no fees of any kind outside of interest charges. Discover is offering no origination fees and even no interest charges if the loan is repaid within 30 days.

On October 18th, the superintendent of New York’s banking regulator encouraged attendees of the New York Bankers Association conference to start their own online lending operations to compete with all the fintech startups.

If banks can match the speed and experience provided by alternative lenders, we just may see more platforms fall and banks rise in 2017.

For Lending Club, Ain’t Nothing But a E,F and G Thang

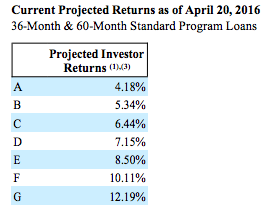

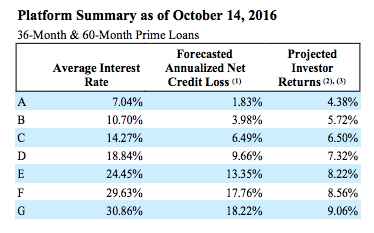

October 15, 2016Investing in a G-grade Lending Club note is projected to earn 313 basis points less than what was projected six months ago. The company published new projected investor returns in their 8-K filed on Friday that showed an expected return of 9.06% on G-grade notes. That’s down from the 12.19% figure they published in an April filing. F-grade note projections decreased by 155 basis points. For Es, it’s down 28 basis points.

“Rate increases are concentrated in Grades F and G with marginal changes in other grades,” the company announced on Friday while reporting a weighted average 26 basis point interest rate increase. But will rate increases save the Fs and Gs from plummeting returns?

As G is the most risky grade, that means the most risky borrowers on Lending Club are projected to earn investors only 9.06%. Is all that risk worth it? Or perhaps more importantly, is that projection even realistic? Six months ago, the riskiest class was projected to earn 12.19%. Nothing has really changed from a macroeconomic standpoint since then, so it’s difficult to even pinpoint why investors should expect a 25% lower return on the riskiest borrowers all of the sudden or why they should be confident that it won’t get worse.

On the plus side, projected returns on As through Ds are up.

Who’s Stealing Lending Club’s Borrowers?

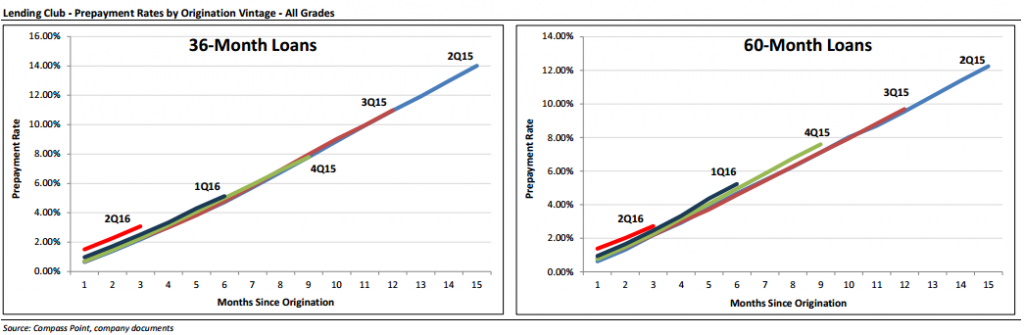

October 11, 2016 A shocking amount of borrowers pay off their Lending Club loans early, the data shows, but the trend has accelerated recently. What’s happening out there?

A shocking amount of borrowers pay off their Lending Club loans early, the data shows, but the trend has accelerated recently. What’s happening out there?

3.07% of people that took a 36-month loan from Lending Club in the 2nd quarter of this year had already paid them off in full just two months later, according to a report published by Compass Point. That’s double the pace that Lending Club experienced three years ago. Meanwhile, 1.51% of Q2 borrowers paid off their 36-month loan in less than 1 month!

And the trend continues as the loans age. Depending on which Lending Club vintage you examine, more than 25% of borrowers are paying off their loans prior to maturity. Several Lending Club users that I’ve connected with suspect that these borrowers are simply paying off these loans using the proceeds of another loan. Discover is a prime suspect, what with their no origination fees and marketing campaigns directed directly at Lending Club. It might also be Prosper or even Lending Club giving the borrower a second loan to pay off their first. There’s no way to know for sure but the trend is notable for two reasons.

Retail Investors Get Sacked

Retail Investors Get Sacked

1. Retail investors on the platform are actually penalized when loans are paid off in full after the 12th month but prior to maturity. Lending Club assesses a 1% fee to the investor purely on the outstanding principal when this happens, so the investor is not only deprived of their future interest but also unfairly hit with a penalty charge over which they have no control. And it’s material because two to three times as many borrowers are paying off their loans early after the first 12 months as they are before it. That’s a lot of penalties for investors to get stuck with especially since their returned cash will no longer generate a return until they’re able to reinvest it into a loan of equal quality. That used to mean a cash drag of a few days, but shifts in the industry have created instances in which there might be no new loans available to replace the previous ones.

FICO Arbitrage?

2. Even the lowest quality borrowers, Grade G, seem to have no trouble paying off their loans early, according to Compass Point’s report. One might wonder how they’re obtaining credit outside of Lending Club so easily. One theory put forth by some retail investors on the Lend Academy forum is FICO arbitrage. Basically, when a borrower consolidates their credit card debt using a Lending Club loan, they are reducing their revolving credit usage and increasing their installment credit. FICO’s algorithm might not correctly interpret this as a 1:1 transfer of debt and instead give the borrower’s score a boost. The new artificially improved score could signal to rival lenders that the borrower is deserving of an even lower interest rate. It’s common knowledge that a creditor could request from a credit bureau the names and addresses of consumers above a certain score and then offer credit to those consumers. And that might be why many borrowers seem to only be using Lending Club as a pit stop on their refinancing journey.

Of course if borrowers are using a second Lending Club loan to pay off their first loan, then the above two scenarios have far more serious implications, but as of now all that is known is that the pace of early payoffs is accelerating. Compass Point’s report states, “while still early, we believe the shift in trend is worth monitoring as it could impact retail and institutional investor returns from Lending Club loans.”

CFPB’s Power Structure Ruled Unconstitutional – Concentration of Enormous Power a Threat to Individual Liberty

October 11, 2016 The enforcement agency long panned for not being accountable to anyone, including Congress, has finally been checked by the judicial branch. On Tuesday, October 11th, the United States Court of Appeals for the District of Columbia Circuit, ruled the CFPB’s structure is unconstitutional because as a single-person-run agency of the executive branch, it is not even accountable to the President of the United States. The CFPB’s existence challenges the very framework set forth by the nation’s founders, the Court asserted.

The enforcement agency long panned for not being accountable to anyone, including Congress, has finally been checked by the judicial branch. On Tuesday, October 11th, the United States Court of Appeals for the District of Columbia Circuit, ruled the CFPB’s structure is unconstitutional because as a single-person-run agency of the executive branch, it is not even accountable to the President of the United States. The CFPB’s existence challenges the very framework set forth by the nation’s founders, the Court asserted.

The opening of the 110-page decision cites Article II of the United States Constitution. “The executive Power shall be vested in a President of the United States of America,” adding that Article II grants the President alone the authority and responsibility to “take Care that the Laws be faithfully executed.” As time has passed however, independent executive agencies have been created and overseen by multi-member commissions, which have become an acceptable check on the individual power of one person.

In other words, to help preserve individual liberty under Article II, the heads of executive agencies are accountable to and checked by the President, and the heads of independent agencies, although not accountable to or checked by the President, are at least accountable to and checked by their fellow commissioners or board members. No head of either an executive agency or an independent agency operates unilaterally without any check on his or her authority. Therefore, no independent agency exercising substantial executive authority has ever been headed by a single person. Until now. – Excerpt from the Court of Appeals decision

As it stood previously, CFPB Director Richard Cordray essentially had unlimited power to write his own rules, attack and fine companies whether warranted or not, personally motivated or not, on whatever whim he so desired. While very unpopular among Republicans and even among some Democrats, he received recent acclaim for his agency’s work on the Wells Fargo fake account scandal. Other moves have been more dubious, like their foray into lawmaking without the legislative branch (see a 1341-page law they invented) and reinterpreting their own statutory authority by expressing an interest to regulate commercial finance, all while potentially engaging in “chokepoint-like” tactics to intimidate business models they don’t like.

The Court of Appeal’s decision is especially damning because the CFPB was caught making legal errors in their enforcement action against a mortgage lender that led to this review to begin with. In effect, in a case that questioned whether or not the agency’s mere existence is rogue in that of itself, the CFPB was actually going rogue in how they applied the law. Basically, they removed any doubt about whether or not oversight should be warranted.

The CFPB will not be dismantled as a result of the decision and it will still possess incredible enforcement power. The decision instead directs the organization to conform to an existing executive agency structure, either through a multi-member commission or be directly accountable to the President of the United States.

The WSJ reported that the CFPB had no comment and is currently reviewing the decision.

“The CFPB’s concentration of enormous executive power in a single, unaccountable, unchecked Director not only departs from settled historical practice, but also poses a far greater risk of arbitrary decision-making and abuse of power, and a far greater threat to individual liberty, than does a multi-member independent agency,” the Court asserted.

Merchant Cash Advance Misinformation Abounds – What’s A Broker To Think?

October 10, 2016

Last week, at least two panelists at the major commercial loan broker conference critiqued merchant cash advances, even going so far as to assign an arbitrary cost to them. Craig McGrain, President of factoring company Durham Funding, said they cost about 75%. Bob Coleman, owner of The Coleman Report, an SBA loan journal, said that merchant cash advance contracts should stipulate that prices are basically equivalent to 100% APR. Neither accurately describes a merchant cash advance if for no other reason than because a merchant cash advance is merely a methodology or a mechanism, not a price. The term itself is derived from the process of making a merchant an advance on their future projected sales. With hundreds of companies employing that concept, some are able to do it at a low cost and others at a high cost.

And it’s obviously the high cost ones to which their disdain was directed. But even then, when MCAs are properly structured as a purchase of future sales, there is no calculable APR because there is no assigned time frame, predetermined payments, or interest rate. This doesn’t mean an MCA product can’t be expensive, because surely they can be, but assigning randomly high percentages to scare people only compounds the misinformation that has persisted for years.

On a panel I participated in with Bob Coleman, Coleman said that these purchases were really just loans. The New York Supreme Court, however, repeatedly disagrees with him. In Platinum Rapid Funding Group Ltd v. VIP Limousine Services, Inc. and Charles Cotton, the court affirmed a purchase of future receivables for an upfront payment, adding that the request for the Court to convert the Agreement to a loan and assign an interest rate to it would require unwarranted speculation, and would contradict the explicit terms of the sale of future receivables in accordance with the Merchant Agreement.

In Merchant Cash & Capital, LLC v G&E Asian Am. Enter., Inc., the court reached the same conclusion.

With regard to McGrain of Durham Funding, he said that 70%-80% of companies that apply for his company’s factoring services have already used an MCA. This kind of competitive pressure is probably a leading reason why a factor would mischaracterize MCAs. In fact, the factoring industry has felt so threatened by MCAs, that two years ago the International Factoring Association voted to ban all MCA companies from their organization.

This isn’t to suggest that factoring is an inferior product and that MCA is the newer better thing. On the contrary, factoring is an excellent loan alternative and to McGrain’s credit he said that he believed the free market would work everything out. To facilitate that, more MCA brokers need to be educated on factoring and SBA lending. And in return commercial finance brokers need to understand the true nuts and bolts of MCA. That process gets sullied when misinformation abounds. Merchants will get the best help when the brokers fully understand all of the market’s options.

My panel with SBA lending expert Bob Coleman and equipment leasing veteran Kit Menkin at the NACLB conference last week highlighted some differences of opinions across these closely related industries but also demonstrated areas in which we all agree. Small businesses have different needs and it’s up to the brokers to prescribe the most appropriate solution. Whether it’s short-term or long-term, cheap or expensive, proactive or reactive, there’s capital out there. Hopefully the kind of cooperative engagement the NACLB conference provided this year will continue to be fostered for years to come.

Loan Brokers Have it Easy in Alternative Lending

October 6, 2016 On a panel at the NACLB Conference in Las Vegas, Tom Zernick, the President of SBA Lending at First Home Bank explained that signing up a broker isn’t so simple. They have to conduct due diligence on them in advance, he said, because ultimately all their broker partners have to be reported to the SBA. Brokers can receive a 1% commission for completing a deal and also charge a separate fee to the merchant on their own but the merchant has to be aware of all of it and all the amounts reported to the SBA, he said.

On a panel at the NACLB Conference in Las Vegas, Tom Zernick, the President of SBA Lending at First Home Bank explained that signing up a broker isn’t so simple. They have to conduct due diligence on them in advance, he said, because ultimately all their broker partners have to be reported to the SBA. Brokers can receive a 1% commission for completing a deal and also charge a separate fee to the merchant on their own but the merchant has to be aware of all of it and all the amounts reported to the SBA, he said.

And even that might not be enough on its own, according to the panel that Zernick was part of. Brokers should be keeping a log of the services performed to earn those fees and the hours spent on each task, like an attorney would.

Contrast that with alternative lending where brokers and fees are not reported to any agency.

One good thing about SBA lending these days though, according to Zernick, is that when he started in the business about 30 years ago, he joked it could take about a year to fund a loan but that today in reality it takes less than 30 days on average to fund.