Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Loan Brokers Have it Easy in Alternative Lending

October 6, 2016 On a panel at the NACLB Conference in Las Vegas, Tom Zernick, the President of SBA Lending at First Home Bank explained that signing up a broker isn’t so simple. They have to conduct due diligence on them in advance, he said, because ultimately all their broker partners have to be reported to the SBA. Brokers can receive a 1% commission for completing a deal and also charge a separate fee to the merchant on their own but the merchant has to be aware of all of it and all the amounts reported to the SBA, he said.

On a panel at the NACLB Conference in Las Vegas, Tom Zernick, the President of SBA Lending at First Home Bank explained that signing up a broker isn’t so simple. They have to conduct due diligence on them in advance, he said, because ultimately all their broker partners have to be reported to the SBA. Brokers can receive a 1% commission for completing a deal and also charge a separate fee to the merchant on their own but the merchant has to be aware of all of it and all the amounts reported to the SBA, he said.

And even that might not be enough on its own, according to the panel that Zernick was part of. Brokers should be keeping a log of the services performed to earn those fees and the hours spent on each task, like an attorney would.

Contrast that with alternative lending where brokers and fees are not reported to any agency.

One good thing about SBA lending these days though, according to Zernick, is that when he started in the business about 30 years ago, he joked it could take about a year to fund a loan but that today in reality it takes less than 30 days on average to fund.

Merchant Cash Advance’s Impact on Factoring

October 6, 2016 A little more than two years ago, the International Factoring Association voted to ban merchant cash advance companies from membership, citing loose underwriting standards and competitive pressure.

A little more than two years ago, the International Factoring Association voted to ban merchant cash advance companies from membership, citing loose underwriting standards and competitive pressure.

On Wednesday, at the NACLB conference in Las Vegas, Craig McGrain, President of factoring company Durham Funding, hinted on a panel at just how strong that competitive pressure has become. According to him, about 70-80% of their applicants today already have a merchant cash advance. Five years ago, it was only 5% of businesses, he said. He thinks a lot of that has to do with small businesses not knowing what all of their available options are.

The numbers may not be all that shocking considering that Funding Circle VP Michael Rabil also said at the conference that 30-40% of their applicants already have an MCA. Funding Circle provides small business term loans.

That’s a lot of merchants turning to MCA before finding their way to another product.

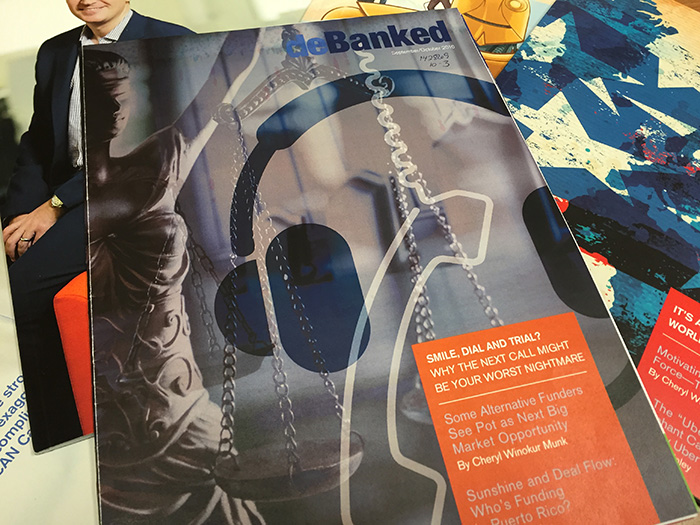

Mind The TCPA And Get deBanked All Over Again

October 4, 2016

deBanked’s September/October 2016 issue is set to go in the mail very soon. And in this issue, we wade chest-deep into a trend that has many brokers and funders worrying behind closed doors. In the last year there has been a surge of TCPA lawsuits, whether for robo-dialing, Do-Not-Call-List violations or something else. Are industry players being irresponsible or is there something else amiss? deBanked went looking for the answers and you might be surprised by some of the things we found.

If you’re wondering what TCPA lawsuits even are or how they might affect you, this story will hopefully teach you about the risks of marketing over the phone. Smile Dial… and Trial? You’ll want to read this.

If you’re already subscribed to receive the magazine, you’ll be getting your copy soon. If not, you should SUBSCRIBE NOW FREE

Time To Get Back On Track! The Commercial Loan Broker Conference and Lend360 Kick Off This Week

October 2, 2016

If you’re one of those people who book things at the last minute, well then there’s technically still time to register for the NACLB’s Commercial Loan Broker Conference and Lend360. As each are taking place over roughly the same few days this week, you should expect a great experience regardless of which one you choose to go to. You could also split your staff up and attend both!

I’ll personally be at the Commercial Loan Broker Conference at the Red Rock Casino in Las Vegas and am scheduled to participate in an industry reporter’s panel there early Thursday morning.

At last year’s Lend360, Congressman David Scott (D-GA) famously blessed the online lenders after urging them to educate policymakers about what they do.

The industry hopes to see you at one or both of these shows:

Commercial Loan Broker Conference

Who should go?: Business loan brokers, MCA brokers, equipment finance companies, lenders, MCA funders, investors, etc.

When is it?: October 4 – 6

Where is it?: Las Vegas

How do I sign up?: Register here

Lend360

Who should go?: Consumer Lenders, Business loan brokers, MCA brokers, MCA funders, investors, etc.

When is it?: October 5 – 7

Where is it?: Chicago

How do I sign up?: Register here

Bonus: Use promo code deBanked15 for 15% off the registration price

RIP The Retail Investor in Marketplace Lending?

September 30, 2016 Now that credible sources are finally conceding that the pure marketplace lending model is dead, Prosper announced in an email on Thursday that they are shutting down their secondary market for retail investors.

Now that credible sources are finally conceding that the pure marketplace lending model is dead, Prosper announced in an email on Thursday that they are shutting down their secondary market for retail investors.

“We are writing to let you know that as of October 27, 2016, Prosper will no longer offer the Folio Investing Note Trader platform, the secondary market for Prosper Notes. Prosper has found over time that very few investors are using the secondary market and, as such, has made the decision to no longer offer this service. We apologize for any inconvenience that this causes. Prosper remains committed to its retail investor clients and to providing them a great experience.”

An official statement sent by Prosper CEO Aaron Vermut to LendAcademy’s Peter Renton said that the move in no way changes their commitment to the retail investor. But some vocal retail investors did not appear convinced, according to a forum thread on the subject. The few reddit comments posted about this announcement also showed concern.

In July, I joked that marketplace lending would become Goldman Sachs lending, a marketplace for Wall Street by Wall Street. Coincidentally, representatives from Goldman Sachs actually spoke during two presentations at the Marketplace Lending and Investing conference that took place earlier this week in NYC. During one, Goldman Sachs Bank USA CEO Stephen Scherr, laid out the company’s plan to compete against marketplace lenders by relying on their own balance sheet, something they see as an advantage.

In the meantime, Prosper’s elimination of its secondary market means that retail note buyers will need to hold the notes to maturity, making them totally illiquid. While investors may not have been using the market very much historically, permanently dismantling the escape hatch isn’t likely to inspire confidence.

Coincidentally, Lending Club sent out their own email hours after Prosper’s, assuring retail investors that they were committed to providing them with a great investment experience. “We’re proud that we have the largest retail investor base of any company in the marketplace lending industry and are committed to expanding our offering so more retail investors can access Lending Club products,” wrote Patrick Dunne, Lending Club’s Chief Capital Officer. “We have ambitious long term goals. We aspire to allow every type of investor – individual retail and institutional investors – to participate in what we believe is a compelling product that can offer solid risk-adjusted returns.”

it remains to be seen what exactly will happen next for these companies and the industry.

Marketplace Lending: Where No One Makes Any Money?

September 28, 2016 At the Marketplace Lending and Investing conference in NYC, LendAcademy founder and p2p lending expert Peter Renton asked a group of panelists a stunning question, “Why is no one making any money?”

At the Marketplace Lending and Investing conference in NYC, LendAcademy founder and p2p lending expert Peter Renton asked a group of panelists a stunning question, “Why is no one making any money?”

For the sake of context, Renton explained that if banks were basically the most profitable business type on Earth, then how could it be that those companies infringing on their space or partnering up with them weren’t partaking in that.

The question was posed to Noah Breslow of OnDeck and Sam Hodges of Funding Circle, two of the most high profile players in the alternative small business lending industry. Both companies have been operating at a loss despite being in business for quite some time, in the case of OnDeck, almost ten years now.

Breslow took the question in stride, saying that “first you have to look at the unit economics of a loan. If you’re not profitable there, you’re in trouble. You can’t scale your way out of that.” He added that there are indeed competitors that fail on this test alone who won’t likely be around for much longer.

But as to why they personally were still not profitable? He put a lot of emphasis on their continued strategy to expand.

Funding Circle’s Hodges offered a similar explanation, saying that they have spent a lot of resources on expanding into five countries. He also said that “their plan takes them to profitability next year.”

Of course, neither OnDeck nor Funding Circle are as diversified in their product offerings as banks, explaining perhaps why the analogy between bank profitability and their profitability isn’t apples to apples. LoanDepot CEO Anthony Hsieh touched upon this in his presentation earlier in the day when he said that his company acquires an astounding 600,000 leads per month, a record high, but with very low conversions. So many [lenders] are monoline, he said.

Surely that affects the bottom line.

Google Payday Loan Ad Ban Conspiracy Theory Gains Steam: It Was The CFPB

September 28, 2016 This past May, Google told the world that they were the good guys.

This past May, Google told the world that they were the good guys.

That’s when they banned payday lending ads from their search results to “protect [their] users from deceptive or harmful financial products” all the while brushing aside the fact they were significant investors in LendUp, a payday loan company.

But LendUp wasn’t just any payday company. They were disrupting the entire game, according to a 2013 story that appeared in TechCrunch that hyped up how they were all about helping borrowers with poor credit improve their credit scores so that they could move up the ladder.

Less than three years later, LendUp CEO Sasha Orloff was still preaching the same principles. “Everything has to be transparent. There is no fine print. No hidden fees. And everything has to get someone to a better place,” Orloff insisted.

But that wasn’t true, according to a Consent Order published by the CFPB and settlement agreement released by the California Department of Business Oversight, in which the company agreed to pay millions in refunds and penalties. LendUp miscalculated APR and for years did not even report the payment history of many eligible borrowers to credit agencies. In fact no loan information was even reported to any credit bureau at all up until February 2014. They also weren’t transparent about their fees.

“Many of the benefits Respondent advertised as available to consumers who moved up the LendUp Ladder were, in fact, not available,” the CFPB asserts in its September 26th order. “Although it advertised all of its loans nationwide, from 2012 until 2015, Respondent did not offer any loans at the Platinum or Prime levels outside of California. In many states Respondent still does not offer such loans.”

Not that they did any better in California, where the DBO charged them with violating basic state laws through expedited funding fees, extension fees, and the condition that they buy other goods or services in order to get a loan.

Not that they did any better in California, where the DBO charged them with violating basic state laws through expedited funding fees, extension fees, and the condition that they buy other goods or services in order to get a loan.

LendUp told the WSJ that the settlements “address legacy issues that mostly date back to our early days as a company, when we were a seed-stage startup with limited resources and as few as five employees.”

But LendUp may just be a pawn in a bigger game between the CFPB and Google.

I fingered the CFPB as being the likely culprit behind Google’s payday loan advertising ban back in May 2016, when it was very likely that a CFPB investigation of LendUp was currently taking place. That theory was even picked up by The New Yorker. Today it looks awfully likely.

The CFPB mentioned LendUp’s use of facebook advertising and Internet search results advertising in its Order against the company. “Respondent used online banner advertisements appearing on Facebook and with Internet search results (emphasis mine) that included statutory triggering terms, but Respondent failed to disclosed in those advertisements the APR and whether the rate could be increased after consummation.”

Internet search results were used to carry out the deceptive practices, they allege? Sounds like Google had a potential problem on their hands.

Let’s recap:

- November 2013 and January 2016: Google Ventures invested in LendUp which promoted itself as a disruptively transparent and educational short term lender whose mission was to help consumers move up the ladder

- May 2016: Google suddenly bans payday loan ads from their search results seemingly out of nowhere

- September 2016: The CFPB and California DBO announce settlement orders over LendUp’s deceptive practices, wherein it was alleged that LendUp did not exactly do what it advertised and their ads in Internet search results violated TILA and Regulation Z

Was a CFPB investigation the real reason that Google had a change of heart about its lucrative payday loan advertising revenues?

It’s hard to ignore the evidence.

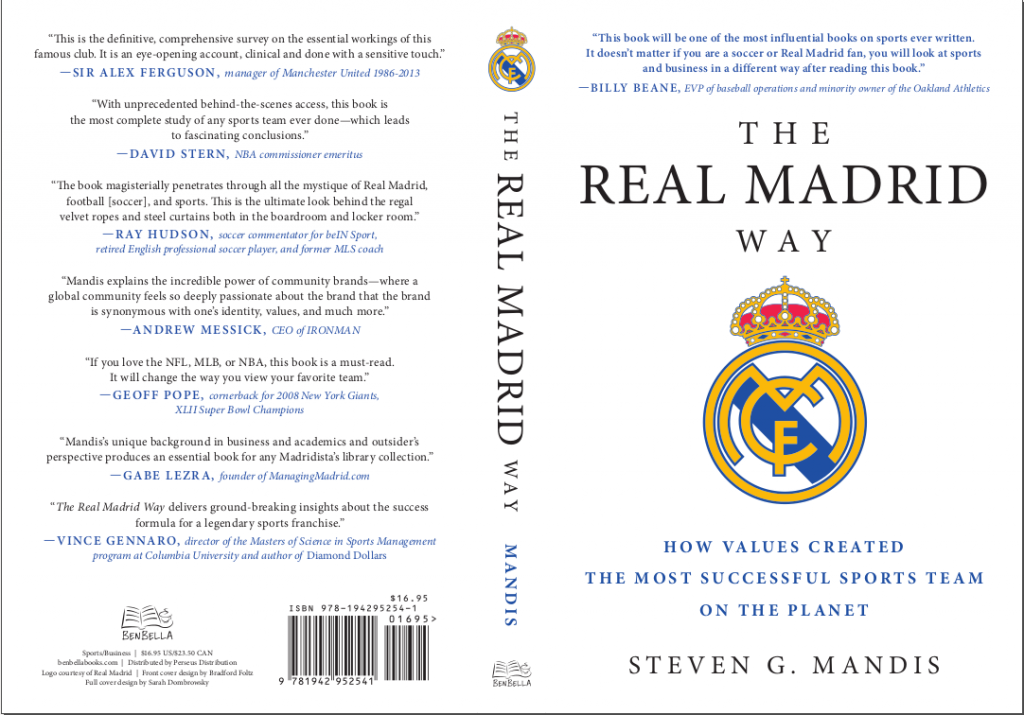

Kalamata Capital Chairman Steven Mandis Authors Second Book

September 25, 2016 Kalamata Capital Chairman Steven Mandis is doing more than just approving small businesses up to $750,000 in under 24 hours. He’s also just authored a new book, The Real Madrid Way: How Values Created the Most Successful Sports Team on the Planet.

Kalamata Capital Chairman Steven Mandis is doing more than just approving small businesses up to $750,000 in under 24 hours. He’s also just authored a new book, The Real Madrid Way: How Values Created the Most Successful Sports Team on the Planet.

Not a subject you expected from a tech-driven small business lender? Steven Mandis is not your average industry executive…

Prior to Kalamata, he worked at Goldman Sachs in the investment banking, private equity, and proprietary trading areas. He assisted Hank Paulson and other senior executives on special projects and was a portfolio manager in one of the largest and most successful proprietary trading areas at Goldman. After leaving Goldman, he cofounded a multibillion-dollar global alternative asset management firm that was a trading and investment banking client of Goldman’s.

During the financial crisis, Mandis was a senior adviser to McKinsey & Company before becoming chief of staff to the president and COO of Citigroup and serving on executive, management, and risk committees at the firm.

He’s also an adjunct professor at Columbia Business School, where he teaches classes of MBA and executive MBA students on strategic issues facing investment banks and the European financial crisis.

His first book, What Happened to Goldman Sachs? was widely acclaimed. “Several authors have tackled the question of how Goldman’s culture changed post-1999 but none so deftly as Steven G. Mandis, a banker-turned-sociologist,” wrote the Wall Street Journal. I also read it cover-to-cover myself back in March of 2015.

In Real Madrid, “Mandis is the first researcher to rigorously analyze both the on-the-field and business aspects of a sports team. What he learns is completely unexpected and challenges the conventional wisdom that moneyball-fueled data analytics are the primary instruments of success.”

Former NBA Commissioner David Stern said of the book, “With unprecedented behind-the-scenes access, this book is the most complete study of any sports team ever done–which leads to fascinating conclusions.”

Are you a finance buff? Sports buff? Perhaps both? You’ll want to read his new book.