Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Prosper, A Marketplace for the World’s Richest Banks and Billionaires?

February 28, 2017

Credit Suisse, Deutsche Bank, Goldman Sachs, Morgan Stanley, and funds tied to some of the world’s richest billionaires (including George Soros) all make up the “consortium of institutional investors” and “syndicate of lenders” involved in Prosper’s recently announced landmark deal. The terms allow for the investors to purchase up to $5 billion of loans on the platform while the lenders will provide warehouse financing up to $1 billion. It’s safe to say that this is not your father’s peer-to-peer lender.

The WSJ reported too that investors will receive warrants to buy equity in Prosper that’s tied to the amount of loans they buy, all the way up to 35% of the company if they buy the full $5 billion.

Prosper used to call itself a “peer-to-peer lending marketplace” but these days it’s adopted a slightly different label, “consumer lending marketplace.”

Back in July, I half-jokingly scoffed at the phrase marketplace lending as the industry had begun to call itself, seeing that it was morphing into just Wall Street lending after Goldman Sachs announced it would actually be launching an online consumer lending arm to compete against Lending Club and Prosper.

The deal is obviously great for Prosper, whose future seemed kind of up in the air, but it’s hard to get excited about the world’s biggest banks and richest funds now being the consortium behind an online lender who pioneered peer-to-peer lending, if things like peer-to-peer lending excited you.

To be fair, peers/retail investors can still invest on the platform too so I guess there’s that.

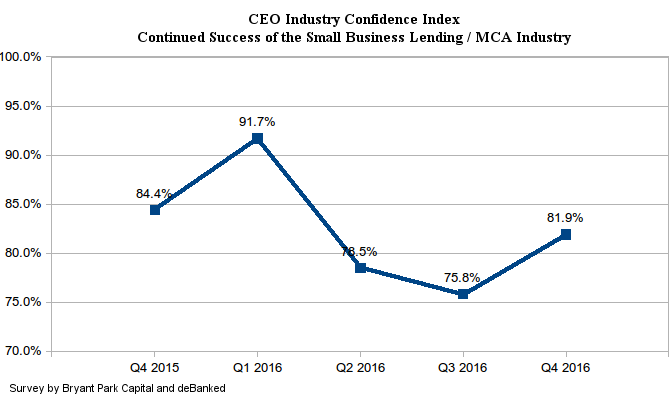

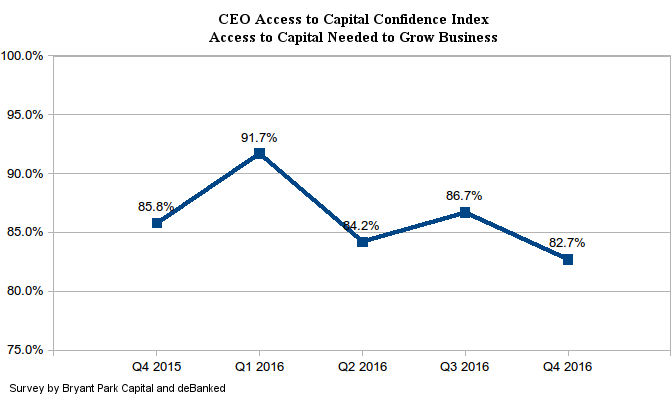

Confidence Stable For Small Business Lenders and MCA Companies

February 26, 2017Recent events may be putting a slight damper on the confidence of industry CEOs in being able to access capital needed to grow their businesses, but continued success of the industry in general is ticking back up. This data is according to the latest survey conducted by Bryant Park Capital and deBanked of small business lending and merchant cash advance company CEOs.

Confidence in the industry’s continued success bumped back up to 81.9% in Q4, while confidence in being able to access capital reached its lowest level since the survey’s inception. Still, at 82.7%, it’s high.

In late November of 2016, CAN Capital, one of the industry’s largest companies, encountered problems that caused the company to suspend funding. Several of their competitors since then have reported a boost in submission volume, which they partially attributed to that event.

Pressure on companies to merge or exit the market may also be kindling optimism for larger players who stand to gain market share.

Prospa, Now Valued at $235 Million, is a Major Online Small Business Lender

February 22, 2017 Online small business lending in Australia is taking off, especially for Sydney-based Prospa, who according to the Australian Financial Review, has slightly more than half of the industry’s market share. The company just announced a $25 million (AUD) equity round led by AirTree Ventures that pegged Prospa’s value at $235 million (AUD).

Online small business lending in Australia is taking off, especially for Sydney-based Prospa, who according to the Australian Financial Review, has slightly more than half of the industry’s market share. The company just announced a $25 million (AUD) equity round led by AirTree Ventures that pegged Prospa’s value at $235 million (AUD).

Prospa is significant in that it received early support from US-based Strategic Funding, the same company that just absorbed the US operations of Capify. A 2013 press release said that Strategic would be providing the technology for the electronic servicing, underwriting and cash management of all Prospa Advance accounts in Australia in addition to jointly funding all the merchant cash advances and loans they originated. Sources say however that the arrangement is no longer in effect.

In September 2015, The Carlyle Group, one of the largest private equity firms in the world, participated in a $60 million round for the company. Prospa has now funded more than $250 million to small businesses since inception.

“The market in Australia has been very ripe for alternative finance,” Prospa co-CEO Beau Bertoli said to deBanked about 18 months ago. “We see an opportunity for the alternative finance segment to be more dominant in Australia than it is in America.”

The Australian Financial Review cites Bertoli as more recently saying that the market there could grow to at least $20 billion in the next five years.

Similar to offers in the US, Prospa lends between $5,000 to $250,000 for loans up to one year.

‘Peers’ Continue Retreat from Lending Club

February 18, 2017 The peer aspect of peer-to-peer lending continued to erode last year, according to Lending Club’s year-end earnings presentation. Self-managed individuals, those still making their own investment decisions, only made up $263 million of their 4th quarter’s origination volume, reaching the lowest level in two years. That’s nearly 38% lower from the peak of $419 million in Q1 of 2016.

The peer aspect of peer-to-peer lending continued to erode last year, according to Lending Club’s year-end earnings presentation. Self-managed individuals, those still making their own investment decisions, only made up $263 million of their 4th quarter’s origination volume, reaching the lowest level in two years. That’s nearly 38% lower from the peak of $419 million in Q1 of 2016.

Overall monthly originations haven’t really moved, hovering at around $2 billion per quarter over the last 3 quarters, down from the peak of 2016’s Q1 when they hit $2.75 billion. There’s money coming from somewhere though, of course. A chart in the presentation revealed that 74% of Lending Club’s Q4 originations came from banks and managed accounts. The managed accounts category is comprised primarily of asset managers who invest mainly in marketplace lending.

A glance at Lending Club’s self-managed individual originations as a percentage of total originations per quarter is below:

| Q4 2013 | Q1 2014 | Q2 2014 | Q3 2014 | Q4 2014 | Q1 2015 | Q2 2015 | Q3 2015 | Q4 2015 | Q1 2016 | Q2 2016 | Q3 2016 | Q4 2016 |

| 27% | 27% | 23% | 25% | 19% | 19% | 15% | 15% | 13% | 15% | 17% | 14% | 13% |

Retail investors were largely skimmed over during the Q4 earnings call, with CEO Scott Sanborn and CFO Tom Casey choosing to focus their attention on bank participation. “As you know, banks returning to the platform has been a priority for us and acts as an endorsement of our strength and compliance and controls,” Casey said.

Using the Seeking Alpha transcript as a guide, the word bank was said on the call 32 times while retail investor was only mentioned once.

To that end, Lending Club’s announcement highlighted its bank funding achievement.

Meanwhile, the word retail doesn’t exist anywhere in the announcement unless you count the necessary Safe Harbor Statement.

RIP the retail investor.

Layoffs, Big Losses for OnDeck in Q4

February 16, 2017 OnDeck weathered a brutal fourth quarter driven largely by an increase in provision for loan losses which increased to $55.7 million, up from $20.0 million in the comparable prior year period. $18.7 million of this can be attributed to loans with original maturities of 15 months or longer whose performance has deviated or is expected to deviate, the company said. “As a result, the Provision Rate in the fourth quarter of 2016 was 10.2% compared to 5.6% in the comparable prior year period,” the company reported. For the full year of 2016, the Provision Rate was 7.4%, compared to 5.8% in 2015. CFO Howard Katzenberg said on the earnings call that it will likely continue to hover at around the 7% level.

OnDeck weathered a brutal fourth quarter driven largely by an increase in provision for loan losses which increased to $55.7 million, up from $20.0 million in the comparable prior year period. $18.7 million of this can be attributed to loans with original maturities of 15 months or longer whose performance has deviated or is expected to deviate, the company said. “As a result, the Provision Rate in the fourth quarter of 2016 was 10.2% compared to 5.6% in the comparable prior year period,” the company reported. For the full year of 2016, the Provision Rate was 7.4%, compared to 5.8% in 2015. CFO Howard Katzenberg said on the earnings call that it will likely continue to hover at around the 7% level.

The company lost $36.5 million in Q4 and $86.5 million for the year.

To try and turn things around, OnDeck is laying off up to 11% of their staff as part of a “cost rationalization plan.”

James Hobson, their COO, recently announced his resignation and March 15th is his last official day.

On the earnings call, Katzenberg wouldn’t say how many loans in their portfolio were 15 months or longer, but did say that it’s more than a third of their book. This is notable given that this segment is the one in which performance isn’t matching their models and led to the recalibration of loss expectations.

Meanwhile CEO Noah Breslow explained that losses did not stem from their partnership with Chase since Chase held all those loans on their own balance sheet. Breslow said their role in that relationship is servicing.

No origination channel was directly responsible for the loss provision increase. One analyst surmised if perhaps third party brokers or funding advisors, as OnDeck calls them, might be responsible, but the company said that origination channel wasn’t a factor.

Despite the fact that OnDeck is now using the 5th generation of their proprietary OnDeck Score, they were unable to predict performance on loans that now make up more than a third of their portfolio, yet the company said they remain very confident in their scoring model.

“Loans sold or designated as held for sale through OnDeck Marketplace represented 15.8% of term loan originations in the fourth quarter of 2016 compared to 39.8% of term loan originations in the comparable prior year period,” the company reported.

‘Debt Collection Terrorist’ Wants FCC to Get Rid of Implied Consent in TCPA

February 9, 2017 Craig Cunningham, the serial TCPA plaintiff who once aspired to author a book titled, Tales Of A Debt Collection Terrorist: How I Beat the Credit Industry At Its Own Game and Made Big Money From the Beat Down, now wants to make it easier to sue for TCPA violations.

Craig Cunningham, the serial TCPA plaintiff who once aspired to author a book titled, Tales Of A Debt Collection Terrorist: How I Beat the Credit Industry At Its Own Game and Made Big Money From the Beat Down, now wants to make it easier to sue for TCPA violations.

Cunningham appeared in a deBanked story about telemarketing last year after it was discovered that he had sued alternative business finance companies for alleged violations. Declining to speak with me at the time, there was plenty to glean from his trail of forum posts where he uses the alias Codename47. One post stands out. “TCPA enforcement for fun and for profit up to 3k per call,” is the title of one thread he started in 2014 on the FatWallet forum.

And if his motives are fun and profit, then a petition filed by Cunningham with the FCC to limit the scope of “prior express consent” might concern you because it would create more opportunities for him and others to initiate lawsuits. This week, the FCC actually asked the public to comment on his petition.

With this Public Notice, we seek comment on a petition for rulemaking and declaratory ruling filed by Craig Moskowitz and Craig Cunningham (Petitioners).1 Petitioners request that the Commission initiate a rulemaking “to overturn the Commission’s improper interpretation that ‘prior express consent’ includes implied consent resulting from a party’s providing a telephone number to the caller.”2 Specifically, Petitioners request that the Commission issue a rule requiring that for all calls made to wireless and residential lines subject to the Telephone Consumer Protection Act (TCPA) restrictions in 47 U.S.C. § 227(b)(1)(A)(iii) and 47 U.S.C. § 227(b)(1)(B),3 “prior express consent” must be express consent specifically to receive autodialed and/or artificial voice/prerecorded telephone calls at a specified number, and such consent must be in writing.4 In addition, Petitioners seek a declaratory ruling to remove uncertainty regarding the meaning of “prior express consent” resulting from previous Commission orders.5

In the original description of Cunningham’s never-written book, his co-author Brian O’Connell, a famous writer, wrote this of Cunningham’s baiting strategy:

“The key was baiting the collections agent on the other end of the line and waiting for the agent to say something incriminating that crossed the line into what the law considered abuse. He began taping calls and soon had his first lawsuit against a security alarm company looking for $450 from an early termination fee.”

He has long since moved on from just debt collectors and files a lot of suits over allegedly unwanted calls.

Comments on Cunningham’s FCC proposal to make suing even easier, can be submitted online or by mail.

What Shakeout? Breakout Capital Secures $25 Million Credit Facility

February 8, 2017 Put a tally up on the board for small business lenders in 2017. McClean, VA-based Breakout Capital, which just announced a move into a larger office last week, has also secured a $25 million credit facility with Drift Capital Partners. Drift is an alternative asset management company.

Put a tally up on the board for small business lenders in 2017. McClean, VA-based Breakout Capital, which just announced a move into a larger office last week, has also secured a $25 million credit facility with Drift Capital Partners. Drift is an alternative asset management company.

Breakout is young by today’s industry standards, founded only two years ago by former investment banker Carl Fairbank, who is the company’s CEO. And don’t count them out just because they’re not in New York or San Francisco. Washington DC’s Virginia suburbs have become somewhat of a hotspot for fintech lenders. OnDeck, Fundation, StreetShares and QuarterSpot all have offices there, Fairbank points out. “And Capital One is right up the street,” he adds while explaining that the community has a strong talent pool that is familiar with creative lending. Breakout has already grown to about 20 employees and they’re still growing, he says.

Fairbank considers Breakout to be a more upmarket lender, whose repertoire includes serving the near-prime, mid-prime customer. CAN Capital and Dealstruck had focused on this area and both companies stopped funding new business in 2016. As I point this out, I ask if that suggests that segment is perhaps too difficult to make work.

“Candidly, that’s the part of the market that I feel the best about,” he says matter of factly. The company tries to product-fit deals based on the borrower, and will even make monthly-payment based loans. “I think the subprime side with the stacking and the debt settlement companies is a very very difficult place to play right now,” he says, adding that they have worked with subprime borrowers using their original bridge program but that they’ve kind of pulled back from doing those. As with all programs regardless, their goal is to graduate merchants into better or less costly products later on. We have helped merchants move on to get SBA loans, he maintains.

That all sounds very hands on, and part of it is, Fairbank confirms while asserting that technology does indeed do a lot of the legwork. “There’s absolutely a human element to underwriting these deals,” he says. He also agrees with much of what RapidAdvance chairman Jeremy Brown wrote in a deBanked op-ed titled, The New Normal. Both Breakout and RapidAdvance refer to themselves as technology-enabled lenders, an acknowledgement that tech is a component of the company, not the entire company itself.

“I think we will see the beginning of the demise of fully automated, no manual touch funding,” Brown wrote in his article.

Brown also predicted that the legal system will ultimately impose order on some industry practices like stacking or that a state like New York could take a public policy interest in products he believes have legal flaws. As he was writing that, Governor Cuomo’s office published a budget proposal that redefined what it means to make a loan in the state. And it leaves much to be desired, some sources contend. Two attorneys at Hudson Cook, LLP, for example, published an analysis that demonstrates how its wording is ambiguous and far-reaching.

“What they really need to do is take the time to think through the implications and basically do a full study of the market to ensure that what they’re pushing forward is going to have the desired consequences,” Breakout’s Fairbank offers on the matter.

This doesn’t mean he’s anti-regulation. The company already holds itself to high standards and customer suitability and is a founding member of the Coalition for Responsible Business Finance.

“I personally do believe that there’s bad forms of lending or cash advances in the market and I’m sure that’s what Cuomo thinks as well but at the same time, it’s getting pushed very quickly and they really really ought to step back and do the research to understand the broader implications and to understand what exactly they’re trying to accomplish,” he maintains.

His pragmatism extends to the OCC’s proposed limited fintech charter, which he finds intriguing, assuming it gets buttoned up. “I believe it’s a concept worth pursuing,” he says, explaining that regulators will need to get comfortable with unsecured lending.

In the meantime, he’s optimistic about Breakout’s prospects. “In a time when institutional appetite for alternative finance companies has dried up, we believe our ability to raise a credit facility in this market speaks volumes about what we have already accomplished, our position as a leading player in the space, and our prospects for strong, but measured, growth,” Fairbank is quoted as saying in a company announcement. The company was also invited and joined the Task Force for the PLUM Initiative, a collaboration between the U.S. Small Business Administration (SBA) and the Milken Institute to more effectively provide capital to minority-owned businesses throughout the United States. The Task Force consists of a very select group of industry leaders, who are in positions to improve access to capital in underserved markets, according to the announcement.

While other companies are making adjustments or in his opinion, continuing to make questionable underwriting decisions, Fairbank thinks his formula for success works. “I think that we do look at deals differently than most folks because I intentionally built the core of my underwriting team with folks who are not from this space so they take a more traditional approach and mix it with some of the greatest aspects of alternative finance.”

SoFi Plays It Safe With Super Bowl Ad – And Kind of Wants to Be Your Bank

February 6, 2017“Here’s to conquering more together in 2017,” SoFi’s Super Bowl ad asserts. The company wants to help you own a home, start a family and see the world. They essentially want to be your bank for life, and now that their acquisition of Zenbanx allows them to offer checking accounts, they pretty much can be. It was no surprise then that their infamous tagline “Don’t Bank” was nowhere to be found in their Super Bowl ad. Watch below:

The ad they ran last year received criticism for labeling people as either great or not great. Maybe it wasn’t the best approach, but it was a very SoFi thing to do at the time.

This year, the only thing missing from their feel-good we-want-to-be-with-you-through-all-your-life-milestones ad is a voice coming on at the end to say “There are some things money can’t buy, for everything else, there’s MasterCard.”

Perhaps SoFi will consider changing their slogan from Don’t Bank to Bank With Us. It’s only a matter of time.