Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

One Of The Most Devastating Court Decisions Against Merchant Cash Advances Has Been Overturned

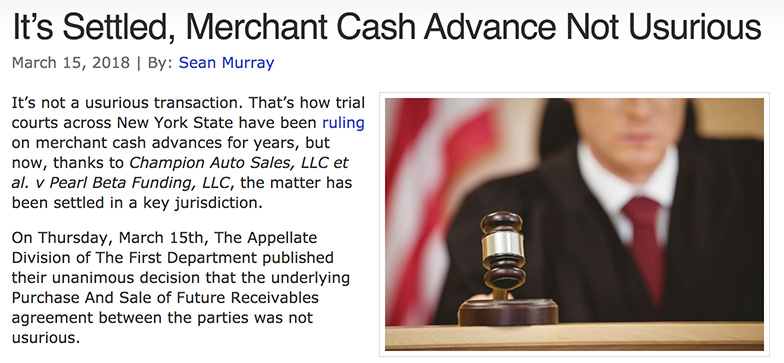

January 29, 2020 Merchant Cash Advances have sat on comfortable legal footing in New York ever since an appellate court ruled in favor of Pearl Beta Funding, LLC against Champion Auto Sales, LLC in 2018, but even so, it hasn’t stopped lawyers from trying to invalidate merchant cash advance (MCA) contracts on behalf of aggrieved customers.

Merchant Cash Advances have sat on comfortable legal footing in New York ever since an appellate court ruled in favor of Pearl Beta Funding, LLC against Champion Auto Sales, LLC in 2018, but even so, it hasn’t stopped lawyers from trying to invalidate merchant cash advance (MCA) contracts on behalf of aggrieved customers.

That’s because an MCA provided by New York-based Merchant Funding Services LLC to a business known as Volunteer Pharmacy in 2016 was ruled by New York Supreme Court Judge David F Everett to be so “criminally usurious on its face” that the normal process required to vacate a Confession of Judgment could simply be bypassed without even having to evaluate the merits of each side’s arguments and the matter automatically won in favor of Volunteer Pharmacy. The judge’s written decision, which voided the MCA contract ab initio, was replete with a scathing opinion of MFS’s business model.

The decision quietly stunned the merchant cash advance industry. MFS understandably appealed.

Dozens of lawsuits against MCA companies in the ensuing years went on to cite Judge Everett’s decision in Volunteer Pharmacy with limited success. And while the industry sat around to find out what would happen in that case, Pearl Beta Funding, a rival to Merchant Funding Services, won an appeal of its own, the landmark usury case in March 2018 that seemingly solidified once and for all the commonly held understanding that such MCA agreements were not usurious.

Despite this, the uncertainty of Volunteer Pharmacy still lingered in the background, that is until now.

On January 29th, 2020 the Appellate Division, 2nd Department, of the Supreme Court of New York, overturned Judge Everett’s decision and ruled in favor of Merchant Funding Services. The panel of judges said they need not even weigh a lot of Everett’s contentions because he was wrong on the underlying procedural issue, that a judgment by confession could be vacated in such an instance without having to go through the normal legal process.

The ruling ultimately provides clarity on the process that determines how a judgment by confession can be vacated. One major impact is that lawyers seeking to invalidate merchant cash advance agreements will no longer have Volunteer Pharmacy as a crutch to rely on.

Quarterspot is Shifting Its Business Focus

January 22, 2020Last week, several industry insiders reported receiving an email from NY-based company Quarterspot that said their agreement had been terminated.

The contents stated that the company is “shifting its business focus and will no longer be originating loans, but will continue to service currently outstanding loans.”

deBanked has confirmed that to be true. More information may be reported as it becomes available.

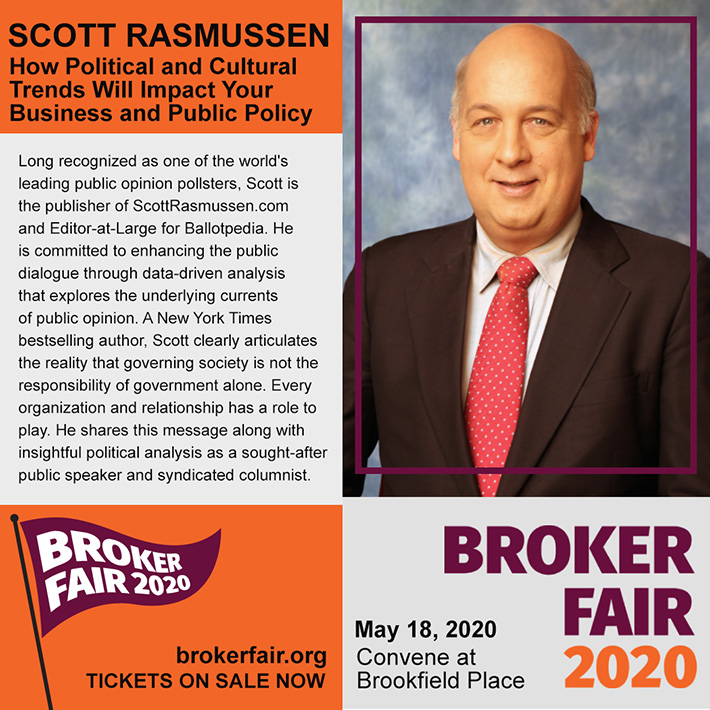

Broker Fair 2020 Announces Two Special Keynote Speakers

January 17, 2020Two special guests will speak at Broker Fair 2020 on May 18th in New York City. Scott Rasmussen and John Henry will complement a roster of leading professionals from the commercial finance industry. Broker Fair 2020 will be deBanked’s largest ever event.

TICKETS ARE ON SALE NOW AND EARLY BIRD PRICING IS STILL AVAILABLE!

deBanked CONNECT MIAMI Kicks Off Today

January 16, 2020

deBanked’s annual South Florida event, deBanked CONNECT MIAMI, begins today at 1:30pm at The Loews Hotel in Miami Beach. Check-in will take place at the Rotunda on the 2nd level.

This event is SOLD OUT. More than 500 people are registered to attend this year.

Got an event question? Email: events@debanked.com

Got a general deBanked question? Email: info@debanked.com

Having trouble with the deBanked Events mobile app?

Make sure you have updated to the latest version on Android. Try to uninstall and reinstall on iOS. Still having trouble? email events@debanked.com

Missed out on today? Or want to get a head start on deBanked’s next event? Broker Fair 2020 in New York City is right around the corner! Register now at: https://brokerfair.org

Dodd-Frank’s Small Business Lending Data Collection Rule Could Still Take Years to Implement

January 12, 2020 Small business lenders: Are you ready to regularly submit loan application data to the Consumer Financial Protection Bureau? No? Good, because almost ten years after Dodd-Frank passed, the provision that requires the CFPB to collect small business lending data still hasn’t been implemented.

Small business lenders: Are you ready to regularly submit loan application data to the Consumer Financial Protection Bureau? No? Good, because almost ten years after Dodd-Frank passed, the provision that requires the CFPB to collect small business lending data still hasn’t been implemented.

And apparently we’re still years away.

Section 1071, as it’s known, modified the Equal Credit Opportunity Act and defined a small business lender as any company that engages in any financial activity. So if you’re wondering if this thing even applies to whatever you do in your corner of small business finance, it probably does.

The rule has taken so long to implement that consumer advocacy groups have actually sued the CFPB over the delay. The CFPB took note followed by initiative and hosted a symposium late last year to discuss how it might go forward. The next steps from here are to convene a panel of small business lenders, have that panel issue a report, propose what the rules on collection will be, collect feedback on the proposal, formulate a final rule, issue a rule, and then set a time for when it will go into effect. That process could mean that the earliest that data collection takes place is in 2023, possibly even longer as the entire financial services industry may need time to develop the infrastructure and human resources to comply.

Beyond that, advocates and critics of Section 1071 do not even entirely agree on what purpose data collection will even serve. Some believe the intent is merely for the government to have access to data it otherwise might not have while others believe that the CFPB could use statistics it deems discriminatory to bring enforcement actions against financial institutions. Sounds like we could use a few more years to get on the same page…

A recording of the 2019 Symposium is below:

Jonathan Braun Has Checked In To Prison

January 2, 2020 Jon Braun, who Bloomberg Businessweek profiled in a 2018 story series, checked into FCI Otisville on Thursday. He was sentenced to 10 years in prison on May 28th for drug related offenses he committed a decade ago. He was originally scheduled to surrender on August 25th but he successfully delayed the date until today, January 2nd.

Jon Braun, who Bloomberg Businessweek profiled in a 2018 story series, checked into FCI Otisville on Thursday. He was sentenced to 10 years in prison on May 28th for drug related offenses he committed a decade ago. He was originally scheduled to surrender on August 25th but he successfully delayed the date until today, January 2nd.

I have not attempted to contact Mr. Braun since the day of his sentencing. But purely by chance I shared an elevator with him in the Brooklyn Federal Courthouse on May 28th just mere minutes after he had been handed ten years. Given the opportunity, I asked him how he felt about what just happened.

“I hope it goes by quick,” he replied stoically.

The End Of An Era – deBanked Through The Decade

December 30, 2019

deBanked estimated that approximately $524 million worth of merchant cash advances had been funded in 2010.

In 2019, merchant cash advances and daily payment small business loan products exceed more than $20 billion a year in originations.

First Funds

Merchant Cash and Capital

Business Financial Services

AmeriMerchant

Greystone Business Resources

Strategic Funding Source

Fast Capital

Sterling Funding

iFunds

Kabbage

OnDeck

Square Capital

Amazon Lending

Funding Circle USA

Yellowstone Capital

Entrust Cash Advance

Merchants Capital Access

Merchant Resources International

American Finance Solutions

Nations Advance

Bankcard Funding

Rapid Capital Funding

Paramount Merchant Funding

How GRID Finance’s Cash Advances Are Building Stronger Irish Communities

December 27, 2019

Five years ago, a small company in Dublin put Ireland’s fintech scene on the map by advising local SMEs to “get on the GRID.” GRID Finance, founded by Derek F Butler, introduced a peer-to-peer lending model to Irish businesses at a time when the industry was just beginning to form. From the beginning, the company’s secret sauce was the GRID Score, a proprietary credit score system that enabled the company to take on the difficult task of assessing the risk of SMEs.

Butler, who I sat down with in September at the company’s headquarters alongside Chief Marketing Officer Andrea Linehan, says the GRID Score is an SME’s “passport to the economy.”

It’s the upper tier that GRID caters to while providing a unique product within Ireland known as a cash advance. The setup is similar to Square and PayPal in the US in that the loans are repaid via a percentage of an SME’s credit/debit card transactions on a daily basis. The term of the loan is fixed and the costs are reasonable.

“The reality is that small business funding and financing is a high risk,” Linehan says.

“There’s no subprime market here,” Butler adds. “We’re trying to build a prime cash advance market versus a subprime one in the US.”

Like GRID’s competitors in the industry, Linehan believes that finance in Ireland will transition online. “Ireland is still dominated by two banks,” she says, referring to Bank of Ireland and AIB. The company, therefore, believes it has a good head start on the impending shift. But in the meantime, they’ve learned how important it is to be embedded in the local communities. To that end, GRID has an office in Limerick, Ireland’s third largest city with 95,000 people that’s located about 200km away from its headquarters in Silicon Docks.

Like GRID’s competitors in the industry, Linehan believes that finance in Ireland will transition online. “Ireland is still dominated by two banks,” she says, referring to Bank of Ireland and AIB. The company, therefore, believes it has a good head start on the impending shift. But in the meantime, they’ve learned how important it is to be embedded in the local communities. To that end, GRID has an office in Limerick, Ireland’s third largest city with 95,000 people that’s located about 200km away from its headquarters in Silicon Docks.

And their mission goes beyond providing funds. “If we can help get [SMEs] ready by giving them the tips to improve their financial health right now, let’s try and do that,” Butler says. “We want them to understand their financial health versus their cost of capital.”

While the company has sustained modest growth, Business Post reported earlier this month that GRID plans to raise €100 million in 2020 to provide even more loans through its platform.

Butler likens GRID’s mission to the MetLife Foundation, promoting financial health and building stronger communities. “We do a lot of work with the MetLife foundation because of the impact they have,” he says. “It’s why I launched GRID Finance.”