Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Don’t Steal Deals Bro

June 4, 2015 It’s a scenario that’s become all too common in the merchant cash advance industry. An employee quits or gets fired and within weeks they begin soliciting all the previous clients they worked on for revenge… or money… or both.

It’s a scenario that’s become all too common in the merchant cash advance industry. An employee quits or gets fired and within weeks they begin soliciting all the previous clients they worked on for revenge… or money… or both.

Maybe they signed an agreement that was supposed to prevent this or maybe they didn’t. In my own personal perspective, it shouldn’t matter.

Don’t steal deals bro

If you’re as good a closer as you think you are, your new ISO shouldn’t rely on stealing deals from the last company you worked at. On the one hand you will be taking time away from what’s important, and that’s creating a long term business model. Stealing deals might generate some nice checks but it’s not a business. A ton of new ISOs fail and that’s because they have no idea how to generate new deals. I guess you’re not a closer bro…

On the other hand, stealing deals will permanently burn an industry bridge at best and get you sued at worst. The one thing harder than starting a new business is starting a new business while there is someone out there actively trying to make you fail.

Don’t sue me bro

If you signed an agreement with a non-solicit clause, you probably shouldn’t solicit. Several companies in the industry have used the court system to try and enforce non-solicits or non-competes (no matter how weakly worded) against former employees. Some of these lawsuits have dragged on for years and likely cost the alleged contract breachers hundreds of thousands of dollars just to defend themselves.

There’s a way around this and that’s to negotiate with an employer to amend the agreement prior to your employment there. If they won’t bend on certain clauses like non-competes, then chances are if you go ahead and sign anyway, they are going to try and enforce it even if they end up not succeeding.

“ISOs must always think about the possible consequences under their agreements for moving merchants,” wrote Adam Atlas in a recent Green Sheet article that applies almost equally to the merchant cash advance industry.

Atlas goes on to explain however, that enforcing a non-solicitation could backfire, in the sense that if the ISO feels its trivial or unwarranted, they could escalate their efforts to move deals away. They’ll probably also feel inclined to spread the word and spook the company’s other ISOs. That could really come back to bite.

Be sure to read ISO Legal Blunders by Adam Atlas on the Green Sheet.

Thinking about stealing deals? Consider the legal stuff bro.

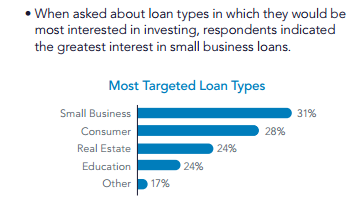

Small Business Lending is King to Institutional Investors

June 2, 2015

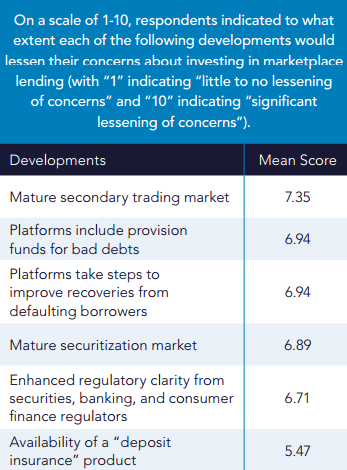

Richards Kibbe & Orbe LLP and Wharton FinTech polled more than 300 institutional investors to gauge their thoughts on marketplace lending. They published their findings in a recently released report.

The surveyors seemed surprised that institutional investors indicated their interest in small business loans was greater than that of consumer, real estate, education, and everything else.

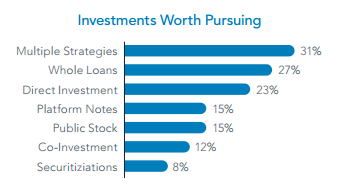

Securitizations ranked lowest on the list of investments worth pursuing and buying whole loans was second only to “multiple strategies.”

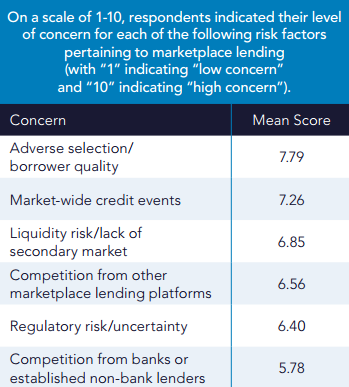

Regulatory risk and uncertainty was low on the list of concerns while borrower quality was the most concerning factor. Curiously, competition was the least concerning of all.

Speaking to the liquidity issues of the assets, institutional investors indicated that the development of a mature secondary trading market was more likely than anything else to lessen their concerns about marketplace lending.

Do any of these results surprise you?

Download the Key Findings report

Why We Shouldn’t Stop Calling it Peer-to-Peer Lending

June 1, 2015 There’s a troubling undercurrent brewing in the marketplace industry, the death of the word peers. We’re not supposed to say peer-to-peer lending anymore since few platforms actually allow for people to lend directly to their peers. In the case of Lending Club and Prosper, investors are actually lending money to the platforms themselves.

There’s a troubling undercurrent brewing in the marketplace industry, the death of the word peers. We’re not supposed to say peer-to-peer lending anymore since few platforms actually allow for people to lend directly to their peers. In the case of Lending Club and Prosper, investors are actually lending money to the platforms themselves.

Emphasizing the appropriate terminology probably makes it easier for people to understand. If it’s not peer-to-peer after all, then calling it that only serves to mislead potential borrowers and investors alike. And yet the term persists largely because the average person is still able to invest in an asset class it never was able to before, notes backed by the performance of individual consumer loans.

It could be argued that without money from peers to buy these notes, the loans themselves would never get issued, making it still peer-dependent or at least peer-relevant.

A game for Wall Street

Jorge Newberry wrote several months ago that the little guy as most of us imagine a peer to be, is dead. He was replaced by Wall Street, BlackRock, and Wealthy bankers. “These were killers,” He wrote. He added that while the industry “initially attracted ordinary citizens to invest in modestly sized consumer loans to people like them, over the last few years those peer investors often have been elbowed out and replaced by Wall Street’s finest.”

Retail investors have bemoaned the trend via online message boards, sometimes even accusing the platforms of giving the institutions first dibs on the highest quality loans and leaving the little guys to fight over nothing but the scraps that are more likely to underperform.

Even Dara Albright, the co-founder of the LendIt conference has acknowledged the takeover. In The Financial Advisor’s Guide to P2P Investing, Albright writes, “Unfortunately, what began as a true person-to-person marketplace – with the ordinary individuals lending to and borrowing from one another – has since become monopolized by institutional investors whose deep pockets and technological advantages have all but driven the individual lenders out.”

Further along in the paper, Albright makes the case that individuals need to take advantage of the yield these loans offer to narrow the wealth divide. She makes a compelling argument for investing but stops short of proposing a solution to regain market share. “There aren’t enough p2p loans to facilitate the strong investment appetite,” she concluded.

But just as the marketplace community has conceded the death of peers, the numbers don’t exactly reflect their sentiment.

Only 28% of Lending Club’s loans went to institutional investors in 2014.

Only 28% of Lending Club’s loans went to institutional investors in 2014.While Newberry and Albright have made the case that retail investors are being locked out, there’s a dangerous flip side, they just might be getting locked in. If marketplace lending truly is becoming a game for Wall Street by Wall Street, then the few retail investors who are invested in it could eventually become collateral damage in a pissing match between wealthy bankers.

Investor faith

There are already concerns that the incentive for marketplaces are not aligned with those of their investors. PeerCube co-founder Anil Gupta wrote this on the LendAcademy forum about Prosper, “The quest to increase originations and revenue will trump any such risk management attempts, like what happened with banks issuing mortgages to unqualified borrowers in order to boost their own bottom lines.” He wrote that in response to an upset user whose borrower declared bankruptcy before making even a single payment towards their Prosper loan.

The user was questioning how Prosper would handle this since the timing of the loan prior to the bankruptcy filing had all the hallmarks of fraud.

Gupta added, “There is very little incentive for LC and Prosper to pursue such collections and recoveries claims. When LC was investing its own money in loans, they pursued collections and recoveries more vigorously (11.19% collection in 2007 vs 5.53% collection in 2011). It is no longer Prosper and LC money at risk.”

The user is not alone in his collections fears. Just a few days earlier I realized that 4.6% of all the notes I had purchased on Lending Club had already defaulted, a number that troubled me considering my average note is only 10 months old. With another 3-4 years still to go until maturity, the rate of defaults is already quite high.

The user is not alone in his collections fears. Just a few days earlier I realized that 4.6% of all the notes I had purchased on Lending Club had already defaulted, a number that troubled me considering my average note is only 10 months old. With another 3-4 years still to go until maturity, the rate of defaults is already quite high.

And while I’ve been told that my own personal stats are relatively normal, other retail investors occasionally run into quirks that force them to question the soundness of the reporting they receive.

For example, veteran users commonly rely on the FICO score updates Lending Club will publish for each issued loan. If a borrower’s score is dropping, you could sell the note for a discount to an interested buyer on a marketplace such as folio. Several people have admitted to using this strategy to mitigate losses. There’s just one problem, a user discovered a discrepancy in Lending Club’s FICO reporting. In at least one case, the borrower’s FICO score may have been overstated by more than a hundred points. For users beholden to the accuracy of these figures in order to properly execute their investment strategy, it’s a difficult pill to swallow.

Call it a kink or an oddity. Maybe it’s something that needs to be fixed or maybe something is being miscommunicated. Whatever is going on there, these are the kinds of risks that institutional capital is supposed to be able to tolerate in their quest for yield, but it’s gut wrenching for retail investors.

In the instance of the suspected bankruptcy fraud, several responses by fellow investors gave the impression that the platform simply isn’t going to care because they make money off of issuing loans, not collecting on them. That’s the exact type of Wall Street attitude that could come back to hurt retail investors.

Marketplace lending might not technically be designed as peer-to-peer but the little guy and their actual peers certainly have their funds at stake. Calling it a game for big banks, the wealthy, and Wall Street only encourages the players involved to take bigger risks, reduce transparency, and shrug off genuine criticism.

We can’t let that happen.

Mapping the Business Financing Industry (Sneak Peek)

May 27, 2015People often ask what the real presence of the merchant cash advance & business lending industry is like in New York City. Below is a map of Midtown Manhattan.

We apologize if we didn’t plot your company on here. Let us know you exist by signing up for our magazine.

In the May/June issue that’s being sent off to the printers at this very moment, we explore the industry scene in lower Manhattan. Midtown may have been a birthing place and permanent home for industry titans, but Wall Street, long believed to be a haven for stock brokers has been overrun by a new kind of broker.

You’ll just have to stay tuned to read more. If you’re not signed up to get our free print magazine, register now.

Also in the May/June issue:

- An examination of a new trend, consolidating loans and advances.

- Watching everyone else get rich off alternative lending? Whether you’re in underwriting, administration, operations, or sales and whether you have a lot of money to invest or just a little, there are opportunities available to “get in”. You might be in this industry but are you in this industry? We’ll run through the basics of what’s available out there. Become a player or just educate yourself.

- And more!

The Co-brokering Phenomenon: In Business Loans & Merchant Cash Advance

May 25, 2015 Meet the broker’s broker, the middleman serving the middleman. Some call this co-brokering since both parties will typically share in the commission.

Meet the broker’s broker, the middleman serving the middleman. Some call this co-brokering since both parties will typically share in the commission.

Wait, what?

The broker’s broker might have relationships that the little broker does not. They could have leverage over their funding partners because of the amount of volume they can produce or the amount of professionalism they bring to the table. And they likely have a canny ability to close deals that otherwise would get tossed by the wayside.

Disintermediation is the war cry of today’s famous tech-based lenders but in the Year of the Broker, reintermediation has been the unforeseen byproduct. Big lenders such as OnDeck are shedding third party funding advisors but those advisors aren’t magically going away.

A number of them are still getting their deals funded at OnDeck, just indirectly. They have to go through a broker whom OnDeck has not cut off, a handful of salespeople have told me. Many brokers acknowledge that OnDeck’s rates and terms are not easily attainable elsewhere so they’d rather share a commission with an OnDeck approved broker than risk a dead deal with no commission.

And CAN Capital is known to offer comparable pricing to OnDeck but it’s been reported that new brokers must go through a rigorous audit before CAN will accept their business. It’s not something everybody wants to go through.

With the two largest funders in the industry imposing real barriers to doing business with them, sanctioned brokers play toll booth operator for the swarm of shops that can’t get their deals submitted without them.

Perhaps as a direct result of that, there is now an entire niche of brokers whose only business is brokering deals for other brokers. They have little to no interaction with merchants. They have no marketing budget. They might not even have a website. And they play an almost mystical role of gatekeeper and power broker.

Onesy-twosy woes

A strong focus within the industry has been growth. There’s a lot of time, resources, and salesmanship that goes into courting the lucrative partnerships. Large funders, especially those with VC backing, are typically not interested in mom and pop broker shops. “If they’re only going to send one or two deals per month, we don’t want them,” I’ve heard time and time again.

Even five to ten deals a month can draw yawns. It’s nothing particularly against the mom and pop brokers, but experience has apparently shown them that the same amount of resources are spent on the onesy-twosy brokers as the ones doing a hundred deals a month. The cost benefit analysis has to make sense, they say.

That’s left hundreds or perhaps even thousands of mom and pop brokers to fend for themselves. What outsiders might not seem to realize is that the commission on a $50,000 loan or advance can be $5,000. That’s potentially enough for a stay-at-home parent to pay for the rent, groceries, and all the other bills. A onesy-twosy broker might be completely insignificant to a funder doing a billion dollars worth of deals a year, but to a mom and pop broker, it only takes one deal to pay their bills and only a handful to make them rich, especially if they live in middle America where the cost of living is cheaper.

In From Lowes to Loans, superstar broker William Ramos said he made $66,000 on just one deal alone. While his shop produces more than a million dollars in deal flow a month, it’s easy to see what’s drawing the hoards of newbies in. A $66,000 commission might be the only commission someone needs for an entire year.

There is no licensing required so becoming a broker is as easy as imagining that you are one. And as the space invites the less knowledgeable, a more sinister element has found opportunity as well.

Shady

“There is no president/ruler of the MCA world that can help you with your commission debacles,” wrote PSC’s Amanda Kingsley on an industry forum. That was part of her reply to a thread titled, co-brokering scumbags. The thread might be new, but the circumstances aren’t. A broker sent their deal to another broker who got the deal closed with a funder. The original broker supposedly got screwed out of the commission.

“There is no president/ruler of the MCA world that can help you with your commission debacles,” wrote PSC’s Amanda Kingsley on an industry forum. That was part of her reply to a thread titled, co-brokering scumbags. The thread might be new, but the circumstances aren’t. A broker sent their deal to another broker who got the deal closed with a funder. The original broker supposedly got screwed out of the commission.

It’s a case of stolen deals. “You just have to find the right people to work with. There are a lot of shady characters in this industry,” wrote another user.

1st Capital Loans Managing Member John Tucker, who recently authored, Broker Business Planning, wrote in reply to the thread, “Get everything in writing and research your lender/partner heavily before contracting with them. Talk to other brokers and ask them about their experience with said lender/partner in terms of paying on new deals, renewals and residuals. Get a ‘feel’ for them.”

Several faulted the aggrieved party for not taking the time to hammer out a contract that would allow them to rectify the situation easily through a lawsuit. But even with a contract, pursuing the offender legally could cost more than the commission lost. A stolen deal might cost a broker a few hundred or a few thousand dollars, figures worthy of small claims court.

“Under no circumstances would I ever co-broker a deal,” wrote Tucker. “There’s just no reason to unless you are a newbie and getting trained by said broker.”

But another user wrote, “Sometimes you don’t even know you are co-brokering until after the fact.”

Unscrupulous brokers will be purposely deceitful but for others walking the thin line between broker and funder, it’s difficult to judge what constitutes direct. There are brokers that wholeheartedly believe that if any portion of their own funds are invested in a deal, then they too are a direct funder. That means a broker that syndicates with a variety of funders could be so inclined to identify themselves as a direct funder by extension.

Kingsley wrote, “You have to understand what a ‘broker’ is in this space and understand that it is A LOT different than brokering in another industry.”

She also pointed out that it’s not always the little guy that’s susceptible to becoming a victim, as could be the case if an early deal default leads to a commission chargeback. When that happens, the funder will take back the full commission on the deal from the broker of record. It’s the responsibility of that broker to claw back whatever split of the commission they shared with the sub-broker.

“The broker you sub-brokered for, can vanish,” Kingsley wrote.

Ban the bad guys?

Several industry veterans have suggested creating an ISO/funder blacklist for those that steal commissions or deals. The challenge is that a stolen deal is not always a black and white situation. Often times there are expiration dates built into contracts that allow funders to claim deals if they have not been closed by the submitting broker within a specified period of time. Other times it’s a case of miscommunication, or the victim conveniently left out key details that would certainly add a degree of color to the situation.

Calling out an offender online can quickly devolve into a he said/she said schoolyard brawl. Unfortunately, this might be the only remedy a victim has, especially if they have limited financial resources to pursue legally, or the only evidence of their deal is a handshake or an email.

The bad guys, if they’re engaged in trickery on a large scale, tend to get identified rather quickly. There’s always a few that come in, burn a lot of bridges, and then find themselves completely ostracized from the industry. When the damage is done, they might never be heard from again or they might try to repeat the process by using a different name. Blacklisting a broker or funder wouldn’t be foolproof, especially if the company owner legally changes their name, which has actually happened before.

Trust

Through it all, Tucker offered this advice, “In a nutshell, the only true thing protecting your compensation is a very good relationship with an honest, credible and ethical lender.”

And if you have to go through a broker, make sure you choose the right one. Don’t blindly send your deal to somebody you met on a message board. An unscrupulous player will tell you exactly what you want to hear. Ask around for references. If nobody’s ever heard of them, chances are you’re talking to the wrong shop.

Even the author of that thread conceded that co-brokering offers benefits. “I’m all for co-brokering deals, especially if someone has a solution that may suit the client better than a traditional MCA or when an MCA wont work,” he wrote.

So there just may be a place for the broker’s broker, whether as a gatekeeper, power broker, or toll booth operator. And like it or not, reintermediation has ironically become a byproduct of disintermediation. There are sadly no algorithms that exist to vet how a broker might treat another broker. Co-brokering is a trade that relies on the most basic of basics, trust.

Nothing’s more valuable.

OnDeck Gets Taste of its Own Medicine

May 24, 2015 You know those subtle and not so subtle knocks OnDeck has made about merchant cash advances over the years regarding costs and transparency? Well, the tables have turned.

You know those subtle and not so subtle knocks OnDeck has made about merchant cash advances over the years regarding costs and transparency? Well, the tables have turned.

A supposed unnamed merchant shared their capital raising adventure stories with Fundastic and apparently confused the OnDeck cost factor of 1.24 with an APR of 24%. “The interest rate was 24%, which we thought was excessive, as well as the daily $984 payments we got as part of the deal, but in the end we moved forward with the line,” the business owner reported. A Fundastic editor’s note explained the merchant’s APR was actually around 52% because of the closing fees.

The business owner continued to gripe about not receiving an amortization schedule, as well as the fact that they couldn’t pay off the loan early without incurring a penalty.

Apparently the simplified dollar for dollar cost that OnDeck outlined wasn’t forthcoming enough for them, and they were much more satisfied when they switched to Lending Club.

The merchant then went on to explain that their Lending Club business loan rate was only 9.9%, down from OnDeck’s 24%.

Transparency and full understanding at last?

Ironically, Fundastic had to add yet another note to show that the APR was actually 12.96%. 9.9% was not an APR. “LendingClub had a transparent loan — reasonable interest rate (we have 9.9% + 3% origination for a 2-year loan),” the business owner wrote, yet it seems he was unaware of the APR here either.

Fundastic ultimately concluded, “If you qualify for both LendingClub and OnDeck business loans, I can’t see any reason why you would go with OnDeck. LendingClub’s loans are cheaper in cost [and] more transparent.”

Lending Club might’ve been cheaper in this scenario but the merchant appears to have gotten similar information from both lenders. I’m not sure how much more transparent a lender can be when they spell out exactly how much you have to pay back, though an APR would be useful for certain comparative purposes.

Them’s fightin’ words

The jab at OnDeck though is reminiscent of the way OnDeck historically attacked merchant cash advances. In a 2008 press release, they wrote, “On Deck Capital fills the void between bank loans and alternative business financing products such as merchant cash advances which, similar to payday loans, charge excessive percentage rates for short term capital.”

The jab at OnDeck though is reminiscent of the way OnDeck historically attacked merchant cash advances. In a 2008 press release, they wrote, “On Deck Capital fills the void between bank loans and alternative business financing products such as merchant cash advances which, similar to payday loans, charge excessive percentage rates for short term capital.”

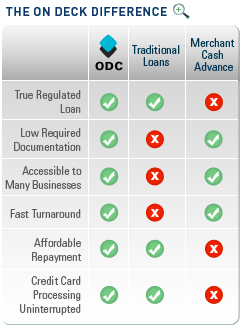

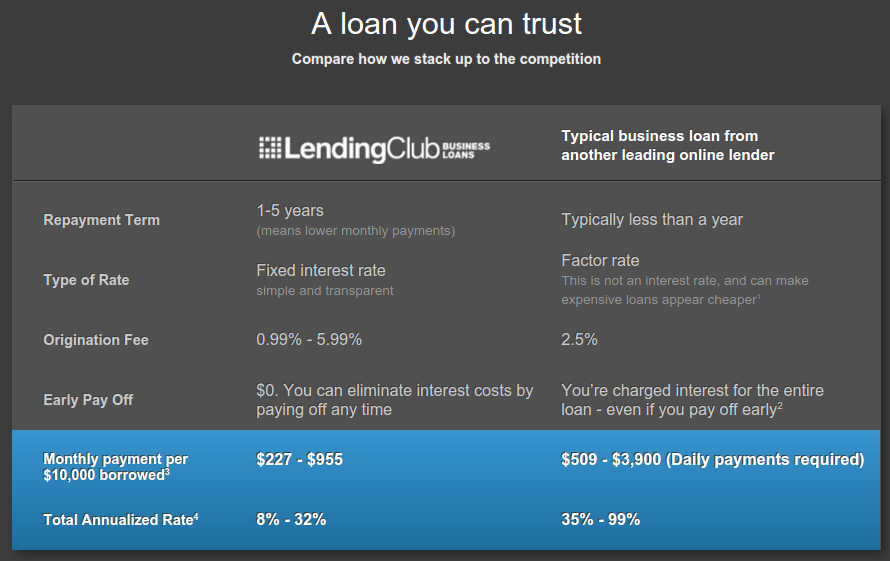

They even used to display this little chart to explain just how much merchant cash advance sucked compared to them.

Affordable repayment? NOPE!

Meanwhile, OnDeck is still not profitable after 8 years. That either just goes to show how hard it will be for them to compete with Lending Club’s pricing or it indicates that Lending Club is severely underpricing its business loans. It might be the latter.

Lending Club’s business loan program is still highly experimental and dozens of business lenders have entered the space with the belief that undercutting higher priced products right out of the gate will magically yield positive results.

Does this look familiar? OnDeck is being attacked by Lending Club with its own playbook:

And in case you weren’t sure if they were comparing themselves to OnDeck specifically, the 2.5% origination fee is the number that appears right on OnDeck’s website. “We charge an origination fee of 2.5% of the loan amount for your first loan,” it states.

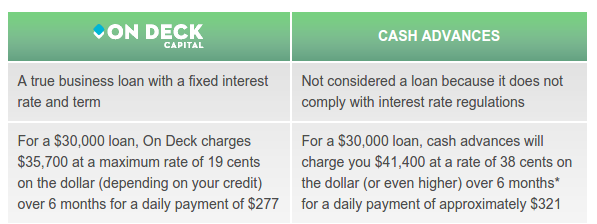

And here’s a snippet of a chart that used to appear on OnDeck’s website:

OnDeck has repeatedly stated that competitive pressure has not been the reason that their interest rates are dropping. It may actually be in anticipation of a brewing public relations war. Lending Club’s supporters are beginning to attack OnDeck in the same way that OnDeck attacked merchant cash advance companies.

Most merchant cash advance companies held firm on their terms over the years and it has paid off. Costs have come down where warranted, but few have been interested to actually underprice their product and risk bankruptcy just to appease criticism.

The circumstances are slightly different for OnDeck who has more to lose as a public company. If their model is dependent entirely on growth and Lending Club begins to snatch some of the lucrative partnerships away from them, their shareholders might suffer in a big way. They can’t have that, so they’re dropping their rates.

Perhaps they should take a page from the merchant cash advance playbook and hold firm, or given their current financials, even raise their rates. Let Lending Club do their thing. Whether the rate is 9.9% or 12.96% is great for a small business, but it’s unlikely to be sustainable or profitable for the lender.

How safe is small business lending really?

Did you know that 29.4% of all Cold Stone Creamerys that received an SBA 7(a) loan defaulted? 29.4% of all Quiznos have defaulted. 26.4% of all Aamco Transmissions have defaulted.

Scarier yet, the SBA’s special ARC loans that were put together in the wake of the recession had an anticipated 60% default rate across the board.

These figures should serve as a warning to any startup business lender, especially if they’re taking jabs at their higher priced competitors.

It’s a great time to get a loan as a merchant, but a politically tough environment for a lender to price that loan profitably. One day you’re the hot new low cost alternative serving up a public relations beating to the standard bearers of alternative finance, the next day someone’s using the exact same strategy on you.

Can OnDeck take the heat?

Write for deBanked

May 20, 2015

Missed your calling? deBanked is looking to hire a journalist to keep up with the industry’s explosive growth.

This is a paid work-from-home opportunity. Freelancers are welcome, but we’re open to an exclusive arrangement as well. You cannot be employed or contracted with a funder/lender or similar business however. You must have excellent writing skills, communication skills, and at least a fundamental understanding of the industry.

The role involves phone and email interviews with industry executives and writing for our blog, magazine, and newsletters. There may occasionally be face-to-face interviews.

Contact sean@debanked.com if interested.

—-

Established in 2010, deBanked covers the alternative finance ecosystem, with topics ranging from peer-to-peer lending to bitcoin to merchant cash advance financing.

PSC and Hudson Cook, LLP Align to Promote Best Practices in Merchant Cash Advance Industry

May 18, 2015 Earlier today, New York-based PSC announced an alliance with nationally renowned law firm Hudson Cook, LLP to educate members of the merchant cash advance industry. PSC provides full backend systems and support staff for more than a dozen merchant cash advance companies.

Earlier today, New York-based PSC announced an alliance with nationally renowned law firm Hudson Cook, LLP to educate members of the merchant cash advance industry. PSC provides full backend systems and support staff for more than a dozen merchant cash advance companies.

The move is significant because it focuses on the adoption of best practices. The only other similar initiative has come from from the Small Business Finance Association (SBFA), but no organization has ever actually made guidelines public, at least not since the Electronic Transactions Association published a white paper in March 2008.

Both Hudson Cook and the SBFA are said to be separately working on their own public best practice frameworks in collaboration with industry participants.

Three attorneys for Hudson Cook recently took on the industry’s most polarizing topic, stacking, when they authored, Stacking: Is it Tortious Interference?. “The analysis of what is ‘improper’ interference versus vigorous, but acceptable, competition will be based on the specific facts of each case,” they wrote.

The law firm may draw from another well established best practice playbook, like the one that exists for the Online Lenders Alliance in the consumer lending space.

PSC recently hired Amanda Kingsley, the woman behind the headline, “Year of the Broker” in our last issue. Kingsley spoke often of best practices in her interview with deBanked Magazine.

PSC recently hired Amanda Kingsley, the woman behind the headline, “Year of the Broker” in our last issue. Kingsley spoke often of best practices in her interview with deBanked Magazine.

A month ago at the LendIt conference, Karen Mills, the former head of the Small Business Administration, said she asked several regulatory bodies who would stand up to oversee small business lending. “No one stood up,” she said.

For now, that seems to mean that the industry is on its own. “PSC also intends to maintain its commitment to its members by providing standards to help them better adhere to all new legal requirements and regulatory practices,” the release said.

It’s a step in the right direction.