Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

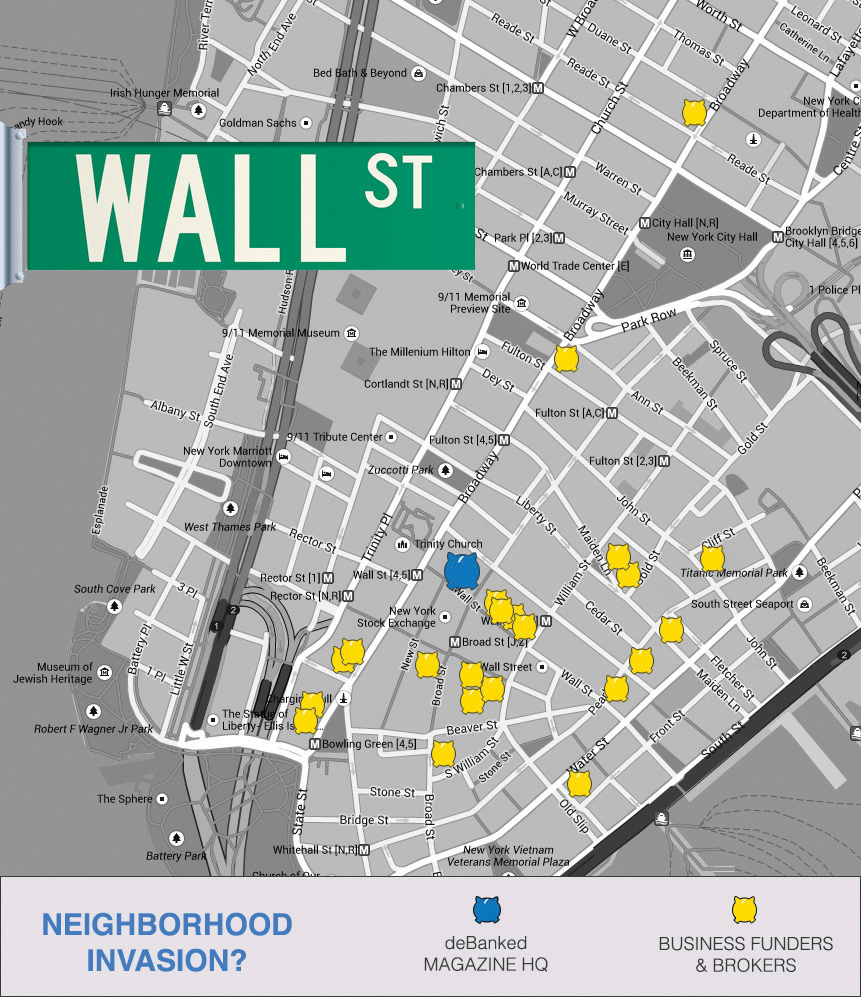

Wall Street Has a New Landlord

June 20, 2015 “You stole my deal bro!”

“You stole my deal bro!”

“No I didn’t. The merchant hated your offer,” replies back a 25-year old dressed in a dark pinstripe suit with no tie.

He then takes a pull from his half-smoked cigarette and continues, “The guy wanted 90k and you offered him twenty. I was at least able to get him fifty. What’d you think was going to happen?”

I walk past the two who eye me suspiciously and am quickly out of hearing range of their conversation. They were strangers, but I know exactly what they were talking about. Walking around the neighborhood here, I feel oddly at home.

This is Wall Street, a new stronghold for the small business financing industry. Midtown has traditionally been the epicenter for merchant cash advance companies, but somewhere along the way, new players started opening up their shops in lower Manhattan.

As a born and bred New Yorker, I never really saw a need to visit the actual street of Wall Street. To my knowledge, it was simply emblematic of high finance, not really a physical place anymore.

But earlier this year when I signed a lease at 14 Wall Street, I would be thrust into the middle of America’s biggest breeding ground for financial brokers and learn once and for all that the ebb and flow of Wall Street isn’t exactly gone, just transformed.

From my office up on the 20th floor, I can see into the windows of the top five stories of the New York Stock Exchange building. The floors appear to be set up for traders, with long white continuous desks peppered with large monitors on both sides. Everyone sits and stares intensely at their screens, pressing buttons on their keyboard at rapid fire pace. Nobody runs around screaming orders anymore.

Outside, tour guides tell excited onlookers about the stock exchange’s past. It’s a historical landmark, a place to learn about history, not necessarily witness it. The spirit is still alive though in a zombified made-for-the-cameras kind of way. OnDeck recently kicked off their IPO there and so too did Lending Club.

Outside, tour guides tell excited onlookers about the stock exchange’s past. It’s a historical landmark, a place to learn about history, not necessarily witness it. The spirit is still alive though in a zombified made-for-the-cameras kind of way. OnDeck recently kicked off their IPO there and so too did Lending Club.

While tourists dance around aimlessly and upload photos to facebook to show they were there, men and women in the office floors above them are engaged in a different kind of dance. Packed in elbow to elbow with phones glued to their ears, commercial financing brokers shout large numbers at an accelerated pace.

Often lacking luxury amenities such as windows, brokers on Wall Street are weathering the heat and lack of oxygen to move money to Main Streets all across America.

When they come out for air to breathe, the tourists move out of their way, as if they’ve suddenly become aware that people are actually trying to get some work done down here.

The little strip of Broad Street between Wall Street and Exchange Place is kind of like a schoolyard for the merchant cash advance industry. War stories are exchanged, cigarettes shared and dreams dreamed. One day, I’m going to start my own ISO and I’ll do it differently because…

You can walk in any direction. The industry can be found on Broad Street, William Street, Pine Street, and Broadway. It’s on Water Street, Rector Street, Maiden Lane, and Fulton Street. It extends outward almost infinitely to Midtown, Brooklyn, Queens, Long Island, Staten Island, The Bronx, Westchester, Orange County, and New Jersey.

You can walk in any direction. The industry can be found on Broad Street, William Street, Pine Street, and Broadway. It’s on Water Street, Rector Street, Maiden Lane, and Fulton Street. It extends outward almost infinitely to Midtown, Brooklyn, Queens, Long Island, Staten Island, The Bronx, Westchester, Orange County, and New Jersey.

And while there are hubs in the outer parts, the most unique experience by far is down here on Wall Street, where you’re infinitely more likely to overhear professionals shouting “ACHs” and “stacks” than “puts” and “calls.”

Although the guides teach tourists that Wall Street as they imagined it to be is dead, Wall Street itself can never die.

Every now and then a pedestrian will look up at the offices above and wonder if the magic of fast-talking finance still exists. Is that world gone forever?

Not quite…

The stockbrokers may be gone, but there’s a new landlord. Wall Street belongs to the small business financing industry now.

The Official Business Financing Leaderboard

June 20, 2015A handful of funders that were large enough to make this list preferred to keep their numbers private and thus were omitted.

| Funder | 2014 |

| SBA-guaranteed 7(a) loans < $150,000 | $1,860,000,000 |

| OnDeck* | $1,200,000,000 |

| CAN Capital | $1,000,000,000 |

| AMEX Merchant Financing | $1,000,000,000 |

| Funding Circle (including UK) | $600,000,000 |

| Kabbage | $400,000,000 |

| Yellowstone Capital | $290,000,000 |

| Strategic Funding Source | $280,000,000 |

| Merchant Cash and Capital | $277,000,000 |

| Square Capital | $100,000,000 |

| IOU Central | $100,000,000 |

*According to a recent Earnings Report, OnDeck had already funded $416 million in Q1 of 2015

| Funder | Lifetime |

| CAN Capital | $5,000,000,000 |

| OnDeck | $2,000,000,000 |

| Yellowstone Capital | $1,100,000,000 |

| Funding Circle (including UK) | $1,000,000,000 |

| Merchant Cash and Capital | $1,000,000,000 |

| Business Financial Services | $1,000,000,000 |

| RapidAdvance | $700,000,000 |

| Kabbage | $500,000,000 |

| PayPal Working Capital* | $500,000,000 |

| The Business Backer | $300,000,000 |

| Fora Financial | $300,000,000 |

| Capital For Merchants | $220,000,000 |

| IOU Central | $163,000,000 |

| Credibly | $140,000,000 |

| Expansion Capital Group | $50,000,000 |

*Many reputable sources had published PayPal’s Working Capital lifetime loan figures to be approximately $200 million in early 2015, but just a couple months later PayPal blogged that the number was more than twice that amount at $500 million since inception. The print version of deBanked’s May/June magazine issue stated the smaller amount since it had already gone to print before PayPal’s announcement was made.

Lending Club Violated Securities Laws, Forced to File Rescission Offer

June 12, 2015Lending Club appears to have violated the securities laws of several states when it issued stock options as compensation between July 2012 and October 2014. According to an official Rescission Offer filed with the SEC on June 12th, Lending Club is offering to buy back both common stock shares and unexercised options to remedy their mistake. Combined, 40,469,837 shares of common stock are subject to the offer. Their reason for doing so is as follows:

We have issued shares of common stock or granted options to purchase shares to our current and former employees and consultants. From July 2012 through October 2014 (or during the periods specified on the addendum to this offering circular with respect to residents of certain states), the options we granted and shares issued upon exercise of the options may not have been exempt from the registration or qualification requirements under applicable securities laws.

The filing admits they violated the laws of at least 16 states and Puerto Rico.

For New York, it says, “We were required to apply for an exemption from the broker-dealer registration and securities issuance requirements with the State of New York to issue the shares and/or options to you without registration or qualification. Because of our failure to apply for an exemption, you have three years to seek a remedy for our failure to register.”

For New York, it says, “We were required to apply for an exemption from the broker-dealer registration and securities issuance requirements with the State of New York to issue the shares and/or options to you without registration or qualification. Because of our failure to apply for an exemption, you have three years to seek a remedy for our failure to register.”

For California, it says, “Certain options and shares issued pursuant to the 2007 Stock Incentive Plan may have been granted or issued in violation of the California Corporate Securities Law.”

The market price of the improperly issued shares amounts to $700 million. However, few if any shareholders subject to the rescission offer would likely accept it since it proposes buying back the shares at their original value + interest. Those values range from $0.06 to $8.94 per share. Lending Club closed today at $17.28, at double the highest proposed rescission offer price.

Indeed, no company officers are moving to accept the offer as it specifically states, “Seven of our officers and directors, who together hold 1,044,892 shares of common stock and options to purchase 11,081,780 shares of common stock, all of which shares are subject to this rescission offer, are eligible to participate in the rescission offer. We have been advised that these officers and directors do not intend to accept the rescission offer.”

Indeed, no company officers are moving to accept the offer as it specifically states, “Seven of our officers and directors, who together hold 1,044,892 shares of common stock and options to purchase 11,081,780 shares of common stock, all of which shares are subject to this rescission offer, are eligible to participate in the rescission offer. We have been advised that these officers and directors do not intend to accept the rescission offer.”

However, if the stock price were to drop by more than 50% between now and July 15th (the deadline to decide), the rescission offer would actually become in the money for a handful of investors. The odds of that happening are pretty slim.

Lending Club’s explanation for getting in this mess in the first place is as follows:

We became subject to the reporting obligations of section 15(d) of the Securities Exchange Act of 1934, as amended (Exchange Act) upon the effectiveness of our registration statement for our member payment dependent notes on Form S-1 on October 10, 2008. As a result, we were no longer entitled to rely on the qualification requirements pursuant to section 25102(o) of the California Corporate Securities Law. Because we could not rely on section 25102(o) of the California Corporate Securities Law, the options we granted and the shares issued upon exercise of these options during this period may have been issued in violation of California securities laws. In July 2014, we applied for a permit for qualification from the California DBO. In connection with the review of the permit application, the California DBO has required that we make this rescission offer to certain holders of any outstanding, unexercised options or shares of common stock issued upon exercise of stock options. Accordingly, we are making the rescission offer to the approximately 598 persons who received grants of options or purchased common stock upon exercises of options under the 2007 Stock Incentive Plan (except with respect to shares of our common stock which were subsequently sold by such persons at a price per share that exceeded the exercise price per share plus interest at the legal rate from the date of exercise, and therefore would exceed the amount of the rescission offer). If our rescission offer is accepted by all offerees, we could be required to make an aggregate payment to the holders of these options and shares of up to approximately $34.2 million, which includes statutory interest.

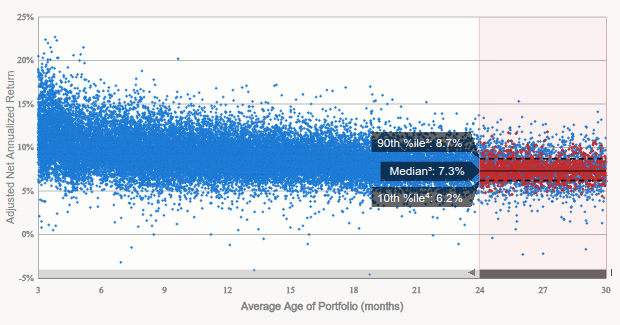

Is the Premium Gone in Peer-to-Peer Lending?

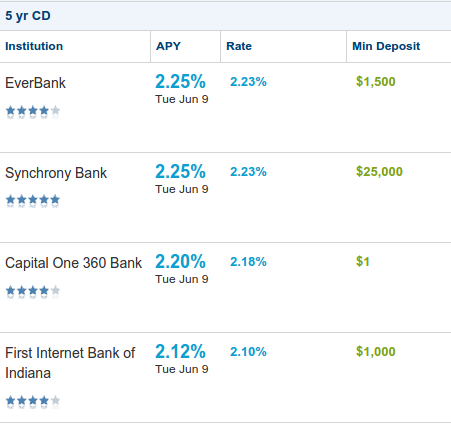

June 10, 2015FDIC insured 5-year CDs are now paying as high as 2.25% APR. Compare that against 5-year notes offered by Lending Club and Prosper that will pay ___________.

According to Lending Club, the average 2-year aged portfolio is yielding an average return of 6.2% to 8.7%. On loans maturing in 5 years, the numbers will be even lower. With peer-to-peer (P2P) lending being all the rage over the last few years, these returns look surprisingly benign.

Did something change?

According to Simon Cunningham’s LendingMemo analysis, investor returns have fallen almost 2% in two years. Cunningham wrote, “In 2014 something changed. Lending Club began to lower interest rates without adjusting FICO at all. Basically, for the first time in their company’s history they began to decrease the reward for investors without decreasing the risk.”

FICO stayed the same and rates came down, a move that was intentional and rationalized by Lending Club CEO Renaud Laplanche when he said, “By [lowering interest rates] we believe we can generate more positive selection. For example, this means people who now take a 10% loan offer, but who would have rejected a 12% offer, are typically also higher quality borrowers. So the belief is that part of the rate cut will be absorbed by lower defaults.”

Ironically, online business lender OnDeck, who has also lowered interest rates, might disagree with that psychology. Back on their Q4 2014 earnings call, OnDeck CEO Noah Breslow reported that their borrowers were basically taking the first offer they could get because of the time and stress associated with continuing the search.

For Lending Club, their gamble could mean that someone that would’ve taken a 12% offer is now taking a 10% offer even though they would’ve taken a 12% offer or a 15% offer or an 18% offer. Instead they are worried that borrowers will choose nothing if a loan is perceived to be too expensive. This experiment has wreaked havoc on investor yields.

“Folks shouldn’t enter this investment assuming a 7% return when they actually go on to receive 5.5%,” wrote Cunningham. He goes on to explain that average investor returns could go as low as 3.7%.

The price of risk

If you’ve been earning 0% in your savings account for the last few years, the returns in P2P have likely been a welcome reprieve. But as the probability that that Fed will soon raise rates increases, so too have riskless yields. According to bankrate.com, FDIC insured 5-year CDs are now paying as high as 2.25%, a figure that’s only 1.45% to 3.25% lower than Cunningham’s P2P estimates. Is the spread commensurate with the risk?

If you’ve been earning 0% in your savings account for the last few years, the returns in P2P have likely been a welcome reprieve. But as the probability that that Fed will soon raise rates increases, so too have riskless yields. According to bankrate.com, FDIC insured 5-year CDs are now paying as high as 2.25%, a figure that’s only 1.45% to 3.25% lower than Cunningham’s P2P estimates. Is the spread commensurate with the risk?

Previously, I’ve explained that Lending Club is not actually a middleman in a marketplace. No matter which notes an investor buys, they are in fact lending money to Lending Club itself. None of the notes matter if Lending Club goes bankrupt. An investor might as well be buying stock in the company.

Furthermore, none of the yield projections take into account a swift and brutal recession or a landmark legal ruling that could jeopardize an entire portfolio overnight. The loss of risk in Lending Club notes is your entire investment. It’s not just about the potential for low yield or negative yield. There is an inherent risk of total loss.

On a $100,000 investment, the added premium for a very risky asset over a riskless asset is potentially about $1,450 to $3,250 a year. Or is it?

Taxing away the premium

As loans default, investors might think they can offset the interest with their losses. That’s not the case because the interest is counted as normal income and the losses as capital losses. That means the losses can only be offset by capital gains income from other investments.

As loans default, investors might think they can offset the interest with their losses. That’s not the case because the interest is counted as normal income and the losses as capital losses. That means the losses can only be offset by capital gains income from other investments.

Therein lies the problem for an investor that has no capital gains. In that case, the IRS only allows individuals to deduct up to $3,000 in losses*. If someone is not investing outside of P2P lending, they’re at a big disadvantage.

Without capital gains, an investor could end up with this situation:

$10,000 in Lending Club interest income and $5,000 in Lending Club losses would result in being taxed on $7,000 in income (3k deduction limit). Talk about a yield killer.

With capital gains, any amount of losses can be offset against them.

On the Lend Academy forums, investors have hypothesized scenarios where the $3,000 limitation could lead to net yields below 1%!

To a relatively serious investor, the premium earned for investing in a very risky asset can be entirely wiped out by a tax limitation. Strangely then, the net dollar reward in a 5-year FDIC insured CD could potentially be the same as buying exotic consumer lending notes where total loss is very plausible. In that case, the notes offer no rational sense to invest in.

Indeed many P2P investors on the Lend Academy forums have reported plans to close their accounts or to invest only through IRAs where the tax rules are different.

Another tax

With P2P lending still a relatively young and confusing industry, a small retail investor may require the help of an accountant to prepare their returns, especially if they used folio where notes can be traded. Be aware that the hourly rate of tax preparation will cut into gains earned in P2P.

What’s in it for investors?

2.25% isn’t a very enticing offer, but neither is 5.5% if that’s the estimated figure barring any legal setbacks, bad recession, company failure, and tax consequences. As the economy prepares itself for an eventual increase in rates, the returns on savings accounts and CDs will rise over time. And yet Lending Club is curiously moving in the opposite direction. That’s great for borrowers, bad for investors.

The point at which it will no longer make economic sense to invest in P2P is eerily just around the corner if it’s not here already…

OnDeck Stock Pummeled in Run Up to Lockup Expiration

June 10, 2015 OnDeck (ONDK) hit a new low on Tuesday, bottoming out at $13.94 in intraday trading. It closed at $14.03. Absent any recent company news, the trend downward was likely a side effect of downward pressure on Lending Club (LC) as their lockup period expired. Lending Club closed at $16.97 near its all time low.

OnDeck (ONDK) hit a new low on Tuesday, bottoming out at $13.94 in intraday trading. It closed at $14.03. Absent any recent company news, the trend downward was likely a side effect of downward pressure on Lending Club (LC) as their lockup period expired. Lending Club closed at $16.97 near its all time low.

The OnDeck drop may have also been caused by the recent story that appeared in Barrons that labeled the company and the industry they operate in, risky, saturated, and overpriced.

On Deck is a different business. Its profits come from using its own balance sheet to make risky, high-interest rate loans to small businesses. With rivals as large as Goldman Sachs gathering around these companies’ shallow high-tech moats, the competition for quality borrowers will make it tougher for On Deck to keep growing loan originations near a triple-digit pace without loosening underwriting standards. Even in today’s benign conditions, On Deck charges off more than 12% of its loans annually, while its yields on those risky loans have declined for nine straight quarters. It’s a subprime lender in dot-com clothing.

Barrons laid out the case that OnDeck is a lender. OnDeck has always taken the position that they are a tech company. The conflicting market perceptions have made their stock price very chaotic.

OnDeck’s lockup period expires on June 15th.

Bless You, Fund Me: What Words Predict About Loan Performance

June 7, 2015 Way back in 2006 when I was just a baby merchant cash advance* underwriter, I encountered a book store that was borderline qualified. The final phone interview would make or break their approval so I grabbed my pen and paper and dialed their number.

Way back in 2006 when I was just a baby merchant cash advance* underwriter, I encountered a book store that was borderline qualified. The final phone interview would make or break their approval so I grabbed my pen and paper and dialed their number.

I went through the checklist of questions and they passed. But what really convinced me that it was a deal worth doing was the amount of times the owners made references to God. They were clearly religious people which indicated to me that they were probably also of high moral character. It didn’t matter what religion it was or if their beliefs aligned with mine, I was simply captivated by their values.

After approving the deal and funding them, they actually mailed me a handwritten letter to express their gratitude. It concluded with, “God Bless You!” and I hung it up on the wall of my cubicle to remind myself of the good I was doing for small businesses.

A few weeks later, the payments stopped. All of their contact numbers were disconnected and the owners of the store could not be located. They completely disappeared along with almost all of the money. Looking up at the note on my wall, a shiver went up my spine. Had I been duped? And did they use religion as a tool to influence my decision?

I thought that surely they must’ve encountered legitimate financial difficulty but I believed that even if so, people with their values would’ve been more forthcoming about it. Instead they just took the money and split and were never heard from again.

I learned a lesson about being emotionally influenced on a deal and it turns out there were clues this outcome might happen all along.

Bless you

In a study titled, When Words Sweat: Written Words Can Predict Loan Default, Columbia University professors Oded Netzer and Alain Lemaire, and University of Delaware professor Michal Herzenstein analyzed the text of more than 18,000 loan requests made on Prosper’s website. Applicants that used the word God were 2.2x more likely to default on their loans. And the phrase Bless you correlated higher on the default scale as well, though not as high as other non-religious words.

On the list of words more likely to be mentioned by defaulters are, I promise, please help, and give me a chance. Statistics actually show that someone promising to pay is less likely to pay than someone that doesn’t explicitly promise.

Among the other more common words likely to be mentioned by defaulters is hospital. This word holds special significance to me because in my last year as a sales rep, almost all of my underperforming accounts were supposedly due to the business owners or their family members being in the hospital.

Among the other more common words likely to be mentioned by defaulters is hospital. This word holds special significance to me because in my last year as a sales rep, almost all of my underperforming accounts were supposedly due to the business owners or their family members being in the hospital.

And it wasn’t just me. It seemed like every deal that was going bad in the office involved the hospital. Any time one of us was due to contact an account with an issue, we made bets that a hospital would come up in the story. (Seb, if you’re reading this, apparently it’s not a coincidence.)

I express no opinion regarding whether or not their stories were true, but statistics show that borrowers that mention hospital are more likely to default.

In the study’s Abstract, the professors wrote:

Using a naïve Bayes analysis and the LIWC dictionary of writing styles we find that those who default write about financial hardship and tend to discuss outside sources such as family, god and chance in their loan request, while those who pay in full express high financial literacy in the words they use. Further, we find that writing styles associated with extraversion, agreeableness and deception are correlated with default.

While the study focused on Prosper, their almost identical competitor, Lending Club, may have realized this trend earlier. In March 2014, Lending Club announced that investors would no longer be able to view the free-form writing portion of the borrower loan application. Citing “privacy reasons,” investors lost a valuable clue into the repayment probability of their notes.

But would it really have helped? The researchers wrote:

Using an ensemble learning algorithm we show that leveraging the textual information in loan requests improves our ability to predict loan default by 4-5.7% over the traditionally used financial information.

Nothing to see here folks, move along and approve

Curiously, Lending Club doesn’t want its investors to have access to a data point with such significant importance. Perhaps it’s because of disasters like this, where one borrower used the free-form writing section to spew profanities. Ironically, the loan was approved and issued anyway.

For tech-based platforms like Lending Club however, they noticed the “story” aspect of a loan had become less relevant because of overwhelming investor demand. Investors weren’t evaluating the written portion of the loan application as much anymore. According to their blog post at the time of the announcement, “Fewer than 3% of investors currently ask questions and only 13% of posted loans have answers provided by borrowers. Furthermore, loans are currently funding in as little as a few hours – well before borrower answers and descriptions can be reviewed and posted.”

It had become all algorithms and APIs where loans were fully funded by investors before the written portions could even be published on the website. Had anyone actually taken the time to read the above loan application answers, they probably wouldn’t have allocated money towards it.

But while removing the storyline from the data might give investors fewer methods to detect a good loan, it could actually protect them from getting drawn into a bad loan.

One of the authors of the above referenced study, Professor Michal Herzenstein of University of Delaware, found in 2011 that borrowers could manipulate lenders into not only approving them, but giving them more favorable terms.

You can trust me 😉

In a story that appeared on UD’s website in 2011, titled Good Storytelling May Trump Bad Credit, Herzenstein’s research discovered that borrowers who constructed a trustworthy picture of themselves “could lower their costs by almost 30 percent and saved about $375 in interest charges by using a trustworthy identity.”

The study referred to six possible categories or identities that borrowers would try to impress upon lenders to describe themselves (trustworthy, successful, economic hardship, hardworking, moral, religious). The story explains:

The more identities the borrowers constructed, the more likely lenders were to fund the loan and reduce the interest rate but the less likely the borrowers were to repay the loan – 29 percent of borrowers with four identities defaulted, where 24 percent with two identities and 12 percent with no identities defaulted.

It’s a case of measurable borrower manipulation.

“By analyzing the accounts borrowers give and the identities they construct, we can predict whether borrowers will pay back the loan above and beyond more objective factors like their credit history,” said Herzenstein. “In a sense, our results offer a method of assessing borrowers in ways that hark back to the earlier days of community banking when lenders knew their customers.”

Today’s tech-based lenders that are dead set on removing this human aspect from the equation may be taking a shortsighted approach after all as they evidently still struggle to make predictions with their numbers-only approach.

For example, a poster on the Lend Academy forum recently wrote this to me about early defaults in today’s algorithmic environment, “It would be nice if LC could predict who is going to default in the first few months of the loan and deny them, but I don’t think that is entirely possible.”

It reminded me of a big merchant cash advance deal I approved years back that passed all of the qualifying criteria with flying colors and still defaulted on the very first day. The merchant’s response to why he defaulted on day one? He felt like screwing us over… “Come sue me,” he said.

In a later meeting to review the deal’s paperwork, a group of managers agreed that I had done all I could to make the approval decision except one. I failed to account for the asshole factor.

Far from satire, it is not uncommon for financial companies to refer to an asshole factor in some regard. It’s a very subjective variable but it can make all the difference between an applicant that’s going to pay and one that’s not. Suddenly none of the hard data matters.

Is the applicant an asshole?

In a recent blog post by loan broker Ami Kassar, titled The Single Most Important Rule in Our Company, Kassar wrote, “if a customer, employee, or partner acts like a jerk – we don’t want to do business with them. If you want to be less diplomatic, you can call the rule – the no ###hole rule.”

In a recent blog post by loan broker Ami Kassar, titled The Single Most Important Rule in Our Company, Kassar wrote, “if a customer, employee, or partner acts like a jerk – we don’t want to do business with them. If you want to be less diplomatic, you can call the rule – the no ###hole rule.”

In many circumstances, the measure of someone being an asshole is relative to another person’s perception. There’s even an entire book on that subject if you’re interested. But what’s trickier, is that according to some studies, being an asshole is a positive thing in business. Would that also make them better borrowers statistically?

Referring back to the original cited study, one has to wonder if there might potentially be a list of words that more closely correlate with being an asshole. I don’t think anyone’s ever examined the Prosper data for that before.

You might not be able to quantify asshole-ishness from the text, but something as basic as a person’s pronouns can speak volumes about their personality or intentions. According to Professor James Pennebaker in the Harvard Business Review:

A person who’s lying tends to use “we” more or use sentences without a first-person pronoun at all. Instead of saying “I didn’t take your book,” a liar might say “That’s not the kind of thing that anyone with integrity would do.” People who are honest use exclusive words like “but” and “without” and negations such as “no,” “none,” and “never” much more frequently.

But saying “I” over “we” doesn’t necessarily make you less of a liar. Pennebaker discovered that depressed people use the word “I” much more often than emotionally stable people.

Being emotionally stable would probably make for a better borrower than a depressed one, but with all these influential and conflicting language clues, how can an underwriter possibly make the right choice?

For instance, if the following line appeared on the free-form writing portion of an application, how should it be interpreted?

Using all of the mentioned research as a guide, I’m inclined to consider the applicant a: trustworthy depressed lying asshole that’s not going to pay.

I = Depressed

We = Liar

God = 2.2x more likely to default

Have always been able to pay back = trustworthy

Hurry up and fund me = asshole

We could easily get caught up in the language here and ignore the obvious positives about this hypothetical applicant, such that they have an 800 FICO score and a solid six figure income. Shouldn’t that weigh more heavily? It’s easy to get distracted.

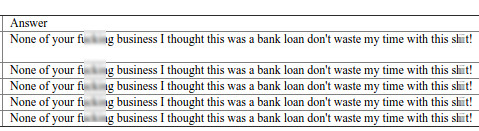

Perhaps Lending Club’s removal of the free-form writing section was for the investors’ own good. Even the borrower that repeatedly wrote, “None of your f**king business I thought this was a bank loan don’t waste my time with this sh**t!” is still current on all their payments after two and a half years.

To brokers like Kassar, the asshole factor is not so much about the likelihood of default anyway, but peace of mind. “Why invest emotional energy in putting up with shenanigan’s when there are so many good people who need our help,” he wrote.

Word is bond?

Regardless of what one study revealed about applicants that invoked God said about the likelihood of default, declining applicants on the basis of writing or talking about God could certainly be argued as religious discrimination. In many instances, religion is a protected class. Sometimes you have to ignore correlations because they can be deemed discriminatory.

One thing is for sure though, back in 2006 the upstanding characters I had created in my mind about the religious book store owners were upended when they disappeared into the night with all the money. Their words got in my head and I approved them perhaps because of it.

Years later, an asshole defaulted on the first day and not long after that, there would be a mysterious spate of accounts whose poor performance would be attributed to supposed hospital related events.

What’s buried in a person’s words? The answers allegedly. I promise…

When the Money’s Gone in Peer-to-Peer, It’s Gone

June 4, 2015 If you held on to stock index funds throughout the financial crisis, you eventually made all your money back and then some. A beautiful characteristic of the stock market is that being down doesn’t erase the money lost permanently. The value can always go right back up.

If you held on to stock index funds throughout the financial crisis, you eventually made all your money back and then some. A beautiful characteristic of the stock market is that being down doesn’t erase the money lost permanently. The value can always go right back up.

With peer-to-peer member payment dependent notes, like the kind Lending Club and Prosper sell to investors, there is no comparable way to recover losses. Once a loan defaults, that money is gone. Optimism, a market rally, and good consumer news won’t bring it back.

Anil Gupta, the co-founder of PeerCube summed this up well in the Lend Academy forum:

With losses in P2P lending, the challenge is you never recover “double digit percentage” losses incurred. There is finite life for a loan and once it is charged off, you not only have lost your principal but also any possibility of future returns from the sunk money in the loan. With stock, at least you don’t realize losses until you are ready to realize them or company goes bankrupt or you can wait out for stock to recover or double-down. Troubled P2P notes are like stock options that expire worthless.

The potential to lose money permanently with no chance to recover simply by waiting it out should weigh heavily on your decision to invest in P2P notes.

Don’t Steal Deals Bro

June 4, 2015 It’s a scenario that’s become all too common in the merchant cash advance industry. An employee quits or gets fired and within weeks they begin soliciting all the previous clients they worked on for revenge… or money… or both.

It’s a scenario that’s become all too common in the merchant cash advance industry. An employee quits or gets fired and within weeks they begin soliciting all the previous clients they worked on for revenge… or money… or both.

Maybe they signed an agreement that was supposed to prevent this or maybe they didn’t. In my own personal perspective, it shouldn’t matter.

Don’t steal deals bro

If you’re as good a closer as you think you are, your new ISO shouldn’t rely on stealing deals from the last company you worked at. On the one hand you will be taking time away from what’s important, and that’s creating a long term business model. Stealing deals might generate some nice checks but it’s not a business. A ton of new ISOs fail and that’s because they have no idea how to generate new deals. I guess you’re not a closer bro…

On the other hand, stealing deals will permanently burn an industry bridge at best and get you sued at worst. The one thing harder than starting a new business is starting a new business while there is someone out there actively trying to make you fail.

Don’t sue me bro

If you signed an agreement with a non-solicit clause, you probably shouldn’t solicit. Several companies in the industry have used the court system to try and enforce non-solicits or non-competes (no matter how weakly worded) against former employees. Some of these lawsuits have dragged on for years and likely cost the alleged contract breachers hundreds of thousands of dollars just to defend themselves.

There’s a way around this and that’s to negotiate with an employer to amend the agreement prior to your employment there. If they won’t bend on certain clauses like non-competes, then chances are if you go ahead and sign anyway, they are going to try and enforce it even if they end up not succeeding.

“ISOs must always think about the possible consequences under their agreements for moving merchants,” wrote Adam Atlas in a recent Green Sheet article that applies almost equally to the merchant cash advance industry.

Atlas goes on to explain however, that enforcing a non-solicitation could backfire, in the sense that if the ISO feels its trivial or unwarranted, they could escalate their efforts to move deals away. They’ll probably also feel inclined to spread the word and spook the company’s other ISOs. That could really come back to bite.

Be sure to read ISO Legal Blunders by Adam Atlas on the Green Sheet.

Thinking about stealing deals? Consider the legal stuff bro.