Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

January/February 2016 Cover Teaser

January 25, 2016The January/February 2016 issue of deBanked magazine is set to ship soon. Can you guess who is on the cover???

If you don’t already get the hard copy of our magazine, you can SUBSCRIBE HERE FREE. To review previous issues in HTML or PDF, click here.

Platinum Rapid Funding Group Sets Annual Funding Record

January 25, 2016Platinum Rapid Funding Group, a Long Island, NY based merchant cash advance provider, set a new personal-best funding record last year, according to company VP of Partner Relations Corey Cicero. Through direct and indirect channels, the company originated more than $100 million worth of funded deals during 2015.

The growth has led to what seems like a never-ending hiring spree at their Uniondale office. Cicero told deBanked that they plan to beat their 2015 figures this year by a wide margin. “We are still hiring,” he said.

deBanked visited their office back in September and as evidenced by the above photo, they are not a small shop.

Experts on Marketplace Lending Featured by Experian (Video)

January 21, 2016Experian, the company many marketplace lenders are using for credit reports, recently put together a short video that features some of the industry’s experts. They include:

- Peter Renton, Founder, Lend Academy

- Scott Sanborn, COO, Lending Club

- Sam Hodges, Co-founder, Funding Circle USA

- Andrew Smith, Partner, Covington & Burling

- Joseph DePaulo, CEO, College Ave.

- Kathryn Ebner, VP, Credibly

Check out the video:

If it’s not loading on your browser, view the original here.

Why OnDeck Didn’t Sign The Small Business Borrowers Bill of Rights

January 21, 2016 Recent media reports attempting to spin OnDeck’s loan programs in a negative light have been quick to point out that they have not signed on to the Small Business Borrowers Bill of Rights. There’s apparently an obvious reason for that, they weren’t invited to participate in the drafting of it…

Recent media reports attempting to spin OnDeck’s loan programs in a negative light have been quick to point out that they have not signed on to the Small Business Borrowers Bill of Rights. There’s apparently an obvious reason for that, they weren’t invited to participate in the drafting of it…

In a recent interview with Lend Academy’s Peter Renton, Breslow addressed this even further. “I think if you look at the actual principles and the way the document is written, there is a clear bias towards longer term loans in the document,” Breslow told Renton, pointing out that the group is a small circle of lenders that focuses on 3-year loans. “We don’t think a three-year product is appropriate for many types of small businesses out there, but if you can’t get access to a long term loan we don’t think that means you shouldn’t get a loan at all,” he added. “So what we’d love to see either in the BBOR or some other industry standard that you might see developing over the next year is a broader perspective on what types of financing businesses should have access to and to be clear, we’re very supportive over time, kind of inclusive industry standards that encompass the range of products that we think small businesses should have access to and that access should be fair, efficient and transparent.”

You can listen to the entire interview which covers many more topics below:

Or read the full transcript here.

Renton is a co-founder of the LendIt conference, the biggest marketplace lending event of the year. If you haven’t secured tickets yet to the April conference in San Francisco, you should sign up here before it’s too late. Last year the conference was completely sold out.

Moody’s Position on Marketplace Lending

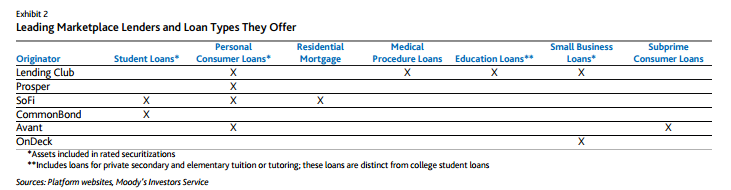

January 21, 2016You can’t slap a FICO score on to an entire industry but you can still assess its short term and long term risks. That’s precisely what ratings agency Moody’s has done in a report they published last month titled, 2016 Outlook – Marketplace Lending Platforms Will Continue to Evolve, Expand Loan Types.

In their report, Moody’s defines “marketplace lending” as “the growing industry of Internet-based, alternative lending platforms for consumers and small businesses.” And there’s good news, they predict it will further expand globally in 2016. The US is not even the biggest game in town, according to Moody’s, China is. “China will remain by far the largest market for marketplace lending and similar online lending platforms,” they wrote.

OnDeck was labeled as the leading player in the small business loan market, SoFi and CommonBond for student loans, and Lending Club, Prosper, SoFi, and Avant for personal consumer loans.

Listed among the industry’s risks is the Madden v. Midland decision. Ironically, merchant cash advance companies who gave up doing purchases of future receivables in exchange for becoming a “true lender” have found themselves wondering if merchant cash advance was perhaps the safer model all along. “Questions remain about the viability of the loan origination model many marketplace lenders currently use, in which a partner bank originates the loans, then promptly sells them to the marketplace lender,” the Moody’s report states. “This model allows marketplace lenders to take advantage of federal “rate exportation” laws and offer loans with interest rates that exceed the maximum rate otherwise allowed.”

Below are some of the other highlights:

- An increase in interest rates will not have an impact on performance but defaults will rise moderately

- Defaults on student loans will continue to be low

- Unemployment is not expected to rise in the near term

Most people probably can’t name more than 5 peer-to-peer lending platforms in the US. Meanwhile in China, there are so many that 800 of them have already failed or were recently facing major liquidity issues. There are more than 2,600 platforms there nationwide.

Lending Club Stock Curiously Clobbered

January 20, 2016When Lending Club’s share price was nearing its all-time lows late last year, one might think that company executives would be eager to buy, if for no other reason than to signal long-term confidence. That’s precisely what company CEO Renaud Laplanche did when he bought 60,000 shares on November 30th. And from that date until December 10th, the stock rose from $12.02 to $14.16. That put them within a dollar of their $15 IPO price, a reassuring sign even if they were still down 50% from their all-time high a year earlier.

Here’s what happened next:

- December 14th: The company’s Chief Financial Officer sold 13,950 shares

- December 15th: Board member and former US Treasury Secretary Larry Summers sold 23,421 shares.

- December 16th: The Fed raised interest rates

- December 18th: The company’s Chief Risk Officer sold 75,000 shares. (stock closed at a new all-time low of $11.48)

- January 6th: The company’s Chief Marketing/Operating Officer sold 35,000 shares. (stock closed at a new all-time low of $10.12

- January 11th: The company’s Chief Technology Officer sold 12,500 shares. (stock closed at a new all-time low of $9.24)

- January 12th: The company’s Chief Technology Officer sold 12,500 shares.

- January 13th: The company’s Chief Technology Officer sold 12,500 shares. (stock closed at a new all-time low of $8.86)

- January 14th: The company’s Chief Technology Officer sold 12,500 shares. (stock closed at a new all-time low of $8.02)

While company insiders were selling relatively small blocks of shares and likely doing it to bank just a little bit of their paper wealth, the trades coincided with the company’s plunge to oblivion and perhaps contributed to the drop in the first place. On January 14th, the date of the last insider sale, trading volume spiked to nearly 5x the daily average and the share price hit a record intraday low of $7.76.

While company insiders were selling relatively small blocks of shares and likely doing it to bank just a little bit of their paper wealth, the trades coincided with the company’s plunge to oblivion and perhaps contributed to the drop in the first place. On January 14th, the date of the last insider sale, trading volume spiked to nearly 5x the daily average and the share price hit a record intraday low of $7.76.

Lending Club finished at $7.34 on January 19th, a new all-time record low, with dips as low as $7.05 intraday. That means the stock has dropped nearly 40% since the CEO bought shares less than two months ago. By comparison, the S&P 500 is down 9.5% over that time period.

The share price death spiral has arguably made it easier to spread fear. In the Lending Club subforum on the LendAcademy website for example, a user claiming to manage a hedge fund urged members who use Lending Club’s marketplace to sell everything now and prepare for an armageddon of loan defaults. That thread was suspiciously created around the market open of January 14th, the date with the most trading volume since the IPO.

Meanwhile investors in Lending Club’s notes have remain largely unperturbed. And why wouldn’t they? They’re still enjoying very attractive returns and despite all the doom and gloom, everything is pretty much business as usual.

In a note to shareholders, Compass Point Research and Trading, LLC set a price target of $12 for Lending Club back in December on the risk of the Madden v. Midland case, Congressional investigations into terrorism finance, and the California Department of Business Oversight inquiry into marketplace lenders. While all are perhaps concerning, none seem to present an immediate threat. The most likely reason for the run on Lending Club is that general market fear is stoking reminders of the 2008 crash in which anything related to lending was toxic. As of Tuesday’s close, OnDeck, a business lender often compared to Lending Club, was down 61% from their IPO price. Lending Tree, an online consumer lending portal was down 51% from its 52 week high.

Meanwhile, Lending Club posted positive results in the 3rd quarter. Compared to the same period last year, revenue more than doubled, adjusted EBITDA tripled, and loan originations doubled. They also posted a profit. Overall, these results should not have caused the stock to drop by 50% over the next few months.

As a marketplace, Lending Club does not keep the loans it makes on its balance sheet. That’s something a lot of investors might be overlooking. They may have been clobbered these last few months but the fears might be somewhat unfounded. ..

FICO-Free Zone

January 15, 2016![]() Many lenders and alternative funders over the last several years have stressed a reduced dependence on FICO scores, but SoFi might be the first lender to declare their turf a “FICO-Free Zone.”

Many lenders and alternative funders over the last several years have stressed a reduced dependence on FICO scores, but SoFi might be the first lender to declare their turf a “FICO-Free Zone.”

In a blog post, SoFi co-founder Daniel Macklin vented that his 15 years of credit history in the UK prior to moving to the US counted for nothing at all. To fix that, he felt pressured to obtain and use credit just to build his score, which he referred to as counterintuitive. For those that have been in this country all along though, his gripe was that things that should matter in a credit score for some reason don’t. “The FICO score calculation doesn’t consider things like your savings, your cash flow, your ability to pay non-credit bills like water and electric or your future earnings,” he wrote.

That’s the opposite of how other marketplace lenders are thinking.

In an online discussion I had six months ago with some members of the Lend Academy forum regarding a borrower’s ability to repay as evidenced by their bank statements, the feedback was resoundingly negative. “I have a feeling if you ask to crawl someone’s bank account, they’ll just go elsewhere,” one user said. “Seems that’d only work on subprime borrowers who have limited bargaining power,” he added.

The logic behind the defense of a continued FICO-oriented approach was steeped in competitive advantage, basically that no sane borrower would ever consider disclosing additional information about their financial situation to one lender when another would just give them a loan on FICO score alone. Ironically that translated to, anyone who wants their creditworthiness to be judged on their ability to pay probably can’t afford to pay, at least that was my takeaway from it.

But over in SoFi land, the student lender “has chosen to not use FICO scores when evaluating the financial wherewithal of applicants.” They alternatively examine your more complete financial situation and well-being, things marketplace lending investors on other platforms (at least for consumer loans) seemed to argue couldn’t and shouldn’t be done.

SoFi is no small fish. To date they have issued around $7 billion in loans.

Hedge Fund Manager Tells P2P Lending Enthusiasts That He’s Shorting Them

January 14, 2016 On the Lend Academy forum, a user claiming to be a hedge fund manager lectured enthusiasts about their naiveté. “I manage a hedge fund and I’m short pretty much everything in the realm of P2P lending. Everything. I hope you don’t take it personally,” he opened with.

On the Lend Academy forum, a user claiming to be a hedge fund manager lectured enthusiasts about their naiveté. “I manage a hedge fund and I’m short pretty much everything in the realm of P2P lending. Everything. I hope you don’t take it personally,” he opened with.

Then with the kind of abrasive charm one might expect from a hedge fund manager, he went on to accuse Lending Club of engaging in “brazenly negligent lending.” “You can’t listen to what they tell you about a FICO score. The same thing happened in 2007,” he argued.

When users pushed back with math, he ranted that consumers were basically all on the verge of default, the system is being gamed, fraud is rampant, and the underwriting is worse than ever. “My honest advice is to get out now, if you can,” he added.

As Lending Club’s share price ($8.02) sank to another all-time low today, one has to wonder if fear mongering like this could be having an effect out there or if there really is something to worry about.

What do you think? You can catch up on the thread here.