Stories

Jackie Reses is Leaving Square Capital

October 2, 2020 Square Capital’s lead executive, Jacqueline Reses, is leaving the company. Square announced on October 2, that her resignation would be effective as of October 31. Reses is largely responsible for developing Square’s robust lending business, one that effectively made the company one of the largest non-bank small business lenders in the country.

Square Capital’s lead executive, Jacqueline Reses, is leaving the company. Square announced on October 2, that her resignation would be effective as of October 31. Reses is largely responsible for developing Square’s robust lending business, one that effectively made the company one of the largest non-bank small business lenders in the country.

It’s time to hang up my boots and say goodbye to my good friends at @Square. To the people I’ve worked with: everything I love about Square is related to you. It is my privilege and honor to have been along for the ride with you.

— Jackie Reses (@jackiereses) October 2, 2020

I shared my thoughts with Squares today because the place is so special! I thought I would share. pic.twitter.com/tXAE0dZhK9

— Jackie Reses (@jackiereses) October 2, 2020

Square Capital’s Jackie Reses Reveals Why They Really Gave Up Merchant Cash Advances

April 14, 2016At Lendit, Bloomberg Reporter Emily Chang asked Square Capital head Jacqueline Reses to explain the real reason behind Square’s shift from merchant cash advances to loans.

Reses said that it was not a customer issue, but an investor one. “This industry and this conference more than anyone understands the nuance between MCAs and loans,” she said. “From an investor side, that’s really where the savings are between the form of an MCA and the form of a loan, in that there’s an actual repayment date.”

Reading between the lines, she seemed to be saying that investors like certainty and exact terms whereas the traditional merchant cash advance product was harder to sell off or securitize because they lack a defined element of time.

Fast loan approvals shouldn’t be criminalized

Referring to the criticism that online lenders have been getting recently for their fast approvals, Chang specifically asked if companies like OnDeck were approving loans too quickly.

Reses responded, “I don’t think the ability to execute something quickly, smoothly, transparently, should be criminalized as something that requires oversight, and so I think being good at something should be well regarded.” She later added, “I think the notion that credit decisions being swift is a problem is just misguided.”

Transparency

Reses used the word “transparency” several times but in explaining such did not reference the disclosure of Annual Percentage Rates even once. Instead she mentioned the importance of spelling out the total dollar cost to the merchants, subtly reconfirming the findings that are coming from many other alternative lenders.

Was the move from MCA just about investors though?

Read our initial assessment and expanded theory.

Watch the full “fireside chat” video below:

Square Makes Jeopardy’s Daily Double

September 17, 2020“What is Square?”

That was the right question to the answer read by Jeopardy host Alex Trebek during an episode that aired this week. Contestant “Beth” hit a Daily Double and waged $2,000 to try and take the lead over “David” and “Joe.”

@Jack, hello pic.twitter.com/zwIzdAyTVT

— Nick D 👨👧 (@ndimichino) September 17, 2020

Square employees reacted on twitter by pointing out that the quoted transaction cost was a little out of date, but mostly took the honorable mention in stride.

We've made it! https://t.co/MZoZofrsno

— Jackie Reses (@jackiereses) September 18, 2020

Round Two of PPP Is Targeting Much Smaller Businesses

May 4, 2020 $79,000. That’s the average loan size reported in Round Two of the PPP so far. The figure is about a third of the average size approved in Round 1. Some of that is by the SBA’s design. On April 29th, the SBA disabled submission access to all lenders whose assets exceed $1 billion to prioritize small lenders and their small business customers.

$79,000. That’s the average loan size reported in Round Two of the PPP so far. The figure is about a third of the average size approved in Round 1. Some of that is by the SBA’s design. On April 29th, the SBA disabled submission access to all lenders whose assets exceed $1 billion to prioritize small lenders and their small business customers.

Though the pause button for big lenders was only in effect for eight hours that day, it was recognition that the playing field had not been level in the first round. JPMorgan Chase, the largest lender in round 1, for example, had an average PPP loan size of $515,304 in that round.

It’s a competitive process for limited dollars. 5,400 direct PPP lenders have already participated in the second round. More than 80% of those have less than $1 billion in assets. Senator Marco Rubio, a champion of PPP, called the latest figures released by the SBA as “all good news.”

Square Capital, meanwhile, has taken small to the extreme. Their average PPP loan approval as of April 29th was just $16,000, according to stats published by Square Capital head Jackie Reses on twitter. But only 2,711 of the 38,000+ approved had received the funds so far.

Still, that average is significantly smaller than the average loan size of $73,000 approved by Ready Capital in Round 1, a non-bank lender that got widespread attention for approving more PPP loans than any other lender in the country. Those record-breaking numbers, however, led to delays in borrowers receiving their funds to the point where as of April 30th, the responsibility of funding those loans had reportedly transferred to Customers Bank.

OnDeck has also played a role in the PPP, though only as an agent despite being approved by the SBA to lend. That news, which was revealed last week in the company’s quarterly earnings call, is likely due to the company’s current predicament brought on by government-mandated shutdowns.

Square to Expand Beyond Business Loans to Consumer Loans

June 27, 2017Square is making the leap from business loans to consumer loans, according to the WSJ. The company, which already makes loans to its payment processing clients, will now begin offering loans to the customers of those clients. The WSJ reports that the loans will be available in six states including California, New York and Florida. They also used a wedding photographer and a veterinarian as examples of services that consumers may wish to finance.

Square Capital head Jacqueline Reses is quoted as saying that there are no plans to get into car loans or mortgages.

Square Lent $251 Million to Small Businesses in Q1

May 4, 2017It was another big quarter for Square Capital, who originated more than 40,000 business loans for a total of $251 million. That’s an increase of 64% year-over-year but only up 1.2% from the previous quarter. The company had $51 million in loans held for sale on their balance sheet as of March 31st.

Overall, Square, Inc. had a net loss of $15 million for the quarter compared to a $96.7 million loss over the same period last year. Investors took the news in stride, pushing the stock price up from under $18.50 to temporarily over $20.

Of notable interest in the fine print of their 10-Q, is acknowledgement that there have been and could be challenges to the chartered bank model on which they rely to make their loans, to the point where they say it’s possible they could one day have to revert back to the merchant cash advance model.

We have partnered with a Utah-chartered, member FDIC industrial bank to originate the loans. There has been, and may continue to be, regulatory interest in and/or litigation challenging partnered lending arrangements where a bank makes loans and then sells and assigns such loans to a non-bank entity that is engaged in assisting with the origination and servicing of the loan. If our bank partner ceases to partner with us, ceases to abide by the terms of our agreement with them, or cannot partner with us on commercially reasonable terms, and we are not able to find suitable alternatives and/or obtain licenses to make loans ourselves, Square Capital may need to enter into a new partnership with another qualified financial institution, revert to the merchant cash advance (MCA) model, or pursue an alternative model for originating loans, all of which may be time-consuming and costly and/or lead to a loss of institutional third party investors willing to purchase such loans or MCAs, and as a result Square Capital may be materially and adversely affected.

Square originally relied on the merchant cash advance model but switched to making loans after they found it challenging to package them up and sell them to investors.

A Glimpse into Square Capital’s Marketing

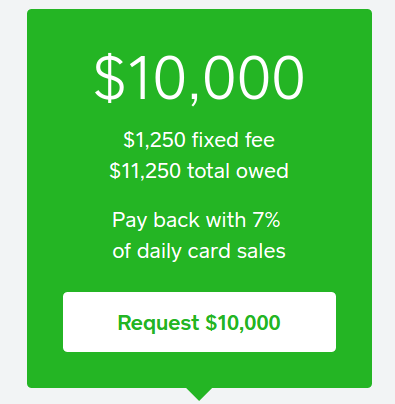

October 20, 2016As a merchant, Square has marketed their Square Capital program to me before. But this is the first time I’ve received direct mail marketing from them. Here’s a snapshot of what that looks like:

To view the potential offers, merchants are directed to log in to their Square accounts where they will see multiple terms. Even though their particular product is a loan made possible through Celtic Bank, all of the proposed loan offers are presented using the Total Cost of Capital method. That means cost is disclosed as a precise dollar amount so that potential borrowers will know exactly how much they will have to pay. Several studies have indicated that this is the easiest to understand, though it has been subject to some debate.

“There are no ongoing interest charges for your loan, only the one-time upfront fee that is listed as a dollar amount,” the Square Capital FAQ page states. “The total cost of the loan is a fixed fee and the total amount owed never changes.”

“There are no ongoing interest charges for your loan, only the one-time upfront fee that is listed as a dollar amount,” the Square Capital FAQ page states. “The total cost of the loan is a fixed fee and the total amount owed never changes.”

One of the defining features that makes Square Capital’s loan product different from a merchant cash advance or a purchase of future sales, is that Square enforces a fixed 18 month term. “If the loan hasn’t been repaid in full at the end of 18 months, the remaining loan balance will be due in full,” they state. That is completely unlike a purchase transaction in which there is no deadline or term. Even MCA purchase transactions that stipulate fixed daily payments do not actually have fixed terms. That’s usually because if a merchant’s sales activity rises or falls, they have the contractual right to request an adjustment to those payments to effectuate the basis of the agreement, that future sales be delivered in accordance with the unpredictable ebb and flow of business. That makes the date in which delivery will be satisfied in full unknowable. It’s that unknowable that can cause MCA transactions to be more expensive than their loan counterparts, though that is absolutely not always the case.

For Square, unknowable contract satisfaction dates likely made it difficult to bundle these deals up to sell off to institutional investors. Square Capital head Jackie Reses articulated this challenge during her appearance on an April 2016 LendIt stage. “From an investor side, that’s really where the savings are between the form of an MCA and the form of a loan, in that there’s an actual repayment date,” she said.

Even institutional investors recognize and understand that MCA purchase agreements do not have fixed terms.

Square Capital Outgrows Square

August 11, 2016 You don’t need to process payments through Square anymore to get a loan from Square Capital. Restaurants that use Upserve, a restaurant payments and data analytics system, are now eligible as well.

You don’t need to process payments through Square anymore to get a loan from Square Capital. Restaurants that use Upserve, a restaurant payments and data analytics system, are now eligible as well.

Formerly known as Swipely, Upserve is still relatively small, with only 7,000 restaurants as customers. But it’s a milestone for Square nonetheless, whose loan program within their own ecosystem has become so successful, that they feel comfortable venturing outside of it.

“We are proud to partner with Upserve and offer loans through Square Capital to even more small businesses who traditionally face barriers when seeking access to funds,” said Jacqueline Reses, Head of Square Capital.

The move puts them on a path to truly competing with other alternative lenders such as OnDeck and CAN Capital. Loans are repaid just like they are through Square, through a percentage of each day’s card sales with the option to repay early at no additional fee.

See Post... reses lung function and decreases death rate that would help ease the panic.... will know very quickly if that's even on the table. (my hunch is there is something), , your 1st option if numbers slow down doesnt mentioned deaths but is really best case scenario with all that is being implemented, you didnt include worse case or averag... |

See Post... reses lung function and decreases death rate that would help ease the panic.... will know very quickly if that's even on the table. (my hunch is there is something), , they are dying from more than decreased lung function. they are dying from septic shock and multiple organ failure, too.... |

See Post... reses lung function and decreases death rate that would help ease the panic.... will know very quickly if that's even on the table. (my hunch is there is something)... |