OnDeck Reports Q1 Net Loss of $59M, Suspends Non-PPP Lending Activities

O nDeck has suspended the funding of its Core loans and lines of credit to new or existing customers (unless the loan agreement has already been executed).

nDeck has suspended the funding of its Core loans and lines of credit to new or existing customers (unless the loan agreement has already been executed).

The company has also suspended its pursuit of a bank charter. The company has instituted a 15% pay reduction for its full-time employees, a 60% pay reduction for part-time employees, and furloughed additional employees that will receive benefits but no salary. OnDeck CEO Noah Breslow and members of the Board took a 30% pay reduction.

The company said that PPP funding has not really reached real small businesses like the ones they serve and as such only a handful of their customers have received PPP funds. While OnDeck is approved to operate as a PPP lender themselves, they have been acting as an agent of them in the interim and will dedicated their resources almost entirely to this endeavor. The company anticipates that originations of its own products could contract by 80% or more in Q2.

The company has not tripped any covenants or triggers with its own lenders as of yet but is currently in discussions with them on a path forward in this environment.

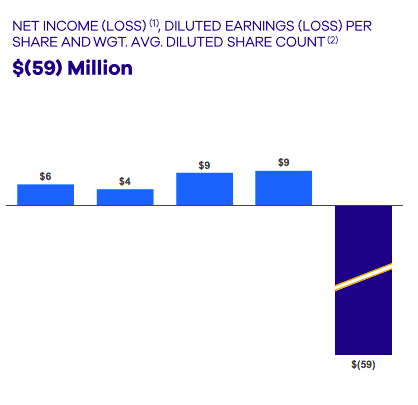

OnDeck reported a Q1 net loss of $59M on Thursday morning. The first quarter loss was driven by an increase in the Allowance for credit losses to reflect the increase in expected credit losses related to the COVID-19 pandemic. Provision for credit losses was $107.9 million. The Allowance for credit losses increased to $206 million at March 31, 2020, up $55 million or 36.1% from year-end and $58 million or 39.5% from a year ago. The 15+ Day Delinquency Ratio increased to 10.3% from 9.0% the prior quarter and 8.7% a year-ago reflecting a broad-based decline in portfolio collections since mid-March.

OnDeck reported a Q1 net loss of $59M on Thursday morning. The first quarter loss was driven by an increase in the Allowance for credit losses to reflect the increase in expected credit losses related to the COVID-19 pandemic. Provision for credit losses was $107.9 million. The Allowance for credit losses increased to $206 million at March 31, 2020, up $55 million or 36.1% from year-end and $58 million or 39.5% from a year ago. The 15+ Day Delinquency Ratio increased to 10.3% from 9.0% the prior quarter and 8.7% a year-ago reflecting a broad-based decline in portfolio collections since mid-March.

Noah Breslow, chief executive officer, is quoted in the announcement:

“In the span of several weeks, the spread of COVID-19 led to government-mandated lockdowns for small businesses both in the US and globally, placing our customers under unprecedented economic stress.After a successful and rapid transition to remote work, we effected immediate changes to our business to preserve liquidity, support our customer base, manage our loan portfolio and reduce costs. With an uncertain timetable for the reopening of the economy, and the effectiveness of government stimulus for small businesses unclear, we will be reducing debt balances in the second quarter and focusing on managing our portfolio, delivering government stimulus to our customer base and ensuring the company has the runway to scale operations again when the economy reopens.”

The company fully utilized its initial $50 million share repurchase authorization in the first quarter of 2020. On February 10, 2020, the Board authorized the company to repurchase up to an additional $50 million of common shares, and the company has approximately $23 million of remaining capacity under that authorization. The company suspended share repurchases late February but maintains authorization to resume purchases at its sole discretion.

For 2020, OnDeck expects:

- Portfolio contraction reflecting an 80% or more reduction in second quarter origination volume

- Increased delinquency and charge-offs stemming from COVID-related economic deterioration

- Reduced Net Interest Margin reflecting a lower portfolio yield

- Reduced operating expenses, on pace to cut second quarter expenses by approximately 25%.

The company had been on a modestly positive trajectory as of year-end 2019.

The company’s stock had a somewhat minor rally on Wednesday, closing at $1.61. That’s still substantially down from where it stood on February 20th at $4.22. It hit a low of 66 cents on March 18th. The share price dropped by nearly 19% after earnings were released on Thursday morning.

This story will be updated as the information becomes available.

Last modified: April 30, 2020Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.