Archive for 2021

Ohio Sends State Reps to Vegas to Pitch Fintech Companies

October 28, 2021 As brokers, lenders, and fintech companies look into having offices outside of New York or California now more than ever before, the state of Ohio used Money 20/20 to pitch their state as the best home for any company dealing with money or the innovations surrounding it.

As brokers, lenders, and fintech companies look into having offices outside of New York or California now more than ever before, the state of Ohio used Money 20/20 to pitch their state as the best home for any company dealing with money or the innovations surrounding it.

With Ohio’s lack of a state-level corporate income tax, relatively low rent, and modest wages compared to places like New York, headquartering in the state is a business decision that Terry Gore, Senior Director of Financial Services in Fintech for Jobs Ohio, referred to as a “no brainer.”

“I’ve been coming to this event for the last four years, the organization probably the last five or six years, and we think we have a very unique value proposition for the audience this year,” said Gore. That [proposition] is fintech, insurtech, in terms of the ecosystem that we have in Ohio, and using that to support their continued growth and expansion.”

Gore broke the pitch down into three main components about why Ohio is the most economically sensible state to headquarter a company in.

“We’re ranked in the top three in terms of headquartered banks and insurance companies, and we’re the fifth largest final services sector in the US market, so from a potential partner standpoint, I think we’ve checked that box.”

He went on to stress the access to higher education that Ohioans have, arguing that their talent pool is right up there with that of New York and California.

He went on to stress the access to higher education that Ohioans have, arguing that their talent pool is right up there with that of New York and California.

“Most people don’t know, just from a number of citizens’ perspective, we’ve got just under twelve million, we have talent,” said Gore. “We’ve got over 200 colleges and universities, from a talent pool perspective, those companies could tap into that.”

The final component Gore stressed was Ohio’s geography. Nestled in between New York and Chicago, he described it as the perfect place for a company that does a wide array of business across the heartland and the coasts to call home.

“We’re in the eastern standard time zone, we’re just a short two hour flight from three quarters of the financial centers in North America. So you know it’s one of those things where you don’t have to be located in New York to be able to drum up business in New York, you can just literally have a day trip and work that market.”

Ohio has already become a home for major players in the fintech world with companies like Klarna and AllianceData already hosting their headquarters in the state.

“We’ve been able to attract California based companies like Upstart, who moved into central Ohio and opened up their second headquarters, which is now larger than their California based location,” Gore said.

In the midst of their efforts to express all the benefits their state offers, Gore admitted that perception of his state to the rest of the country has a major influence on the decision making that goes into doing business there.

“We want to be viewed more traditionally than what the state has been viewed as, and that’s pretty much focused on manufacturing or a fly-over state. If you’re going to complain about the weather, I can’t help you.”

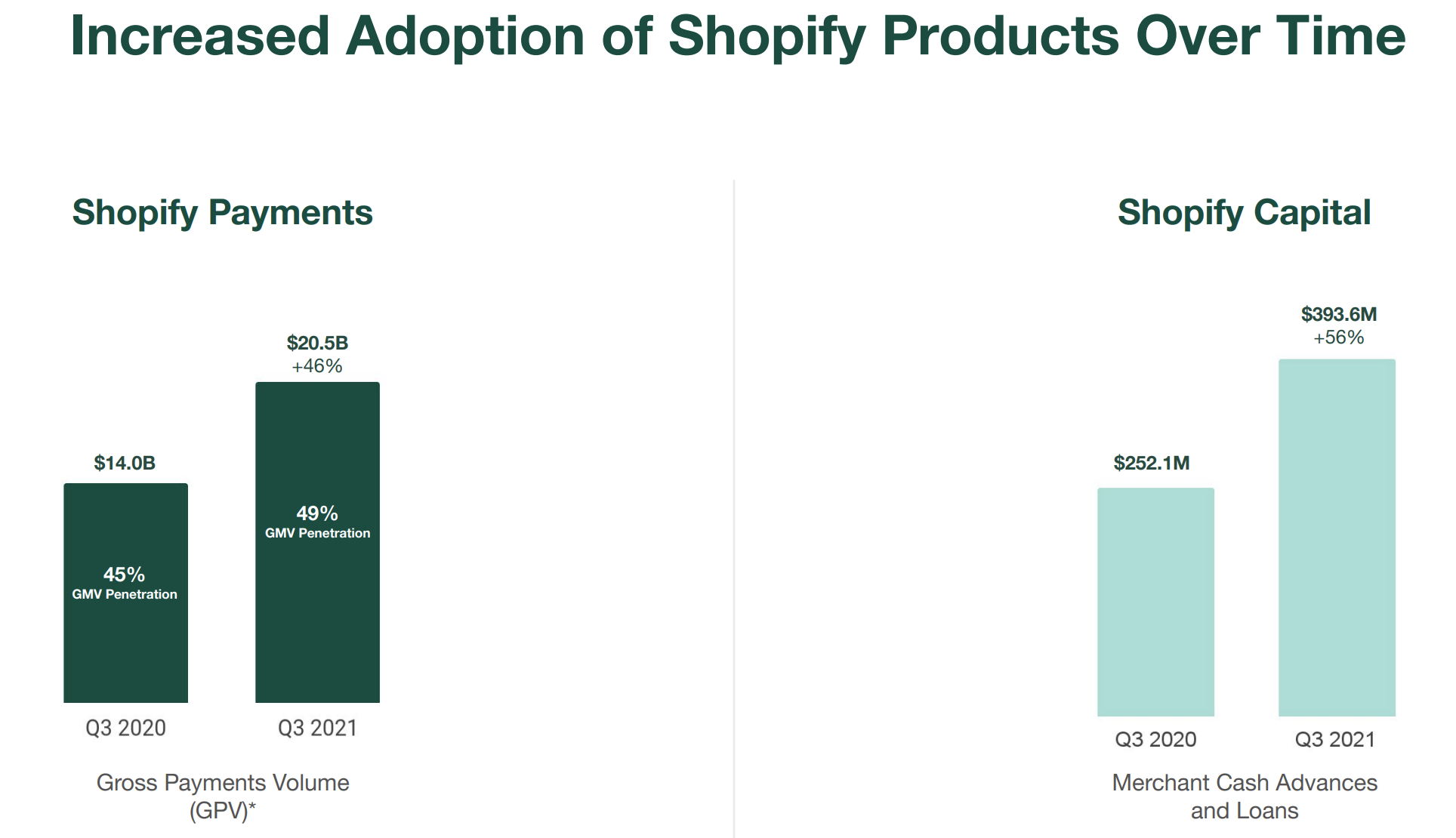

Shopify Capital Originated $393.6M in MCAs and Business Loans in Q3

October 28, 2021Shopify Capital, the funding arm of e-commerce giant Shopify, originated $393.6M in merchant cash advances and business loans in Q3, the company reported. That’s up from the $363M in the previous quarter.

Covid was a boon to Shopify Capital given its dependence on e-commerce businesses. Its 2020 funding volume was almost double that of 2019.

“Shopify Capital has grown to approximately $2.7 billion in cumulative capital funded since its launch in April 2016,” the company announced. The large volume and continued success has landed the Shopify Capital division in the company’s “core” bucket of “near-term initiatives” that will build the company for the long term, according to a presentation accompanying Q3 earnings.

Robinhood Posts Rough Q3

October 26, 2021 Robinhood revealed a steep $1.3B loss on Tuesday. Thought it was highly attributable to share-based compensation, several areas of their growth went into reverse. Transaction-based revenues, for example, were only $267M in Q3, a sharp drop from the $451M in Q2.

Robinhood revealed a steep $1.3B loss on Tuesday. Thought it was highly attributable to share-based compensation, several areas of their growth went into reverse. Transaction-based revenues, for example, were only $267M in Q3, a sharp drop from the $451M in Q2.

That’s not all. Assets Under Custody, Average Revenue Per User, and Monthly Active Users all shrank as well.

“This quarter was about developing more products and services for our customers, including crypto wallets,” said Vlad Tenev, CEO and Co-Founder of Robinhood Markets, in the company’s official statement. “More than one million people have joined our crypto wallets waitlist to date. With 24/7 live phone support, we believe that Robinhood is becoming the most trusted and intuitive platform for retail and crypto investors. And looking ahead, we’re committed to delivering tax-advantaged retirement accounts to help everyone invest for the long term.”

Networking, Data, and Innovation Dominate Money 20/20

October 26, 2021 It was not only a focus to sell, showcase, network, and collaborate that drove thousands of attendees to this year’s Money 20/20 in Las Vegas on Monday, it was also the desire to share what kind of innovation everyone has been up to.

It was not only a focus to sell, showcase, network, and collaborate that drove thousands of attendees to this year’s Money 20/20 in Las Vegas on Monday, it was also the desire to share what kind of innovation everyone has been up to.

“It’s great to be back, in person, in Vegas,” said Scarlett Sieber, Chief Strategy and Growth Officer for Money 20/20. After last year’s pandemic-induced cancellation, Sieber spoke about how her and her team have been working to make this the best show yet. “We’ve been researching, strategizing, and imagining what a refreshed Money 20/20 would feel like, and it’s great to see it alive.”

The event was mostly dominated by payments services, who all seemed to be competing with each other rather than networking, largely offering the same services with different branding. Coming in at a far second was cryptocurrency, and their effort to share the impact that their industry has had on all aspects of finance. In the speaking sessions throughout the day, almost every panel at least touched on the legitimization of cryptocurrency in the finance world.

In her first time at the event, Brittany Desposito, Senior Business Development Representative at Appian, an enterprise and workflow application building software, spoke about what her company gets out of sponsoring an event like Money 2020. “We get to learn lots of industry trends [while] trying to figure out what we can market more to fintech companies, and what they are looking for, and what challenges they’re facing,” said Despositio.

“This is a great place to sort of get a pulse of what’s going on, see the various interesting players, and what their [new] solutions are”, said Ani Narayan, a Product Lead at Modern Treasury, a payments operations platform. Narayan stressed the positive impact in-person meetings have on companies like his, giving his company the chance to add clients to their book of business that they would never have been able to prior. “It’s a great opportunity to meet people, potential customers, partners, that you could be working with or potentially could work with, so it’s just a great place to bring the entire community together.”

“It’s our first time here, and what we found out is that [Money 20/20] is a real business spot for every party in the industry,” said Erick Padilla, Head of Growth at DAPP, a company who claims to be building the most advanced payment “railway” in Mexico. Padilla spoke about what the value of a show like Money 20/20 can truly be worth to a company like his. “We can meet some of the people that we haven’t had a chance to meet before because we’ve been in different parts of the world, and now we get this opportunity to meet in person, to get to the decision makers we have been looking for.”

When asked about his company’s intention to return to an event of this size, Padilla not only said he would return, but that he would upgrade his ticket to make more of a presence at the event. “We’re going to get a booth next time,” said Padilla.

The show will continue on Tuesday, as companies will be able to have one last chance to possibly make the connection they came to Las Vegas hoping for.

deBanked Presents: The Broker NFT Collection

October 26, 2021Watch out CryptoPunks, deBanked has minted a limited edition set of its own Broker NFTs.

Drawing from the animated style popular in the NFT community, this collection of ten “brokers” is a diverse light-hearted tribute to the professionals in the business finance industry. Each broker in the collection has been individually minted on the ethereum blockchain.

The artwork was drawn by Cindy Recile and the NFTs minted via deBanked’s own ethereum smart contract. (See here on etherscan.)

The other news is that we’ll be giving some of these away for free. (stay tuned for those details!)

Today’s NFT market has things like pixelated punks and bored apes literally selling for millions of dollars.

A jpeg with no picture other than 4 words of text that say: “Fintech is Killing me,” is currently up for sale for more than $400, if that can be believed.

The act of minting an NFT cost Ethereum gas but if there is any particular thing you would like to see deBanked turn into an NFT, let us know and maybe we’ll make it happen! Email info@debanked.com.

Fintech Happy Hour Discussion Prioritizes Data, Innovation, and Potential

October 22, 2021 In celebration of New York Fintech week, Ocrolus and Codat hosted Thursday’s happy hour with a panel discussion on “the power of combined data”. Pete Lord, CEO of Codat and David Snitkof, Head of Analytics at Ocrolus, discussed how their respective companies are working to innovate the fintech space by harnessing how to most productively make use of their most valuable commodity—data.

In celebration of New York Fintech week, Ocrolus and Codat hosted Thursday’s happy hour with a panel discussion on “the power of combined data”. Pete Lord, CEO of Codat and David Snitkof, Head of Analytics at Ocrolus, discussed how their respective companies are working to innovate the fintech space by harnessing how to most productively make use of their most valuable commodity—data.

The event was open to those in the fintech space, but primarily served as a mixer and networking event. The panel had discussion topics, moderator questions, and an audience question-and-answer session.

After the event, Snitkof spoke about how the choices available to potential borrowers are so vast, that this vastness of funding sources may be creating a knowledge gap between borrowers and funders. Through fintech, Snitkof appears to believe this knowledge gap can be bridged.

“I think awareness is a really big deal where in many cases people think the only place they can go get a loan is their bank,” said Snitkof. “In fact, there are more lenders out there and they’re all different, which is the important thing. They all use different data, they all use different technology, they all might offer different types of products, and if you’re a borrower, it pays to do some learning.”

When speaking about fintech companies themselves, Snitkof stressed the need for a company to find their niche. “I think what fintech companies can do is really try to make clear how they’re different. The most successful fintech companies that I know of, at least the most exciting ones right now, are ones that don’t try to be everything to everyone.”

Codat, the main showcaser of the event, have people that are equally as excited about both their company and industry’s potential outlook.“I think fintech is just getting started,” said Lord, when asked about Codat’s role in innovating the fintech space. “[Our] role is in connecting the different systems that are used by small businesses that enable them to thrive and to be able to do more business.”

Lord spoke about the increase in speed of the logistical processes that his company creates by innovating antiquated data entry systems via the Codat platform. “[We] provide a layer of intelligence on top of the data that we make available to clients to allow them to get more value faster, and then provide a better experience using that to their small business customers.”

Codat employees also spoke about the state of fintech, along with their direct involvement in changing the way financial transactions occur across a vast array of industries and institutions.

“I think small business owners and people who work at large corporations or medium sized businesses are now expecting similar experiences [like] the financial services they use to power their everyday activities,” said Nick Codron, Codat’s Strategic Account Manager of North America. “All of these software companies are moving into financial services, there is a big play for being the [top] platform and the central business operating system.”

Other employees believe that it is not just a desire for business owners to integrate technology into the financial services space, but a game of catchup; hinting that fintech, as a community, is behind the eight-ball when it comes to the pace of innovation.

“I think there’s a lot of catching up the world needs to do in terms of digitizing financial services not just for small businesses, but for consumers and large corporations,” said Andrew Rho, who recently just transitioned to a Strategy Management position at Codat. “If you can have easy access to those products, services and design concepts and materials that help your dreams come true, that’s an e-commerce business right there.”

“In that sense, you see fintech touch everything,” said Rho.

Slava Rubin, Founder of Indiegogo, to Keynote Broker Fair 2021

October 22, 2021 Broker Fair announced that Slava Rubin will be its keynote speaker for its 2021 conference on December 6th in New York City.

Broker Fair announced that Slava Rubin will be its keynote speaker for its 2021 conference on December 6th in New York City.

REGISTER HERE FOR BROKER FAIR 2021

Who is Slava Rubin?

Slava Rubin is an entrepreneur and innovator in the fintech space for nearly 20 years. Slava built an alternative investment platform, a venture fund, an equity crowdfunding platform, a perks crowdfunding platform, and an angel investment portfolio. Slava is a founder of Vincent, a company which has developed the largest database of alternative investments (crypto to NFTs, trading cards to art, real estate to venture and debt) and is changing how people access them. He is also founder & managing partner at humbition, a $30M early-stage operators venture fund built by founders, for founders. Slava also founded Indiegogo, a company dedicated to empowering people from all over the world to make their ideas a reality. As CEO for over 10 years from inception in 2006, Slava grew Indiegogo from an idea to over 500,000 campaigns and more than $1B distributed around the world. While at Indiegogo, Slava launched one of the nation’s first equity crowdfunding businesses. Slava’s angel portfolio includes 4 unicorns – Carta, Hedera, GOAT, & Turo. He is also a founding advisor to multiple companies including Hedera Hashgraph – a top 60 blockchain protocol.

Prior to Indiegogo, Slava was a strategy consultant working on behalf of clients such as MasterCard, Goldman Sachs and FedEx. He is also the founder of “Music Against Myeloma,” a charity that raises funds and awareness for cancer research in partnership with the International Myeloma Foundation. Slava is currently a member of the board for NYSE traded (WSO) Watsco Inc., and privately held, Indiegogo.

Slava represented the crowdfunding industry at the White House during the signing of the JOBS Act under the Obama administration and has helped navigate bringing equity crowdfunding to the American public. He also pioneered security tokens in the United States – having been a catalyst for selling fractionalized ownership of the St. Regis hotel in Aspen using blockchain technology. He has made many TV appearances including being a regular guest commentator on CNBC. He has also been often quoted in NYTimes and Wall Street Journal.

Slava has received numerous awards including Fortune 40 under 40, Observer 20 Heros under 40, and the Wharton Young Leadership award for 2015.

Slava holds a B.S.E. from the Wharton School of Business

Q&A with Isaac Wagschal on One Percent Ventures’ Intentions to Transform MCA

October 21, 2021One Percent Ventures, a loaded name with implications depending on who reads it, is the latest small business funding company to enter the fray. No, it’s not funding for the one percent, but rather the numerical percentage the company would make off first-time clients with near-perfect performance. They’d make just one percent…

The concept, which caught the attention of deBanked, had to be explained in detail, especially when a merchant paying only $500 on a $50,000 advance was communicated as an example. Say what? The catch is in a rebate and the cost independent of the broker’s commission. Nevertheless, One Percent Ventures CEO Isaac Wagschal seems to be bringing in a new concept, one that was originally supposed to be 0%, he says, but he was already stuck with his company name. deBanked did a Q&A to find out exactly how it all works.

– The Editor

Q&A

Q (Adam Zaki): Why did you choose the name One Percent Ventures?

A (Isaac Wagschal): The original idea for One Percent Ventures wasn’t to be a funding company that gives one percent deals. Originally, we were going to provide branding and marketing services to small businesses who do not have any marketing, but can benefit from it. Our compensation was to be a one percent partnership in the company. Then a situation came my way where I was able to form a team of people with extensive knowledge and experience in the MCA space. I grabbed the opportunity and switched from marketing to funding small business.

We designed the product with a rebate that refunds basically the entire cost of the first advance. I realized that if we changed the rebate where instead of refunding 100% of the 1st advance factor cost, we keep 1%, I wouldn’t have to change the name and logo of the company. This is the reason our merchants are now paying one percent. If I had not already determined the name, the merchants would have been paying zero instead of one percent.

Q: What was the most difficult part of the shift from marketing to funding?

A: Shifting from marketing to funding was very difficult because of the nature of the market which existed at that time. That difficult transition forced the creation of our unique product, which includes rebates and payment-pauses. I looked into the mainstream MCA product in-depth, and realized that from a marketing point of view the product is flawed, and cannot be marketed properly. The more I scrutinized the MCA industry, I realized that the problems are not just from a marketing perspective. There are existential problems that need to be addressed, or they will eventually cause the demise of the industry altogether. Default rates are so high that mathematically the industry is forced to charge extremely high prices. This makes the product unmarketable to merchants who are not in the absolutely highest risk bracket.

I knew that unless we remade the product to be more attractive and marketable to a larger market share, the funding industry had no tangible room for expansion. Why would we want to get into this market space in the first place? As a team, we agreed that instead of hiring ISO-reps and underwriters, we would first hire accountants, actuaries, and data analysts.

We applied the same psychological principles used in marketing, where you try to predict and manipulate people’s reactions. By doing that, we were able to redesign the old MCA product. We introduced a rebate system that gives the merchant an opportunity to potentially only pay a $500.00 factor cost on a $50k advance. In this way, we expanded the current market share, and turned it into a hot product. I hear from ISOs on a daily basis who recontacted old unsuccessful leads, and turned them into deals after they presented the OPV-rebate and payment-pause-award system. This proved that the OPV product is expanding the market share.

Q: What are your thoughts about the market share in MCA?

A: The current market share consists of the absolute highest risk merchants who are willing to pay such high prices. It is becoming harder and harder to maintain deal flow. This has forced the industry to slowly keep raising the standard with respect to how many positions we are willing to accept. If nothing happens, we will soon find ourselves talking about 10th and 15th positions. This is certainly not sustainable, and puts an amazing amount of stress on the ISOs who are working tirelessly to maintain deal flow. They see it all happening, but feel helpless because at the end of the day, they can only present a product that a funder puts on the table. The tiny market of willing and able merchants is also a source of stress, and a key factor to the mistrust that is largely present between ISOs and funders.

Q: What are your thoughts on a relationship with the ISOs and funders?

A: Let’s face it, the way the current ISO-Funder relationship is set up scientifically creates a conflict of interest. It is simple math – when a funder loses a renewal that carried a potential profit of 50k and thinks that the deal could have happened if not for the 14 points that is reserved for the ISO, there is a natural conflict of interest. You can be honest with your ISOs and even give Rolexes and call them your partners on paper, but the spreadsheet still calculates a conflict of interest at the end. The lavish gifts are nice, but they do not eliminate the scientific conflict of interest.

We have corrected this fundamental problem by designing our business model so that our ISOs are genuine partners. This too is simple math – when a funder’s product is designed to issue an unheard-of large rebate, and 3rd party costs are deducted from the final rebate amount, the merchant will obviously be super happy because of the astronomic refund. More importantly, by using this model, the conflict of interests between ISO and funder is erased because mathematically the merchant paid the commission, not the funder!

Q: How does OPV make money? How do merchants qualify for all of your incentives? What are these incentives?

A: Let me first answer the latter part and explain how our product works and then I’ll come back to answer how we make money.

Our typical product is a ninety-day term at 1.49 sell rate. At mid-term, if the merchant didn’t miss any payments, they are eligible for an add-on, largely known as a renewal. At this phase, we begin to issue an OPV-Pause award after each cycle of four consecutive successfully completed payments. The pause awards can be submitted smoothly on our automated online system either one at a time, or they can be saved and initiate a pause for an entire week. After the final payment, if the merchant didn’t miss more than three payments, excluding the pauses, we refund the entire factor cost of the first advance except for 3rd party fees, processing fees, and 1% of the advance, which gives us only $500 profit on a 50k advance.

Every merchant that qualifies for funding, automatically qualifies for all the incentives. The OPV funding model is actually designed to perform better when more merchants actually receive the rebate. Why? Because that also means there has been a drop in the default rates. If every merchant was to qualify for the rebate, it would mean we had a zero percent default rate, which would allow us to make a healthy return, even if we made profit only on the 2nd advance.

This is precisely the reason we added the OPV-Pause awards. It is in our best interest to keep the merchant motivated to stay current on their payments, in order to qualify for the rebate. We even added a condition that in the event a merchant doesn’t have an unused pause award, they can purchase an OPV-Pause for 20% the daily payment. The goal must be to lower default rates so that we can lower the end cost. In this way we can expand the market share and keep the MCA industry alive. The OPV product is designed to do just that.

Q: What are your immediate goals for OPV? How about long term?

A: Phase I was designing the product and building the platform. Now in phase II, we plan to fund deals for at least a year before making any significant changes. We want to build relationships and earn trust by being transparent and honest, even when it hurts. At phase III we will analyze the data and make tweaks we deem necessary. At phase IV, given that the canary returned from the coal mine, we will share our intelligence, and license the OPV platform to reputable funders throughout the MCA industry.

Q: What is your outlook on the future of the non-bank small business funding/lending sphere?

A: In an effort to truly make a constructive change towards preserving the MCA industry, I will speak openly about the elephant in the room. We are all aware of the unfavorable new laws and regulations that constantly threaten our existence. As long as there are politicians who need to win elections, they will be on the hunt for “do-good projects.” There will always be a lobbyist that is looking for deal-flow, who is willing to provide the perfect “do-good” project. One of those will be – “Let’s save the poor merchant from the greedy funder.” The politician can only succeed because the nature of the MCA industry is such that our funders share only the good news. The bad news is confidential, so there is a stigma of excess profit in the MCA sphere. If we can successfully change that stigma, then we will be a thriving industry for many years to come.