Archive for 2019

Salaries For All, Even For Gig Workers

October 16, 2019 “If we don’t solve the problems, there’s just a nightmare coming.”

“If we don’t solve the problems, there’s just a nightmare coming.”

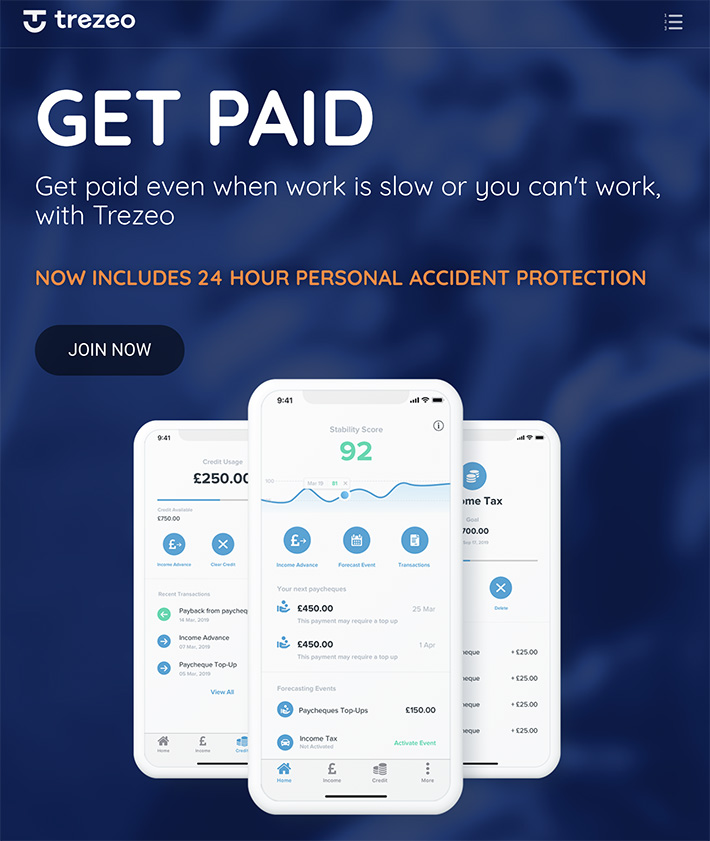

This is how Trezeo’s CEO and Co-founder Garrett Cassidy views the work that he and his company are doing. Created in 2016 with the aim to provide support to self-employed people via income smoothing, Trezeo offers workers whose income streams may be irregular the opportunity to have structured and regular paydays similar to those who earn a salary. And with the number of self-employed in the UK currently at approximately five million, as well as projections showing that the majority of US workers will be freelancers by 2027, the company sees its efforts as essential to solving future problems. “There’s a lot of noise around the gig economy,” Cassidy asserted. “But the world is moving that way and we’re very much like ‘that’s fine, you can push back all you want, it’s going that way and we need to create the services that will work for these people.’”

The way it works is that Trezeo serves as an alternative lender, offering regularly paid funds to the customer’s account in exchange for their income that comes in at a later date. A major difference between it and other alternative lenders though is that Trezeo does not charge interest on these advances, instead collecting its revenue from a weekly membership fee of £3.

“We want to allow them to build their own financial resilience and also start looking a bit more useful for traditional financial institutions to engage with,” Cassidy explained. “Our ultimate vision is if you choose to be freelance or self-employed why should you cut yourself off from financial security, why should you trade flexibility for security, and, therefore, that’s the whole ethos of the income smoothing.”

Beyond this service Trezeo has plans to include additional features, such as an income verification system that would help workers be approved for large loans, like mortgages, from banks; as well as an opt-in pension, where instead of being committed to paying a fixed amount each pay cheque, customers could pay 5% of their total income for that period. Trezeo has already gotten the ball rolling with such expansions with the release of its personal accident and disabilities insurance, which covers customers for £300 per week for six months in the case that they are unable to work.

While it may sound as if self-employed and freelance workers are signing up for Trezeo to be their surrogate employer, Cassidy is quick to emphasize that this is instead a new system built to reflect the opportunities presented by technology, distant but reminiscent of the employment structures that came before.

“We’re trying to recreate [the structure] in a way so that a self-employed person controls it and over time can decide what they want … We’re not trying to make them employees, we’re very careful about that, but we’re trying to make it an employee-like experience for them so that they can very easily manage their finances and see them like an employee traditionally would … Platforms are making it easier for people to take the choice of flexibility.”

Speaking to Cassidy in Trezeo’s Irish office in the National Digital Research Centre, an early stage investor in tech companies, we’re snuggly located close by St. James’s Gate Brewery, where the cobbled streets are filled with the nutty and barley-laden smell of Guinness being brewed.

From here is where the development team operates, whereas the risk, sales, and marketing teams work from their London office, with the UK being their only market at this time. However Cassidy assured me that the company is looking interestedly abroad to Western Europe and America with plans to expand.

“This is a very big niche globally,” Cassidy remarked. “And as we’ve gone along, we’ve realized how much of an impact we can have.”

BFS Capital Launches Canadian Tech Hub

October 16, 2019 Small business lender BFS Capital is making an expansion push with the creation of a new data science and engineering hub in Toronto. BFS, which serves customers in a trifecta of jurisdictions that in addition to Canada includes the U.S. and the UK, has undergone a technological transformation that includes building out a tech team for the next generation of the firm’s products.

Small business lender BFS Capital is making an expansion push with the creation of a new data science and engineering hub in Toronto. BFS, which serves customers in a trifecta of jurisdictions that in addition to Canada includes the U.S. and the UK, has undergone a technological transformation that includes building out a tech team for the next generation of the firm’s products.

BFS Capital CEO Mark Ruddock took some time to discuss the Toronto expansion with deBanked.

“We have an ambitious roadmap and plan to innovate quickly,” said Ruddock, “As a result, we had to ask ourselves, where could we best do this? We looked at cities across North America with strong tech and data science talent, and which were millennial friendly. We were frankly quite surprised by Toronto. Something fundamental is happening in Toronto – it’s fast becoming a leading city for data science, AI, and mobile app development in North America.”

Indeed, deBanked hosted its inaugural Canadian event in Toronto this past July after keeping an eye on its burgeoning fintech scene there for years.

“We are seeing a fundamental transformation happening in our customer base, from a less digitally savvy generation of entrepreneurs willing to accept the traditional financial products to a demanding, digital first generation, seeking new financial solutions,” said Ruddock, pointing to a two-pronged approach of real-time algorithmic decisioning and a mobile-first user design. “The intersection of those two things is the tipping point for small business financial services for the next while,” he added.

BFS Capital is finding that the younger generation is well equipped with technological skillsets, noted Ruddock, pointing to the Universty of Toronto and University of Waterloo as two of the best schools in North America for tech talent.

National Business Capital & Services Expands into Cannabis Funding with CannaBusiness Financing Solution

October 15, 2019 Today National Business Capital & Services (NBC&S) announced it has begun serving cannabis companies. Through its new program, CannaBusiness Financing Solution, NBC&S is now accepting applications for loans starting at a minimum of $10,000 from firms in the industry that are over one year old.

Today National Business Capital & Services (NBC&S) announced it has begun serving cannabis companies. Through its new program, CannaBusiness Financing Solution, NBC&S is now accepting applications for loans starting at a minimum of $10,000 from firms in the industry that are over one year old.

“The CannaBusiness Financial Solution will allow business owners to seamlessly obtain the capital they need, and allocate funding toward either hiring new employees, purchasing inventory, marketing strategies, or any other business need right away, without government regulations hindering growth opportunities or having to give up equity,” explained NBC&S President Joseph Camberato. “We’re not a bank and the lenders we work with aren’t banks either, so it falls into a different area of commercial lending.”

CannaBusiness is available in the 33 states where cannabis is legal, be it for medicinal or recreational uses, as well as in Canada.

“It’s a rapidly growing space, no pun intended,” joked Camberato when asked about the differences in funding cannabis companies compared to the industries NBC&S has served in its 12 years of business. “It would still be underwritten, just like one of our normal businesses. But we’re definitely going to want to know a little bit more about the business and understand what exactly they’re doing, how they’re operating, and exactly what are they’re focused on.” They’ll also examine if the business is in compliance with state laws. Qualifying cannabis companies must be in business for at least 1 year, with a minimum of $10K in monthly revenue. There is no minimum FICO score requirement.

While it’s not the first funder for cannabis companies, NBC&S views the move as a step in the right direction to “get ahead of the curve” according to Camberato. “We’re living through a modern-day prohibition, I think in 20 years we’ll look back on it and talk about it with our grandchildren and be like, ‘wow’ … I don’t think people realize how big of a deal this really is, but it is a business and it is another industry that has bloomed in front of us, again no pun intended. I think it’s fascinating that we get to witness this and that we’re really at the forefront of it and helping folks get the funds they need to grow.”

While it’s not the first funder for cannabis companies, NBC&S views the move as a step in the right direction to “get ahead of the curve” according to Camberato. “We’re living through a modern-day prohibition, I think in 20 years we’ll look back on it and talk about it with our grandchildren and be like, ‘wow’ … I don’t think people realize how big of a deal this really is, but it is a business and it is another industry that has bloomed in front of us, again no pun intended. I think it’s fascinating that we get to witness this and that we’re really at the forefront of it and helping folks get the funds they need to grow.”

Jumping off from the politically charged word of ‘prohibition,’ NBC&S’ Vice President of Marketing, T.J. Muro, noted that he believed cannabis legislation to be one of the few issues that can be bipartisan, saying, “Out of everything today in our political climate, I think it’s the one thing that has unified people in the political parties. The liberal side appreciates the cultural influence and significance there, and then on the more conservative side it’s the tax revenue.”

The upcoming Senate vote on the SAFE Banking Act will put this theory to the test. The bill, which would allow the cannabis industry wider access to banking, has already passed the House.

CAN Capital Announces New CCO

October 15, 2019We are proud to announce that we have hired David Lafferty as CAN Capital’s new Chief Credit Officer (CCO.) Lafferty brings his expertise in commercial lending, business development, operational planning and profit & loss management to the CAN Capital team.

Lafferty has over twenty years of proven experience providing financial services to small businesses. He is the former Vice President of Capital Markets and Credit and Risk Management at Marlin Business Bank. In that role, he has assisted small businesses in obtaining the capital they need to operate and grow, with a special focus on helping businesses finance the lease or purchase of equipment. Lafferty is a graduate of Pennsylvania State University, and a member of the Equipment Leasing and Financing Association (ELFA) Small Ticket Advisory Council.

“I have focused my entire career on serving the small business owner as they are the backbone of the United States economy. Being given the opportunity to join this team in a time when the company is experiencing rapid growth and gaining significant market share is extremely exciting. I am really looking forward to joining an already very talented workforce as we take CAN Capital to the next level,” said Lafferty.

Ed Siciliano, CAN’s CEO, had this to say about the new hire: “I’m very excited to welcome Dave to CAN Capital. He will be joining a strong group of talented people focused on Risk and Credit Underwriting and applying his deep experience in small business lending to calibrate CAN’s 20-year proven credit models. We all welcome Dave and feel fortunate to have him join.”

A Philadelphia native who now resides in New Jersey, Lafferty is the proud father of twin sons. When he isn’t helping small businesses succeed, you’ll find Lafferty golfing or riding motorcycles, or on the water boating and fishing in Punta Gorda Isles, Florida.

Please join us in welcoming new CCO David Lafferty, who, along with our dedicated group of CAN Capital team members, is ready to support our mission of helping every small business succeed.

About CAN Capital

CAN Capital, Inc., established in 1998, is the pioneer in alternative small business finance, having provided access to over $7 billion in capital for over 81,000 small businesses in a wide range of locations and different business types. As a technology powered financial services provider, CAN Capital uses innovative and proprietary risk models combined with daily performance data to evaluate business performance and facilitate access to capital for entrepreneurs in a fast and efficient way.

CAN Capital, Inc. makes capital available to businesses through business loans made by WebBank, member FDIC, and through Merchant Cash Advances made by CAN Capital’s subsidiary CAN Capital Merchant Services, Inc. ©2019 CAN Capital. All rights reserved

Media Contact: Carey Kirk, 678-858-6911, ckirk@cancapital.com

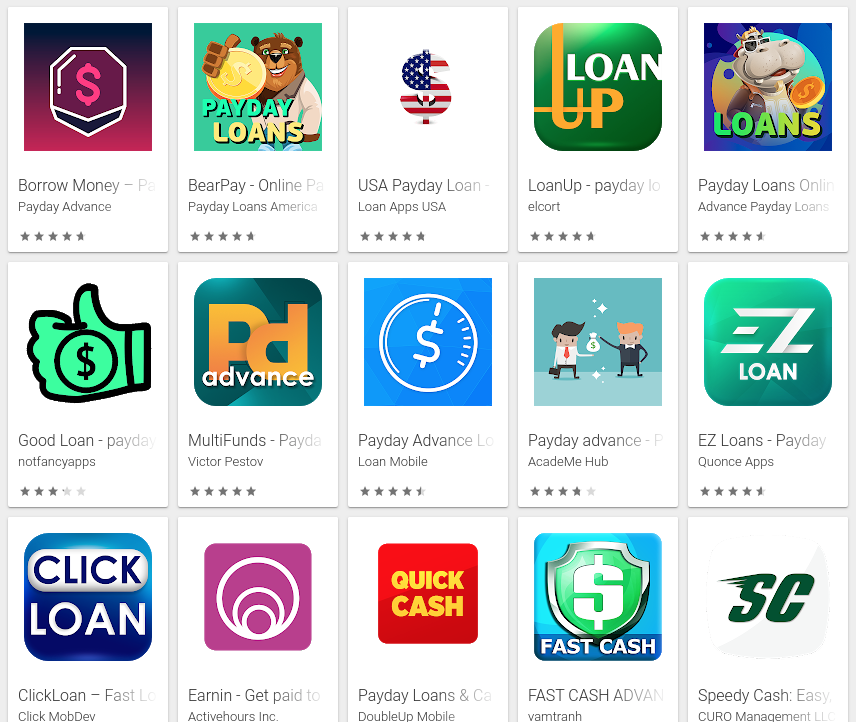

Google Bans Loan Apps From App Store If Personal Loan Offers Exceed 36% APR

October 12, 2019

Google is implementing new rules for consumer lenders who have apps in the Google Play app store. And they’re pretty strict. If a lender offers loans that exceed 36% APR, their app will be banned. If the repayment period of the loan is 60-days or less, the app will be banned.

Google is implementing new rules for consumer lenders who have apps in the Google Play app store. And they’re pretty strict. If a lender offers loans that exceed 36% APR, their app will be banned. If the repayment period of the loan is 60-days or less, the app will be banned.

It doesn’t matter what lenders call these loans, at least according to Google’s updated policy. “Peer-to-peer loans” were used as just one example of a loan category subject to the new rules.

Despite the new rules and a WSJ story announcing that payday loans had been shut out of the platform, deBanked determined that hundreds of payday loan apps are still available for download. This includes Nas-backed Earnin which is under investigation by regulators in multiple states.

Google banned payday loan ads from its search result pages in 2016. The move was viewed in some circles as hypocritical since Google’s VC arm, Google Ventures, had just invested in a payday lender (LendUp) that offered loans in excess of 400% APR. However, LendUp was also affected by the ban, a move that LendUp’s then-CEO Sasha Orloff embraced. Orloff blogged about the irony, writing, “If effectively enforced, Google’s ban will push the payday loan marketing competition away from ads and toward natural search, where safer alternatives with quality content can shine.”

Perhaps Google aims to achieve a similar objective with its app store.

The full text of Google’s new personal loan rule for its app store is below:

We define personal loans as lending money from one individual, organization, or entity to an individual consumer on a nonrecurring basis, not for the purpose of financing purchase of a fixed asset or education. Personal loan consumers require information about the quality, features, fees, risks, and benefits of loan products in order to make informed decisions about whether to undertake the loan.

- Examples: Personal loans, payday loans, peer-to-peer loans, title loans

- Not included: Mortgages, car loans, student loans, revolving lines of credit (such as credit cards, personal lines of credit)

Apps for personal loans must disclose the following information in the app metadata:

- Minimum and maximum period for repayment

- Maximum Annual Percentage Rate (APR), which generally includes interest rate plus fees and other costs for a year, or similar other rate calculated consistently with local law

- A representative example of the total cost of the loan, including all applicable fees

We do not allow apps that promote personal loans which require repayment in full in 60 days or less from the date the loan is issued (we refer to these as “short-term personal loans”). This policy applies to apps which offer loans directly, lead generators, and those who connect consumers with third-party lenders.

High APR personal loans

In the United States, we do not allow apps for personal loans where the Annual Percentage Rate (APR) is 36% or higher. Apps for personal loans in the United States must display their maximum APR, calculated consistently with the Truth in Lending Act (TILA).

This policy applies to apps which offer loans directly, lead generators, and those who connect consumers with third-party lenders.

New York Attorney General Secures Judgment Against Cardis Enterprises International

October 11, 2019 New York Attorney General Letitia James announced today that she had secured default judgments against numerous entities and individuals involved in a $30 million fraud.

New York Attorney General Letitia James announced today that she had secured default judgments against numerous entities and individuals involved in a $30 million fraud.

In December 2018, the New York Attorney General’s Office filed suit against Cardis and company personnel Aaron Fischman, Stephen Brown, Steven Hoffman, and Seth Rosenblatt for participating in the fraudulent marketing of Cardis to investors. The complaint further alleged that, while Cardis was raising significant investor funds, Fischman was fraudulently diverting much of the proceeds to enrich himself, family members, and his favored charities.

Default judgments were entered against Cardis Enterprises International N.V., Cardis Enterprises International (U.S.A.) Inc., Cardis Enterprises International B.V., and Chosen Israel LLC, along with several individuals related to Aaron Fischman as relief defendants.

“The case remains ongoing with several motions pending,” the AG wrote in a public statement, “including a motion for leave to amend the complaint to re-plead claims against Stephen Brown (who was previously dismissed from the case) and the remaining defendants.”

The Broker: Funding Businesses The Irish Way

October 10, 2019 I’m sitting in the lobby of The Marker Hotel, a 5-star 7-story property on the edge of Dublin’s Grand Canal Dock. Here in Ireland’s major tech hub, I’m waiting for a self-identified corporate finance broker by the name of Rupert Hogan, the managing director of BusinessLoans.ie. Outside of our email exchanges, I don’t really know what to expect. I’ve met brokers from the US, Canada, Mexico, UK, and Hong Kong, but never Ireland.

I’m sitting in the lobby of The Marker Hotel, a 5-star 7-story property on the edge of Dublin’s Grand Canal Dock. Here in Ireland’s major tech hub, I’m waiting for a self-identified corporate finance broker by the name of Rupert Hogan, the managing director of BusinessLoans.ie. Outside of our email exchanges, I don’t really know what to expect. I’ve met brokers from the US, Canada, Mexico, UK, and Hong Kong, but never Ireland.

When he arrives, he doesn’t disappoint. Hogan is full of energy and enthusiasm. He has a natural charisma and friendly manner that’s well-suited for a relationship-based business. It just so happens that SME finance in Ireland is still heavily reliant on person-to-person contact and Hogan is at the forefront of helping potential borrowers look beyond the bank for their financing needs.

SMEs are looking for speed and ease in the loan process, Hogan says. Historically, business owners would call on their bank for financing, invoking the sanctity and reliability of decades-old personal relationships, but Hogan explains that relationships between SMEs and banks just aren’t what they used to be. “[SMEs] feel like they’re going to get the runaround,” he says.

That’s where he comes in. And it could be any kind of business, he explains. Hogan jumps from a call with an import/export business to one in retail, followed by one with an agricultural equipment company. He has to understand a bit about them all no matter what it is, to figure out a proper financial solution. BusinessLoans.ie doesn’t charge for their service but they do receive a commission from the financial company if a deal closes.

That’s where he comes in. And it could be any kind of business, he explains. Hogan jumps from a call with an import/export business to one in retail, followed by one with an agricultural equipment company. He has to understand a bit about them all no matter what it is, to figure out a proper financial solution. BusinessLoans.ie doesn’t charge for their service but they do receive a commission from the financial company if a deal closes.

“Corporate” finance may evoke images of big city corporations engaged in international commerce but Hogan’s company can connect SMEs with as little as €5,000 through an unsecured business loan or merchant cash advance. Invoice Financing, leasing, and trade finance are also tools at his disposal. It’s not all small, however, as he hands me a rate sheet for one lender that will go up to €25M. Interest rates on these products when compared with their American and UK brethren are quite reasonable, and suggest also that the target clientele is not subprime.

As we sit there drinking coffee, Americano style in my honor, an executive for a local SME lender happens to spot him while passing by. After they exchange pleasantries, Hogan explains to me that he submits deals to that lender through their online broker portal. And so I ask him if doing everything online has become the standard in Ireland.

“It’s getting there,” he says, while acknowledging there’s still a ways to go with the population that’s conditioned to handling their financial dealings offline. The company’s domain name is perhaps perfectly positioned to capture that transitioning audience. When businesses decide to look for a loan online, he explains, “I hope they go to BusinessLoans.ie”

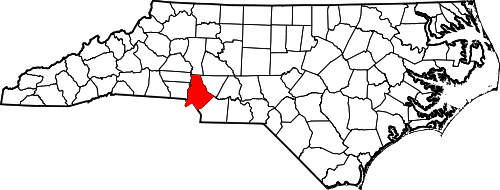

Mecklenburg County Launches Small Business Loan Program

October 10, 2019 This week Mecklenburg County, North Carolina launched its Small Business Loan Program. Offering up to $75,000 dollars with fixed 2% interest rates, the county has appropriated $2.75 million to fund the program for its first year. Being managed by the Carolina Small Business Development Fund, the CSBDF will have the authority to sign off on which small businesses will receive loans.

This week Mecklenburg County, North Carolina launched its Small Business Loan Program. Offering up to $75,000 dollars with fixed 2% interest rates, the county has appropriated $2.75 million to fund the program for its first year. Being managed by the Carolina Small Business Development Fund, the CSBDF will have the authority to sign off on which small businesses will receive loans.

Split into two tiers, one for businesses operating for less than two years or who are without revenue and the other for companies operating for at least two years, both tiers offer a micro loan and a conventional business loan. The former of these being a loan of less than $50,000 and the latter being one of over $50,000. Included with these loans are entrepreneurship training and mentoring.

Among the stipulations and requirements for the loans are that applicants have an annual revenue under $1 million and that they should not have any open tax liens, unpaid judgments, or principal and business bankruptcy in the previous five years. This risk-adverseness may be the definitive difference between such publicly provided funds and their private counterparts.

Accumulatively, the CSBDF has invested $59.7 million into programs such as these so far, with 735 loans having been authorized thus far.