Small Business

EIDL Applicants Still Waiting for Funds as Deadline Approaches

December 16, 2021 There is a major pileup of applicants waiting to hear back from the SBA regarding EIDL applications, according to Iron Capital Equities, a fintech firm who owns websites that help businesses through the EIDL application process. According to a press release by the company, many applicants who have not yet received funding seem to believe they’ve been ghosted by the SBA.

There is a major pileup of applicants waiting to hear back from the SBA regarding EIDL applications, according to Iron Capital Equities, a fintech firm who owns websites that help businesses through the EIDL application process. According to a press release by the company, many applicants who have not yet received funding seem to believe they’ve been ghosted by the SBA.

The EIDL deadline to file an application is December 31.

“90% (9 out of 10) of our 400 client applicants are still in limbo, with no update regarding the status of the funds,” states co-founder Matthew Elling. “The short-term economic outlook from small businesses is dim, so these funds are highly sought after.”

Elling insisted that he is in constant contact with his customers, and says his company is doing everything they can to service these clients who are playing the waiting game.

“Even though we are a financial technology company, we still ‘talk’ with our customers,” Elling continued. “We understand their struggles in a post COVID economic environment, we have provided them with advice on the SBA assistance like EIDL and the two PPP rounds for payroll and business expense assistance during and after the government-imposed lockdowns.”

EIDL loans were a beacon of hope for many businesses struggling to survive in the pandemic. This type of government funding isn’t a grant, and needs to be paid back by the merchant at a term of 30 years at 3.75% annual interest.

Was That Loan Forgiven? The Tax Man Cometh

March 10, 2021 With tax season upon us, the events of 2020 will soon be reviewed and evaluated by everyone’s best friend, the IRS. Lenders that offered debt forgiveness might have done a favor to distressed borrowers in 2020, but a consequence of that courtesy is that the borrowers’ forgiven debt might be taxable.

With tax season upon us, the events of 2020 will soon be reviewed and evaluated by everyone’s best friend, the IRS. Lenders that offered debt forgiveness might have done a favor to distressed borrowers in 2020, but a consequence of that courtesy is that the borrowers’ forgiven debt might be taxable.

This is as good a time as ever to review a report prepared by Grassi Advisors & Accountants whether you are a lender that forgave debt or a borrower that had debt forgiven.

“This issue was noticed early last year,” said deBanked President Sean Murray, “but at the time everyone was so focused on PPP forgiveness, the EIDL program, and government stimulus, that I think the potential consequences of lenders forgiving non-PPP debt for their borrowers were lost in the shuffle. Imagine you’re a borrower that had $100,000 of non-PPP debt forgiven last year and you’re only now about to learn that the IRS may classify that as income. Or worse yet, you don’t even realize it and are told that later on during an audit.”

In May 2020, deBanked labelled this as a hidden tax time bomb that was set to detonate in 2021. And now here we are.

Failing Main Street NY

December 21, 2020 During the election, we heard candidates on both sides to toss around the phrase “small businesses are the backbone of the American economy.” A staple of exhausted political rhetoric, made trite despite its truth because for many politicians it’s a talking point, not a platform. We must move from rhetoric to action. To do so, America’s political leaders need a real understanding of what small businesses need—and what they don’t.

During the election, we heard candidates on both sides to toss around the phrase “small businesses are the backbone of the American economy.” A staple of exhausted political rhetoric, made trite despite its truth because for many politicians it’s a talking point, not a platform. We must move from rhetoric to action. To do so, America’s political leaders need a real understanding of what small businesses need—and what they don’t.

The struggle between understanding and posturing is on display right now in Albany. While small business owners struggle to open their doors, the legislature passed a so-called “truth in lending for small business” bill that claims to provide more disclosure to business owners seeking financing. Led by Senator Kevin Thomas and Assemblyman Ken Zebrowski the bill is currently pending before Governor Cuomo. The legislators recently authored an op-ed that further demonstrates their failure to recognize that the innocuously named bill is rife with faults and lacks a competent grasp of small business issues. The critical blind spots in the bill’s design threatens billions of dollars in capital leaving New York—a failing small businesses owners can scarcely afford at such a difficult time.

Yet, rather than incentivizing finance providers to stay in New York, the legislature is focused on complex disclosures that lack real meaning or understanding to small business owners. Senator Thomas opined on the Senate floor “… the reason I introduced this bill is because people don’t use standard terminology.” Interestingly, this bill creates several new terms and metrics that would be required to be disclosed that have never been used before in finance. Terms like “double-dipping” and new confusing metrics that even the CFPB under President Obama labeled as “confusing and misleading” to consumers. This bill’s fatal flaw is that it has confused information volume with transparency, somethings a recent study proved would harm small business owners.

Even Senator Thomas acknowledged the legislation’s myriad of problems while still encouraging its passage. In his colloquy with Senator George Borrello on the Senate floor, right before he called New York small business owners “unsophisticated,” he mentioned how his bill had “many issues” that he “hoped” would be worked out before implementation. Hope is not a strategy and it won’t help small business owners obtain the financing they need to stay in businesses. Advancing legislation that would limit options for entrepreneurs working to stay in businesses during a pandemic that has crippled the New York economy represents a reprehensible failure of leadership.

Minority-owned businesses have faced a disproportionate economic impact from the pandemic. According to the Fed, Black-owned businesses have declined by 41% since February, compared to only 17% of white owned businesses. Further, the Paycheck Protection Program (PPP), the federal government’s signature relief program for small businesses, has left significant coverage gaps: these loans reached only 20% of eligible firms in states with the highest densities of minority-owned firms, and in counties with the densest minority-owned business activity, coverage rates were typically lower than 20%. Specific to New York, only 7% of firms in the Bronx and 11% in Queens received PPP loans. Moreover, less than 10% of minority-owned businesses have a traditional banking relationship—something that was initially required to have access to the PPP.

The lack of cogency and lazy approach to this legislation is a disservice to the hard-working entrepreneurs who continue to open their businesses while facing daily economic uncertainty. Governor Cuomo has worked tirelessly to continue to provide economic relief to both businesses and consumers—removing billions in financing for small businesses will only hinder this effort. New York can do better.

Steve Denis

Executive Director

Small Business Finance Association

Merchant Indicted For Sending Fake Bank Statements to Online Lenders

December 7, 2020 On December 17, 2018, the owner of a mexican restaurant in Springfield, Illinois, is alleged to have submitted altered bank statements to National Funding, Inc as part of a loan application to obtain $35,000. What he got in return was an indictment by a federal grand jury.

On December 17, 2018, the owner of a mexican restaurant in Springfield, Illinois, is alleged to have submitted altered bank statements to National Funding, Inc as part of a loan application to obtain $35,000. What he got in return was an indictment by a federal grand jury.

On Dec 2, 2020, the US District Court for the Central District of Illinois unveiled a seven-count indictment against Omar Hernandez-Lopez. Hernandez-Lopez is the owner of El Tapatio De Jalisco Inc DBA La Fiesta Grande.

Prosecutors say Hernandez-Lopez sent doctored PNC bank statements to two lenders, National Funding and Loan Depot in multiple instances. The actual charge is that the defendant knowingly made a false statement for the purpose of influencing the action of a lender in connection with a loan application.

Apparently, no falsehood is too small. For example, in one count the defendant is alleged to have changed a monthly ending bank statement balance of negative $72.91 to positive $131.90, a difference of $204.81. He is also said to have obscured the amount incurred in overdraft fees.

The penalty if found guilty on any one count? Up to 30 years in prison.

Prosecutors cite Title 18, United States Code,§ 1014.

Defendant is innocent until proven guilty. A copy of the indictment can be viewed here.

Fed Lowers Minimum Main Street Lending Program Loan to $100,000: Too Little, Too Late?

November 8, 2020 “$100,000, we can make that work,” said Ryan Metcalf, head of Public Policy Affairs at Funding Circle. “But we can help a lot more small business if it was $50,000.”

“$100,000, we can make that work,” said Ryan Metcalf, head of Public Policy Affairs at Funding Circle. “But we can help a lot more small business if it was $50,000.”

Metcalf was referring to a recent change in the minimum loan amount in the Main Street Lending Program (MSLP.) Just recently, the Federal Reserve lowered the minimum loan amount for the MSLP for a third time, to $100,000. The change was intended to broaden the underused Cares Act aid facility but it might not be enough.

Though changing the program days before, at a press briefing Thursday Fed chair Jerome Powell said SMB aid projects like PPP and the MSLP were up to the gridlocked House and Senate.

“The Fed cannot grant money to particular beneficiaries; we can only create programs or facilities to make loans that will be repaid,” Powell said. “Elected officials have the power to tax and spend, and to make decisions about where we as the society should direct our collective resources.”

Despite Powell’s talk of inaction in the face of an undecided congress, Metcalf said the Fed’s actions have proved that changes can be made to existing programs. Metcalf has been fighting for changes to MSLP for months on behalf of the small business lending community, he says.

In July, Metcalf, in partnership with the Innovative Lending Platform Association and Marketplace Lending Association, wrote a letter to the fed to argue for changes to the MSLP.

The letter argued that the Cares Act made non-depository finech lenders eligible to participate in PPP lending. Though these lenders saved millions of jobs, they were not allowed to lend through the MSLP facility.

Even if they could, the minimum loan size was still too large for “main street” American businesses that needed capital. The letter advocated for a lower minimum of $50,000, allow lenders that were approved for PPP to lend in the MSLP, and create a Special Purpose Vehicle for fintechs.

Metcalf said the Fed has only responded, “that is not under consideration.”

So far, 400 borrowers have taken out $3.7 billion in loans, of the $600 billion allocated. The program offers Fed backed five-year loans with differed principal and interest payments and minimal rates. With the facility’s deadline approaching Dec 31 and no changes in sight, Metcalf said the program’s vultures are circling.

If new aid, revisions, or at least an extension is not passed by when the government is funded Dec 11, Metcalf said the program might be finished.

Back in September, Powell testified before Congress that lowering the minimum any further wouldn’t change the adoption rate.

“We have very little demand below a million, as I told the chair a while back,” Powell said. “We’re not seeing demand for very small loans. And that’s really because the nature of the facility and the things you’ve got to do to qualify, it tends to be larger sized businesses.”

Mnuchin has consistently argued that grant programs like PPP would most benefit smaller firms. Metcalf said this was only the case because the MSLP facility has left out smaller firms and alternative lenders that need the capital.

“My response to that was no, there’s been no uptick in your program because the requirements of the program are not attractive enough to make it workable,” Metcalf said. “Don’t scrap the entire program altogether; look at the proposal that we sent you back in July and work with us on amending the facility.”

Amid Pandemic, Small Businesses Pivot to Sell Personal Protective Equipment

September 23, 2020 A number of small businesses—including those in the merchant cash advance industry—faced with little or no way to make money for months—have pivoted to selling personal protective equipment.

A number of small businesses—including those in the merchant cash advance industry—faced with little or no way to make money for months—have pivoted to selling personal protective equipment.

It’s no wonder businesses across the U.S. have shifted gears. With the pandemic raging, and consumers and businesses trying to return to some sort of normalcy, there’s high demand for these products, causing even businesses that previously had no connection to them to spring into action.

“It’s not my forte; I had to pivot just to make sure I could stay afloat before things turned around,” says John DiCanio, founding partner of Direct Merchant Funding in Bethpage, N.Y.

This past spring, at a time when everything in the MCA business stopped, he heard from a merchant in the medical supply field that masks were becoming very important. The merchant connected him to a contact in Hong Kong from whom he was able to buy hospital-grade and non-medical grade masks and sell them to local hospitals, local businesses and others.

DiCanio says he did it for a short time only—two months—which was enough to tide him over under his

regular business started coming back. Mask-making is still a big business and a lot of people are still doing it, but he prefers to stick to merchant cash advance, which he’s been doing for around 15 years. He says business has picked up enough that he no longer has the need to do anything on the side—and he hopes it stays that way.

Many funding industry participants are still selling these types of products, but it’s somewhat of a hush-hush business. Not everyone wants to talk about it for any number of reasons, including embarrassment and fear of looking weak to customers and business connections. Even so, small businesses that pivoted say they are doing the best they can to stay afloat—and there’s no shame in that.

Kat Rosati, founder of Apparel Booster in Riverside, Calif., a product development agency for luxury and socially conscious brands, began hand-sewing masks to help support her business that had been hit-hard by the pandemic.

She has manufacturing partners all over the world, and production was at a standstill for her various products. She couldn’t import fabric needed for the company’s various projects and a lot of production partners were forced to close. Luckily, she had a connection to a fabric mill in Pennsylvania that focuses on antimicrobial products that was willing to provide her with material.

She hired temporary workers to help her make masks, which she’s producing at a rate of about 150 a week. She sells them to consumers and small businesses. The revenue has helped defray overhead expenses, among other things. “It hasn’t been super profitable, but it’s definitely helped keep the business alive,” she says.

She had to furlough her four-person team because she can’t afford to pay them without regular client work coming in. Her husband, who works in the restaurant industry, was also furloughed. So whatever money she can bring in, helps. “I’m watching small business owners around me that haven’t made any kind of pivot close left and right,” she says. “The fact that I can keep mine alive makes it worth it for me.”

To be sure, small businesses pivot for all sorts of reasons, and it’s not always because they are struggling. Francis Perdue, a publicist and business consultant in Birmingham, Ala., began selling PPE products including gloves, kn95 masks, surgical masks, customizable cloth masks, child and adult-sized shields, suits, gowns and the Xenon Fever Defense machine which uses AI technology to measure skin temperature and detect potential fever. She says she saw a need for these types of products in local schools as well as in hospitals and clinics in predominantly black neighborhoods. She is still consulting, but doing this as a side gig while the need persists.

Another example is MORGAN Li, a retail and hospitality manufacturer in Chicago Heights, Ill. The company identified the need and opportunity to help businesses remain open or reopen to customers while abiding by new recommendations to support public health. Thus, the company began producing customized social distancing materials including sneeze guards, safety shields, signage and floor graphics for various businesses to remind employees and customers to comply with social distancing requirements, according to a spokeswoman.

More recently, Andy Rosenband, the company’s chief executive, saw another opportunity to help communities prepare for another critical stage—reopening schools. He created a line of personal protective equipment that specifically addresses the challenge of social distancing in schools to keep students, teachers and staff safe.

For some small businesses, the shift is likely to be a permanent one.

JB Herrera, founder of Perceptive Insights a San Diego-based small and medium business consulting and mentoring company, says his firm was growing, but PPE products offer the ability to create a broader impact and are likely to be more profitable than merely a consulting business.

He has clients in China and back in December when things were starting to get bad there, he realized that the problem could spread massively to the U.S., and if it did, 80 percent or more of businesses would be negatively impacted, in his estimation. Using his business expertise regarding supply chains and pre-existing and new contacts, his company shifted gears to introduce in March a line of FDA-registered products designed to create and maintain safe environments. The products include commercial and personal cleaning solutions, masks, light technology disinfectants, air filtration, and personal sanitizing kits.

Even before the pandemic, the PPE market was worth several billion, he says, and that’s likely to grow exponentially over the next five to 10 years. So much so, that he expects the new business line to represent 90 percent of his revenue for the next three years—at least.

“Even after the spike goes away, it’s still going to be a profitable business in its own right,” he says.

NYC Taxi Drivers Protest, deBanked Reporter Goes For a Ride

September 17, 2020 On Thursday, NYC taxi drivers shut down the Brooklyn Bridge to formally protest the financing costs tied to their taxi medallions, the certificate that allows them to operate in the five boroughs. Tensions over “Medallion loans” have been bubbling over since last year when it was revealed that many borrowers had signed a Confession of Judgment to obtain their loan, which basically waived their right to settle any disputes with their lender in court should they be unable to make the payments. Since then, COVID has completely devastated an already suffering industry…

On Thursday, NYC taxi drivers shut down the Brooklyn Bridge to formally protest the financing costs tied to their taxi medallions, the certificate that allows them to operate in the five boroughs. Tensions over “Medallion loans” have been bubbling over since last year when it was revealed that many borrowers had signed a Confession of Judgment to obtain their loan, which basically waived their right to settle any disputes with their lender in court should they be unable to make the payments. Since then, COVID has completely devastated an already suffering industry…

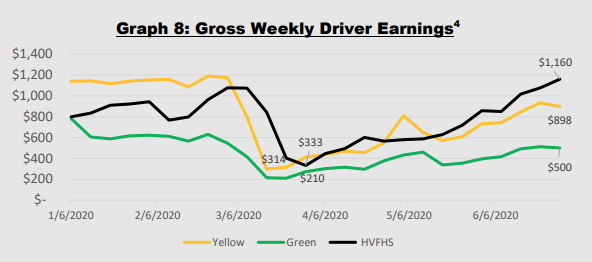

“Before it was good, we could make $100-$150 a day,” said Mohammad Ashref, a local Brooklyn taxi driver in a video interview with deBanked reporter Johny Fernandez. “Now it’s very hard to survive, we work very hard to make 60, 70, or $80 a day, but what can I do? I have to make a living. We have no other choice.”

Ashref technically drives a green cab, different from the yellow cabs that were protesting on the bridge in that they’re not permitted to accept street-hails throughout most of Manhattan. Green taxis also operate through a permit rather than a medallion, a still relatively new concept that was first rolled out in 2013 to facilitate ride-hailing in the outer boroughs where yellow cabs did not spend much time.

Ashref technically drives a green cab, different from the yellow cabs that were protesting on the bridge in that they’re not permitted to accept street-hails throughout most of Manhattan. Green taxis also operate through a permit rather than a medallion, a still relatively new concept that was first rolled out in 2013 to facilitate ride-hailing in the outer boroughs where yellow cabs did not spend much time.

In the interview with Fernandez, Ashref pointed out that the success of the taxi business is intertwined with the restaurant industry. Many riders in the boroughs depend on cabs to take them to restaurants or night clubs, but with the complete ban on indoor dining still in effect within city limits, that need has mostly dried up.

According to the NYC Taxi & Limousine Commission, yellow and green cabs were making as little as $314 and $210 a week respectively during the peak period of the shutdowns. In a 40 hour week, these amount to a fraction of the $15/hour local minimum wage and that’s even before factoring in driver costs like a vehicle lease, loan payments, insurance, and more.

deBanked has been exploring several areas of the New York City economy over the last few months. For instance in July, reporter Johny Fernandez looked into how the pandemic was affecting a street performer in Times Square that was dressed as Batman.

“The business now is slow,” Batman said. “There’s so few people at this moment […] At this moment I see people scared, they don’t want pictures…”

Batman, like others in New York City, was hopeful that a return to normalcy was just around the corner.

NYC Restaurants Have Had Enough, Two Lawsuits Filed to Reopen Indoor Dining

September 9, 2020 The five buroughs of New York City are still quiet. Restaurants remain closed to inside dining; gyms still await their regulars to return (beefcakes deflating with inactivity), and in-person schooling has been pushed back once again, while the districts take an extra week to prepare.

The five buroughs of New York City are still quiet. Restaurants remain closed to inside dining; gyms still await their regulars to return (beefcakes deflating with inactivity), and in-person schooling has been pushed back once again, while the districts take an extra week to prepare.

Through it all, business owners are losing money. Some have had enough.

Il Bacco, an Italian restaurant in Queens, is leading the charge. The restaurant recently filed a $3 billion class-action lawsuit against New York, signed by more than 300 restaurants. Il Bacco is a three-story eatery in Little Neck, 500 feet from the Nassau county border where restaurants can open to 50% capacity.

Another group of restaurants met separately at a rally in Staten Island to speak out against the inaction of lawmakers and to formally propose a separate lawsuit to force the reopening of restaurants.

On behalf of Bocelli, Joyce’s Tavern, and the Independent Restaurant Owners Association Rescue- (IROAR) papers were filed in Richmond County, calling for the emergency opening of restaurants throughout NYC at 50% capacity. IROAR was started last week as a confederation of 14 disgruntled restaurants. More recently the association has grown to 180 members.

Tina Maria, daughter of the owner at Il Bacco, also started an online petition with more than 5,000 signatures at writing.

On Sept 9th, shopping malls can open to 50% capacity and Casinos to 25% capacity, but restaurants like Il Bacco still struggle to make up for six months of decreased activity.

In speaking at the rally on Tuesday, Bob Deluca owner of Delucas Italian Restaurant said he and his workers have put in hundreds of hours of work a week just to see government officials keep his business from opening. Now he said, enough is enough.

“We’re being discriminated against, we’re being bullied,” Deluca said. “My mother told me to always stand up to bullies and stand up for people in need who are being bullied. Right here, this is our knockout punch.”

Deluca dropped the lawsuit on the podium, punctuating his frustration. He said he never wanted it to come to this, but it has come to it. Deluca reacted to Mayor Bill de Blasio’s comment from two weeks ago, stating restaurants were for the middle class and wealthy people.

“We are workers, it’s not a luxurious lifestyle, we are barely middle class,” Deluca said. “What about the waiters, the busboys, what about the dishwashers the bartenders, and the cooks. To say restaurants are for the middle class and wealthy is the most ignorant statement I’ve ever heard.”