Small Business

What Ever Happened to Gradual Change?

March 13, 2012 Did we really go from one extreme to the other?

Did we really go from one extreme to the other?

CNN 8/25/10: Credit Card Debt at 8 Year Low

NY Post 2/26/12: U.S. Credit Card Debt Nearing Toxic Levels (U.S. Consumer Debt at highest point in a decade)

In 18 months, we managed to go from barely using our credit cards to TOXIC LEVELS! So much for gradual change. On August 25, 2010, the Dow Jones reached an intraday trading low of 9,925. As we write this article, it’s currently priced at 13,177.

The unemployment rate in August 2010 was 9.6%. Many believed that figure to be understated. In February 2012, it was 8.3%.

The headlines change so quickly that we’re starting to wonder what the heck is actually happening in this country. Every story announces that something is either the best thing in history, the worst thing in the world, on the verge of destruction, or never seen before. Many people are not even sure how to interpret these fluctuations. Does it mean that we’re in the middle of a full blown recovery or are we experiencing pre-storm volatility as we near the cliff of a catastrophic depression?

In August 2010, the average price of a gallon of gas was under $2.81. Today it’s over $3.71. And consumer spending is increasing but only because Americans are going deeper into debt. Meanwhile the the demand for business loans is increasing, signaling that the private sector is optimistic and preparing for growth.

Don’t take our word for it but the stock market is probably the best indicator of what all this data means. Using the efficient markets hypothesis as a basis, we believe that the recent surge in stock prices indicates that we are on the path to recovery. When the experts realized that the economy was on track to perform well, the market immediately priced stocks as if things were already great. That’s why you can’t beat the market. By the time you’re ready to make a trade, the price has already changed. Today’s Dow means tomorrows success.

It’s time to jump on the recovery bandwagon!

Right?

– deBanked

https://debanked.com

Are You Ready to Ride The Merchant Cash Advance Wave?

February 18, 2012Less than a year after we acknowledged the stunning absence of Merchant Cash Advance financing from the mainstream media, suddenly it’s the only thing being talked about. It took a few years but journalists are finally learning to complete the phrase of banks aren’t lending with, fortunately there are other options. The term Merchant Cash Advance is being thrown around so much that financial institutions that offer different funding programs entirely such as American Express are trying to attach their names to it. They are now trying to rebrand their product as Express Merchant Financing. This isn’t to be confused with a Dallas, TX based company called Express Working Capital which offers Merchant Cash Advances. You can understand why there is so much confusion. Merchant Cash Flow Loans too, which are micro loans based on gross sales are often identified as Merchant Cash Advances even though there is little common ground.

But let’s not fuss over small details because it’s not just the funding companies that are talking about it now, it’s the media.

No matter how well your website is designed or how good your sales people are, it’s important to recognize that small business owners think like normal consumers. According to a 2007 Nielsen Survey, 63% of people’s trust in a company forms from newspaper sources and 56% from television sources. Even though this type of financing has been around since the 1990s, the lack of news coverage has held the industry back. Despite the advancement of social networking and internet background searches, the majority of Americans still have that If it’s on TV, it must be true mentality. Why else would political candidates still be spending billions of dollars on TV commercials to get their message across?

The broad use of Merchant Cash Advance terminology, the recent recognition by the mainstream media, and the march of average Americans into the reseller market is an omen. A wave is coming. Whether some deem the current industry’s size to be $600 million a year or $1 billion is irrelevant. Merchant Cash Advance and similar financing programs have the potential to be a $10 billion market annually, especially since the major banks are retreating from SBA loans.

We suspect that in 2012, particularly the latter half of it will be explosive unlike the entire industry has seen before. Too many small businesses have been waiting on the sidelines since 2008. If the trend of rising employment is correct and a real recovery is underway, then we’ve got all the ingredients for a perfect storm. Confident Business Owners + Fast, Easy Access to Capital = American Recovery.

Call these business loan alternatives whatever you want: Merchant Cash Advances, Merchant Cash Flow Loans, Express Merchant Financing, etc. Just make sure you have a surfboard. A giant wave is coming.

– deBanked

https://debanked.com

Does Your Mom Sell Merchant Cash Advance?

February 4, 2012Five years ago, everyone seemed to add the phrase, “but I also do mortgages on the side” in response to questions about their career.

“I’m a stockbroker, but I also do mortgages on the side.”

“I’m a school teacher, but I also do mortgages on the side.”

“I’m a stay at home mom and a loving wife, but I also do mortgages on the side.”

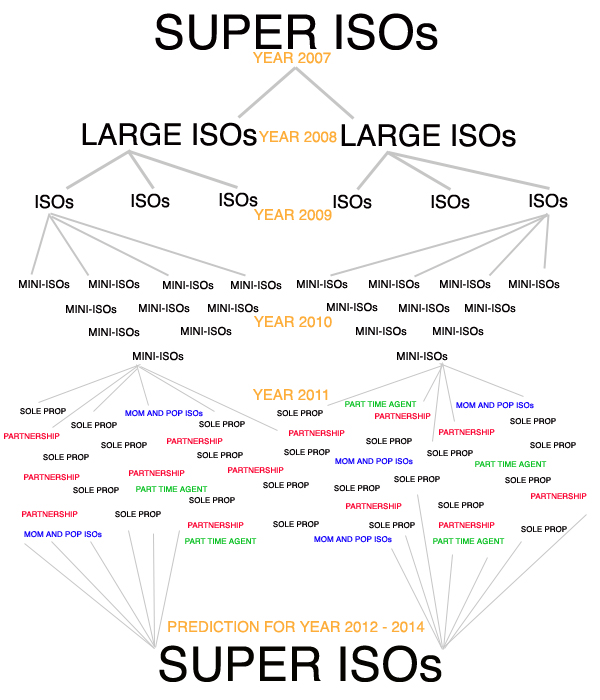

Times have changed and today the new side gig is reselling Merchant Cash Advance (MCA), at least in the New York metropolitan area. The Independent Sales Office (ISO) model is dissipating into a few thousand sole proprietors, all of whom are competing for the same prospects. Most of them started at one of the larger ISOs or funding sources and have over time traded it for the opportunity to work for themselves. Others have pushed it aside as a part time gig while earning a living in another line of work.

It’s encouraging to see that the entrepreneurial spirit is alive and well in the city that never sleeps, but riding solo has its disadvantages. For instance, marketing budgets are more constricted. This inhibits the ability to attract clients, especially when competing against a sizable ISO, who likely has thirty times more to spend on advertising, systems, and service.

It’s encouraging to see that the entrepreneurial spirit is alive and well in the city that never sleeps, but riding solo has its disadvantages. For instance, marketing budgets are more constricted. This inhibits the ability to attract clients, especially when competing against a sizable ISO, who likely has thirty times more to spend on advertising, systems, and service.

And yet, I haven’t heard many complaints from independent agents, which may mean the MCA industry is far from over-saturated. Sixteen of my former co-workers have gone on to start their own MCA ISOs. I even know a pair of twin brothers that run ISOs independent of each other. Some of these newly formed mini-ISOs (less than five people) break apart and each member seems to go on and repeat the cycle.

The Derailing of the Shakeout

In early 2008, it was predicted that low budget marketing would cause a massive shakeout of MCA resellers. David Goldin, the CEO of AmeriMerchant published the following in his blog:

There is another train of thought that is inevitable to fail – those that thought they can sell business cash advances with minimal capital expenditure, meaning hiring unqualified salespeople using inexpensive marketing techniques such as voice broadcasting (with these providers giving the same data to 100s of phone rooms) to dial hundreds of thousands of businessses an hour with a prerecorded message. (Merchants around the country are getting 3 – 5 prerecorded calls a day). The challenge is the quality of anyone that is going to press ‘2’ on their phone for money tends to be “lower hanging fruit” and lower quality deals. With the recent credit crunch and many merchant cash advance funding companies tightening up, some merchant cash advance agents were seeing approval rates as low as 15%-20%. There is no way they can survive and stay in business with that kind of approval rate.

Back then, it was quite popular to have a hundred sales agents in a single room making phone calls. Overhead was the biggest part of the budget, which in places like New York City, could consist of tens of thousands of dollars in rent alone. Add that to all the money that was spent on technology, payroll, dialers, and commissions, and it became really easy to generate a net loss.

With the emergence of mini-ISOs, many are foregoing traditional overhead expenditures such as the renting of a centralized office. Technology costs are also being eliminated since most people already own a personal computer and a cell phone, the only two tools really necessary to interact with prospects. As for state of the art auto dialers? Well, many agents are completely fine using inexpensive resources such as phone books or public UCC filings. Ask around in the MCA industry and you’ll learn just how prevalent this practice is.

There are so few barriers to entry in the MCA industry, that it catches a lot of folks from other financial fields off guard. We receive a dozen e-mails a month from mortgage brokers, stockbrokers, and insurance agents asking what licensing requirements they will need to sell MCA. There are none of course, but they more are shocked to learn that there are no regulations to abide by either. Take your cell phone, throw in your e-mail, spend twenty bucks on a website and you’re an official MCA reseller! It’s just that easy. Thousands of people are getting in on it.

Who is Who?

The flood of resellers and fly-by-night agents is making it increasingly difficult to know where all the MCA money is actually coming from. Here on the Merchant Processing Resource’s website, we’ve created transparency by listing the largest direct funding providers. Need to know if that UCC filing is MCA related? We can help you with that too.

We’re also working on creating an official directory of resellers, for which there will be some requirements for inclusion. That means if you’ve e-mailed us on this topic already and you haven’t heard from us yet, be patient. You will be contacted soon with instructions on how to become an approved MCA reseller.

Consolidation

In the meantime, the increasing fragmentation also presents an incredible buying opportunity. Large ISOs that are looking to add to their portfolios and leverage the brand names that mini-ISOs have created should be able to buy them out at very affordable prices. When this practice starts to happen, it’ll be interesting to see what the market value of mini-ISOs are. Could a business owned by two individuals with a pool of two hundred clients be worth $50,000? $100,000? $300,000? Once someone sets the bar, we should prepare for a year of consolidation, and the little guys will get gobbled up by the big ones. A lot of folks could end up walking away very rich or disappointed. Perhaps now is a good time for your Mother to go into the MCA business for herself and flip the value created for a nice profit a year from now.

ISOs on Steroids

The popularity of co-funding or syndication is also allowing the remaining large ISOs to really flex their muscles in a way they weren’t able to in 2008. Syndication is where an ISO is able to invest their own capital in the MCA deals they close. For instance, on an advance of $20,000, $15,000 of it might come from the MCA funding source, and the remaining $5,000 from the ISO themselves. As long as these accounts perform well, syndicating can create a supernatural rate of growth. This further whets the appetite for opportunities to expand.

So why are mini-ISOs a buying opportunity? Customer loyalty is something big companies can’t always shake, no matter how much is spent courting them. Furthermore, these mini-ISOs tend to have historical performance records on their clients, data that is incredibly valuable. Should a Super ISO invest $20,000 in a small business that has never used MCA before or should they invest it in a business that has responsibly used MCA for two years with no issues, exhibits fierce loyalty, and has a proven record of success? The opportunity to participate in funding that business now and repeated times in the future should be worth a lot.

The Unknown

There are other forces at work that may reshape the industry in a way we can’t predict. The incredible rise of micro-lending is cannibalizing the MCA market, but is also allowing ISOs to offer a variety of financial products to a larger pool of businesses. One New York City MCA funding source privately revealed that micro-loans now make up 80% of their monthly funding volume, a stunning shift from their MCA-only portfolio of 2010.

The growing popularity has also caught the attention of regulators and in some states, the purchase of future credit card receivables is being governed by existing lending laws. The day may come when every agent needs a license to sell, but until then, thousands of people are playing the biggest game in town, helping small businesses get funding to grow. Are you a part of it?

– deBanked

https://debanked.com

The Small Business Lending Climate is Bad, But it’s Not a Disaster

January 27, 2012 We’re proponents of the Merchant Cash Advance (MCA) financial product, but we also believe in objectivity. Over the last several years, MCA providers have collectively rallied the masses by branding themselves as a source of business financing in an economy where financing is scarce.

We’re proponents of the Merchant Cash Advance (MCA) financial product, but we also believe in objectivity. Over the last several years, MCA providers have collectively rallied the masses by branding themselves as a source of business financing in an economy where financing is scarce.

Many people consider the collapse of Lehman Brothers on September 15, 2008 to be the official start of the latest recession. Some will argue that we’re still in that recession. We would probably agree with that. Either way, there hasn’t been much improvement in the financial markets.

Yesterday, on Sean Hannity’s radio show, guest speaker Donald Trump, said “banks aren’t lending.” That’s verbatim and it says a lot, considering that yesterday was January 26th, 2012, a full three years after Lehman’s demise.

A friend of ours that does commercial banking in Philadelphia reiterated the same thing to us a few months ago and even went so far to reveal that restaurants and retail establishments are on their lending blacklist. These revelations paint a grim picture and it’s fortunate that the MCA industry has risen to the challenge to support small business owners.

But there is light at the end of the lending world’s black hole. This morning we had a meeting with a big bank in New York City and of course we asked the question, “Are you lending to small businesses?” They responded, “yes”, and we expected them to follow it with a “but.” Except they didn’t. In fact, they said that small business lending was their biggest market right now.

Intrigued, we demanded to know more. Approximately 50% of applications are being approved and the criteria is as follows:

- Minimum two years in business

- Minimum personal FICO score of 680

- Minimum $250,000 in annual sales

- Must have consistent pattern of sales

- No history of overdrafts or NSFs

- Must prove history of keeping substantial cash reserves in the business account

- Must be current with all vendors and business property landlord

- Collateral may be required

- Maximum approval amount is 20% of annual gross sales

This checklist is challenging. That’s why leveraging your future credit and debit card sales to obtain a large chunk of capital upfront is not only the preferred method of financing for businesses with bad credit, but also for those that are making a serious investment in themselves.

Nonetheless, if a bank IS lending, we’ll be the first ones to admit it. MCAs offer a lot of powerful benefits, but if all banks start lending again one day in the future, quoting Donald Trump might not have the same impact it once did. Fortunately, there are twenty other reasons why MCA is a solid solution, and what banks are doing or aren’t doing is completely irrelevant.

– deBanked

https://debanked.com

Note:

If you are a small business located in the New York City area that is interested in a loan as described above, we would be happy to personally refer you to that bank.

The 28% You Don’t Want – New IRS TIN Matching Regulation

January 21, 2012 If your merchant service provider (MSP) doesn’t have your proper business information on file, you could be in for a world of hurt. As per Section 6050W of the Housing Assistance Tax Act of 2008, all electronic payment transactions have been reported to the IRS since January 1st of last year. In order to ensure this reporting is accurate, certain business data must match the data on file with the IRS, such as:

If your merchant service provider (MSP) doesn’t have your proper business information on file, you could be in for a world of hurt. As per Section 6050W of the Housing Assistance Tax Act of 2008, all electronic payment transactions have been reported to the IRS since January 1st of last year. In order to ensure this reporting is accurate, certain business data must match the data on file with the IRS, such as:

- Your Taxpayer Identification Number (TIN)

- Your Legal Business Name

- Your Legal Business Address

- Your Business Organization Type (e.g. Corporation, LLC, Partnership, Sole Prop., etc.)

MSPs are required to report gross revenue, so chargebacks and refunds are included. The official ruling states:

Section 6050W(a) provides that each payment settlement entity must report the gross amount of reportable payment transactions for each participating payee. The proposed regulations defined gross amount as the total dollar amount of aggregate reportable payment transactions for each participating payee without regard to any adjustments for credits, cash equivalents, discount amounts, fees, refunded amounts, or any other amounts.

And if your tax information doesn’t match, the IRS will withhold 28% of all your payments starting on January 1st, 2013, whether it’s your fault or not. Once that happens, your MSP can’t refund you and all issues must then be handled with the IRS directly. If you haven’t received any kind of alarming notice that your information doesn’t match, this warning doesn’t apply to you. Although, it can’t hurt to call your account representative to confirm that all information is up to date and verified. Better safe than sorry.

If you didn’t know about this law, now is a good time to read up on the dense technicalities of it in this 520 page document.

Rewards: The Next Phase of Merchant Cash Advance Evolution

January 21, 2012 Sky miles and 1% cash back are practically standard benefits of using your credit card, so why shouldn’t you get a little something extra with your Merchant Cash Advance (MCA)? I pay my credit card bill on time every month because I am a responsible customer. As a result, the bank continues to extend me credit when I need it. But that’s not all they do, they also send me a check for 1% of every purchase that I make. That’s pretty nice of them!

Sky miles and 1% cash back are practically standard benefits of using your credit card, so why shouldn’t you get a little something extra with your Merchant Cash Advance (MCA)? I pay my credit card bill on time every month because I am a responsible customer. As a result, the bank continues to extend me credit when I need it. But that’s not all they do, they also send me a check for 1% of every purchase that I make. That’s pretty nice of them!

Sure, it’s a great way to encourage spending but it also promotes loyalty. I get a million credit card offers a year and I have no desire to switch. Isn’t that something?

The Merchant Cash Advance (MCA) industry could learn a thing or two from this. While funding small businesses is practically a blessing in that of itself, there is a lot of fierce competition between MCA providers. Once a business has used MCA, it seems everybody starts fighting over whose going to fund them next. It must be quite an experience for business owners who are by now used to banks tossing them around like an unwanted hot potato. In the MCA industry, everyone wants to fund the potato.

The truth is though, the terms won’t vary much between firms and even if they do, the transaction cost might not be worth it. Switching to a new MCA provider can result in any of the following:

- A termination fee on your existing merchant account

- The purchase or lease of new POS equipment

- The installation of new POS equipment

- An additional service fee on top of the cost of financing

- Unexpected issues with trust or the service

If you have found success with the company that financed you, we can both agree that it’s easier to stay with them. But without additional incentives, you may be feel like your business isn’t appreciated. That’s probably not true and sometimes our sense of entitlement gets the best of us. The thing is though, we believe a little reward is just what you deserve. What makes a great MCA provider great is their ability to become a true partner in your success, instead of just silently collecting their purchased receivables. That’s why we propose the following:

- Cash back for hitting certain monthly sales targets

- Rewards for hitting certain monthly sales targets (gift cards, free advertising, a small business makeover)

- Access to free consulting (consultations from experts on how to best invest the money you receive)

Imagine the motivation you’d feel if your financing not only got approved, but led to a whole bunch of rewards if you invested that money wisely. We don’t have control over the nation’s MCA providers but we can plant the seed and wait for someone to do it first.

Let’s pretend that your business does $8,000 a month in credit card sales on average. One month, you hit $12,000. I think a little reward is in order! Send us an e-mail and tell us what you think.

– deBanked

Law to Reduce Debit Card Fees to Retailers Has Opposite Effect

December 12, 2011We’ve had many negative things to say about the debit card reform law that went into effect a few months ago (AKA the Durbin Amendment). We’ve repeatedly made claims that retailers won’t participate in the savings but for the few that do, those savings won’t be passed on to the consumer.

According to a recent article in the Wall Street Journal, something much worse is happening; Debit card fees are going up!

“Jason Scherr had a lot on his mind the day after he opened his fifth Think Coffee shop in Manhattan last week. The fan was blowing too hard, the classical music was playing a little too loudly—and he was trying to figure out how to get more customers to pay with cash.

Manhattan coffee-shop owner Jason Scherr says his debit-card fees are higher since the Dodd-Frank law.

A new law that was supposed to reduce costs for merchants that accept debit cards has instead sent Mr. Scherr’s monthly processing bills much higher and forced him to reassess the way he does business.

“My choice is to raise prices, discount for cash or get an ATM,” says Mr. Scherr, a lawyer who has been in the coffee-shop business for more than a decade.

Just two months after one of the most controversial parts of the Dodd-Frank financial-overhaul law was enacted, some merchants and consumers are starting to pay the price.

Many business owners who sell low-priced goods like coffee and candy bars now are paying higher rates—not lower—when their customers use debit cards for transactions that are less than roughly $10.

That is because credit-card companies used to give merchants discounts on debit-card fees they pay on small transactions. But the Dodd-Frank Act placed an overall cap on the fees, and the banking industry has responded by eliminating the discounts.

“There will be some unhappy parties, as there always is when the government gets in the way of the free-market system,” says Chris McWilton, president of U.S. markets forMasterCard Inc. He said the company decided that it couldn’t sustain the discounts under the new rate model because the old rates had essentially subsidized the small-ticket discounts.

Merchants now are trying to offset their higher rates by raising prices, encouraging customers to pay in cash or dropping card payments altogether.”

Read the full article at WSJ.com

Occupy Main Street?

October 10, 2011 We didn’t protest… but we decided to see who was. Nowhere in the strange crowd did we find outraged business owners. Could the occupiers of Wall St. also be fighting against Main St.?

We didn’t protest… but we decided to see who was. Nowhere in the strange crowd did we find outraged business owners. Could the occupiers of Wall St. also be fighting against Main St.?

Wall St. bankers might have a lot of money, but small businesses employ the most jobs in America. Chances are if you are unemployed, unhappy, or overworked, it will ultimately be Main St. that will save you. But for time being, nobody is hiring. Business owners are pointing the fingers at banks, citing the lack of loans has stalled expansion. Excuses, excuses…

Wall St. might have perverted capitalism to enrich themselves, but Main St. has done just the opposite lately. When presented with an opportunity, thousands of businesses are unwilling to take the risk. “We’re just holding on for right now,” is a phrase we hear way too often from Mom and Pop shops.

We posed this question to an unnamed ‘Occupy Wall St.’ protester today:

MPR: “If we gave you $10 today, could you turn it into $20? “

PROTESTER: “Hell, I could turn it into $100. You can make money on a lot of stuff going on down here.”

Capitalism lives… It’s the drive and execution that enables someone with $1 to turn it into $2, $5, or $100 in a marketplace. It’s an intuition that Americans are born with, even those with anarchistic tendencies yelling in protest against it.

But something has happened to our beloved Main St.

Opportunities to grow are being passed up, and with that the ability to hire more workers. The rich get richer by investing their capital and taking risk. In a competitive marketplace, we must always seek out ways to grow, expand, and improve. “Holding on” is not a strategy, at least not one that will lead to hiring. Stability does not prepare you for downturns, nor will it make you rich in the long term. Stability is actually the beginning of a long road that will one day lead you to being mad at those who got rich.

The math is simple. If you turn $1 into $1.10 everyday, while somebody else turns $1 into $2, expect yourself to be very poor by comparison 20 years from now. Whether you have a small retail store or a national franchise, don’t let your guard down, take chances, think big, and elbow your way to the top 1%. You’ll create a lot of jobs on the way.

Once you’re ready to turn $1 into $2, don’t worry about the lack of bank loans, Merchant Cash Advance providers will offer you $1 in return for $1.30. You net the profits and can redo it as often as you like. Naysayers will tell you it’s expensive and it would be if you didn’t invest the dollar. Rebuilding the economy begins with small business. Show them growth, show them jobs, show them how you were born to turn one dollar into two…

deBanked

http://www.merchantprocessingresouce.com

Learn about Merchant Cash Advance Here

Some video clips we took while we were at the Wall St. protest: