small business owners

NYC Taxi Drivers Protest, deBanked Reporter Goes For a Ride

September 17, 2020 On Thursday, NYC taxi drivers shut down the Brooklyn Bridge to formally protest the financing costs tied to their taxi medallions, the certificate that allows them to operate in the five boroughs. Tensions over “Medallion loans” have been bubbling over since last year when it was revealed that many borrowers had signed a Confession of Judgment to obtain their loan, which basically waived their right to settle any disputes with their lender in court should they be unable to make the payments. Since then, COVID has completely devastated an already suffering industry…

On Thursday, NYC taxi drivers shut down the Brooklyn Bridge to formally protest the financing costs tied to their taxi medallions, the certificate that allows them to operate in the five boroughs. Tensions over “Medallion loans” have been bubbling over since last year when it was revealed that many borrowers had signed a Confession of Judgment to obtain their loan, which basically waived their right to settle any disputes with their lender in court should they be unable to make the payments. Since then, COVID has completely devastated an already suffering industry…

“Before it was good, we could make $100-$150 a day,” said Mohammad Ashref, a local Brooklyn taxi driver in a video interview with deBanked reporter Johny Fernandez. “Now it’s very hard to survive, we work very hard to make 60, 70, or $80 a day, but what can I do? I have to make a living. We have no other choice.”

Ashref technically drives a green cab, different from the yellow cabs that were protesting on the bridge in that they’re not permitted to accept street-hails throughout most of Manhattan. Green taxis also operate through a permit rather than a medallion, a still relatively new concept that was first rolled out in 2013 to facilitate ride-hailing in the outer boroughs where yellow cabs did not spend much time.

Ashref technically drives a green cab, different from the yellow cabs that were protesting on the bridge in that they’re not permitted to accept street-hails throughout most of Manhattan. Green taxis also operate through a permit rather than a medallion, a still relatively new concept that was first rolled out in 2013 to facilitate ride-hailing in the outer boroughs where yellow cabs did not spend much time.

In the interview with Fernandez, Ashref pointed out that the success of the taxi business is intertwined with the restaurant industry. Many riders in the boroughs depend on cabs to take them to restaurants or night clubs, but with the complete ban on indoor dining still in effect within city limits, that need has mostly dried up.

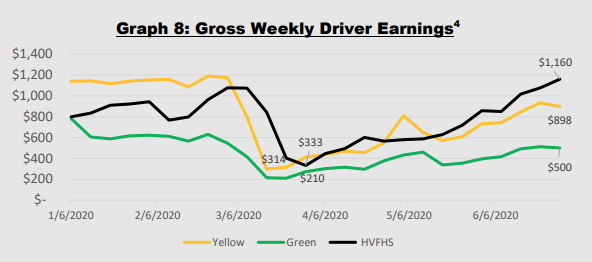

According to the NYC Taxi & Limousine Commission, yellow and green cabs were making as little as $314 and $210 a week respectively during the peak period of the shutdowns. In a 40 hour week, these amount to a fraction of the $15/hour local minimum wage and that’s even before factoring in driver costs like a vehicle lease, loan payments, insurance, and more.

deBanked has been exploring several areas of the New York City economy over the last few months. For instance in July, reporter Johny Fernandez looked into how the pandemic was affecting a street performer in Times Square that was dressed as Batman.

“The business now is slow,” Batman said. “There’s so few people at this moment […] At this moment I see people scared, they don’t want pictures…”

Batman, like others in New York City, was hopeful that a return to normalcy was just around the corner.

NY Small Business Owners Protest $15 Minimum Wage

March 8, 2016 Small business owners in New York have registered dissent against Gov. Andrew Cuomo’s plan to raise the minimum wage in the state to $15 per hour, the highest minimum wage in the country.

Small business owners in New York have registered dissent against Gov. Andrew Cuomo’s plan to raise the minimum wage in the state to $15 per hour, the highest minimum wage in the country.

In November last year, Cuomo announced that New York will raise the wages of permanent and seasonal workers to $15 by 2021. The business owners gathered in Albany on Tuesday to reject the proposal, claiming that the tax cut offered to ease the process is too little to offset the cost.

Small businesses generate roughly $950 billion in revenues annually and created 2 million jobs in 2014.

American Express wants to lend more to small businesses

February 10, 2016American Express hopes to tide over the bitter credit-card deal with Costco by lending to small businesses.

The two companies ended their 16-year partnership when Costco joined hands with Citi in March 2015. This June, customers will receive their Costco-brand Visa credit cards.

AmEx wants to turn its focus on what it is already familiar with — small business loans. In 2014, AmeEx cards for small businesses funded $190 billion in purchases, up from $122 billion in 2010, with enough reason to believe that there is room to grow the business.

AmEx hopes for the small-business loans to make up for the lost revenue from the Costco deal which accounts 20 percent of the company’s outstanding loans, according to a Reuters report.

The Importance Of A Profitable Business Model And Creative Financing For Your Broker Office

August 10, 2015 Continuing The Year Of The Broker Discussion, I wanted to touch on another aspect that isn’t discussed too often in our space (Independent Broker or Independent Agent space), and that’s the importance of creating a profitable business model and rounding up creative debt financing for our Office.

Continuing The Year Of The Broker Discussion, I wanted to touch on another aspect that isn’t discussed too often in our space (Independent Broker or Independent Agent space), and that’s the importance of creating a profitable business model and rounding up creative debt financing for our Office.

I believe it was the Roman Playwright, Plautus, that said, You must spend money to make money. This is certainly true for Independent Brokers and Agents, as we are entrepreneurs in every sense of the word, or if you operate a one man show like I do, then you would be more along the lines of a solopreneur which is new terminology floating around that refers to certain special entrepreneurs who run their business solo with full responsibility over the day-to-day operations.

However, despite the fact that one must spend money in order to make it, it begs the question as to why many new Brokers have very little networks, resources and other sources for financing?

Not only do they lack these resources, but many new Brokers also have not truly developed a scientific business model for their office based on: If I invest XYZ in data, marketing and all other aspects in association of producing 1 new closed deal, I would receive XYZ back into terms of the revenue off the initial closed deal as well as XYZ back in terms of recurring revenues on the renewals of said merchant.

Many new brokers lack both a scientific and profitable business model, along with efficient financing for said business model, which threatens their survival going forward.

Your Profitable Business Model

I argue with investors across the Investment Community all of the time in relation to which is better in terms of building the most Wealth, is it investing in Stocks or operating your own Profitable Business Model? I have always believed creating your own Profitable Business Model was the fastest way to Wealth due to the lack of control one has over the returns you can generate through the Stock Market. Commentators like James Altucher tend to agree with my mentality as he says: The best way to take advantage of a booming stock market is to invest in your own ideas. If you have an extra $50,000 don’t put it into stocks. Put it into yourself. You’ll make 10,000% on that instead of 5% per year.

I’ve always used a model of at least a 400% return within 24 months for operating my office because, not only did I have to cover business expenses and taxes, but I also had to cover my personal expenses, the funding of my emergency funds/savings, and the funding of my retirement accounts which includes SEP IRAs, Social Security, and Health Saving Accounts.

So for example, my model might have it to where if I invest $30,000 into my office, that should produce revenues of around $180,000 within 24 months, revenues include commissions from new deals, renewal deals, side processing residuals and other valued added products. This would leave a profit before taxes of $150,000 or a 500% return. Now the 500% range is just the benchmark used, in terms of actual returns, they have been at least double this amount due to my focus on maintaining clients for the long term as with recurring clients, there are no investment dollars spent on the acquisition of those additional revenues but they do continue to add to the overall “profitability” measurement of the original investment.

Utilizing this predictable model allows for the use of creative financing for leverage, cashflow management, along with the preservation of savings, and other investment portfolios. One of the tools I have been using for creative financing have been Credit Card No Interest Promotional Offers.

Using Credit Card Promotional Offers To Finance Your Office

I’m a Dave Ramsey fan like many Americans, but I’m totally against Mr. Ramsey’s consistent hammering of the use of “debt,” specifically the use of Credit Cards. Credit Cards are just like hand guns, if you put the gun in the hands of a solider, police officer, hunter, or a responsible home owner, then you protect human life, build nations and protect communities. If you put the gun in the hands of the common Chicago inner city street thug, then you get crime and homicide. If you put a Credit Card in the hands of a responsible person, the Credit Card is used to bring a variety of additional benefits to said user. But in the hands of an irresponsible person, the Credit Card just adds to their financial woes.

If you strive to keep your personal credit profile clean and with high efficiency, you should qualify for a number of Credit Cards that not just provide cashback rewards, but they provide short term financing in the form of 0% interest for 12 – 18 months, with a 1% – 3% upfront fee. This means you can receive an up to 18 month loan for only 1% – 3% in borrowing costs. These offers are not presented just when the card is opened, but they are generated usually on a monthly or quarterly basis.

So coming back to my business model, I might put that entire $30,000 on a credit card promo deal for 18 months with an upfront fee of 3%, which means the borrowing costs are $900. I would continue paying the minimum payment every month which is usually calculated as no more than 0.5% – 1% of the outstanding balance. I would invest the $30,000 into my business model and would have obtained the break-even return and profit measurement in a relatively short period of time (usually 3 – 5 months) and then be profitable on the investment. I would eventually end up paying off the outstanding balance on the Credit Card well before the promo period ends, which further increases my positive credit history allowing for larger credit limits to be requested.

Other Benefits Of Credit Cards Over Other Payment Options

Credit Cards also provide a host of other benefits including cashback rewards of anywhere from 1% – 45% depending on the reward category, these rewards and savings are not available through any other form of payment option. If you seek out cards with no monthly fees, setup fees or annual fees, you could run up balances, pay them off before the grace period ends, and obtain a stream of free income.

Credit Cards also include Chargeback Protection that can save you a significant amount of headaches down the line should you run into an unscrupulous vendor, or if you are the unfortunate victim of theft such as a robbery, identity theft, strong-arm theft, etc. For example:

- If someone steals your wallet and goes on a “card swiping spree”, once you report your Credit Card stolen then you aren’t responsible for any of those transactions. This isn’t as efficient if you carried a Debit Card, as the money would be gone from your Checking Account until the Bank recovers the funds in 30 – 90 days, which might cause you some cashflow issues. If you carried Cash, the money might never be recovered.

- If you ordered something from a vendor and didn’t receive it, you are protected with the use of Credit Cards. With a Debit Card or Check, it will again take 30 – 90 days for the dispute to complete with the Bank, however, throughout this period of time the money is still gone from your account until the dispute is over, which might cause some cashflow issues. If you used Cash for the order, the money might never be recovered in this case as even though you are likely to obtain a judgment by suing the vendor, the Courts do not assist you with collections.

To Wrap

In order to survive going forward as an Independent Broker or Agent, remember the importance of developing a profitable business model as well as having low cost sources of financing for said model. Credit Cards are one of the ways you can creatively finance your business model.

I’m on track to end the year with near or over $200,000 in total credit limit availability. This credit limit availability is spread out over a number of different accounts, but some of my favorite Credit Card Accounts include: The Double Cash Card ™ from CitiBank, The Discover IT Card ™ from Discover Bank, The BankAmericard Cash Rewards Card ™ from Bank of America, The Chase Freedom Card ™ from Chase Bank, The Upromise Mastercard ™ from Barclay’s Bank, The QuickSilver Rewards Card ™ from Capital One Bank, and The Blue Cash Everyday Card ™ from American Express.

The Funding Calls That Won’t Stop

November 23, 2014“Your business has been approved for a loan…”

Last week, Chicago Public Radio (WBEZ 95.1 FM) investigated a trend in the small business community, the use of merchant cash advance financing. The station called me in advance to answer some questions about merchant cash advances and I gave my best explanation of the industry and its products.

Of the discussion that lasted more than 30 minutes, only about five of my sentences made it on the air. While I clarify some of my positions below, it was sobering to learn the context of how they were used, as a defense to real life merchant complaints.

The satisfaction rate with merchant cash advances are pretty high and I say that mainly because it’s so rare to hear complaints from anyone other than journalists that can’t believe anyone would accept rates above 6% APR. And while there are indeed bad actors in the industry (as there are in any industry), the gripe one merchant had about phone solicitations that just won’t stop is a recurring theme.

It’s happening to me too.

As an account representative in 2010 calling real time leads sold to five parties at once, I did what anyone would do, I pretended to be a small business myself and inquired through the website that we bought leads from and entered my cell phone as the point of contact

Ring. Ring. Ring…

Within a half hour, representatives from four companies called me, and I learned exactly who my competition was, how they explained the product, and what they would say to win me over. Two of the four were really good and one even referenced my name personally, saying something to the effect of, “If you get a call from Sean Murray, his rates are worse than mine.” Obviously he had already done what I was doing now, which was pretend to be a small business so he could prove to the prospect he was well informed about the alternatives. He had heard my pitch already and was now throwing me under the bus by planting the seed that I was going to offer something more expensive even if it wasn’t the truth.

In the end none of them won because it was all a farce. One never called me again after the first call. Another kept at it for a week and the remaining two followed up for a month.

And then it got quiet…

I had been marked as a dead lead and forgotten about until three months later when one company sent a follow up email. “Smart,” I thought. But then a call came six months later, and then more emails, some from companies I didn’t originally engage with.

And they continued at regular intervals, every couple of months an email or call. Was it interesting? Yes. Annoying? No.

Until this year.

The volume of emails have slowed but I’ve somehow ended up on robo calling lists. “Press 1 to talk to a funding specialist or press 9 to be added to the Do Not Call list”

The volume of emails have slowed but I’ve somehow ended up on robo calling lists. “Press 1 to talk to a funding specialist or press 9 to be added to the Do Not Call list”

The press 9 option doesn’t work for me. Sure, I might be removed from that marketer’s list, but it in no way removes you from anyone else’s list. I knew that already of course because I’ve been on the other end before.

The first time I got one of these calls, I was excited to tell the sales representative who I really was, level with him, and explain that it was a really good idea to take me off the list. But much like other business loan robo call complaints, the representative wouldn’t tell me anything about himself or his company.

I got yelled at.

Every time I tried to ask a question, he’d get louder, insisting I tell him my monthly gross sales volume for the “cash advance I wanted.”

A rogue actor maybe, but I’ve since gotten additional business loan robo calls and have made no progress in getting myself removed. I just hang up now.

Call it sweet irony perhaps. Or maybe a wake up call (pun intended). I applied on a website once four years ago and the rest is history.

My experience with repeat solicitations is marginal compared to somebody that has actually used a merchant cash advance. With the filing of a public UCC-1, anyone in the industry can easily access that data and convert it into a marketing list. And they do.

Brokers that scorn UCC marketing acknowledge that these businesses could be getting called 5-10 times a day. My own clients had reported repetitive calls back when I was an account representative. And while UCC marketing is very cost effective, in today’s market where more than a thousand companies are offering similar financial products, it’s probably safe to say it’s overly saturated.

And if 5-10 calls per day were even remotely accurate, I’d surmise that level of volume is marring the industry’s reputation as a whole.

I could argue though that when customers have a great many options to choose from, they win. With more than a thousand companies offering merchant cash advances and business loans, it’s truly a buyer’s market. Play all the companies against each other and you should end up with the best possible terms. It’s a great time to seek capital.

Except we’ve got to do something about those phone calls, or at least the robo calls.

Every angry robo dial recipient becomes one less person likely to speak positively about the the nonbank financing industry. Aged leads, UCCs and phone calls might be inexpensive, but the cost to undo negative preconceived notions is immeasurable.

Do you want to be known as the company that helped small businesses or the annoying people that won’t stop calling? If merchants are taking to the air waves to complain, it will only be a matter of time before the FTC and FCC become interested.

—

Regarding my comments on the radio about APRs and daily amortization, they were pulled from a conversation that compared daily payment loans to purchases of future sales. I DO believe bad actors exist and every business owner should have an accountant, lawyer, or savvy third party review any contracts they enter into, financial or otherwise.

The Deal

May 25, 2014When times are tough, small businesses take chances. Last year, a family run business in Cohasset, MA made a snap decision and agreed to a $75,000 loan with infinity percent interest, literally. The principal was completely repaid in just 74 days but as per the contract, they still had to make fixed interest payments for as long as the business was open.

It wasn’t necessarily a good deal. Heck, some might think it was a really bad deal, but they got the cash when they needed it. The perpetual fixed payments kicked in after the principal was repaid because the lender structured them as royalty fees. A normal merchant cash advance will take a percentage of a merchant’s sales up until a predetermined amount has been satisfied, but this deal required a percentage forever. Is Wall Street running amok yet again? Shouldn’t people be monitoring stuff like this?

As it would turn out, about 6.5 million people were witness to this transaction. More than half of those people, most of whom are hard-working American families, cheered the business owner on. That’s because this deal had nothing to do with Wall Street and did not involve a commercial loan broker.

The business is named Wicked Good Cupcakes and it’s a deal they made on Shark Tank, a hit TV show on ABC. Kevin O’Leary loaned them $75,000 and took a percentage of every sale until he was repaid just 2.5 months later. Since then he is taking a permanent royalty of 45 cents per cupcake sold.

As quoted in the Boston Business Journal

“The royalty deal has worked great for us,” said Tracey Noonan, the CEO of the company.

Many people told her immediately following the deal that she was stupid. But today, Wicked Good Cupcakes is doing better than ever.

O’Leary, whom the business owners called an “angel in disguise” has referred to the deal as one of the most phenomenal ever made on the show. Wicked Good Cupcakes is actually on pace to do $3 million in revenue in 2014.

While it’s true that part of their success is due to the appearance on the show, nowhere does it say that entrepreneurs have to agree to take a deal if offered one. That means the owners could have walked away from O’Leary’s offer and still experienced the same post-show hysteria of celebrity. But they needed the money… and there was an offer on the table. It wasn’t the best deal, but it was A deal.

And that’s the nature of business. Everything is about circumstances. You could be flush with cash or in a pinch, growing fast or playing defense. All the while opportunities and obstacles approach from every turn.

Unlike consumers who are afforded protections from making decisions that might not be in their best interest, small businesses are free to pursue whatever strategy they want. The best part about capitalism is that you’re the master of your own destiny.

Unlike consumers who are afforded protections from making decisions that might not be in their best interest, small businesses are free to pursue whatever strategy they want. The best part about capitalism is that you’re the master of your own destiny.

The terms O’Leary offered to Wicked Good Cupcakes were not unique. Just recently in the 12th episode of Season 5, he offered a $100,000 loan to Tipsy Elves that once repaid, would still require payments in perpetuity in the form of a royalty fee for every sale. That’s an equivalent APR of infinity. In the end, they turned it down and went with Robert Herjavec’s equity offer instead.

Many viewers have taken to twitter to share their doubts about the viability of the Tipsy Elves business model, which is selling ugly Christmas sweaters. That healthy dose of skepticism is something alternative lenders are no strangers to, and as such they tend to price their deals accordingly.

Even deal making that is done on TV in front of millions of witnesses can go sour. Just ask Marcus Lemonis, the star of the TV show The Profit, who recently made a deal with a business in my own backyard, A. Stein Meat Products in Brooklyn, NY. After learning the business was on the brink of insolvency, Lemonis offered them a cash lifeline in exchange for buying their Brooklyn Burger brand at a bargain price of $190,000. In any other circumstances, that deal might not have happened.

Lemonis expeditiously wired them the cash, but never got what he paid for in return. Mora and Buxbaum, the owners, claim the funds were a loan but they have never made a payment. Defaults like these happen every day, especially in alternative business lending.

Hated to do it but here's the update on stein meats and Brooklyn burger. I tried not to but was ignored for 90 days. http://t.co/4oyYOiXK68

— Marcus Lemonis (@marcuslemonis) May 16, 2014

The entrepreneur applies for a business loan, the loan gets made, and the borrower quickly defaults. The result is that the price goes up for the next guy. That’s the risk part that lenders always talk about, the odds that they’re not going to get paid back. If every business repaid their loans, the average cost of financing in alternative business lending would probably be about 6% a year, around what an A rated personal loan costs on LendingClub, instead of the high double digit or triple digit rates that exist now.

Even Kevin O’Leary isn’t taking any chances, hence he protects himself by charging infinity percent interest, and America thanks him every Friday night for blessing entrepreneurs with an opportunity. It’s not the best deal, but it’s A deal.

Small business owners are sophisticated enough to make tough decisions all on their own. That’s the reason we can put them in the public eye, in front of more than 6 million people who either cheer for their success or literally cry out for their demise. These entrepreneurs don’t go on Rainbow & Unicorn Tank, they go on Shark Tank. Sometimes the entrepreneurs walk away with a partner, sometimes they get a loan with infinity percent interest. In the end, it’s their choice, a choice that 36,000 small businesses hoped they would have in 2012. That’s how many applied to be on the show that year.

Business is business and a deal’s a deal. The ball’s always in your court…

Quotes from Kevin O’Leary

Business is war. I go out there, I want to kill the competitors. I want to make their lives miserable. I want to steal their market share. I want them to fear me and I want everyone on my team thinking we’re going to win.

Here’s how I think of my money – as soldiers – I send them out to war everyday. I want them to take prisoners and come home, so there’s more of them.

You may lose your wife, you may lose your dog, your mother may hate you. None of those things matter. What matters is that you achieve success and become free. Then you can do whatever you like.

I’m not a tough guy. I’m just delivering the truth and only the truth and if you can’t deal with it, too bad.

Nobody forces you to work at Wal-Mart. Start your own business! Sell something to Wal-Mart!

Don’t cry about money, it never cries for you.

The only reason to do business is to make money; that’s the only reason for doing business.

Money has no grey areas. You either make it or you lose it.

Working 24 hours a day isn’t enough anymore. You have to be willing to sacrifice everything to be successful, including your personal life, your family life, maybe more. If people think it’s any less, they’re wrong, and they will fail.

I have met many entrepreneurs who have the passion and even the work ethic to succeed – but who are so obsessed with an idea that they don’t see its obvious flaws. Think about that. If you can’t even acknowledge your failures, how can you cut the rope and move on?

I don’t mind rude people. I want people that I can make money with, so if their executional abilities are good, and they’re arrogant and rude, I don’t care.

Can you handle it?

The Real Impact on Small Business

May 22, 2014 It’s not easy being in the lending business. Just talking about money can make people uncomfortable. Bringing up how much money you have, don’t have, or wish you had is like bringing up politics at Thanksgiving dinner. It’s taboo in this society. It’s even rude to ask somebody how much they make a year. That’s one of two reasons why being a lender or loan broker is so difficult, you’re forced to dive head first into emotionally charged waters.

It’s not easy being in the lending business. Just talking about money can make people uncomfortable. Bringing up how much money you have, don’t have, or wish you had is like bringing up politics at Thanksgiving dinner. It’s taboo in this society. It’s even rude to ask somebody how much they make a year. That’s one of two reasons why being a lender or loan broker is so difficult, you’re forced to dive head first into emotionally charged waters.

The second reason is telling an applicant ‘no’. It feels personal even if it’s not. “It’s just business,” the bearer of bad news will say, but it never feels that way. I know that firsthand through my experience as both a broker and an underwriter. Rejection is a painful experience for an applicant no matter how professional they are.

But sometimes you get to tell an applicant ‘yes’ and that can be an emotionally moving experience as well. Looking back, the only applicants I ever heard cry were the ones that got approved. Some of those approvals were expensive but they were given an opportunity in a world where up until that point, no one was willing to give them any opportunity at all. They were the forgotten businesses of America.

PayPal’s VP of SMB Lending recently said that he feels “blessed to be serving this higher need.” Blessed was an interesting word choice. Being able to support small businesses doesn’t just make him feel happy or hopeful or satisfied, it makes him feel blessed.

What is the real impact that alternative financing companies have on small businesses? Thanks to the funding companies who took the time to find out. Today, we can see for ourselves:

Above is just a small handful of the testimonials you can find on the websites of CAN Capital, Kabbage, RapidAdvance, Fora Financial, and Merchant Cash and Capital. Real businesses, real stories, real impact.

And there you have it…