Regulation

Congressman Cleaver’s Findings on Fintech Lending Mixed

August 30, 2018 Congressman Emanuel Cleaver, II from Missouri announced findings earlier this month from a year-long inquiry he initiated into fintech small business lending practices and minorities. His initial inquiry was to determine if merchant cash advance companies had mechanisms in place to avoid discriminatory lending practices.

Congressman Emanuel Cleaver, II from Missouri announced findings earlier this month from a year-long inquiry he initiated into fintech small business lending practices and minorities. His initial inquiry was to determine if merchant cash advance companies had mechanisms in place to avoid discriminatory lending practices.

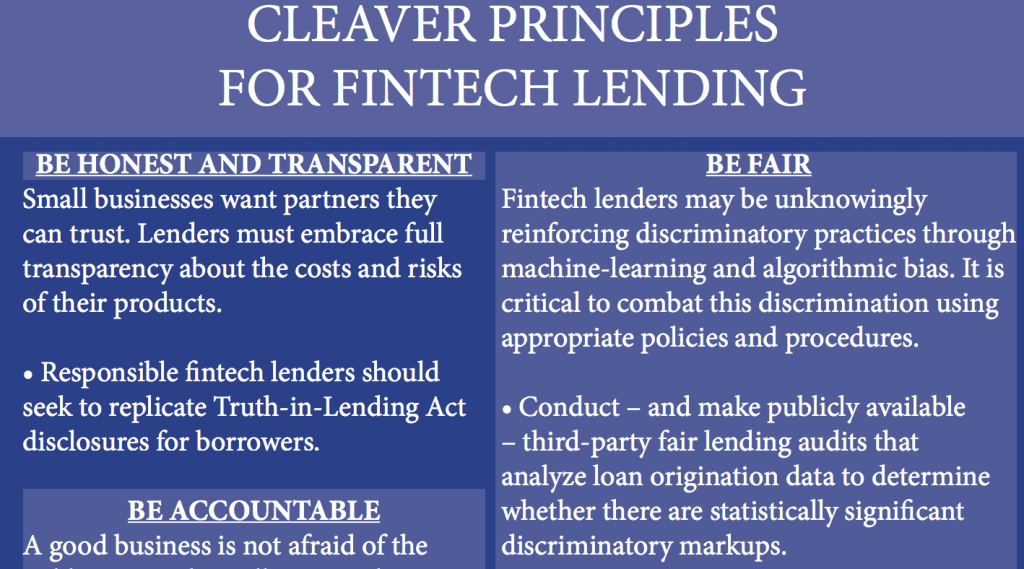

Cleaver concluded that some common practices in non-bank underwriting processes lend themselves to discrimination against minority business owners. One such practice is using a merchant’s personal credit score to determine a business’ credit worthiness, which the report maintains is unfair because “a personal credit score has little bearing on a business model or the owner’s business acumen, and using it unfairly punishes minority business owners who may not have had the same opportunities to build credit.” Another complaint is the common practice of having merchants sign forced arbitration clauses that forbid the borrower to take the lender to court.

The companies that he surveyed included OnDeck, Kabbage, Fora Financial, Lending Club, Biz2Credit and LendUp, even though Lendup only does consumer lending. And OnDeck, Kabbage and Lending Club don’t offer a cash advance product. Still, they make non-bank business loans.

The report also mentioned that algorithms used by some of these companies could inadvertently be discriminatory. That’s because they have the ability to incorporate the number of criminal records and bankruptcies in the merchant applicant’s zip code when making a funding decision. And these numbers tend to be higher in minority neighborhoods.

However, the report also highlighted some good practices, such as including a third party in the lending process to protect from engaging in unintentional discriminatory behavior.

“From the responses gathered,” the report reads, “it has become increasingly clear that a majority of the companies have taken some measure to prevent blatant discrimination. Nevertheless, additional protections are very much needed.”

“The initial findings are clear as day, Congressman Cleaver said in a statement about the report. “We need to further understand how lenders may be intentionally or unintentionally offering higher interest rates to minorities and underserved communities, and work to implement industry-wide best practices.”

The California Business Loan & MCA Disclosure Bill Has Passed

August 30, 2018The bill has passed. With the governor’s signature, all business loan contracts and merchant cash advance contracts in California will soon require a uniform set of formal disclosures including an annualized rate of the total cost. The precise formula for that rate will be determined by the state’s regulatory agency, the Department of Business Oversight.

Update: The bill’s death in committee was challenged by the bill’s author, Senator Steve Glazer, and ultimately allowed to come up for a vote after he complained to the senate majority leader that a committee’s decision is merely a recommendation, not a deciding factor on the bill itself. At 2:10 AM EST, it passed.

Update: The bill has died in the Senate Banking Committee. Daniel Weintraub, who serves as chief of staff to the bill’s author, tweeted after midnight eastern time that the bill was not moving forward.

Thanks to all who supported small business and #SB1235. Unfortunately the Senate Banking Committee killed the bill tonight. We fell one vote short of the four we needed to send the bill to the Senate floor. https://t.co/30ztdW2LbD

— Daniel Weintraub (@DMWeintraub) September 1, 2018

Update: The bill passed the Assembly unopposed and is slated for a late night vote by the Senate Banking Committee.

Update 8/31/18: Today is the last day for the legislature to pass this bill. We will keep you updated

California’s bill to mandate certain disclosures on business loan and merchant cash advance contracts is looking a little bit worse. The Annualized Cost of Capital method (Explained here) that some folks in the industry were accepting of, has been scrapped in favor of whatever formula a state regulator decides to pick. That means if the Commissioner of Business Oversight decides on an APR disclosure, which many industry trade groups believed they had already successfully lobbied against, all loans and non-loans alike would have to report an APR, a mathematical impossibility for a product like merchant cash advance. At present, however, all that is known is that the Commissioner’s choice must be an annualized metric.

According to Bloomberg, the amended version of the bill needs to get approval in both the Assembly and the Senate by Friday before the legislative session ends.

Trade associations that have weighed in on this bill include the Electronic Transactions Association, Commercial Finance Coalition, Small Business Finance Association, and the Innovative Lending Platform Association.

You can view all of our previous coverage about the bill here.

1 Global Capital Charged With Fraud by SEC

August 29, 2018

The Securities & Exchange Commission unsealed a 10-count complaint against 1 Global Capital LLC (“1st Global Capital”), its owner Carl Ruderman, and related parties on Wednesday.

The South Florida firm “fraudulently raised more than $287 million from more than 3,400 investors to fund its business offering short-term financing to small and medium-size businesses,” the complaint begins.

Investors were offered low-risk, high-return investments that 1st Global would use to fund merchant cash advance deals. Ruderman, who owned the company through a trust, misappropriated $35 million of the funds, paying a lot of it to himself and companies he controlled that had nothing to do with MCA, the SEC alleges. Beyond that, millions more went towards other pet projects like a $50 million purchase of distressed credit card debt.

But the deception went deep, the complaint lays out. 1st Global touted a default rate of only 4% despite the fact that 15-18% of their deals over the last 2 years had resulted in collections lawsuits.

By October 2017, the statements investors received showing their monthly performance were faked with the value and performance significantly inflated. By June 2018, one line item on monthly statements (labeled “cash not deployed”) reported that investors collectively had $70 million in idle cash ready to be put into deals. Meanwhile, the company itself only had about $20 million in all of its bank accounts combined, money that was being used for everything including operating expenses, salaries, and commissions.

1st Global’s alleged auditor, Daszkal Bolton, LLP, says they never audited 1st Global’s statements and haven’t had anything to do with the company since 2016. Nonetheless, 1st Global placed Daszkal Bolton’s name on statements given to investors and stated on their website that investor balances were validated by an accounting firm quarterly.

The Seven-Minute Loan Shakes Up Washington And The 50 States

August 19, 2018 It takes seven minutes for Kabbage to approve a small-business loan. “The reason there’s so little lag time,” says Sam Taussig, head of global policy at the Atlanta-based financial technology firm, “is that it’s all automated. Our marginal cost for loans is very low,” he explains, “because everything involving the intake of information – your name and address, know-your-customer, anti-money-laundering and anti-terrorism checks, analyzing three years of income statements, cash-flow analysis – is one-hundred-percent automated. There are no people involved unless red flags go off.”

It takes seven minutes for Kabbage to approve a small-business loan. “The reason there’s so little lag time,” says Sam Taussig, head of global policy at the Atlanta-based financial technology firm, “is that it’s all automated. Our marginal cost for loans is very low,” he explains, “because everything involving the intake of information – your name and address, know-your-customer, anti-money-laundering and anti-terrorism checks, analyzing three years of income statements, cash-flow analysis – is one-hundred-percent automated. There are no people involved unless red flags go off.”

One salient testament to Kabbage’s automation: Fully $1 billion of the $5 billion in loans that it has made to 145,000 discrete borrowers since it opened its portals in 2011 were made between 6 p.m. and 6 a.m.

Now compare that hair-trigger response time and 24-hour service for a small business loan of $1,000-$250,000 with what occurs at a typical bank. “Corporate credit underwriting requires 28 separate tasks to arrive at a decision,” William Phelan, president, and co‐founder of PayNet—a top provider of small-business credit data and analysis – testified recently to a Congressional subcommittee. “These 28 tasks involve (among other things): collecting information for the credit application, reviewing the financial information, data entry and calculations, industry analysis, evaluation of borrower capability, capacity (to repay), and valuation of collateral.”

A “time-series analysis,” the Skokie (Ill.)-based executive went on, found that it takes two-to-three weeks – and often as many as eight weeks—to complete the loan approval process. For this “single credit decision,” Phelan added, the services of three bank departments – relationship manager, credit analyst, and credit committee – are required.

The cost of such a labor-intensive operation? PayNet analysts reckoned that banks incur $4,000-$6,000 in underwriting expenses for each credit application. Phelan said, moreover, that credit underwriting typically includes a subsequent loan review, which consumes two days of effort and costs the bank an additional $1,000. “With these costs,” Phelan told lawmakers, “banks are unable to turn a profit unless the loan size exceeds $500,000.”

According to the National Bureau of Economic Research, the country’s very biggest banks — Bank of America, Citigroup, J.P. Morgan Chase, and Wells Fargo—have been the financial institutions most likely to shut down lending to small businesses. “While small business lending declined at all banks beginning in 2008,” NBER’s September, 2017 report announces, “the four largest banks” which the report dubs the ‘Top Four’—“cut back significantly relative to the rest of the banking sector.”

NBER reports further that by 2010—the “trough” of the financial crisis—the annual flow of loan originations from the Top Four stood at just 41% of its 2006 level, which compared with 66% of the pre-crisis level for all other banks. Moreover, small-business lending at the “Top Four” banks remained suppressed for several years afterward, “hovering” at roughly 50% of its pre crisis level through 2014. By contrast, such lending at the rest of the country’s banks eventually bounced back to nearly 80% of the pre-crisis level by 2014.

That pullback—by all banks—continues, says Kenneth Singleton, an economics professor at Stanford University’s Graduate School of Business. Echoing Phelan’s testimony, Singleton told deBanked in an interview: “Given the high underwriting costs, banks just chose not to make loans under $250,000,” which are the bread-and-butter of small-business loans. In so doing, he adds, banks “have created a vacuum for fintechs.”

All of which helps explain why Kabbage and other fintechs making small business loans are maintaining a strong growth trajectory. As a Federal Reserve report issued in June notes, the five most prominent fintech lenders to small businesses—OnDeck, Kabbage, Credibly, Square Capital, and PayPal—are on track to grow by an estimated 21.5 percent annually through 2021.

Their outsized growth is just one piece—albeit a major one—of fintech’s larger tapestry. Depending on how you define “financial technology,” there are anywhere from 1,400 to 2,000 fintechs operating in the U.S., experts say. Fintech companies are now engaged in online payments, consumer lending, savings and investment vehicles, insurance, and myriad other forms of financial services.

Fintechs’ advocates—a loose confederacy that includes not only industry practitioners but also investors, analysts, academics, and sympathetic government officials—assert that the U.S. fintech industry is nonetheless being blunted from realizing its full potential. If fintechs were allowed to “do their thing,” (as they said in the sixties) this cohort argues, a supercharged industry would bring “financial inclusion” to “unbanked” and “underbanked” populations in the U.S. By “democratizing access to capital,” as Kabbage’s Taussig puts it, harnessing technology would also re-energize the country’s small businesses, which creates the majority of net new jobs in the U.S., according to the U.S. Small Business Administration.

But standing in the way of both innovation and more robust economic growth, this cohort asserts, is a breathtakingly complex—and restrictive—regulatory system that dates back to the Civil War. “I do think we’re victims of our own success in that we’ve got a pretty good financial system and a pretty good regulatory structure where most people can make payments and the vast majority of people can get credit.” says Jo Ann Barefoot, chief executive at Barefoot Innovation Group in Washington, D.C. and a former senior fellow at Harvard’s Kennedy School. But because of that “there’s been more inertia and slower adoption of new technology,” she adds. “People in the U.S. are still going to bank branches more than people in the rest of the world.”

Barefoot adds: “There are five agencies directly overseeing financial services at the Federal level and another two dozen federal agencies” providing some measure of additional, if not duplicative oversight, over financial services. “But there’s no fintech licensing at the national level,” she says. And because each state also has a bank regulator, she notes, “if you’re a fintech innovator, you have to go state by state and spend millions of dollars and take years” to comply with a spool of red tape pertaining to nonbanks.

At the federal level, the current system— which includes the Federal Reserve, Office of the Comptroller of the Currency (OCC), and the Federal Deposit Insurance Corporation (FDIC)—developed over time in a piecemeal fashion, largely through legislative responses to economic panics, shocks and emergencies. “For historical reasons,” Barefoot remarks, “we have a lot of agencies” regulating financial services.

For exhibit A, look no further than the Consumer Financial Protection Bureau created amidst the shambles of the 2008-2009 financial crisis by the 2010 Dodd-Frank Act. Built ostensibly to preserve safety and soundness, the agencies have constructed a moat around the banking system.

Karen Shaw Petrou, managing partner at Federal Financial Analytics, a Washington, D.C. consultancy, is a banking policy expert who frequently provides testimony to Congress and regulatory agencies. She wrote recently that the country’s banking sector has been protected from the kind of technological disruption that has upended a whole bevy of industries.

“The only reason Amazon and its ilk may not do to banking, brokers and insurers what they did to retailers—and are about to do to grocers and pharmacies,” she observed recently in a blog—“is the regulatory structure of each of these businesses. If and how it changes are the most critical strategic factors now facing finance.”

Cornelius Hurley, a Boston University law professor and executive director of the Online Lending Policy Institute, is especially critical of the 50-state, dual banking system. State bank regulators oversee 75 percent of the country’s banks and are the primary regulators of nonbank financial technology companies. “The U.S. is falling behind other countries that are much less balkanized,” Hurley says. “Our federal system of government has served us well in many areas in our becoming a leading civil society. It’s given us NOW (Negotiable Order of Withdrawal) accounts, money-market accounts, automatic teller machines, and interstate banking. But now it’s outlived its usefulness and has become an impediment.”

Take Kabbage, which actually avoids a lot of regulatory rigmarole by virtue of its partnership with Celtic Bank, a Utah-chartered industrial bank. The association with a regulated state bank essentially provides Kabbage with a passport to conduct business across state lines. Nonetheless, Kabbage has multiple, incessant, and confusing dealings with its bank overseers in the 50 states.

“Where the states get involved,” says Taussig, “is on brokering, solicitation, disclosure and privacy. We run into varying degrees of state legislative issues that make it hard to do business. Right now we’re plagued by what’s been happening with national technology actors on cybersecurity breaches and breach disclosures. We are required to notify customers. But some states require that we do it in as few as 36 hours, and in others it’s a couple of months. We’ve lobbied for a national breach law of four days,” he adds, which would “make it easier for everyone operating across the country.”

Then there’s the meaning of “What is a broker?’” says Taussig, who as a regulatory compliance expert at Kabbage sees his role as something of an emissary and educator to regulators and politicians, the news media, and the public. “The definitions haven’t been updated since the 1950s and now we have wildly different interpretations of brokering and solicitation,” he says. “The landscape has changed with e-commerce and each state has a different perspective of what’s kosher on the Internet.”

Washington State is a good example. It’s one of a handful of jurisdictions in which regulators confine nonbank fintechs to making consumer loans. In a kabuki dance, fintech companies apply for a consumer-lending license and then ask for a special dispensation to do small-business lending.

And let’s not forget New Mexico, Nevada and Vermont where a physical “brick-and-mortar” presence is required for a lender to do business. Digital companies, Taussig says, would have to seek a waiver from regulators in those states. “Many companies spend a lot of money on billable hours for local lawyers to comply with policies and procedures,” Taussig reports, “and it doesn’t serve to protect customers. It’s really just revenue extraction.”

All such restraints put fintechs at a disadvantage to traditional financial institutions, which by virtue of a bank charter, enjoy laws guaranteeing parity between state-chartered and federally chartered national banks. The banks are therefore able to traverse state lines seamlessly to take deposits, make loans, and engage in other lines of business. In addition, fintechs’ cost of funds is far higher than banks, which pay depositors a meager interest rate. And banks have access to the Fed discount window, while their depositors’ savings and checking accounts are insured up to $200,000.

The result is a higher cost of funds for fintechs, which principally depend on venture capital, private equity, securitization and debt financing as well as retained earnings. And that translates into steeper charges for small business borrowers. A fintech customer can easily pay an interest rate on a loan or line of credit that’s three to four times higher than, say, a bank loan backed by the U.S. Small Business Administration.

Kabbage, for example, reports that its average loan of roughly $10,000 typically carries an interest rate of 35%-36%. It’s credits are, of course, riskier than the banks’. The company does not report figures on loans denied, Taussig told deBanked, but Stanford’s Singleton says that the fintech industry’s denial rate is roughly 50 percent for small business loans. “Fintechs have higher costs of capital and they’re also facing moderate default rates,” notes Singleton. “They’re not enormous, but fintechs are dealing with a different segment. Small businesses have much more variability in cash flows, so lending could be riskier than larger, established companies.”

Even so, venture capitalists continue to pour money into fintech start-ups. “I’ve gone to several conferences,” Singleton says, “and everywhere I turn I’m meeting people from a new fintech company. One of the striking things about this space,” he adds, “is that there are lot of aspiring start-ups attacking very specific, very narrow issues. Not all will survive, but someone will probably acquire them.”

Even so, venture capitalists continue to pour money into fintech start-ups. “I’ve gone to several conferences,” Singleton says, “and everywhere I turn I’m meeting people from a new fintech company. One of the striking things about this space,” he adds, “is that there are lot of aspiring start-ups attacking very specific, very narrow issues. Not all will survive, but someone will probably acquire them.”

Contrast that to the world of banking. Many banks are wholeheartedly embracing technology by collaborating with fintechs, acquiring start-ups with promising technology, or developing in-house solutions. Among the most impressive are super-regionals Fifth Third Bank ($142.2 billion), Regions Financial Corp. ($123.5 billion), and BBVA Compass ($69.6 billion), notes Miami-based bank consultant Charles Wendel. But many banks are content to cater to familiar customers and remain complacent. One result is that there’s been a steady diminution in the number of U.S. banks.

Over the past ten years, fully one-third of the country’s banks were swallowed whole in an acquisition, disappeared in a merger, failed, or otherwise closed their doors. There were 5,670 federally insured banks at the end of 2017, according to the Federal Deposit Insurance Corp., a 2,863-bank, 33.5% decrease from the 8,533 commercial banks operating in the U.S. in 2007.

It does appear that, to paraphrase an old expression, many banks “are going out of style.” In recent years there have been more banking industry deaths than births. Sixty-three banks have failed since 2013 through June while only 14 de novo banks have been launched. In Texas, which is known for having the most banks of any state in the country, only one newly minted bank debuted since 2009. (The Bank of Austin is the new kid on the Texas block, opening in a city known as a hotbed of technology with its “Silicon Hills.”)

One reason there’s so little enthusiasm among venture capitalists and other financial backers for investing in de novo banks is that regulators are known to be austere. “If you’re a company in the U.S.,” says Matt Burton, a founder of data analytics firm Orchard Platform Markets (which was recently acquired by Kabbage), “and you tell regulators that you want to grow by 100 percent a year – which is the scale you must grow at to get venture-capital funding – regulators will freak out. Bank regulators are very, very strict. That’s why you never hear about new banks achieving any sort of scale.”

But while bank regulators “are moving sluggishly compared to the rest of the world” in adapting to the fintech revolution, says Singleton, there are numerous signs that the status quo may be in for a surprising jolt. The Treasury Department is about to issue (possibly by the time this story is published) a major report recommending an across-the-board overhaul in the regulatory stance toward all nonbank financials, including fintechs. According to a report in The American Banker, Craig Phillips, counselor to Treasury Secretary Steven Mnuchin, told a trade group that the report would address regulatory shortcomings and especially “regulatory asymmetries” between fintech firms and regulated financial institutions.

Christopher Cole, senior regulatory counsel at the Independent Community Bankers Association—a Washington, D.C. trade association representing the country’s Main Street bankers—told deBanked that, among other things, the Treasury report would likely recommend “regulatory sandboxes.” (A regulatory sandbox allows businesses to experiment with innovative products, services, and business models in the marketplace, usually for a specified period of time.)

That’s an idea that fintech proponents have been drumming enthusiastically since it was pioneered in the U.K. a few years ago, and it’s something that the independent bankers’ lobby, whose member banks are among the most threatened by fintech small-business lenders, says it too can support. Treasury’s Phillips “has said in the past that he’d like to see a level playing field,” the ICBA’s Cole says. “So if (regulators) are going to allow a sandbox, any company could be involved, including a community bank. We agree with him, of course, because we’d like to take advantage of that.”

In March, 2018, Arizona became the first state to establish a regulatory sandbox when the governor signed a law directing that state’s attorney general (and not the state’s banking regulator) to oversee the program. The agency will begin taking applications in August with approval in 90 days, says Paul Watkins, civil litigation chief in the AG’s office. Watkins told deBanked that he’s been most surprised so far by “the degree of enthusiasm” from overseas companies. With the advent of the sandbox, he adds, “Landlocked Arizona has become a port state.”

The OCC, which is part of the Treasury Department, may also revive its plan to issue a national bank charter to fintechs, sources say (EDITOR’S NOTE: This had not yet been implemented before this story went to print. The OCC is now accepting such applications) – a hugely controversial proposal that was put on ice last year (and some thought left for dead) when former Commissioner Thomas J. Curry’s tenure ended last spring. At his departure, the fintech bank charter faced a lawsuit filed by both the New York State Banking Department and the Conference of State Bank Supervisors. (Since then, the lawsuit was tossed out by the courts on the ground that the case was not “ripe” – that is, it was too soon for plaintiffs to show injury).

The OCC, which is part of the Treasury Department, may also revive its plan to issue a national bank charter to fintechs, sources say (EDITOR’S NOTE: This had not yet been implemented before this story went to print. The OCC is now accepting such applications) – a hugely controversial proposal that was put on ice last year (and some thought left for dead) when former Commissioner Thomas J. Curry’s tenure ended last spring. At his departure, the fintech bank charter faced a lawsuit filed by both the New York State Banking Department and the Conference of State Bank Supervisors. (Since then, the lawsuit was tossed out by the courts on the ground that the case was not “ripe” – that is, it was too soon for plaintiffs to show injury).

Taussig, the regulatory expert at Kabbage, reports that the Comptroller of the Currency, Robert J. Otting, has promised “a thumbs-up or thumbs-down” decision by the end of July or early August on issuing fintechs a national bank charter. He counts himself as “hopeful” that OCC’s decision will see both of the regulator’s thumbs pointing north.

The Conference of State Bank Supervisors, meanwhile, has extended an olive branch to the fintech community in the form of “Vision 2020.” CSBS touts the program as “an initiative to modernize state regulation of non-bank financial companies.” As part of Vision 2020, CSBS formed a 21-member “Fintech Industry Advisory Panel” with a recognizable roster of industry stalwarts: small business lenders Kabbage and OnDeck Capital are on board, as are consumer lenders like Funding Circle, LendUp and SoFi Lending Corp. The panel also boasts such heavyweights in payments as Amazon and Microsoft.

Working closely with the fintech industry is a “key component” of Vision 2020, Margaret Liu, deputy general counsel at CSBS, told deBanked in a recent telephone interview. CSBS and the fintech industry are “having a dialogue,” she says, “and we’re asking industry to work together (with us) and bring us a handful of top recommendations on what states can do to improve regulation of nonbanks in licensing, regulations, and examinations.

“We want to know,” she added, ‘What the main friction points are so that we can find a path forward. We want to hear their concerns and talk about pain points. We want them to know the states are not deaf and blind to their concerns.”

Can Fintech Startups Become Banks? OCC Opens The Gates

August 1, 2018 Yesterday, the U.S. Treasury Department released a report that prompted the Office of the Comptroller of the Currency (OCC) to say that it would start accepting applications from fintech for special purpose national bank charters.

Yesterday, the U.S. Treasury Department released a report that prompted the Office of the Comptroller of the Currency (OCC) to say that it would start accepting applications from fintech for special purpose national bank charters.

This is boon for fintech companies that, until now, have mostly been prevented from applying for national bank charters because of protest from banks and others that they will not be subject to adequate regulations. But now the OCC, a significant regulator, is opening the door for non-depository fintech companies – like OnDeck and Kabbage – to become banks.

“Over the past 150 years banks and the federal banking system have been the source of tremendous innovation that has improved banking services and made them more accessible to millions,” said head of the OCC, Comptroller of the Currency, Joseph M. Otting, in a statement. “The federal banking system must continue to evolve and embrace innovation to meet the changing customer needs and serve as a source of strength for the nation’s economy…Companies that provide banking services in innovative ways deserve the opportunity to pursue that business on a national scale as a federally chartered, regulated bank.”

The main advantage for fintech companies of having the opportunity to get their own bank charter is that they would now be able to operate nationwide under a single licensing and regulatory system, instead of a myriad of state licenses. Currently, fintech companies must adhere to the regulations in each state where they do business, which can be expensive. And some states have regulations that are stricter than others. That is why this news is bad news for states that feel that this development will allow fintech companies to bypass and undermine their regulation designed to protect consumers.

The OCC’s decision is the latest development in a years long, sustained effort by fintechs to become banks. In fact, for the last several years, Fintech companies have tried attaining bank status by getting the Utah Department of Financial Institutions to allow them to become Industrial Loan Company (ILC) banks. So far, Square, SoFi and NelNet have tried, in some capacity, to become an ILC bank.

The New York Department of Financial Service and the Conference of State Bank Supervisors (CSBS) was angered by the OCC’s decision.

“An OCC fintech charter is a regulatory train wreck in the making,” said CSBS President John W. Ryan in a statement. “Such a move exceeds the current authority granted by Congress to the OCC. Fintech charter decisions would place the federal government in the business of picking winners and losers in the marketplace. And taxpayers would be exposed to a new risk: failed fintechs.”

He said that his organization is keeping all options open to stop what he says is regulatory overreach.

The OCC indicated in its announcement that fintech companies that become special purpose national banks will be subject to heightened supervision initially, similar to other banks. But these special purpose banks would not have to abide by the stricter regulations of deposit-taking banks and they would not have to be insured by the Federal Deposit Insurance Corporation (FDIC) either.

“It is hard to conceive that insured national banks will allow the OCC to allow a fintech entity a national bank charter without insisting that all national bank obligations apply—which is what fintech companies want to avoid,” said Joseph Lynyak, partner and regulatory reform specialist at the law firm Dorsey & Whitney.

Elevate Explains Why Ohio Payday Law Won’t Hurt Them

July 31, 2018 In Elevate’s Q2 2018 conference call yesterday, Chairman and CEO Kenneth Rees mentioned that Elevate wasn’t worried about an Ohio bill, signed into law yesterday, that places significant restrictions on what payday lenders can do in the state.

In Elevate’s Q2 2018 conference call yesterday, Chairman and CEO Kenneth Rees mentioned that Elevate wasn’t worried about an Ohio bill, signed into law yesterday, that places significant restrictions on what payday lenders can do in the state.

The Fairness in Lending Act (House Bill 123) will close a loophole that payday lenders have been using to bypass the state’s 28 percent maximum APR on loans. The law will go into effect at the end of October of this year.

“We don’t believe this legislation will have a material impact on our business for a couple of reasons,” Rees said on the earnings call. “First, the law would only impact our RISE product…and we believe we can migrate most of our RISE customers in Ohio into an Elastic loan or a Today Credit Card.”

Elevate’s RISE product provides unsecured installment loans and lines of credit, while the company’s Elastic product, its most popular, is a bank issued line of credit. Elevate’s Today Credit Card, a partnership with Mastercard, was just launched and is unique in that it offers prime-like features to subprime customers.

The other reason why Rees is not very concerned about the new law is because he said that that RISE Ohio only represents less than five percent of the company’s total consolidated loan balances. Rees said that there may even be opportunity resulting from Ohio’s new Fairness in Lending Act because he said the law will likely reduce credit availability, potentially creating increased demand for Elevate’s Elastic and Today Card products, which he indicated would be acceptable under the new law. The new law does the following:

- Limits loans to a maximum of $1,000.

- Limits loan terms to 12 months.

- Caps the cost of the loan – fees and interest – to 60 percent of the loan’s original principal.

- Prohibits loans under 90 days unless the monthly payment is not more than 7 percent of a borrower’s monthly net income or 6 percent of gross income.

- Prohibits borrowers from carrying more than a $2,500 outstanding principal across several loans. Payday lenders would have to make their best effort to check their commonly available data to figure out where else people might have loans. The bill also authorizes the state to create a database for lenders to consult.

- Allows lenders to charge a monthly maintenance fee that’s the lesser of 10 percent of the loan’s principal or $30.

- Requires lenders to provide the consumers with a sample repayment schedule based on affordability for loans that last longer than 90 days.

- Prohibits harassing phone calls from lenders.

- Requires lenders to provide loan cost information orally and in writing.

- Gives borrowers 72 hours to change their minds about the loans and return the money, without paying any fees.

Apart from brief discussion of the minimal impact of this new Ohio law, Elevate shared its Q2 revenue of $184.4 million, a 22.5 percent increase over last year at the same time.

CA Bill to Revise Definition of Broker: 6/27/18 Hearing Transcript & Video (AB 3207)

July 29, 2018AB 3207 – CA Bill to Revise the definition of broker (6/27/18)

[0:00:02]

Bradford: We started as a subcommittee. We've already heard Assembly Member Arambula’s Bill AB 1289. Do we have a quorum? We’re gonna ask the secretary to call the roll and establish the quorum.

Speaker: Senator Bradford.

Bradford: Here.

Speaker: Bradford here. Vidak.

Vidak: Present.

Speaker: Vidak here. Gaines. Galgiani.

Galgiani: Here.

Speaker: Galgiani here. Hueso.

Hueso: Here.

Speaker: Hueso here. Lara.

Lara: Here.

Speaker: Lara here. Portantino.

Bradford: Quorum is established. So, we have only one other vehicle that will be heard today. That’s AB 3207 by Assembly Woman Limon and she is here present. And when you’re ready, Ms. Limon, you can make your presentation.

Limon: Great. Thank you, Chair. I wanna start off by taking the committee amendments and committing to work on any concerns addressed in the committee analysis. AB 3207 will provide important consumer protections for the thousands of consumers and small business owners who are served by finance lenders and brokers licensed under the California Financing Law. Under existing law, the definition of broker is vague and circular, leading to the confusion from lenders about which entities they can partner with when arranging loans. Further, the definition of broker in existing law was formulated long before the rise of the internet and the evolution of online lead generation. So, our laws need to be updated with this online activity in mind. Lead generators provide valuable marketing services to a wide range of industries and this bill contains a specific exemption clarifying that distribution of marketing materials or factual information about a lender is not a broker brokering activity. However, many online lender generators that serve the lending industry provide more than just marketing services. These entities act as brokers when they bring borrowers and lenders together to arrange a loan based on confidential data provided by a consumer or small business owner. This bill will allow online lead generators to continue to operate in California. Simply, this bill requires 3 basic things from these companies. One, get a business license from the State Department of Business Oversight; two, provide transparent disclosures to the customers; and three, obtain your customer’s consent before selling and transmitting their confidential data. Arguments from the opposition that this bill will cause lead generators to leave the state raise an important question. Why would a bill focused on licensure and transparency cause a small business to leave a very lucrative California market? Over the past 5 months, I have worked extensively with lenders and lead generators to ensure that this bill appropriately addresses the consumer protection concerns in our lending markets without placing unnecessary burdens on the businesses that work in this area. None of these companies have threatened to leave the state. In fact, many of them have applauded the efforts to bring clarity to existing law and bring bad actors out of the shadows and into the light. This bill has the support of consumer and commercial lenders, the Department of Business Oversight, and a coalition of consumer advocates who are here today to voice their support. With me, I have Adam Wright, senior counsel in the enforcement division in the Department of Business Oversight, to answer any questions from the committee.

Bradford: Witnesses and support, please come forward. State your name, organization.

Martindale: Chair Member, Suzanne Martindale with Consumers Union. We do support this measure and really appreciate the author's leadership in seeking to ensure that our laws stay up to date in terms of evolving technologies. Of course, a lot of lending now happens online and the business models have shifted, but that does not mean that consumers are not, you know, any less entitled to receiving protections when third parties acting on behalf of lenders are marketing to them and helping facilitate the origination of loans and also in particular handling sensitive information and the kinds of things that we wanna always ensure are protected. So, we understand that there’s potentially more discussion to be had about finding the sweet spot here, but I really, really think that the time is now to move forward and ensure that the DBO has the enforcement tools that it needs to properly regulate the space so that consumers who receive online loans are no less protected than those who get them in brick and mortar stores. So, for these reasons, we support and request an aye vote.

Bradford: Thank you. Additional witnesses and support.

Coleman: Good afternoon. Ronald Coleman here on behalf of the California Low Income Consumer Coalition (CLICC). Also here in strong support.

Bradford: Thank you.

Aponte-Diaz: Hi. Graciela Aponte-Diaz, Center for Responsible Lending. Also in strong support.

Bradford: Thank you.

Joyce: Hello. Pat Joyce on behalf of Credit Karma. Credit Karma actually has a neutral position on the bill and wanted the opportunity to thank the author and sponsors of the bill for working with us to address our concerns and allow us to remove our opposition. So, thank you.

Bradford: Thank you very much. Next witness.

Preity: Sumanta Preity on behalf of OnDeck Capital. In support of the bill.

Bradford: Thank you.

Glad: Margaret Glad on behalf of NerdWallet.

[0:05:01]

We’re also in that tweener category. We’d been working very productively with the author's office and particularly Mr. Burdock. We appreciate their amendments that they’ve made to date to address NerdWallet’s concerns. We have a couple of more issues related to disclosures as the bill currently stands. They are mandated disclosures that don't represent our business model. We’d have to tell consumers we’re doing things we aren't doing. So, we're continuing to work with the author and his and her staff to resolve those issues. We appreciate the committee's thorough analysis and all the work and hope to come to resolution of our remaining issues.

Bradford: Great. Thank you.

Pappas: Emily Pappas on behalf of Lending Tree. Similar position to what Margaret just said. Our client has generally supported the framework on this bill. We virtually had an opposed and less amended position due to some of the disclosure requirements. However, we learn from the author's office today that they'd be willing to take the amendments that relieve us of our concerns. Therefore, we’ll switch to a neutral position.

Bradford: Thank you. Any additional witnesses in support? Witnesses in opposition.

Quinton: Hi. David Quinton on behalf of the Online Lenders Alliance. I do have a clarifying question. We are in strong opposition as the bill was in print. We've heard discussion about amendments. If all of the amendments that were in the analysis were accepted, I think that moves us to neutral, but we're not clear on that at this point. So, I’m not sure how to proceed.

Bradford: Those are the amendments that we’re referring to that weren’t announced as well as we’re addressing the concerns that we’re raised as well in the bill.

Quinton: Would that be possible so we can—

Bradford: I’m sorry?

Quinton: Oh, she was— I’m sorry. I was listening.

Bradford: Ms. Galgiani.

Bradford: Yeah. Yeah. If you want to, Ms.—

Quinton: Okay. Thank you.

Galgiani: I would just like to clarify with the author the amendments that have been agreed to and looking through the analysis and then trying to complete which all of those are. I wanna make sure that we're on the same page; the author, the members, the opposition. And there are two concerns that I’ll start with that we don't have expressed amendments for, but we're hoping that you'll work with the opposition and your stakeholders over the July break and we can come back and address those. And one is dealing with lead generators being designated assets as opposed to being referred to as brokers and that those lead generators hold the generator licenses. That's a concern. And the other concern is imposing the same standard of liability on lead generators for the acts of those from whom they buy leads as the bill imposes on lenders for the acts of lead generators from whom they buy leads.

Limon: So, I can say that we continue the conversations. it's definitely not a problem. I think that, you know, this bill has gone through 6 rounds of amendments. And so, I think that's reflective of the fact that we continue to have the conversation. On the two separate license definitions, what we know is that creating two separate license licenses for brokers and lead generators would require many companies to attain two separate licenses from the DBO. Additionally, drafting a separate regulatory framework for lead generators would also add confusion for the businesses that would need to decide whether they need a lead generator or a broker license. The bill does require to have one license right now. And the bill provides specific disclosure requirements that makes sense in terms of the online generation world. So, that's kind of where we've been thinking about it in terms of that. In terms of the lender liability, the bill and existing law hold licensees accountable for their own actions. So, both the lenders and the brokers are liable for violations of the law that occur within their companies. For licensed brokers who choose to obtain referrals from unlicensed third party, the bill requires those brokers to establish policies and procedures intended to ensure that those unlicensed parties uphold the consumer protections provided by the law. The issue of the lender liability raised in the analysis is a red herring. Just as existing current law, the bill would continue to practice the practice of holding licensees accountable for their own violations. And I just wanna again say that that's current law.

Galgiani: Okay. So, am I hearing—

Limon: You are hearing that we are happy to continue those conversations. You brought up the two concerns and I wanted to share the feedback on those two concerns.

Bradford: But we're still open to move forward in having— resolve our differences as it relates to the two— those two concerns. We’re not gonna split the baby here today, but we’re gonna try to figure out how to move forward on those concerns.

[0:10:03]

So, we have that commitment as we move forward to address it in a way that we all come together. Am I correct?

Limon: You have the commitment to continue the conversation to try to figure out a way to address it.

Bradford: Yes, sir.

Quinton: So, on the issue of the two remaining issues, so we thank the author for taking the amendments as presented by your consultant in the analysis. But of the two remaining issues, I believe the broker issue is one that we can work with. That's fine. The devil is in the details. The problem is with this issue, as you know, the details have details. It’s a very, very complex issue. So, that’s our one concern, but we can work with the broker issue. I think we’re okay with that. That's fine as it is. However, being held for strict liability for the actions of a third party affiliate is a very far reaching legal standard and we have really serious concerns with that. So, we just wanna clarify if it is still that we are held with strict liability for the actions of a third party affiliate like we would still have to oppose the bill with that. So, I just want clarification on that, Mr. Chairman.

Bradford: Well, as far as that concern, I'm hoping we're gonna sit down at the table again during the break and whittle that out and figure out how we come to consensus. And I understand your concerns and that's why they're still listed as concerns. They haven't been amended in the bill. But hopefully, going forward, we will find some solution or amendment to address that for you.

Quinton: So, I think at this point— to finish my statement and I’ll hand it over very briefly to Jason— at this point, I would say that we would still be opposed until we can see that amendment because that is a very, very serious issue that could hold us liable over issues we have no authority over. And I’d like to introduce Mr. Jason Romrell who is with Lead Smart, one of the leading lead generators in the State of California.

Romrell: Thank you. Chairman and committee members, thank you for allowing me to speak on AB 3207. The thing that I want to make clear, we’re a California-based lead generator. We have a sister company that has a DTL and CFL license. We’ve had those for the last 5 years. Our interest in this bill is not to oppose to bill. It’s to make sure that the good lead generators, the lead generators who function ethically are still allowed to function in fintech environment that is becoming the movement. If we don't do that, we are putting consumers at a huge disadvantage. In fact, we’re putting them at more risk than they’re at now. We have been involved in this discussion with the DBO, with members of the legislature, and even on the federal level for many years. So, the role that we play as a good ethical lead generator is a very important consumer protection role. We have the same objective as Assembly Member Limon. We have the same objective as the DBO. It's to protect consumers. So, the issues that we were facing prior to the amendments being put forward were in the details. There is no opposition to the concept. We want to be here to protect consumers, but it is the details. So, the one thing I do want to mention is lead generation is complex. There a lot of layers to it. It is not a one size fits all activity. And that is one of the challenges in crafting good legislation. So, I'm not going to go into the details that we had issues with because I think, in light of these potential amendments, everything has changed. But what I do wanna point out is the distinction between the good lead generators and the bad lead generators. The good lead generators already do a lot of what is in AB 3207. We get consent. We vet our lenders. We make sure the marketing message that goes to the consumer is accurate, truthful, and proper. We do a lot of that work, and it's time consuming, and it takes a lot of money and energy. The bad lead generators do not care. So, the risk we run with legislation is if we over legislate the good guys. We will. And Assembly Members Limon asked the question “Why would a small business leave California?” If we can't function without the threat of class action lawsuits, if we literally cannot comply with the details of a bill, we’ll move to other markets. If we do that, consumers are injured severely. So, my plea to this committee and to Assembly Member Limon is we are here. We are invested in the process. We want to get it right. We don't want to oppose the bill. We want to make it work for us and for California consumers.

[0:15:02]

And that is our position, is to protect the people that we live and work with everyday.

Bradford: Thank you. Any additional witnesses in opposition?

Bauer: Paul Bauer on behalf of Elevate. I’m kind of in that tweener category that other people have step forward in. I just wanted to lend our voice to those of Mr. Quinton and Mr. Romrell who presented. And we also wanna see the bill be perfected as we move forward. So, I look forward to that work.

Bradford: Thank you. I appreciate it.

Sunley: Alex Sunley on behalf of the Small Business Finance Association. In opposition.

Bradford: Thank you.

Damar: Hi, Dominic Damar here on behalf of Innova. I share Mr. Bauer’s and [0:15:49][Inaudible] position relative to the amendments and look forward to working and hearing from the author on changes to be made. Thank you.

Bradford: Thank you.

Conaway: Good afternoon. This is Jerry Conaway on behalf of Lead Flash. And we're currently in opposition, but looking forward to seeing the amendments. And I'm working with the bill's author to make a great bill. Thank you.

Bradford: Thank you.

Smeltzer: Thank you, Mister Chair and members. Jason Smeltzer here on behalf of the California Financial Service Providers. Also the same position as Mr. Quinton. I would love to see the assembly member and work this out and remove our opposition then.

Bradford: Thank you.

Schriver: Rachel Schriver with the TMX Finance Family of Companies. We’re opposed to the bill in print, but certainly optimistic about finding a path forward.

Bradford: I appreciate it. Any additional witnesses? Any tweeners? All right. We’ll bring it back to the committee. Any questions by the committee members? Mr. Ric Lara. No. Oh. Oh okay. Ms.—

Lara: I just wanna move the bill, but I know Ms. Galgiani—

Galgiani: I wanted to finish and—

Bradford: Yes. Oh, go ahead, Ms. Galgiani.

Galgiani: We’ve done a lot of work on this bill—

Bradford: Yes, we have.

Galgiani: …today and I’ve been in two other committees today since 9 o’clock this morning. So, I wanna make sure we’re on the same page. So, the second item amendment that would provide exemptions from lead generator definition for administrative and clerical tasks, credit bureaus, internet search engines, and social media platforms, has that amendment been agreed to? That's on Page 14B in the analysis. Page 14B addresses the concern. And so, the amendment would be to provide an exemption for those clerical staff, etc.

Wright: And this is Adam Wright on behalf of the DBO. When it comes to that request, we do not believe it's necessary because of the way that the activities are already drafted. We do not believe that it covers search engines or social media advertisements because those two mediums of advertisements do not send actual consumer data to lenders and they are not paid on a per successful loan basis. Thus, they would not be caught up on the activities under a broker.

Galgiani: Okay. Okay. So, what is the amendment that you're taking then because it sounds like no? Am I right or— Maybe we should start with the author sharing with us the amendments that she’s taking because—

Bradford: You know, we’ve spent a whole lot of time in all due respect to the author and to those who are opposing this bill, but a lot of time have been invested here. And we wanna have a vehicle that first protects consumers, but also allows the industry to thrive and survive here in California. And I think the amendments that we've put forth I thought we had understanding and a commitment that we're gonna continue to move forward and keep this vehicle alive and understanding that we have some kind of agreement, but—

Limon: So, here's the deal, right? So, if you look on Page 13 and it says amendments and it describes some of the issues, but there's not specific amendments. So, according to the author’s office, the use of the word “expresses” intends to [0:18:54][Inaudible] consent. Right? We can go on. And so, I think that that’s what we have to continue talking about. Because in the areas where there is very specific things, it’s easier to say yes or no. In the areas where it talks about a concern, but it doesn't give you actual language, that's where we're trying to figure out how.

Bradford: And we’re not gonna find that extra language here today. What we're trying to get clarity on is what has been put forth in analysis those concerns that were raised as well as those amendments that we suggested that we get agreement on that today and we’ll work out the details moving forward with the understanding that we come to agreement, we’ll pull this bill back to the committee.

Limon: Yes. We can provide clarity for all of these amendments. We are just looking for actual language.

Galgiani: Are we drafting those amendments in committee? Committee staff will draft those amendments.

Bradford: Yes.

Limon: Can we draft the amendments and provide them to you?

Bradford: No. I think this committee will work in concert with you in drafting those amendments. That's our understanding of finding common ground on what we have already in analysis.

[0:20:01]

Limon: As long as our office and as the author I’m able to also be part of that, I—

Bradford: That’s our understanding that we’re gonna work in collaboration as we move forward on this thing.

Galgiani: Okay.

Bradford: Galgiani.

Galgiani: Okay. Next, item #4 on my list of concerns in amendments, define term “express consent” and provide the express consent provided by a prospective borrower to one entity satisfies the requirement for all other entities that purchase a consumer's confidential data to obtain express consent and that is addressing the concern outlined on Page 13A of the analysis.

Limon: So, back to the concerns, we’re happy to have a conversation. I’m trying to go to the amendments. So, we are happy to clarify it. So, here’s the confusion, right, that you have some amendments and we've agreed to take those and to work together and then you have the concerns. And the concerns I think need a discussion. We weren't prepared to go back and forth on the concerns here.

Bradford: We’re not trying to do that. So, we're trying to get clarity on those amendments that have been identified, but also address those concerns moving forward as well the two areas of concerns that are being raised so we can keep this vehicle alive and continue our discussion. So, we're—

Limon: We’re I think on the same page that the concerns we need to keep talking about the amendments, we are agreeing to work together on language.

Bradford: I understand that. We have specific amendments that we’re trying to get agreement on today. The concerns, we can work out. You know, that's going forward, but the amendments that we have before, today, we’re trying to get clarity on it. Senator Lara.

Lara: Without skipping over Senator Galgiani, my understanding is that she's already agreed to the amendments.

Galgiani: And we're trying to clarify what those amendments are—

Lara: Okay.

Galgiani: …specifically so that we don't just leave it to the fact that there's going to be a discussion—

Lara: Understood. Understood.

Galgiani: …in July. We want clarity on very specific amendments.

Limon: I started by saying I agree to the amendments. And so, if there are, you know, clear amendments, that's easy because there's language. If there's not language, we have to have a discussion. And what I heard was that we were simultaneously gonna draft those, that language.

Galgiani: And I'm trying to go through those amendments item by item so that we're on the same page and the two that I outlined—

Bradford: Ms. Galgiani, I think what we’re gonna have discussion on and negotiations is on the concerns, but the amendments or the amendments that we’re trying to get commitment on today, the amendments that we have that we're in an analysis that were clearly spelled out in analysis, you're taking those.

Limon: Yes.

Bradford: Great.

Galgiani: And the committee staff is drafting this.

Bradford: Yes. Yes.

Limon: With collaboration from our office so we—

Bradford: That’s right.

Limon: …can draft them together.

Galgiani: Okay. Okay. So, I’ll continue to the fifth one. Requiring that the entity that collects a prospective borrower’s confidential data to provide that borrower with the disclosure described in section 22348. So, in essence, the original point person who collected the personal information is the person who is required to provide the disclosure.

Limon: Uh-huh.

Galgiani: Okay. Number 6, add two additional statements to the disclosure described in section 22348 (A) lenders to whom the prospective borrower is referred may separately contact the prospective borrower and (B) lenders to whom the prospective borrower is referred may separately contact the prospective borrower.

Limon: Yup.

Galgiani: Okay. Number 7, delete the disclosure required under Section 22338.5.

Limon: So, wait—

Galgiani: Okay. And that’s on Page 23—

Limon: You know, I have agreed to the amendments whether it’s clear language. And so, yeah.

Bradford: Okay.

Limon: I think that this feels like it’s leading into a conversation and I just— We wanna have that conversation.

Bradford: Well, I’m gonna go on record right now. The amendments that we have before that was in analysis, I wanna be clear those are the ones you’re agreeing to and we’ll continue to work out the concerns. Am I correct?

Limon: Yes.

Bradford: And if we deviate from that, we will pull the bill back to this committee.

Limon: Right. And we will work together on drafting the language so that it's not just— Right?

Bradford: Drafting the language as it relates to the concerns. Yes. If we all have agreement on that—

Lara: [0:24:51][Inaudible]

Bradford: Exactly. So, we’re taking the amendments that are in the committee’s analysis.

[0:25:00]

That’s the motion you're putting forth, Ms. Galgiani.

Galgiani: Yes.

Bradford: Yes. Yes. Okay. Great. Any additional questions or comments by committee?

Speaker: As amended.

Bradford: As amended. Ms. Limon, would you like to close?

Limon: Unlicensed brokering activity poses a risk to consumer’s financial well-being and this bill will ensure that California's financial regulator can enforce the consumer protections under the California Financing Law. For this reason, today, I ask you for an aye vote.

Bradford: So, we have a motion and it’s do pass as amended to appropriations based on committee analysis. And we will move forward in addressing the concerns as we move forward. Am I correct? So, that’s the understanding then, Secretary, of our amendment. Madam chief consultant, that’s our understanding? Great. All right. Do pass as amended and committee analysis. Madam Secretary, please call the roll.

Speaker: Assembly Bill 3207, motion is do pass as amended to appropriation. Senator Bradford.

Bradford: Aye.

Speaker: Bradford Aye. Vidak.

Vidak: No.

Speaker: Vidak no. Gaines. Galgiani.

Galgiani: Aye.

Speaker: Galgiani aye. Hueso.

Hueso: Aye.

Speaker: Hueso aye. Lara.

Lara: Aye.

Speaker: Lara aye. Portantino.

Portantino: Aye.

Speaker: Portantino aye. We have 5 to 1.

Bradford: All right. Your bill is out.

Limon: Thank you.

Bradford: Thank you. And we look forward to our continued discussion and work on this issue.

[0:26:28] End of Audio

BCFP Launches Regulatory Sandbox for Fintech Companies

July 23, 2018

Mick Mulvaney, the Acting Director of the Bureau of Consumer Financial Protection (Bureau), told The Wall Street Journal last week that the Bureau has launched a “regulatory sandbox” to help fintech firms develop new products and services.

A regulatory sandbox is a framework set up by a regulator that allows certain fintech companies to conduct experiments for innovative products under the supervision of the regulator. The launch of this BCFP regulatory sandbox coincides with the hiring of Paul Watkins last week as Director of the Bureau’s new Office of Innovation.

It would seem no coincidence that Watkins was chosen to direct this new office at the Bureau because he had been in charge of fintech initiatives at the Attorney General’s Office in Arizona, the first state to create a regulatory sandbox earlier this year. Illinois is the process of creating a regulatory sandbox. And state banking regulators in New England spoke to deBanked last year about the possibility of a regional regulatory sandbox. According to an American Banker story, the model for the sandbox follows a 2014 initiative in the UK called Project Innovate, designed to promote competition while focusing on consumer interests. Currently, regulatory sandboxes have been implemented in other countries, including Abu Dhabi, Australia, Canada, Denmark, Hong Kong and Singapore, according to the New York University Journal of Law and Business.

Regulatory sandboxes are controversial. Before the Arizona bill passed allowing for the creation of the regulatory sandbox, a number of consumer advocacy groups protested, including the Southwest Center for Economic Integrity, Arizona Community Action Association, Children’s Action Alliance, and Protecting Arizona’s Family Coalition. These groups believe that the regulatory sandbox is simply a way of allowing fintech companies to bypass regulations at the expense of consumers.

Mulvaney wouldn’t agree. “You can make a strong argument…that new technology actually offers new and innovative ways to protect consumers,” Mulvaney said in The Wall Street Journal story.