PPP

Companies On PPP List Claim to Have Received No PPP Money

July 9, 2020 On Monday the SBA released a list of all the companies who received Paycheck Protection Program loans to the amount of $150,000 and over. Detailing company names, locations, industry, reported jobs supported, as well as the range of the loan received, the list highlights roughly 660,000 loans, or 15% of the total loans issued by the SBA.

On Monday the SBA released a list of all the companies who received Paycheck Protection Program loans to the amount of $150,000 and over. Detailing company names, locations, industry, reported jobs supported, as well as the range of the loan received, the list highlights roughly 660,000 loans, or 15% of the total loans issued by the SBA.

Showing off a minority of businesses who were in the upper tier of amounts received, there are some recognizable names in there. Kanye West’s Yeezy clothes company; a number of high-profile and high-cost law firms; a selection of well-known startups; and, in a stroke of irony, the Ayn Rand Institute, a libertarian think tank which received between $350,000 and $1 million, all make appearances.

Hours after the information’s release, companies began disputing the SBA, saying that they didn’t receive funding despite appearing on the list. Bird, an electric scooter rental startup that was founded in 2017 is one of these.

“Bird was erroneously listed as a company that filed for a PPP loan,” a statement on the issue said. “We did not apply for nor did we receive a PPP loan. We decided as a company not to file an application as we did not want to divert critical funding from small and local businesses.”

This assertion was then followed up by Bird CEO Travis VanderZanden on Twitter, saying that “Bird spoke with Citi early on, but decided not to apply for PPP b/c the money was more deserved by small and local businesses. Citi will confirm this. … It looks like Citi started an application while they waited for our decision on whether to formally apply. We discussed internally and told Citi we didn’t want to apply via email on April 23rd. They confirmed that the temp app was cancelled that evening and never submitted.”

Similarly, venture capital fund Index Ventures claims that it was falsely included in the list. In a tweet, the fund stated that “earlier today, there was an erroneous entry that Index Ventures applied for a PPP loan. We can confirm that Index Ventures did not apply for a PPP loan at any point. Our legal team is looking into why our name is listed and looking to correct it ASAP.” There has yet to be a follow-up statement.

And then, in an odder turn of events, a 72-year-old woman from Millwaukee told CNBC that she had been listed as having received between $5 and $10 million. Geraldine Brimley claims that she actually applied for a PPP loan for her mail delivery company of over $9,000 and received close to $2,300. Asked about the amount the SBA listed her as receiving, she joked saying “I could use it.”

With Brimley having applied through Radius, Bird through Citibank, and Index Ventures claiming to have not applied at all, it seems there were flaws in multiple banks’ processes. If these allegations prove to be true, and these businesses were falsely listed, then it is yet to be clarified where exactly the listed funds are.

Whether they remain with the bank, were deposited in an incorrect account, or if there are cases of fraud to be considered and investigated is yet to be announced. But with the possibility of millions in SBA funds having been miscounted, the $521 billion that is said to have been handed out to PPP applicants may have to be reconsidered and recalculated.

Every Business That Got $150,000 or More in PPP Funds (The List)

July 7, 2020In the interest of transparency, the SBA dumped a list of more than 660,000 businesses that got $150,000 or more in PPP funding.

You can download the entire thing right here.

$100 Million in PPP Fees

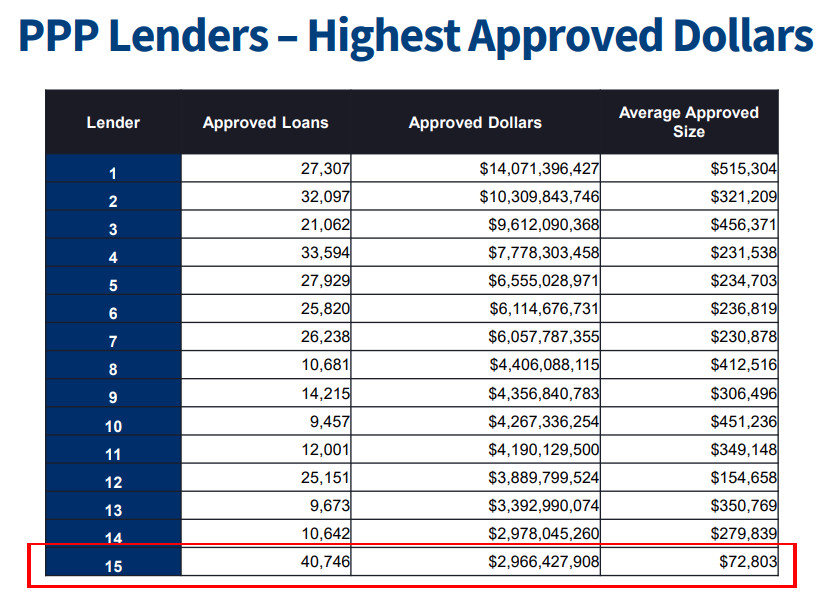

May 12, 2020 $100 million. That’s the gross revenue floor that Ready Capital reported yesterday will be earned from its PPP loan origination efforts. PPP lenders earn between 1% to 5% of the loan amount in the form of a fee from the SBA and Ready Capital was the 15th largest PPP lender by dollars in the first round alone.

$100 million. That’s the gross revenue floor that Ready Capital reported yesterday will be earned from its PPP loan origination efforts. PPP lenders earn between 1% to 5% of the loan amount in the form of a fee from the SBA and Ready Capital was the 15th largest PPP lender by dollars in the first round alone.

The SBA pays 5% for loans under $350,000, 3% for loans between $350,000 and $2 million, and only 1% on loans over $2 million. With the majority of Ready Capital’s loans being for less than $350,000, the pure volume of loans originated (40,000+), translates into significantly larger fee income against a lender who may have originated the same dollar amount but with a much larger average loan size. JPMorgan’s average PPP loan size in Round 1, for example, was $515,000 (an average of a 3% fee) versus Ready Capital’s $73,000 (an average of a 5% fee).

Ready Capital clarified that on a net basis of those fees, they will take home substantially less, since the economics of those fees were in many cases split with referral agents and other partners that contributed in the process. Without committing to a firm figure, they estimated that their net revenue on PPP originations is actually going to be in the neighborhood of 35%-50% of the gross ($35 million to $50 million).

That is so far. Ready approved $3 billion in loans and has so far only funded $2.1 billion of them. The company said it expects that a large percentage that remain will still be funded and they will earn additional fee income respectively from those.

The company also addressed funding delays that had been reported across social media. “While there have been some challenges outside our control that have caused some delays in the distribution of funds, we have facilitated the funding of 2.1 billion through last Friday and are actively working through the remaining population to disperse funds as quickly as possible.”

Ready’s exposure on the loans themselves may be limited. The company said “we do not expect to carry much of the production on the balance sheet at all. So a very small portion will remain on the balance sheet. The majority of it will now be sold off balance sheet.”

Treasury Warns of Audits as Public Companies Return PPP Money

April 28, 2020 In the wake of public outrage at the news that public companies have received millions of dollars from the Paycheck Protection Program, Treasury Secretary Steven Mnuchin today spoke out against such businesses. His comments come after the SBA and Treasury further clarified which businesses actually qualify for PPP, noting that only companies with no access to other forms of capital, such as selling shares or debt, would qualify.

In the wake of public outrage at the news that public companies have received millions of dollars from the Paycheck Protection Program, Treasury Secretary Steven Mnuchin today spoke out against such businesses. His comments come after the SBA and Treasury further clarified which businesses actually qualify for PPP, noting that only companies with no access to other forms of capital, such as selling shares or debt, would qualify.

Speaking on Fox Business, the Treasury Secretary explained that “anybody who took the money that shouldn’t have taken the money, one, it won’t be forgiven and two, they may be subject to criminal liability, which is a big deal … I encourage everybody to look at this and pay back these loans now so we can recycle the money if you made a mistake.” Mnuchin made clear that any company that receives a loan of over $2 million will be audited by the SBA.

A number of cases have made headlines, with Shake Shack and Ruth’s Chris Steak House returning $10 and $20 million, respectively, following calls from the public to refund it. Other publicly funded companies that have returned PPP money include AutoNation ($77 million); Penske Automotive Group Group ($66 million); and the Los Angeles Lakers basketball franchise, which received $4.6 million.

“I’m a big fan of the team but I’m not a big fan of the fact that they took a $4.6 million loan,” Mnuchin said of the Lakers. “I think that’s outrageous and I’m glad they returned it or they would have had liability.”

With the launch of the second round of PPP funding yesterday, the SBA reported that it had processed more than 100,000 loans by 4,000 lenders by 3:30pm that day. Senator Marco Rubio explained on Twitter that a new pacing mechanism had been integrated into the SBA’s E-Tran portal system, lowering the minimum amount of PPP loan applications required for lenders to send a bulk submission from 15,000 to 5,000. The hope for this is that it will enable smaller businesses to reach the funds through more regional lenders and “allow more banks to submit,” explained Rubio.

The Front Line of PPP Lending

April 24, 2020

Susan Lyon, managing director at an independent commercial film company in Solana Beach, California, can’t say enough good things about the quick action her bank took to help her secure emergency government funding during the current pandemic. “They sent out all the forms right away” enabling her to file an application on Friday, April 3 — “the earliest day possible” — she says of the Bank of Southern California. “Then they kept in touch after we sent all the pdf’s back, and they started uploading the loan applications when the Small Business Administration’s website went live the following Thursday.

Susan Lyon, managing director at an independent commercial film company in Solana Beach, California, can’t say enough good things about the quick action her bank took to help her secure emergency government funding during the current pandemic. “They sent out all the forms right away” enabling her to file an application on Friday, April 3 — “the earliest day possible” — she says of the Bank of Southern California. “Then they kept in touch after we sent all the pdf’s back, and they started uploading the loan applications when the Small Business Administration’s website went live the following Thursday.

“The very next day, which was Good Friday,” she adds of the San Diego-based bank, “they e-mailed me at 7 p.m. to say the funds are coming — and two hours later they e-mailed me to say that ‘the funds are in your account.’ It was a high-touch experience.”

Lyon says she will use the bulk of the $130,000, which she received under the government’s Paycheck Protection Program, to pay the salaries of the eight fulltime employees at Lyon & Associates, of which she and husband Mark own 90%.

Lyon’s friend Jennifer Biddle was not so fortunate. Biddle, who operates a flower-growing and distribution business with her husband Frank, has been emotionally devastated, she says, since Torrey Pines Bank dropped the ball on her application for $285,000 to pay employees during the crisis.

“They created an administrative nightmare,” Biddle says of her San Diego-based bank, which failed to forward her paperwork to the SBA. “Being disappointed doesn’t begin to describe my feelings,” she adds.

Based in Vista, California, FBI Flowers has roughly $6 million in annual sales, 40 employees, and a monthly payroll of $114,000. Like her friend Susan Lyon, Biddle also applied for PPP funding on April 3. But she didn’t hear back from her bank for several days “and we thought (the application) was processing,” she reports. When the bank did get back to her a week later, it was to say, “‘We need this other form,’” she says, quoting the bank. “And then they wanted our addendum revised.”

By the time the SBA made the announcement on April 16 that the agency had exhausted the $349 billion allocated by Congress, Torrey Pines was still sitting on her application. “To me it’s negligence,” Biddle says.

“We’re in the middle of our growing season and money is hardly coming in,” she adds. “Our employees are part of a vulnerable population, We were really counting on our bank to do their part and get the application to the SBA. This was what my kids would call ‘an epic fail.’”

Neither Torrey Pines Bank nor its Phoenix-based parent company would comment. “Unfortunately,” Robyn Young, chief marketing officer at Western Alliance Bancorporation, told deBanked, “our bankers are not able to share any information about our clients or client transactions.” (According to a tagline in the e-mail, Forbes magazine has named Western Alliance to its list of the “Ten Best Banks in America” for the past five years in a row.)

Lyon’s and Biddle’s accounts are just two stories – one a rousing success, the other an abject failure – emerging from the Paycheck Protection Program, which was created as part of the $2.2 trillion Coronavirus Aid, Relief, and Economic Security Act (CARES Act). Since the bipartisan bill was signed into law by President Trump on March 27, the SBA has approved 1.66 million small business applications.

Under the PPP, small businesses and self-employed individuals must apply for emergency funding through banks and designated non-bank lenders. Congress authorized the SBA to make emergency, low-interest loans of up to 2½ times a business’s monthly payroll to pay their employees’ wages for eight weeks.

If, after eight weeks, businesses can show they’d spent 75% of the government money keeping furloughed employees on the payroll and covering their health insurance, the loan will be forgiven. The remaining 25% of PPP funding will convert to a grant if it’s spent on rent and utilities.

Now, as the program is being rebooted with new Congressional action for a second round of funding totaling more than $300 billion, many applicants fear that they will again be left out in the cold. “We’ve been hearing that many banks have not been able to handle the torrent of applications,” says Gerri Detweiler, education director at Nav, Inc., a Utah-based online company that aggregates data and acts as a financial matchmaker for small businesses.

Detweiler reports that she and her team at Nav have been working 14-hour days since the CARES Act was signed into law fielding calls and responding to e-mails from the company’s 1.5 million members looking for assistance in navigating the PPP rules. One common experience for small business applicants has been that “many of the banks have been prioritizing customers with deeper and more longstanding relationships,” she says.

One small business owner in Texas, Edward L. Scherer, filed a federal lawsuit in Houston on Easter Sunday charging that Frost Bank, which is headquartered in San Antonio, violated the CARES Act and SBA rules by refusing to accept PPP applications from non-customers. Class action suits alleging illegal favoritism have also been filed against Bank of America, Wells Fargo, J.P. Morgan Chase, and US Bancorp.

For customers and non-customers calling on Bank of America, this would come as no surprise. The Charlotte (N.C.) based giant makes clear that it will only process applications for regular customers. A notice on the bank’s website, declares that only “small business clients who have a lending and checking relationship with Bank of America as of February 15, 2020, and do not have a business credit or borrowing relationship with another bank, are eligible to apply for the Paycheck Protection Program through our bank.”

Although the PPP has been heralded as a way to rescue mom-and-pop businesses, national chain restaurants like Ruth’s Chris Steak House and hotels operating franchises have benefited handsomely. Ruth’s Chris alone received $20 million in crisis funding, according to The Wall Street Journal, which first reported the story.

Although the PPP has been heralded as a way to rescue mom-and-pop businesses, national chain restaurants like Ruth’s Chris Steak House and hotels operating franchises have benefited handsomely. Ruth’s Chris alone received $20 million in crisis funding, according to The Wall Street Journal, which first reported the story.

For the bulk of the country’s small businesses “the money has been trickling in very slowly,” says Sarah Crozier, senior communications manager at the Main Street Alliance, a Washington, D.C.-based advocacy organization that counts 300,000 members. Even for many businesses that have received funding, there remains widespread uncertainty that the loan will be converted to a grant. “There’s not a lot of trust that the PPP loan will be forgiven,” Crozier says. “There’s a lot of confusion.”

That’s a major concern for Randy George, owner of Red Hen Bakery in Middlesex, Vermont – a speck of a place off I-89 near Montpelier, the state capital – who does not want to take on extra debt. Until a month ago, George had been running a $4 million (sales) operation which employed 48 employees. He’s closed down the café, he says, which accounts for about 60% of annual receipts, while keeping on 20 workers to run the bakery.

That operation – which turns out baguettes, croissants, sticky buns and other baked goods for wholesale distribution – has actually ramped up. With most restaurants temporarily shuttered, more New Englanders are eating at home, resulting in the bakery’s nearly doubling its sales to regional grocery stores and supermarkets.

Meanwhile, George has received $411,000 in PPP funding, which he applied for through Community National Bank, located in Barre, Vt., and he’s paying many of his 28 furloughed employees to remain idle. Because of the way the CARES Act program is structured, he says, it’s in his interest to convince laid-off employees not to collect unemployment compensation which includes an extra $600-a-week federal benefit and lasts longer than the eight-week PPP.

“I just called one of my fulltime employees and told him he’ll get to keep his health care if he stays on the payroll,” George explains. “But for part-time people it’s awkward. I’m incentivized to get people back to work and they’re incentivized to go on unemployment.”

At the Portland Hunt & Alpine Club, a bar and restaurant in Maine with the reputation for having the tastiest cocktails in town, if not the entire Pine Tree State, the PPP is not working out for owner Andrew Volk. He secured funding “in the low six figures,” he says, but so far he’s keeping his powder dry. Instead of paying out-of-work employees, he’s letting them collect employment insurance and using a portion of PPP funding for rent and utilities. As for the remaining PPP funds, the question is whether to return the money or keep it as a loan.

Volk says the government program has done little to help him with his most pressing needs. For starters, he was forced to toss out “thousands upon thousands of dollars” worth of perishable foods since his establishment went dark on March 16. All meat, cheeses, sauces, citrus fruit, shrimp, fish and, of course, Maine lobster, went into the dumpster.

Because of a force majeure clause in his insurance policy that explicitly denies indemnification for an “act of God” – “Almost every business interruption insurance policy has a virus and pandemic exclusion,” Volk adds – he will have to eat those losses. “As a small business,” he adds, “we really need support beyond payroll.”

Even many qualified business people who have been approved for PPP funding are still waiting for their funds. Charles Wendel, president of Financial Institutions Consulting, based in Miami, applied for funding “in the five figures,” he says, through Citibank on April 4. That was nearly three weeks ago. “If I were a guy who really needed this money, I’d be screwed,” he says.

In the next round of PPP funding, those who missed out now hope they will be approved quickly by their banks or lenders and that the coronavirus pandemic is brought under control. Meanwhile, the massive unemployment and shutdown of small businesses nationwide are reshaping the contours of the U.S. economy. “Ultimately,” warns Crozier of the Main Street Alliance, “the result of this will be more corporate consolidation and monopolization. That’s what we saw coming out of the ‘Great Recession’ in 2008.”

Ready Capital Was The Biggest PPP Lender By Volume in Round 1 of PPP Funding

April 22, 2020 Ready Capital, a multi-strategy real estate finance company and one of the largest non-bank SBA lenders in the country, was the top PPP lender by loan volume in the country. Company CEO Thomas Capasse appeared on Fox Business yesterday and announced key statistics that aligned with data published by the SBA. By dollars, Ready Capital was the 15th largest PPP lender.

Ready Capital, a multi-strategy real estate finance company and one of the largest non-bank SBA lenders in the country, was the top PPP lender by loan volume in the country. Company CEO Thomas Capasse appeared on Fox Business yesterday and announced key statistics that aligned with data published by the SBA. By dollars, Ready Capital was the 15th largest PPP lender.

“As a leading non-bank, SBA lender, there’s 14 of us, we’re number two in terms of originations last year,” Capasse said on Fox Business, “we focused broadly, we don’t have deposit relationships, so we open our doors broadly to in particular the smaller mom and pop, the local deli, the pizzeria, the nail salon, so just in terms of the numbers, round one of the PPP, we approved 40,000 loans which is number one in the US, it was about $3 billion in total approvals. And our average balance was only $73,000 versus $230,000 for the average in round one.”

Among Ready Capital’s channels for acquiring PPP loan applications is Lendio, who reported consistent figures (a rough average of $80,000 per PPP loan facilitated), and high volume. Lendio has said on social media that they have been working with several partners, Ready Capital among them.

Ready Capital’s Capasse reasoned that their speed could probably be attributed to an affiliated fintech lender. “We are maybe more efficient than some of the banks because we have an affiliated fintech lender which is able to create online portals and processes to work in a more efficient manner and that enabled us to not only process these loans more efficiently but also to provide broad access to the program, to the smaller business owners.”

The company acquired Knight Capital, a small business finance provider, late last year.

Lendio Facilitated More Than 4% of All PPP Transactions

April 21, 2020 Lendio processed $5.7 billion of the $342 billion funded to businesses through the Paycheck Protection Program. With this amount going to just over 70,000 business owners, the Utah company facilitated 4.2% of the total 1.66 million deals through its platform.

Lendio processed $5.7 billion of the $342 billion funded to businesses through the Paycheck Protection Program. With this amount going to just over 70,000 business owners, the Utah company facilitated 4.2% of the total 1.66 million deals through its platform.

“The last few weeks have been an all-out brawl, from solving technical issues to deciphering legislation to managing expectations to dealing with incredible frustration,” Lendio CEO Brock Blake wrote in a recent Forbes article. “In this unprecedented time of crisis and need, there is nothing I would rather be doing than helping small business owners. My co-founder and I started a business on the idea that fueling small businesses fuels the American dream. Now the focus is on saving it.”

While not a direct lender, Lendio utilizes its platform to connect businesses owners with those lenders authorized by the SBA who can provide them with PPP money.

With the national average loan size of PPP money being $206,000, Lendio undercut this amount, instead having an average loan amount of less than $100,000. And with 28 million small businesses in the country, Blake is hoping to continue facilitating loans through this model of high quantity, smaller loan deals once more money is allocated to the program. Joining the chorus that is calling for additional PPP funds, Blake suggests that it could take nearly $850 billion in total to allow American small businesses to weather covid-19, as well as a rethinking of the program so that money can be moved quicker.

“There’s a lot we have learned over the past two weeks as a nation, as an industry, and as business owners. It’s important to take a closer look at the good, the bad, and the ugly of the Paycheck Protection Program, and most importantly, what needs to be done next … Much of the reason why I have been so vocal about the participation of fintech lenders is due to the fact that these lenders’ super power is processing smaller loan amounts at a higher volume. Community banks, on the other hand, specialize in processing large amounts at a lower volume; this is not what Main Street needs right now.

“The fact that fintech and non-bank lenders have been approved to participate in the distribution of PPP loans will make a world of difference if and when more funds are appropriated. Small businesses would have benefited more had these lenders been approved earlier in the process (most of them weren’t approved until the money had actually run out), but they can take heart knowing that more high-tech options will be available in the next phase.”

Small Business Group Advocates For Community Anchor Loan Program (CAP) In Wake Of PPP Wind Down and Possible Refresh

April 17, 2020 At last tally, more than 800,000 small business PPP applications have gone unfunded since the program reached its limit, many of which are genuine mom-and-pop shops that employ less than 25 people.

At last tally, more than 800,000 small business PPP applications have gone unfunded since the program reached its limit, many of which are genuine mom-and-pop shops that employ less than 25 people.

Congress is considering another round of additional PPP funding but Americans may be worrying that such funds will once again go into the hands of some of America’s largest chains. (44.5% of the $349B PPP funds went toward loans over $1 million)

Outspoken successful businessman Mark Cuban has proposed a solution, a lottery system next time around to improve the chances that smaller businesses get their share of the pie. While the public debates the merits of such an approach, one organization (the SBFA) is calling for something much more direct, a targeted fix via a Community Anchor Loan Program (CAP) that would appropriate $10 billion for businesses that were PPP-eligible for loans under $75,000 but did not receive funds.

Deployment of this capital under CAP can and should be administered by non-bank alternative lenders with proven success with this particular small business market, they say.

The proposal also calls for 25% of the funds to specifically be allocated for minority, women, and veteran-owned and agricultural businesses.

In a letter the SBFA submitted to Congress earlier this week, the organization said:

“Women and minority-owned businesses are historically smaller and employ fewer people and, in some communities, are under-banked without the established relationships required to secure a PPP loan. Small farms and agricultural businesses are important to communities and often have trouble qualifying for traditional financing.”

The Small Business Finance Association is a non-profit advocacy organization whose mission “is to take a leadership role in ensuring that small businesses have access to the capital they need to grow and thrive.”