Starting an ISO Shop? Here’s What You Need to do Differently

June 17, 2016 It’s not news that commercial finance brokers are hurting and some are even calling it quits. The industry that didn’t ask for more than a phone and a sharp sales acumen from anyone wanting to start an ISO shop is now stifled with competition. The low barriers to entry that welcomed new companies is causing a seismic shift in the way brokers do business. While some are ready to leave, most are still grappling with the changing times.

It’s not news that commercial finance brokers are hurting and some are even calling it quits. The industry that didn’t ask for more than a phone and a sharp sales acumen from anyone wanting to start an ISO shop is now stifled with competition. The low barriers to entry that welcomed new companies is causing a seismic shift in the way brokers do business. While some are ready to leave, most are still grappling with the changing times.

What’s different about the business now? Almost everything, some say. Gil Zapata who runs a four year old ISO shop, Lendinero, says clients were desperate for money when he started. However he doesn’t think of the competition as fierce but just messy. “There are brokers and ISOs entering and clogging up the system,” he said, “They are obviously fly-by-night and get pulled into it thinking the industry is a fast money maker but it’s really not.”

Competition did what competition does, drove prices and commissions down, costs up and hacked the product. For instance, daily payment ACH loans strongly tied to historical cash flow history didn’t exist. Neither did fancy verbiage for them. The onslaught of online lenders that entered the industry didn’t help either.

OnDeck started selling term loans, which had some similarities to other daily payment products, said Chad Otar, founder of New York-based MCA company Excel Capital Management. “ISOs, on their part have to be careful while pitching these products to clients, explain the contract clearly to avoid penalty.”

The competition has also led to loan stacking, much to brokers’ and lenders’ contempt. And the online lending ilk of Lending Club, Prosper and OnDeck cannot escape it either. Last week, (June 10th), Reuters ran an article calling stacking the latest threat to online lenders where “soft credit inquiries” and “patchy reporting” results in multiple lenders making loans to the same borrower, diminishing the ability to pay.

“Deals become impossible to structure and it becomes difficult for lenders to keep clients on the books when there are second and third names,” said Zapata. The proliferation of loan products that succeeded as a result of competition was a double edged sword. While there are more products to be sold, there are not enough borrowers to lend to.

From a funder’s perspective, that means acquiring and retaining a customer on price rather than an ongoing relationship. “The increased competition has led to commoditization of the MCA,” said Sol Lax, CEO of New York-based business funder Pearl Capital. “It was an exotic financial instrument 5 years ago and the ability to set up shop was restricted. That has changed.”

The ISOs are increasingly reliant on renewals, thanks to the high marketing costs. “A real differentiating factor is whether an ISO syndicates, their default rate, and their renewal rate. All of it is intertwined so that ISOs need to view their business more like investors and less like brokers,” Lax said.

So what would ISOs have done differently? Otar says he would have started an industry coalition similar to the Innovative Lending Platform Association. “I would have tried to pull a Godfather and formed a coalition with other companies and self regulate.”

For Zapata, doing things differently would have meant finding an early backer. “If I had to do this over, I’d have a good investor behind my back,” he said. “Find someone who knows the business and have a good game plan. If you don’t have deep pockets, your chances are minimal.”

Business Finance Companies Visit Capitol Hill

June 17, 2016 Scores of companies providing working capital to small businesses descended on Capitol Hill in early May to educate policymakers about the benefits they provide to the economy. Among them was the Coalition for Responsible Business Finance (CRBF), the Electronic Transactions Association (ETA) and the Commercial Finance Coalition (CFC).

Scores of companies providing working capital to small businesses descended on Capitol Hill in early May to educate policymakers about the benefits they provide to the economy. Among them was the Coalition for Responsible Business Finance (CRBF), the Electronic Transactions Association (ETA) and the Commercial Finance Coalition (CFC).

The inability of banks to satisfy the demands of small businesses is not new, nor is it a problem purely borne out of the recession, data indicates. That’s partially why the Small Business Administration (SBA) exists, according to a 2014 report co-authored by former SBA Administrator Karen Mills.

“If the market will give a small business a loan, there is no need for taxpayer support,” the report states. “However, there are small businesses for which the bank would like to make a loan but that business may not meet the bank’s standard credit criteria.” That occurs so often that the SBA actually had to temporarily suspend guarantees last year because they had reached their limit.

“The SBA has a portfolio of over $100 billion of loans that lenders would not make without credit support,” according to Mills’ report. If that number looks big, it’s because it’s comprised mainly of loans to the larger end of the small business spectrum. Smaller businesses or businesses with smaller needs anyway, continue to be underserved. The average 7(a) loan guaranteed by the SBA in fiscal year 2015 for example was $371,628. Compare that to the $20,000 – $35,000 average deal size reported by some members of the CFC.

“Small firms were hit harder than large firms during the crisis, with the smallest firms hit the hardest,” Mills’ report states, but it adds that small businesses have been responsible for adding two out of every three net new jobs since 2010.

Tom Sullivan, who leads the CRBF, emphasized to deBanked that job creation plays a crucial role in what their organization represents and stressed that it was very important to get the input of small business owners when policymakers consider new regulations.

The CFC meanwhile, estimates that aggregate funding between its members have preserved at least 1 million jobs. And OnDeck, who was on the Hill with the ETA, announced late last year that their first $3 billion in loans have generated an estimated $11 billion in US economic impact and actually created 74,000 jobs.

While the schedules and agendas of each group were different, the CFC reportedly met with nearly two-dozen House and Senate members or their staff in a single day.

BRIEF: Legend Funding Secures $3 million Debt Facility

June 14, 2016New York City-based merchant cash advance company Legend Funding secured a $3 million debt facility from Houston-based investment investment banking firm Ango Worldwide.

Legend provides working capital financing to businesses in the USA and Canada and the company plans to use the funds for expansion. The deal gets Ango some equity and a seat on the board.

“The merchant cash advance industry is experiencing exciting growth and we felt that the legend management team are strongly positioned to take advance of this opportunity,” said Ango CEO John Carson in a news release.

Merchant Cash Advance Definitely NOT a Loan, New York Judge Rules

June 11, 2016

A New York Supreme Court Justice ruled that a purchase of future receivables is not a loan. And it’s not even close, according to a decision and order by The Honorable Jerome C. Murphy in Platinum Rapid Funding Group Ltd v. VIP Limousine Services, Inc. and Charles Cotton.

As a background, the corporate defendant agreed to sell their future receivables to plaintiff in return for an upfront payment, an arrangement commonly referred to as a merchant cash advance. Defendants breached and plaintiff filed a lawsuit accordingly. Defendants asserted twelve defenses including that plaintiff had committed civil and criminal usury. Plaintiff Platinum Rapid Funding Group then moved to dismiss their defenses.

In a 9-page decision, Justice Murphy dismissed nearly all of the defenses, including the one alleging usury, because as he put it, the agreement was not a loan, so there can be no usury. His ruling on that defense is quoted below:

Defendants’ contention that the Agreements violate General Obligation § Law 5-501[1] and Banking Law § 14-a[1], and are civilly and criminally usurious is without merit. A corporation is prohibited from asserting a defense of civil usury (Arbozova v. Skalet, 92 A.D.3d 816 [2d Dept. 2012]). An individual guarantor of a corporate obligation is also precluded from raising such a defense (Id.). Defendants have failed to adequately allege a defense of criminal usury in violation of Penal Law § 190.40, in that they failed to allege that the lender knowingly charged, took or received annual interest exceeding 25% on a loan or forbearance of money. In its bill of particulars, defendant hypothesizes that the terms of the Agreement could result in the payment of criminally excessive interest, but this is clearly insufficient under the pleading requirements.

Essentially, usury laws are applicable only to loans or forbearances, and if the transaction is not a loan, there can be no usury. As onerous as a repayment requirement may be, it is not usurious if it does not constitute a loan or forbearance. The Agreement was for the purchase of future receivables in return for an upfront payment. The repayment was based upon a percentage of daily receipts, and the period over which such payment would take place was indeterminate. Plaintiff took the risk that there could be no daily receipts, and defendants took the risk that, if receipts were substantially greater than anticipated, repayment of the obligation could occur over an abbreviated period, with the sum over and above the amount advanced being more than 25%. The request for the Court to convert the Agreement to a loan, with interest in excess of 25%, would require unwarranted speculation, and would contradict the explicit terms of the sale of future receivables in accordance with the Merchant Agreement.

The detailed explanation reaffirms the obvious distinctions that such a purchase has from a loan, even when such receivables purchased are future receivables. To the extent that defendants argued that a potential outcome of such an agreement could hypothetically be converted to a usurious interest rate, that is a risk that the defendants took, the Court said, and converting this sale agreement to a loan would require “unwarranted speculation.”

Christopher Murray of Giuliano McDonnell & Perrone, LLP is the attorney representing plaintiff Platinum Rapid Funding Group in this action. The case number is 604163/2015 in the New York Supreme Court.

Balance Letters, Payoff Letters, And Not Letting Go

June 10, 2016

The following is a guest-authored opinion piece on the business financing space

Everyone is struggling to keep their head above the water. Just imagine the scene in the movie Titanic. Currently we are in the scene where they zoom out to show the ship sinking slowly with more people in the water trying to survive than on the ship. “Never letting go” is something everyone is doing and clinging on to whatever floats is the only way to survive. The decline in submissions and quality of funded deals is one aspect that many Funding Companies are realizing. No one is letting go of a piece of their portfolio without a fight.

For many A/B paper (for those who go by the grade system) or the Prime to Sub-Prime, 1st position companies know what I am talking about and it’s time to come clean on the truth and the real perception of why things are the way they are.

You can’t get that payoff letter because that Funding Company does not want to let go of their good paying Merchant. Whether the funding was originated from a Broker or organically, that Business is in bed with that funding company and did not have any intention of breaking a relationship until the option was brought to their attention. Whether this Merchant was solicited by another Broker or the Merchant decided to take it upon themselves to seek additional funding, there is one thing that will most often happen.

As soon as the Funding Company receives a request for a payoff letter or balance letter, they will ask why it is needed or delay the process in releasing one or not give one at all until the Merchant is 100% positive and the reasoning and demand is final. Is there anything wrong with this?

To a Broker? Yes. To a Business Owner? No. As many Brokers will fight and try to justify the circumventing of their Merchants, in this case, this is not circumventing at all. The Business has a contract with the Funding Company and until they have a zero balance, that Funding Company has the right to review their account and offer additional funds or discounts to keep their business. This is how it is with any company. Try calling your cable company to cancel your service. What do they do first? They transfer you to the reconciliation department to try to appease you, offer you free or discounted features, and find out what they did wrong or what company you are switching to. Companies are always trying to improve their service and give their clients the best experience.

Throughout the years, if the original Funding Company could offer a better rate or term than what the competing offer is, it has always been in the best interest of the Merchant to continue with that original Funding Company. It is NOT in the best interest nor is it ethical to put the Merchant in another position that will hurt the business or “double up” contracts to equal an amount if ONE company cannot adhere to the request. “Stacking” by offering a second position is one thing, squeezing in as many positions is another, and over time it has hurt many 1st position Funding Companies.

Fast forward to now, the rise in funded accounts that have “defaulted” may have fallen victim to the promises of something better. There is no one educating or clearing the air that there probably isn’t something better… but that advice won’t make anyone commissions and those Funding Companies still rely on Brokers to bring in submissions.

There has been no recourse on this issue, rather growth, and those who have paved the way have found their path covered in dirt. Stomping in this path are other funding companies who have adopted practices from veterans but feel the need to set hierarchy to something they can’t control.

So, with that said, who really sets the rules to what is fair when we are all walking on egg shells? The cost of acquiring a customer and the cost of losing one is an expensive and tricky loss. It is safe to say that once a Merchant is stacked- there is no going back. Should ethics rule over the choices and fate of a Business? Should we put more emphasis on realistic expectations before and after a Business is funded?

A simple request for a payoff letter can open a can of worms. The underlying factors of the difficulties companies face in our industry are all brought upon by the decisions we make when working with each Merchant. At the end of the day you have to ask yourself- am I helping or am I hurting the Business?

Merchant Cash Advance Accounting Q&A

May 25, 2016

As a successful and knowledgeable Merchant Cash Advance accountant I often receive questions from MCA business owners and syndicators. In the last tax season, my accounting firm recognized that many of the questions we receive are distinctly similar. In the following article I address the most common questions my accounting office receives.

Question #1: When I am accounting for my Merchant Cash Advance company isn’t a cash advance accounted for in the same way as a loan? It looks the same on a spreadsheet so isn’t the interest calculated in the same way as a normal loan?

Yoel Wagschal CPA: No. Merchant Cash Advance companies do not have interest. If you have interest then what you have is a loan business, not a Merchant Cash Advance business. Loans use an entirely different method of accounting. If you are still accounting for your Merchant Cash Advances as loans with interest then you will have regulatory issues. If you tell an IRS agent that you are not a loan company but they see your books are exactly like a loan company, how do you think that will end for you? Loans and interest are in a different world. You are the last person who wants to combine those two worlds. You need to see how they do their books at an accounts receivable factoring company and model yourself after them. They do it the way my accounting firm presents it.

Question #2: Your article mentions two ways in which Merchant Cash Advance Companies can account for transactions (cash basis and accrual). Are those the only two ways in which my accounting can be processed?

Yoel Wagschal CPA: I guarantee you would have a big argument if you brought 100 accountants together and asked them all this question: How do I recognize revenue in an accrual basis (from a GAAP standpoint) if I am allowed to take the entire income this year? You would have all kinds of voices and differences of opinions because there is no guidance for this industry. I have done the research and structured an accounting methodology. I’ve spoken with the biggest firms and dealt with the biggest names in this industry. I do have a passion for MCAs. When it comes to a tax standpoint, if you file a cash basis and you want to minimize your exposure, there is really only one way to do it. Those two ways (cash and accrual) can be kept so that they are converted from one to the other at the end of the year. Hence, if you want to prorate the income portion of your receivable (cash basis) I would still keep the books on accrual then convert it at the end of the year. You could do this with a single journal entry because it simplifies the bookkeeping process. You end up with an accrual basis financial statement and a cash basis tax return.

Question #3: I keep being told that my tax liability is based on the difference between what I spend (including funding merchants) and what I receive. For example, if we fund 100K and collect 140K in 140 days how should we keep our books? Right now we don’t recognize any income until we get back the initial funding, even if we renew the merchant over and over. Please elaborate on how revenue should be accounted for. I want to minimize my tax liability but I also want to be sure that this is the correct way to go about it.

Yoel Wagschal CPA: I have a very simple quiz:

YWCPA: Do you trust your accountant?

MCA: Yes. Yes, I do.

YWCPA: You should not. Even if you were my own client I would tell you the same thing. Why do you trust your accountant?

MCA: Because they are a professional. This is what they went to school for. This is what they do for a living.

YWCPA: Do you consider yourself a smart person?

MCA: Yes, I do.

YWCPA: Is it possible that you are smarter than your accountant? Is it possible that they simply learned a different trade than you?

MCA: Yes, that is possible.

YWCPA: Ok, then you should use your own IQ to see if what your accountant says makes sense. If your accountant tells you something that doesn’t make sense about your own business, and you believe your accountant because this is their job then you are not using your high IQ. This is especially true if you have strong negative feeling towards what you are being told. I am not telling you to jump to conclusions. I am saying you should ask questions. Think about this for as long as it takes. Your accounting should be clear and understandable to you.

I am a college professor. When I teach the principals of accounting I always start with debits and credits. I start here because students must know this concept through and through in order to be good accountants. It is the basis of all accounting. New students struggle with the logic behind this principle and I always respond that there are two options: The first option is simply to trust me. They can memorize the information and never know what it means. The second option is to completely understand. This is the option that both my students and Merchant Cash Advance business owners must choose. You, as the business owner, must understand where your own numbers come from. You must understand the foundation of your own accounting. You are entitled and responsible to understand it because of what you must sign on your company’s tax returns.

YWCPA: Do you know what you are signing on the tax return?

MCA: Do I know…?

YWCPA: Do you know what the fine print says directly above where you sign? It says:“Under penalty of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief they are true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.” That is what you sign. Now, do you know what the preparer has to sign?

MCA: The same thing…?

YWCPA: The preparer signs an acknowledgement that they got paid! What I am saying is that you, the business owner, is ultimately responsible for the numbers that are on your tax return. It is you, not the preparer, who certifies that the numbers are legitimate. Of course, accountants are bound by Circular 230 and code of ethics but the level of responsibility is much higher proportionately to the tax payer than to the tax preparer.

Recognizing income only when a deal pays off is clearly, in my humble opinion, “Fraud and Tax Evasion”. I would not sign off on such a tax return. It goes even further that a lot of people who are saying this type of stuff will add that a renewal is an extension of payment and you don’t have to recognize this until the renewal is completely paid off. In this theory you can be in business for 50 years making billions of dollars and pay zero tax. If you were an IRS agent, would you accept that position?

MCA: Mmmm… What’s your point?

YWCPA: Just answer the question. If you were the IRS agent, would it help if the taxpayer told you “my accountant said it was fine”?

MCA: NNNnno.

YWCPA: That’s my point.

Question #4: When my company advances funds to a merchant how do I account for this? Also, how do I account for my company’s income with cash basis (tax return)?

Yoel Wagschal CPA: Ok, we know that in cash basis accounting we don’t recognize revenue before it is actually received. For instance, a grocery store that lets a customer take an order on credit doesn’t recognize revenue at that point. Income is recognized when funds come in.

Now we will think about the Merchant Cash Advance industry. Let’s start with when you advance funds to a merchant. For this example you advance 100k to a merchant and the payback is 140k. The 100k you send to that merchant should not be expensed. That 100k should stay on your balance sheet. You don’t recognize any income because you haven’t collected any income yet.

At the end of the year we have collected half of the advance. It started with 100k funded and 140k to collect. Now we have collected 70k. The most rational way to decide which part of the 70k goes down on the balance sheet and which part should be recognized as income is to prorate it. You should show that half has been collected which means that half of your income should be recognized now. We show it now because you have, in fact, collected revenue.

Question #5: For cash basis (tax return) purposes, when do we realize a loss? How do you show and what do you call the write off of uncollectible merchant cash advances?

Yoel Wagschal CPA: This is a very good question. There are some weird things going on in this industry because normally in a business you don’t exchange money to make money. On a cash basis tax return you would not see a receivable on the cash basis balance sheet. Concurrently, you would not see any bad debt.

Bad debt is usually not something that you see on a cash basis tax return. However, if you really look at the IRS regulations they do understand that even in a cash basis business there are bad debt expenses. Why wouldn’t you usually see bad debt expense? It is because you never recognize any income from the money you didn’t receive. Even with a cash basis tax payment, when a taxpayer lends money to a vendor (in a ‘normal business situation’) and that vendor doesn’t pay the taxpayer back, we know the taxpayer is entitled to take a bad debt expense.

In the Merchant Cash Advance situation, where we exchange money to make money, what could be more of a ‘normal business situation’? This is how your business works so if a merchant does not pay you back then you are entitled to a bad debt expense (of course, the actual realizable cash loss). This bad debt expense gets realized when the Merchant Cash Advance company is certain they are not going to get paid. In the rare situations where you have already written off a bad deal and the merchant does end up paying, you will need to reduce your bad debt expense for the following year or you can add it to your income for the following year.

As far as labeling, I believe the IRS wouldn’t care what you call it. I understand why you want to label it differently. The truth is that this comes only out of the fear that an amateur might look at it. A real trained knowledgeable professional will understand it. Bottom line is, it is perfect (although not normal) for a cash basis taxpayer to have a bad debt expense. But, you can see nothing here is the norm. So do we care for the amateur or for the expert?

Question #6: (This is for “syndicators” which we define here as entities who provide funds to MCA companies before those funds are sent to merchants). Should I do my books whenever I get a payment, week to week, or in one lump sum? From a GAAP or accounting perspective do we use immediate revenue recognition or the deferred method?

Yoel Wagschal CPA: If you want to simplify your bookkeeping I suggest after the fact accounting. Just be sure to maintain absolute consistency. At the end of the year your accountant should be able to take your information, adjust it to a proper trial balance, and create your year end reports. However, if you do not maintain the highest degree of accuracy and consistency then your accounting work will be much more time consuming and potentially flawed.

In my office we have all different types of clients. We have clients who want their books maintained on a live basis. This means we are responsible for taking the information off their MCA platforms and processing it in the accounting system.

We also have clients who want weekly reports. This is a more tempered measurement of the MCA activity. It paints the MCA picture in broader strokes while still maintaining absolute control where tax liability is concerned.

Finally we have clients who only want monthly or yearly reports. This almost completely separates the deal-to-deal MCA activity from the accounting activity. It leaves my accounting firm with the responsibility of tax liability and accounting while the MCA company does their own MCA deal tracking. Whichever approach works best for the individual companies is what you should choose.

In all of these cases there is one fundamental accounting rule and that is 100% consistency. I teach all of my clients to be very disciplined. We recommend having one bank account that is strictly used for funding and receiving money and a completely separate account for operations. For the larger clients we recommend they fund from one account and receive in another account. There is no problem shifting money between these accounts because when an accountant looks at your books it is very easy to follow your transactions.

After you have separated the accounts we can do the actual accounting work for you. However, as we are about to explain the basic journal entries for MCA accounting we caution you to remember this ‘Breaking Bad’ example. In the TV Show Breaking Bad the show’s star (Walter White) explains why he is irreplaceable. Someone else cannot simply step in and recreate his product. His argument is that he is a chemist with multiple advanced degrees as well as years of experience and research. He cannot simply impart all of the knowledge he has to someone in a matter of days. No one can match his intellect simply by watching his actions. His explanation is that a less experienced person would not be able to know if something was off. How would a less experienced person know if one of the ingredients was the wrong type? How would they know if the temperature was slightly off or the cooling phase took too long?

The same practical concept must be applied here, when you are doing the accounting for your MCA transactions. If there was an error in the journal entries, if a procedure was misunderstood and then applied over and over again, if a large transaction was classified incorrectly – how would you know? Only a highly skilled accountant with knowledge of the MCA industry will be able to look over your work and make sure that all of the procedures have been followed correctly. We are about to provide the most basic journal entries for MCA accounting. However we insist you use caution in implementing these entries. We stress that you should consult with a trained accountant who can understand the procedures and recognize mistakes.

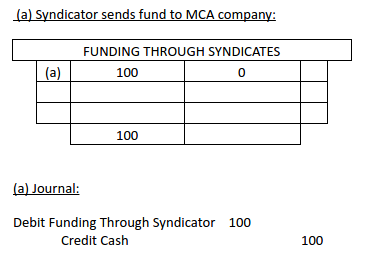

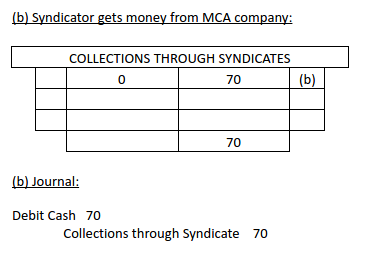

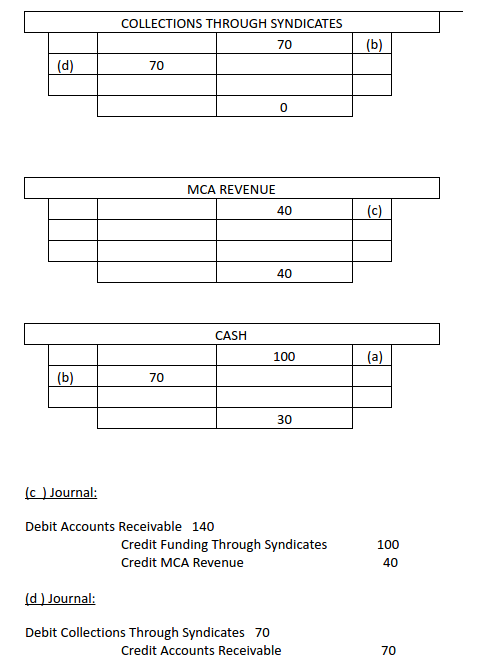

First, we start by looking at an entity who sends funds to an MCA company. As this is where the money trail starts, this is where we will start as well. When a syndicator sends funds to an MCA company they should set up a temporary ledger account. We usually call this “funded thru syndicates”. Every time they send money to the MCA company this entry will show a credit to cash and a debit to this temp account. It won’t have any meaning now but it will have a lot of meaning at the end of the year when they need to produce their financial statements. When this syndicator receives back their money they should debit cash and credit a different account. We usually call this different account ‘collections through syndicates’.

Now, the number of this type of transaction is going to depend entirely on how many deals the syndicator gets involved with and how often they receive cash back from the MCA company. Let’s say there are an accumulation of small transactions that happen over the year. Their outcome is going to be that their ‘funding through syndicate’ account is going to have a debit balance. For the sake of this example, we will make that debit balance 100k. Their ‘collections thru syndicate’ account is going to have a collective credit balance. For this example we will say the credit balance is 70k. As we said, these transactions will not have much meaning when you are processing them individually, but now they will show the bigger picture to your accountant (and hopefully to you!).

The ‘funded through syndicate’ account is at 100k because the syndicator provided the MCA company with 100k (which then went to merchants). Of course, they are not only getting 100k back. In this business the syndicators must make money on the funds they provide. For the sake of this example, the syndicator will look to get back 140k. Now you see that balance outstanding is 70k.

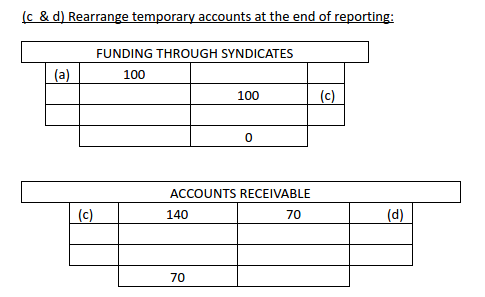

The MCA receivable has a debit balance of 70k, which is what they owe and their revenue is 40k. That’s the difference between the 140k and the 100k.

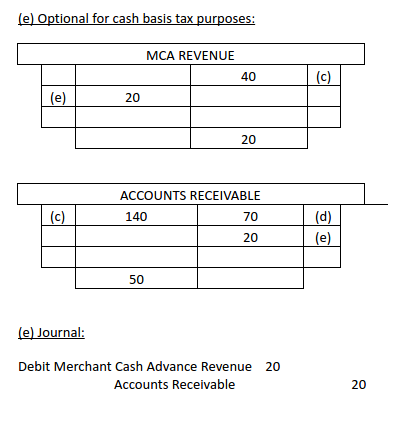

Now the temp accounts are down to zero. The next step looks at the 70k receivable. We know that 20k of it is uncollected revenue. Based on what we have before, which is used for cash basis purposes, I will add another journal entry crediting merchant cash receivable 20k. This will bring down my receivable to 50k which represents the principal portion of the 100k. This shows the syndicator gave the MCA company 100k and half of it is collected. Now we debit MCA revenue and that brings down the syndicator’s revenue from 40k to 20k for cash basis.

As far as GAAP is concerned we don’t have special guidance for this industry. The industry is very unique. We do have the principal of industry practices constraint. I have been very involved in this industry for years. I had a lot of talks with dozens of people all over the country. Investors, funders, creditors, ISO’s, professionals, etc, basically all walks of life connected to this industry. I do feel and believe that the way everyone wants and expects to see the reporting is the way I explained it. As far as MCA companies are concerned they do recognize revenue when your performance obligation has been completed; that is funding. Everything the funder does in the future is collecting their money. There is no performance that this merchant wants from the funder. As a matter of fact the merchant (customer) would be very happy if the funder ceases his activity which is strictly collections. In all other cases where we see revenue being deferred the company still has an obligation to perform. For example, prepaid phone service or insurance both provide services after the bill has been paid. Regarding uncertainty, I feel that this is no different than uncollected receivables. This is why we have a bad debt provision. The bad debt is based on historical performance of each one’s experience. As a side note, I do see a pretty consistent ratio across the line. Uncertainty leads you to the subject of derivatives. Derivatives are uncertain and unknown. Everything is underlined by a future event in the market value of a later date. This is different, as I explained. For instance, a grocery store’s AR is not certain in regards to how much they are going to collect. That is why we always work with fair estimates.

Question #7: How does this journal entry affect my tax returns? Won’t the IRS want it explained? Do they need to see it on each merchant cash advance or all in one entry?

Yoel Wagschal CPA: The IRS is not in the habit of asking to see your internal accounting unless they are performing an audit. They want to see the final result which is your tax return. This is the final report you provide to them. If you are audited then you have to substantiate your numbers and they ask for your ledger. If this happens they will see one journal entry (the one we just discussed) and they will ask how you got to those numbers. Here you will need to provide all the necessary backup, which you will undoubtedly have in your excel sheets, platforms, and correspondence. My accounting firm keeps a detailed record of all financial information we receive. When we do the final journal entry we keep and file all of the source documents that were used to calculate those numbers. We suggest you do the same not simply because the IRS may ask for them but because your investors may ask, your partners may ask, or you may need to present this information in order to diversify your business portfolio. The most important reason to have accurate and reliable financial information is, of course, that it will be used by the business owner – YOU!

Phone (845) 875-6030

Fax (845) 678-3574

Email: cjt@ywcpa.com

http://ywcpa.com

Business Loan Brokers and MCA ISOs Call it Quits

May 17, 2016

Hard times reported just a month ago are already turning into farewells

Hard times for those facilitating small business financing solutions are starting to cause a visible exodus from the space. In their wake, industry vendors have told deBanked of unexpected credit card charge disputes for leads long past purchased or for ISO software previously paid for.

One failed ISO who lasted just 14 months aired it all out on an industry forum. “I do have to say the entire journey was not fun or lucrative. I lost $250,000 of my own money [and] could not broker a deal to save my life,” he wrote. From what he could also tell during his experience, is that nobody else around him was really making any money either.

He’s not alone in feeling this way. Another user just two months earlier started a thread with this title, “Does anyone really make money in merchant cash advance?” In it, he wrote, “The merchant cash advance industry sucks. I’ve been in this business for now 1 year after 20 years of sales experience and what I find is that this industry is the craziest thing I have ever seen.”

Some sales reps or ISO owners are simply venting frustrations and continuing on but others are writing real goodbye letters. A few days ago for example, one long-time MCA industry consultant wrote on LinkedIn that he was “done with merchant cash advance” and that he had finally moved on to something that made him happy, which from the looks of it, is a career in playing Poker full time.

Gil Zapata of Lendinero wrote to deBanked in an email about what’s happening out there. “Lead generation is expensive,” he said. “Most people think that obtaining a new client is just cold calling. Wrong. There is a cultivation process.”

And part of it may be a misunderstanding of what the sales process is like, he insinuates. “Many people who have tried entering this industry think it’s the mortgage business,” he said. “It’s not.”

On forums, users often attribute some of the issues to “low grade professionals,” salespeople who would clearly benefit from more training. They’re part of the reason why an official training course is in the works and should be available some time this year.

“Good agents are not easy to find. Recruiting, hiring, and training is costly,” said Zapata.

And even then with the right salespeople, he added that “a lot of the internet leads are dead deals or not the best leads. Forming partnerships is not easy if you are looking to generate massive deal flow.”

Bright Spot

Unlike some who are throwing in the towel, Zapata is not going anywhere. Neither is another sales rep who contacted deBanked off the record. Just 16 months in to the business, he’s reportedly funding more than $500,000/month just from cold calls and claims that he is not stacking any deals. He admittedly says that he eats at his desk and never leaves. Being an equity trader in a prior life is what helped him succeed at this, he said.

“Some ex-stock brokers who can pound the phones can do very good,” Zapata said. “We only lose deals to hot shot brokers in N.Y. who were aggressive stock brokers or sold some sort of financial product out of Wall Street.”

Indeed, just last week deBanked learned that a sales rep from NYC that we had previously spoke with had just bought a red Lamborghini to celebrate his long and hard fought success. He’s not even 30-years-old yet and business is obviously going well.

Indeed, just last week deBanked learned that a sales rep from NYC that we had previously spoke with had just bought a red Lamborghini to celebrate his long and hard fought success. He’s not even 30-years-old yet and business is obviously going well.

More than a year ago, I wrote that it had become much too late to get into this business if all you had was a couple thousand bucks in startup funds. At Transact 16, one attendee told me they believed that the absolute minimum needed to stand a chance in setting up your own ISO shop at this point was $250,000, purely because marketing costs have skyrocketed.

Might it really take the cost of a new Lamborghini to start an ISO these days? If true, that would ironically mean that as a generation of disenchanted brokers make their way for the exits, they may be passed by an entirely new generation of brokers riding exotic Italian cars on their way in.

Even so, they should heed caution from those that have spent years in the trenches. “This industry is not as easy as it seems,” Zapata wrote. “Cost can eat you up alive.”

Stairway to Heaven: Can Alternative Finance Keep Making Dreams Come True?

April 28, 2016

The alternative small-business finance industry has exploded into a $10 billion business and may not stop growing until it reaches $50 billion or even $100 billion in annual financing, depending upon who’s making the projection. Along the way, it’s provided a vehicle for ambitious, hard-working and talented entrepreneurs to lift themselves to affluence.

Consider the saga of William Ramos, whose persistence as a cold caller helped him overcome homelessness and earn the cash to buy a Ferrari. Then there’s the journey of Jared Weitz, once a 20 something plumber and now CEO of a company with more than $100 million a year in deal flow.

Their careers are only the beginning of the success stories. Jared Feldman and Dan Smith, for example, were in their 20s when they started an alt finance company at the height of the financial crisis. They went on to sell part of their firm to Palladium Equity Partners after placing more than $400 million in lifetime deals.

Their careers are only the beginning of the success stories. Jared Feldman and Dan Smith, for example, were in their 20s when they started an alt finance company at the height of the financial crisis. They went on to sell part of their firm to Palladium Equity Partners after placing more than $400 million in lifetime deals.

The industry’s top salespeople can even breathe new life into seemingly dead leads. Take the case of Juan Monegro, who was in his 20s when he left his job in Verizon customer service and began pounding the phones to promote merchant cash advances. Working at first with stale leads, Monegro was soon placing $47 million in advances annually.

The industry’s top salespeople can even breathe new life into seemingly dead leads. Take the case of Juan Monegro, who was in his 20s when he left his job in Verizon customer service and began pounding the phones to promote merchant cash advances. Working at first with stale leads, Monegro was soon placing $47 million in advances annually.

Alternative funding can provide a second chance, too. When Isaac Stern’s bakery went out of business, he took a job telemarketing merchant cash advances and went on to launch a firm that now places more than $1 billion in funding annually.

All of those industry players are leaving their marks on a business that got its start at the dawn of the new century. Long-time participants in the market credit Barbara Johnson with hatching the idea of the merchant cash advance in 1998 when she needed to raise capital for a daycare center. She and her husband, Gary Johnson, started the company that became CAN Capital. The firm also reportedly developed the first platform to split credit card receipts between merchants and funders.

BIRTH OF AN INDUSTRY

Competitors soon followed the trail those pioneers blazed, and the industry began growing prodigiously. “There was a ton of credit out there for people who wanted to get into the business,” recalled David Goldin, who’s CEO of Capify and serves as president of the Small Business Finance Association, one of the industry’s trade groups.

Competitors soon followed the trail those pioneers blazed, and the industry began growing prodigiously. “There was a ton of credit out there for people who wanted to get into the business,” recalled David Goldin, who’s CEO of Capify and serves as president of the Small Business Finance Association, one of the industry’s trade groups.

Many of the early entrants came from the world of finance or from the credit card processing business, said Stephen Sheinbaum, founder of Bizfi. Virtually all of the early business came from splitting card receipts, a practice that now accounts for just 10 percent of volume, he noted.

At first, brokers, funders and their channel partners spent a lot of time explaining advances to merchants who had never heard of them, Goldin said. Competition wasn’t that tough because of the uncrowded “greenfield” nature of the business, industry veterans agreed.

Some of the initial funding came from the funders’ own pockets or from the savings accounts of their elderly uncles. “I’ve met more than a few who had $2 million to $5 million worth of loans from friends and family in order to fund the advances to the merchants,” observed Joel Magerman, CEO of Bryant Park Capital, which places capital in the industry. “It was a small, entrepreneurial effort,” Andrea Petro, executive vice president and division manager of lender finance for Wells Fargo Capital Finance, said of the early days. “A number of these companies started with maybe $100,000 that they would experiment with. They would make 10 loans of $10,000 and collect them in 90 days.”

That business model was working, but merchant cash advances suffered from a bad reputation in the early days, Goldin said. Some players were charging hefty fees and pushing merchants into financial jeopardy by providing more funding than they could pay back comfortably. The public even took a dim view of reputable funders because most consumers didn’t understand that the risk of offering advances justified charging more for them than other types of financing, according to Goldin.

Then the dam broke. The economy crashed as the Great Recession pushed much of the world to the brink of financial disaster. “Everybody lost their credit line and default rates spiked,” noted Isaac Stern, CEO of Fundry, Yellowstone Capital and Green Capital. “There was almost nobody left in the business.”

RAVAGED BY RECESSION

Perhaps 80 percent of the nation’s alternative funding companies went out of business in the downturn, said Magerman. Those firms probably represented about 50 percent of the alternative funding industry’s dollar volume, he added. “There was a culling of the herd,” he said of the companies that failed.

Life became tough for the survivors, too. Among companies that stayed afloat, credit losses typically tripled, according to Petro. That’s severe but much better than companies that failed because their credit losses quintupled, she said.

Who kept the doors open? The firms that survived tended to share some characteristics, said Robert Cook, a partner at Hudson Cook LLP, a law office that specializes in alternative funding. “Some of the companies were self-funding at that time,” he said of those days. “Some had lines of credit that were established prior to the recession, and because their business stayed healthy they were able to retain those lines of credit.”

The survivors also understood risk and had strong, automated reporting systems to track daily repayment, Petro said. For the most part, those companies emerged stronger, wiser and more prosperous when the crisis wound down, she noted. “The legacy of the Great Recession was that survivors became even more knowledgeable through what I would call that ‘high-stress testing period of losses,’” she said.

ROAD TO RECOVERY

The survivors of the recession were ready to capitalize on the convergence of several factors favorable to the industry in about 2009. Taking advantages of those changes in the industry helped form a perfect storm of industry growth as the recession was ending.

The survivors of the recession were ready to capitalize on the convergence of several factors favorable to the industry in about 2009. Taking advantages of those changes in the industry helped form a perfect storm of industry growth as the recession was ending.

They included making good use of the quick churn that characterizes the merchant cash advance business, Petro noted. The industry’s better operators had been able to amass voluminous data on the industry because of its short cycles. While a provider of auto loans might have to wait five years to study company results, she said, alternative funders could compile intelligence from four advances within the space of a year.

That data found a home in the industry around the time the recession was ending because funders were beginning to purchase or develop the algorithms that are continuing to increase the automation of the underwriting process, said Jared Weitz, CEO of United Capital Source LLC. As early as 2006, OnDeck became one of the first to rely on digital underwriting, and the practice became mainstream by 2009 or so, he said.

Just as the technology was becoming widespread, capital began returning to the market. Wealthy investors were pulling their funds out of real estate and needed somewhere to invest it, accounting for part of the influx of capital, Weitz said.

At the same time, Wall Street began to take notice of the industry as a place to position capital for growth, and companies that had been focused on consumer lending came to see alternative finance as a good investment, Cook said.

For a long while, banks had shied away from the market because the individual deals seem small to them. A merchant cash advance offers funders a hundredth of the size and profits of a bank’s typical small-business loan but requires a tenth of the underwriting effort, said David O’Connell, a senior analyst on Aite Group’s Wholesale Banking team.

The prospect of providing funds became even less attractive for banks. The recession had spawned the Dodd-Frank Financial Regulatory Reform Bill and Basel III, which had the unintended effect of keeping banks out of the market by barring them from endeavors where they’re inexperienced, Magerman said. With most banks more distant from the business than ever, brokers and funders can keep the industry to themselves, sources acknowledged.

At about the same time, the SBFA succeeded in burnishing the industry’s image by explaining the economic realities to the press, in Goldin’s view.The idea that higher risk requires bigger fees was beginning to sink in to the public’s psyche, he maintained.

Meanwhile, loans started to join merchant cash advances in the product mix. Many players began to offer loans after they received California finance lenders licenses, Cook recalled. They had obtained the licenses to ward off class-action lawsuits, he said and were switching from sharing card receipts to scheduled direct debits of merchants’ bank accounts.

As those advantages – including algorithms, ready cash, a better image and the option of offering loans – became apparent, responsible funders used them to help change the face of the industry. They began to make deals with more credit-worthy merchants by offering lower fees, more time to repay and improved customer service. “The recession wound up differentiating us in the best possible way,” Bizfi’s Sheinbaum said of the changes.

His company found more-upscale customers by concentrating on industries that weren’t hit too hard by the recession. “With real estate crashing, people were not refurbishing their homes or putting in new flooring,” he noted.

Today, the booming alternative finance industry is engendering success stories and attracting the nation’s attention. The increased awareness is prompting more companies to wade into the fray, and could bring some change.

WHAT LIES AHEAD

One variety of change that might lie ahead could come with the purchase of a major funding company by a big bank in the next couple of years, Bryant Park Capital’s Magerman predicted. A bank could sidestep regulation, he suggested, by maintaining that the credit card business and small business loans made through bank branches had provided the banks with the experience necessary to succeed.

Smaller players are paying attention to the industry, too, with varying degrees of success. Predictably, some of the new players are operating too aggressively and could find themselves headed for a fall. “Anybody can fund deals – the talent lies in collecting the money back at a profitable level,” said Capify’s Goldin. “There’s going to be a shakeout. I can feel it.”

Smaller players are paying attention to the industry, too, with varying degrees of success. Predictably, some of the new players are operating too aggressively and could find themselves headed for a fall. “Anybody can fund deals – the talent lies in collecting the money back at a profitable level,” said Capify’s Goldin. “There’s going to be a shakeout. I can feel it.”

Some of today’s alternative lenders don’t have the skill and technology to ward off bad deals and could thus find themselves in trouble if recession strikes, warned Aite Group’s O’Connell. “Let’s be careful of falling into the trap of ‘This time is different,’” he said. “I see a lot of sub-prime debt there.”

Don’t expect miracles, cautioned Petro. “I believe there will be another recession, and I believe that there will be a winnowing of (alternative finance) businesses,” she said. “There will be far fewer after the next recession than exist today.”

A recession would spell trouble, Magerman agreed, even though demand for loans and advances would increase in an atmosphere of financial hardship. Asked about industry optimists who view the business as nearly recession-proof, he didn’t hold back. “Don’t believe them,” he warned. “Just because somebody needs capital doesn’t mean they should get capital.”

Further complicating matters, increased regulatory scrutiny could be lurking just beyond the horizon, Petro predicted. She provided histories of what regulation has done to other industries as an indication of the differing outcomes of regulation – one good, one debatable and one bad.

Good: The timeshare business benefitted from regulation because the rules boosted the public’s trust.

Debatable: The cost of complying with regulations changed the rent-to-own business from an entrepreneurial endeavor to an environment where only big corporations could prosper.

Bad: Regulation appears likely to alter the payday lending business drastically and could even bring it to an end, she said.

Still, regulation’s good side seems likely to prevail in the alternative finance business, eliminating the players who charge high fees or collect bloated commissions, according to Weitz. “I think it could only benefit the industry,” he said. “It’ll knock out the bad guys.”