“Do It Better Than How You Learned It”: How Paul Pitcher Came To Be In Canada

June 27, 2019 Few kids who dream of running their own international business actually grow up to live that fantasy. Even fewer end up working alongside their childhood heroes. Paul Pitcher is doing both, and he’s loving every minute of it.

Few kids who dream of running their own international business actually grow up to live that fantasy. Even fewer end up working alongside their childhood heroes. Paul Pitcher is doing both, and he’s loving every minute of it.

Growing up in Annapolis, Maryland, the Managing Partner at First Down Funding and SharpShooter Funding studied at Severn School and immersed himself in sport. Under the eye of his father, Pitcher began playing basketball and baseball at the age of 4. Golf came later, and it followed him into his young adult life as he played at a collegiate level while enrolled at the University of Tampa, where he studied International Marketing and Finance. And upon graduation, Pitcher landed a job in Washington D.C., working in sales for the Washington Wizards and Capitals.

Sports accompanied him in each phase of his life, so it comes as no surprise that it is entwined with his current business ventures.

After leaving the Regional Sales Manager position he held with the Wizards and Capitals, Pitcher became a broker, eventually establishing First Down in 2012 – seeing it as a solution to a problem many business owners across the country face: acquiring capital. Offering funds via merchant cash advances, First Down provides financial aid to small and medium-sized businesses.

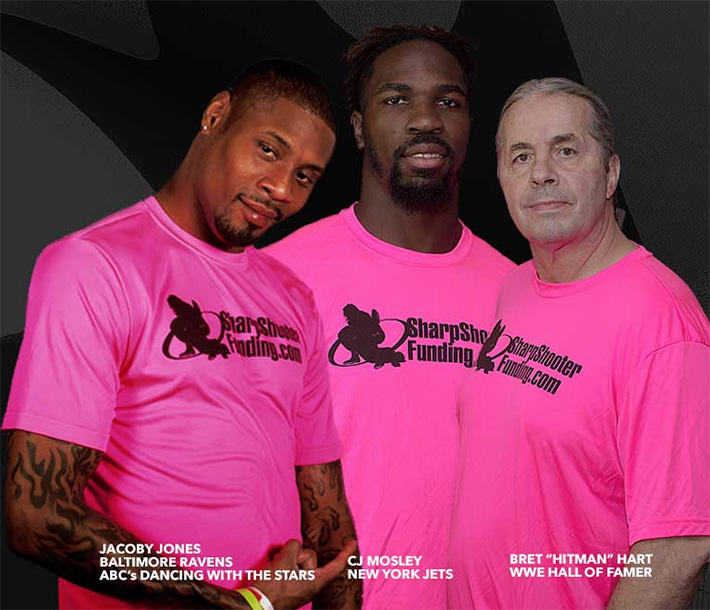

And after enjoying success in the United States, lightning struck on June 6th, 2015. Out of the blue, over 25 Canadian business owners applied for funding from First Down. Chalking it up to ads First Down had placed across social media, Pitcher decided to dive into the new, northern market, but only after consulting with the only Canadian he knew, WWE Hall of Famer Bret ‘Hitman’ Hart.

Having met the wrestler in 1993, Pitcher gambled on Hart remembering the 10-years-old kid in the Looney Toons t-shirt that he took a photo with two decades ago. And it paid off. Following discussions of what First Down did and how it met the needs of the Canadian market, Hart partnered with the company and now serves as commissioner to SharpShooter, the Canadian arm of First Down.

With the backing of a hero from his youth behind him, Pitcher expanded beyond the borders of the US, and with this came further support from sports stars. Recent years have seen CJ Mosley of the New York Jets, Jacoby Jones of the Baltimore Ravens, and the Shogun Welterweight Champion Micah Terill partnering with Pitcher.

With the backing of a hero from his youth behind him, Pitcher expanded beyond the borders of the US, and with this came further support from sports stars. Recent years have seen CJ Mosley of the New York Jets, Jacoby Jones of the Baltimore Ravens, and the Shogun Welterweight Champion Micah Terill partnering with Pitcher.

Noting that the spirit and culture of sport has definitely bled into First Down and SharpShooter from both his own personal life as well as the lives of those athletes that are partnered to it, Pitcher affirms that healthy competition is integral to both sport and business.

Believing that it’s just as important to win as it is to develop the environment you are in, Pitcher is in the funding market for the long-run. And it is exactly this that attracts him to Canada. Comparing it to Baltimore in his home state, he sees the Great White North as a region that is less saturated with funding firms like you would find in New York or Chicago, in other words, he sees it as a place of opportunity, where there is room to grow.

Of course, with such opportunity there are growing pains, like the populace’s level of product knowledge as well as the building of trust between business owners and SharpShooter, but Pitcher welcomes it. Emphasizing his love for competition, he calls for more firms like his to enter the market, be they big or small, as according to him, it could only help build upon the culture of non-bank funding that has taken root in Canada.

“Whatever you do, do it better than how you learned it,” are among the final words Pitcher leaves me with, and with the other closing remarks hinting at further expansion beyond Canada, the Managing Partner seems to be living by this maxim. Be it the education he picked up in Tampa, the lessons learnt in sales, or even a chance encounter with a childhood hero, Pitcher appears to be aiming to continually build and expand upon what he has experienced.

Paul Pitcher is also speaking on a sales and marketing strategies panel at deBanked CONNECT Toronto on July 25th alongside Smarter Loans President Vlad Sherbatov and SEO Consultant Paul Teitelman.

WATCH CAPITOL HILL HEARING LIVE: Crushed by Confessions of Judgement: The Small Business Story

June 26, 2019 The House Committee on Small Business will meet for a hearing titled, “Crushed by Confessions of Judgement: The Small Business Story” today at 11:30am. This hearing is intended to bolster support for The Small Business Lending Fairness Act, a bill to outlaw COJs in small business loans and merchant cash advances nationwide. (Read more about this initiative here)

The House Committee on Small Business will meet for a hearing titled, “Crushed by Confessions of Judgement: The Small Business Story” today at 11:30am. This hearing is intended to bolster support for The Small Business Lending Fairness Act, a bill to outlaw COJs in small business loans and merchant cash advances nationwide. (Read more about this initiative here)

The hearing will be live streamed here when it commences.

The witnesses scheduled to testify include:

Mr. Hosea Harvey

Law Professor and Consumer Finance Law Expert

Philadelphia, PA

Mr. Jerry Bush

Former Owner of JB Plumbing & Heating of Virginia, Inc.

Roanoke, VA

Mr. Shane Heskin

Partner, White and Williams, LLP.

Philadelphia, PA

Mr. Benjamin R. Picker

Shareholder, McCausland Keen + Buckman

Devon, PA

As New Regulations Sweep The Industry, Find Out Where The Next Big Opportunities Are

June 25, 2019

Connect with peers, learn from the pros, and find out what the future holds!

Federal Lawmakers Not Convinced NY Confession of Judgment Ban is Enough

June 25, 2019

The recent New York State law that effectively ended the era of Confessions of Judgment in the small business finance industry is apparently not enough to satiate the outrage of some federal lawmakers. This morning, Rep. Nydia M. Velázquez (D-NY) and Rep. Roger Marshall (R-KS) introduced the “Small Business Lending Fairness Act” that would outlaw confessions of judgment in small business financing transactions nationwide.

Given the impact the New York law is expected to have, the effort may appear to be duplicative. But not quite. The New York law prohibits COJs from being filed in New York against out-of-state debtors. As New York had the friendliest commercial COJ process, financial companies were using New York courts to file COJs against debtors in all 50 states whether there was a nexus to New York or not. By requiring the debtor be in New York, as the new law requires, the utility of COJs in the New York courts for the other 49 states has been eliminated.

However…

That doesn’t mean that courts in other states don’t allow commercial COJs to be filed in their home states. Some do, such as California and Pennsylvania, for example, but the process isn’t as friendly or as easy as New York’s. (See an analysis of California’s and Pennsylvania’s COJ process here)

That is where the proposed federal law would have the most reach and why a federal bill is not merely an academic exercise at this stage.

The federal bill’s language is not new. It mirrors a bill introduced by Senators Sherrod Brown and Marco Rubio in December. No movement has been made on it since but they reportedly intend to move forward with it.

Velázquez intends to keep the momentum going.

“I was appalled to find out that New York State has become an epicenter for dishonest lenders seeking to swindle small businesses around the country,” Velázquez said. “That’s why I’m proud to introduce this legislation and will be leading a hearing this week to further expose these abusive practices.”

The hearing she refers to is titled, “Crushed by Confessions of Judgement: The Small Business Story” and it’s being held tomorrow at 11:30am on Capitol Hill. It will be livestreamed here.

An alleged victim of predatory lending is among the guest speakers. Mr. Jerry Bush, who was featured in Bloomberg’s controversial series on merchant cash advances, is on the witness list. Bush reportedly lost his business after a series of unfortunate business dealings. Nobody from the small business finance industry is currently appearing to offer any opposing testimony on the matter of COJs. If that changes, deBanked will provide an update.

The hearing will be livestreamed on the deBanked homepage.

The Industrial Hemp and CBD Industries, and the Potential Risks for Merchant Cash Advance Funders

June 22, 2019 Authored by Josh Herndon of Global Legal Law Firm

Authored by Josh Herndon of Global Legal Law Firm

It seems that we are constantly being bombarded by news of the growing industrial hemp and cannabidiol (more commonly known as “CBD”) industries. Indeed, industrial hemp (and products derived therefrom, such as CBD) is now legal, and these industries have experienced substantial growth that is expected to continue into the foreseeable future. As such, the businesses in these industries seem to be ideal candidates for merchant cash advances (an “MCA”, or “MCAs”), as such businesses seem more than capable of repaying an MCA.

However, businesses in the industrial hemp and CBD industries are still subject to federal law, and their ability to sell their product can be impacted by enforcement of federal law by federal agencies. MCA funders partnered with such businesses may be harmed by if those businesses are unable to generate the sales needed to repay MCAs. Nevertheless, the possibility of an enforcement action by a federal agency doesn’t mean that all activities in which a business in the industrial hemp and CBD industries could engage would be a violation of federal law. Indeed, there are industrial hemp-related and CBD-related business- activities that likely would not violate federal law.

In sum, MCA funders considering MCAs to businesses in the industrial hemp and CBD industries need to be aware of all risks associated with such MCAs before making an informed decision about whether to make such MCAs.

Background Regarding The Industrial Hemp And CBD Industries.

A fast-growing, sustainable and inexpensively produced plant, industrial hemp is a variety of cannabis sativa L. that contains less than 0.3 percent plant chemical delta-9 tetrahydrocannabinol (more commonly known as “THC”). Unlike marijuana (which, like industrial hemp, is derived from cannabis), which is cultivated to yield psychoactive THC, industrial hemp yields more than 25,000 oil and fibrous products that are embraced by farmers as a hedge against lower-value soy, cotton and alfalfa crops.

Industrial hemp was legalized late last year pursuant to the Agricultural Improvement Act of 2018 (also commonly known as the “Farm Bill”). Related thereto, production of industrial hemp skyrocketed in 2018, with 112,000 acres licensed for cultivation, 3,546 cultivation licenses issued, 78,176 total acres cultivated, and 40 universities conducting research.

Numerous products are derived from industrial hemp including CBD, which is an oil-based product that has uses as a nutritional supplement and food additive In fact, seventy-eight percent of all industrial hemp grown in 2018 was for CBD. The market for CBD has exploded, and is expected to continue exploding. According to the Brightfield Group, industrial hemp-based CBD sales hit $170 million in 2016, and it is anticipated that a 55% compound annual growth rate over the five years thereafter will cause the market for industrial hemp-based CBD to crack the billion-dollar mark.

In addition to legalizing industrial hemp, the Farm Bill also guarantees that industrial hemp and industrial hemp-derived products can be imported, exported and transported from state to state like any other crops. The Farm Bill also allows industrial hemp businesses to access insurance and banking.

The FDA And Its Role With Respect To The Industrial Hemp And CBD Industries.

Although the Farm Bill legalized industrial hemp, industrial hemp and CBD businesses do not have carte blanche to take whatever actions they want with respect to their products. That is because the United States Food and Drug Administration (the “FDA”) is responsible for protecting and promoting public health through controlling and supervising food safety, tobacco products, dietary supplements, prescription and over-the-counter pharmaceutical drugs, cosmetics, animal foods and feed and veterinary products.

The FDA has stressed that although industrial hemp is no longer an illegal substance under federal law, it will continue to regulate cannabis products under the Food, Drug, and Cosmetic Act (the “FD&C Act”) and Section 351 of the Public Health Service Act. That means that any cannabis product (such as CBD) that is marketed with a claim of therapeutic benefit, regardless of whether it is hemp-derived, must be approved by the FDA before it can be sold. In fact, the FDA has specifically cited deceptive marketing practices as one of its chief concerns, and it has clearly established that selling unapproved products with a therapeutic claim is unlawful.

The FDA has stressed that although industrial hemp is no longer an illegal substance under federal law, it will continue to regulate cannabis products under the Food, Drug, and Cosmetic Act (the “FD&C Act”) and Section 351 of the Public Health Service Act. That means that any cannabis product (such as CBD) that is marketed with a claim of therapeutic benefit, regardless of whether it is hemp-derived, must be approved by the FDA before it can be sold. In fact, the FDA has specifically cited deceptive marketing practices as one of its chief concerns, and it has clearly established that selling unapproved products with a therapeutic claim is unlawful.

The FDA has also confirmed that the addition of CBD to food products and dietary supplements is unlawful, even if the CBD is derived from industrial hemp. The FDA’s rationale is that CBD is an active ingredient in FDA-approved drugs, and its addition to the food supply and dietary supplements is illegal under the FD&C Act.

Recent FDA Actions Involving The Industrial Hemp And CBD Industries, And The Impact On Those Industries.

The FDA recently, and dramatically, showed how it will exercise its authority over industrial hemp and CBD products on March 28, 2019, when it (along with the Federal Trade Commission) issued warning letters to three businesses who sell CBD products alleging false, unfounded, unsubstantiated, and egregious health claims about (without sufficient evidence or FDA approval) their products’ ability to limit, treat or cure. The three businesses had advertised a range of CBD-containing supplements, and boasted the ability of those supplements to effectively treat diseases (including cancer, Alzheimer’s and fibromyalgia) and “neuropsychiatric disorders” in both humans and animals. The FDA threatened the three businesses with product seizures, injunctions and sales proceeds reimbursement.

The above actions by the FDA understandably sent shockwaves through the industrial hemp industry, and those actions underscore the risks faced by industrial hemp and CBD companies. For instance, virtually all CBD products that make health and wellness claims, or are deemed a food or drug, are potentially subject to scrutiny from the FDA because such products are mostly sold over the internet and enter the “stream of interstate commerce”. However, it is such health and wellness applications, and food and beverage infusion, that makes CBD and other oil-based hemp derived products attractive to the consumers who are the target market of CBD companies. As such, industrial hemp companies that sell CBD products almost inevitably invite FDA scrutiny as a result of their efforts to market their products to their customers, and potentially imperil their ability to sell their products to those customers.

The above actions by the FDA understandably sent shockwaves through the industrial hemp industry, and those actions underscore the risks faced by industrial hemp and CBD companies. For instance, virtually all CBD products that make health and wellness claims, or are deemed a food or drug, are potentially subject to scrutiny from the FDA because such products are mostly sold over the internet and enter the “stream of interstate commerce”. However, it is such health and wellness applications, and food and beverage infusion, that makes CBD and other oil-based hemp derived products attractive to the consumers who are the target market of CBD companies. As such, industrial hemp companies that sell CBD products almost inevitably invite FDA scrutiny as a result of their efforts to market their products to their customers, and potentially imperil their ability to sell their products to those customers.

A Cautionary Tale For MCA Funders.

Although the industrial hemp and CBD industries seem to be ideal markets for MCA as a result of their past and anticipated future growth, the recent actions of the FDA described above highlight the very real perils faced by businesses in those industries. At first glance, businesses in those industries seem to be ideal candidates for repaying MCAs because of what appears to be bountiful future sales. However, product seizures and/or injunctions ordered by the FDA obviously could prevent businesses in those industries from selling their product and generating receivables from such sales. An MCA funder partnered with such a business would obviously be harmed if the business couldn’t generate the receivables needed to repay an MCA.

Fortunately, there are circumstances under which businesses in the industrial hemp and CBD industries can likely operate without fear of an enforcement action by the FDA. For instance, the FDA allows cannabis and cannabis-derived products to be introduced into interstate commerce where it approves such products (such as with the FDA’s approval of Epidiolex, a seizure medication containing CBD, in 2018). Moreover, the FDA has identified three lawful hemp derivatives (including hulled hemp seeds, hemp seed protein, and hemp seed oil) that can be marketed legally as long as they are not promoted with a therapeutic claim.

Based on the above, the circumstances under which an MCA funder should, or should not, make an MCA to a business in the industrial hemp and CBD industries can be very confusing. MCA funders need an insight into the industrial hemp and CBD industries, and the very real risks faced by those industries as described above, before making MCAs to businesses in those industries.

Fortunately, competent legal counsel versed in the MCA industry, as well as the industrial hemp and CBD industries, can provide such insight, and legal advice related thereto. As a practical matter, an MCA funder should not make an MCA to a business in the industrial hemp or CBD industries without first getting advice from such legal counsel so that the MCA funder can fully understand the risks involved in making such an MCA, and the circumstances in which such an MCA should, or should not, be made.

Bio

Mr. Herndon is an attorney at the Global Legal Law Firm, whose attorneys are well recognized as top industry experts. Mr. Herndon works in the compliance field helping electronic payment processing companies avoid getting fined, arrested, violate rules, or get sued from internal or external threats. Mr. Herndon is also involved in litigation in the payments space, including defending and pursuing electronic payments companies.

It’s Official, The Confession of Judgment Era is Over

June 19, 2019 The New York State legislature passed a bill (S06395) late Thursday night that effectively eliminates Confessions of Judgment (COJ) in the small business finance industry.

The New York State legislature passed a bill (S06395) late Thursday night that effectively eliminates Confessions of Judgment (COJ) in the small business finance industry.

The Senate voted in favor 61-1.

The Assembly voted in favor 83-43.

The new law which goes into effect immediately after Governor Andrew Cuomo signs it, prohibits anyone from filing a COJ against a party that does not reside in New York State. That means if a small business or individual resides in any state that isn’t New York, you cannot file a COJ against them in New York. This matters greatly because 99% of all COJs industry-wide were being filed in New York due to the incredible ease and speed that New York Courts offer to turn those into valid judgments.

Debtors that reside in New York can still be subjected to New York COJs.

A particular sensational story series published by Bloomberg Businessweek created the impetus to change how such New York judgments by confession might impact out-of-state residents. The names of the Bloomberg reporters are written into the Bill’s official memo in the footnotes, memorializing for all time how this law came to be.

Within the small business finance industry, the percentage of funders that required a Confession of Judgment as a condition of their financing was relatively small. And their usage has been limited since COJs were only first introduced as a potential risk mitigation tool on merchant cash advances five years ago in 2014. However, Bloomberg News estimated that COJs have resulted in more than $1 billion in collective judgments over the years, mostly against non-New York businesses.

deBanked has received numerous inquiries regarding what this new law means for COJs already signed but not yet filed. That is a question for an attorney.

Michele Romanow to Keynote deBanked CONNECT Toronto

June 18, 2019Michele Romanow, a TV star on Dragon’s Den and Co-founder of Clearbanc, will be the keynote speaker at deBanked CONNECT Toronto on July 25th. She joins other industry executives speaking at the event from across the business finance industry in Canada.

Tech titan Michele Romanow is an engineer and a serial entrepreneur who started five companies before her 33rd birthday. A “Dragon” on CBC’s hit show Dragons’ Den, Michele is the co-founder of Clearbanc, which in 2018 gave entrepreneurs more than $100 million in funding; SnapSave, which was acquired by Groupon; and Buytopia.ca, ranked #3 on the Profit Hot 50 list of fastest growing companies. Named in WXN’s “100 Most Powerful in Canada” and listed as the only Canadian on Forbes’ “Millennial on a Mission” list, Michele brings her incredible entrepreneurial savvy to every stage.

Michele has driven new digital solutions to many of the world’s leading brands, including P&G, Netflix, Starbucks, and Cirque du Soleil, and she has advised Fortune 100s and governments on innovation, AI, blockchain, and the new economy. She was a finalist for the EY Entrepreneur of the Year Award; the RBC Canadian Women Entrepreneur Awards; and was a Cartier Women’s Initiative Award global finalist.

Awarded Angel Investor of the Year by the Canadian Innovation Awards, Michele is a prolific angel investor who has also co-founded the Canadian Entrepreneurship Initiative with Richard Branson to encourage more women entrepreneurs. Michele In the media, Michele’s work has been profiled in Forbes, The New York Times, Entrepreneur, The Globe and Mail, and Chatelaine.

During her Civil Engineering undergrad at Queen’s University, Michele founded The Tea Room, the first zero-consumer-waste coffee shop. She was also given the Queen’s Tricolour — the highest honour awarded by the university — and, after completing her Queen’s MBA, she founded Evandale Caviar, a vertically integrated commercial fishery.

Michele is currently a director for Vail Resorts, Freshii, League of Innovators, Queen’s Business School and Shad Valley, a transformational program that develops the entrepreneurial potential of exceptional Canadian youth.

Other great executives speaking at deBanked CONNECT Toronto:

That’s All Folks! COJ Ban in New York May Pass on Wednesday

June 17, 2019 The New York legislature has until Wednesday night to pass two bills that would prohibit the use of COJs, one on out-of-state debtors entirely and the other from being used as a condition in a financial contract. Either or both would effectively outlaw their use in the small business finance industry in New York State. If they do not pass a Floor vote by Wednesday night, the clock on the debate would reset until 2020 and the bills would have to be reintroduced in January.

The New York legislature has until Wednesday night to pass two bills that would prohibit the use of COJs, one on out-of-state debtors entirely and the other from being used as a condition in a financial contract. Either or both would effectively outlaw their use in the small business finance industry in New York State. If they do not pass a Floor vote by Wednesday night, the clock on the debate would reset until 2020 and the bills would have to be reintroduced in January.

Both bills have momentum. Both bills have a Democrat sponsor. The Democrats control the Assembly, the Senate, and the Office of the Governor. The bills have at least some support from Republicans. By all counts, at least one of these bills should pass this week.

Bill A07500 would prevent COJs being filed against Non-New York parties by requiring that they only be permissibly filed in a county in which the debtor party “resides.” This bill has already sailed through three committees, the most recent of which had unanimous bipartisan support. Its counterpart in the Senate is S06395.

A03636 is targeted specifically at small business lenders and merchant cash advance companies. “This bill will protect small businesses from predatory lenders that often offer loans and cash advances on the pre-condition that they sign a confession of judgment,” it says.

It’s possible the bills could also be reworded at the last minute.

There is no doubt where the impetus for these bills stems from. A07500’s official memo, for example, cites the controversial Bloomberg story series authored by Zeke Faux and Zachary Mider in its footnotes.

If either or both bills pass by Wednesday night, they would still require the signature of the governor. That step, a technicality, would probably provide clarity on the official date of which the amended law would go into effect.