Are You Ready to Ride The Merchant Cash Advance Wave?

February 18, 2012Less than a year after we acknowledged the stunning absence of Merchant Cash Advance financing from the mainstream media, suddenly it’s the only thing being talked about. It took a few years but journalists are finally learning to complete the phrase of banks aren’t lending with, fortunately there are other options. The term Merchant Cash Advance is being thrown around so much that financial institutions that offer different funding programs entirely such as American Express are trying to attach their names to it. They are now trying to rebrand their product as Express Merchant Financing. This isn’t to be confused with a Dallas, TX based company called Express Working Capital which offers Merchant Cash Advances. You can understand why there is so much confusion. Merchant Cash Flow Loans too, which are micro loans based on gross sales are often identified as Merchant Cash Advances even though there is little common ground.

But let’s not fuss over small details because it’s not just the funding companies that are talking about it now, it’s the media.

No matter how well your website is designed or how good your sales people are, it’s important to recognize that small business owners think like normal consumers. According to a 2007 Nielsen Survey, 63% of people’s trust in a company forms from newspaper sources and 56% from television sources. Even though this type of financing has been around since the 1990s, the lack of news coverage has held the industry back. Despite the advancement of social networking and internet background searches, the majority of Americans still have that If it’s on TV, it must be true mentality. Why else would political candidates still be spending billions of dollars on TV commercials to get their message across?

The broad use of Merchant Cash Advance terminology, the recent recognition by the mainstream media, and the march of average Americans into the reseller market is an omen. A wave is coming. Whether some deem the current industry’s size to be $600 million a year or $1 billion is irrelevant. Merchant Cash Advance and similar financing programs have the potential to be a $10 billion market annually, especially since the major banks are retreating from SBA loans.

We suspect that in 2012, particularly the latter half of it will be explosive unlike the entire industry has seen before. Too many small businesses have been waiting on the sidelines since 2008. If the trend of rising employment is correct and a real recovery is underway, then we’ve got all the ingredients for a perfect storm. Confident Business Owners + Fast, Easy Access to Capital = American Recovery.

Call these business loan alternatives whatever you want: Merchant Cash Advances, Merchant Cash Flow Loans, Express Merchant Financing, etc. Just make sure you have a surfboard. A giant wave is coming.

– deBanked

https://debanked.com

The SEO War for ‘Merchant Cash Advance’

February 12, 2012 Let’s admit it, we’re all at war. If you’ve uttered the terms Panda, PageRank, Backlinks, or Organic in the last few months, you know what we’re talking about. We didn’t choose this fight, Google forced it upon us. And so after a long day of phone calls and handshakes about affordable working capital, we return to our homes at night and search the web. Not for information of course, but to find out where our company website pops up when we Google the phrase: Merchant Cash Advance or other relevant terms. Today we ask, is the fighting worth it?

Let’s admit it, we’re all at war. If you’ve uttered the terms Panda, PageRank, Backlinks, or Organic in the last few months, you know what we’re talking about. We didn’t choose this fight, Google forced it upon us. And so after a long day of phone calls and handshakes about affordable working capital, we return to our homes at night and search the web. Not for information of course, but to find out where our company website pops up when we Google the phrase: Merchant Cash Advance or other relevant terms. Today we ask, is the fighting worth it?

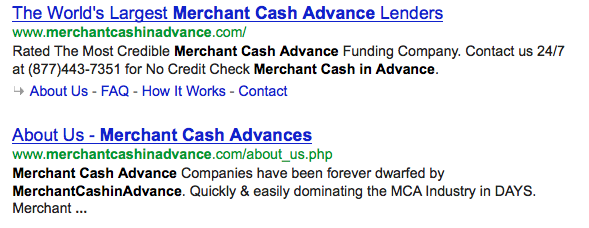

In 2007, back when the industry hadn’t put much thought into the Internet, the #1 search result for Merchant Cash Advance was the blog by David Goldin, the CEO of Amerimerchant. It made sense because it was a self proclaimed “online resource dedicated to the merchant cash advance industry.” There, small business owners and competitors could read about the trials and tribulations of an industry on the verge of explosive growth. It was interesting, it was informative, and best of all, he ranked first without trying.

Nowadays, it’s all commercial. Merchant Cash Advance companies with fat advertising budgets are spending thousands to rank for their favorite keywords, with Merchant Cash Advance still high on that list. The friendly information resource has been replaced by a website that not only crushed the competition in search positioning but seems to publicly brag about it too.

As we write this article, the top 10 Google search results for Merchant Cash Advance are:

1. Merchant Cash in Advance

2. YellowStone Capital

3. Entrust Cash Advance

4. Merchants Capital Access

5. Merchant Resources International

6. American Finance Solutions

7. Nations Advance

8. Bankcard Funding

9. Rapid Capital Funding

10. Paramount Merchant Funding

Do keep in mind that your results may differ slightly depending on your region. Google geographically targets searchers to bring them the most relevant matches.

How much is the #1 spot worth? The market priced it at $75,000 three months ago when MerchantCashinAdvance.com was sold in an online auction for that amount (saved in pdf). So which powerful Merchant Cash Advance company unloaded their precious website? None. The owner of the site was actually an SEO guru looking to make a quick buck. He studied the industry a bit and then within two months ranked a site at the top of Google.

75k might even be considered a steal, as we were actually approached to purchase that website ourselves in August 2011. The exchange was a bit contentious, with them being unwilling to accept less than $200,000 and us making an insulting offer of $100. Perhaps it was jealousy or perhaps it was because we didn’t realize how a Merchant Cash Advance website could be worth so much, but the discussion quickly degraded into name calling and we never spoke again.

How many small businesses are searching for Merchant Cash Advance anyway? According to Google, there are 14,800 searches for it a month. We assume that at least 75% of those are from the companies offering it. You probably Google the phrases several times a day yourself. Admit it!

The real money is in the long tail keywords, since merchants are more likely to personalize their search. Being first for merchant loan for bad credit might be more potent than Merchant Cash Advance. It’s tough to say since deBanked doesn’t really rank for either of those. Then again, we’re an information destination, much like David Goldin’s Blog was/is.

We’re not SEO experts, but we do quite alright with Google ourselves. Without giving away all of them, this is our current placement for just the following keywords:

- Merchant Cash Advance directory: 1, 2

- Largest Merchant Cash Advance companies: 1

- Merchant Cash Advance UCC: 1, 2, 3

- Merchant Cash Advance statistics: 1

- Merchant Cash Advance stats: 1, 2

- Merchant Cash Advance default: 1, 2

- Merchant Cash Advance UCCs: 2, 3, 4, 5

- Merchant Cash Advance laws: 2

- Merchant Cash Advance forums: 2

- Merchant Cash Advance articles: 3

- Merchant Processing: 3

- Merchant Cash Advance Jobs: 8

- Sell your mom for cash: 1 (don’t ask)

MerchantCashinAdvance.com was no different and they claimed to be #1 for over 300 business lending related keywords. A spreadsheet of the analysis they put up during the auction can be found here.

With nothing more than an organic search presence, they claimed to have had the following results:

Month of July for 2011: Received 647 calls & 148 online business lending applications: Funded 81 deals, $26,000.00 profit.

Month of August for 2011: Received 731 calls & 234 online business lending applications: Funded 113 deals, $29,500.00 profit.

Month of September 2011: Received 1026 calls & 276 online business lending applications: Funded 147 deals, $41,750.00 profit.

If that’s the case, then $75,000 was a bargain. That no doubt led to the auction of a similar site just a month later. MerchantCashAdvances.org is currently ranking 51st for Merchant Cash Advance. They claimed to earn $12,500 annually in ad revenue and $200,000 in commissions. The starting bid was $10,000 and although there were many inquiries, it didn’t sell.

That doesn’t mean it wasn’t worth the price. Most Merchant Cash Advance companies are secretly or not-so-secretly investing thousands into SEO campaigns. Black hat SEO is rampant and even the most reputable companies have engaged in it at some point. The underwriting room is the one they show their clients. The sales floor is the one they show their new recruits. But ask where the internet marketing room is, and they’ll claim it doesn’t exist. But it does of course. They’re usually small quarters with no windows that are filled with computers armed with software like ScrapeBox, Article Marketing Robot (AMR), XRumer, and a list of working proxies.

Even the white hats are building backlinks manually and creating endless articles for use on their own company blogs or for services like BuildMyRank. One moderately sized Merchant Cash Advance company in New York City has just as many SEO employees as they do sales representatives. For some, this is just the beginning. It’s not unusual to spend $10,000 – $20,000 a month on pay-per-click campaigns.

The Internet has become a place where the person with the most to spend wins. Because of competition, a paid Google campaign for Merchant Cash Advance keywords can cost $20 per click! We did a phone call with Google and were told that less than 10% of clickthroughs convert into a sale or completed form. If only 1 out of every 10 visitors calls or inquires through the site, that amounts to $200 for a single lead. If only 1 out of every 5 of those leads turn into a closed deal, the acquisition cost is effectively $1,000. That number is awful especially considering commissions and factor rates have been rapidly declining over the last year. And merchants wonder why this financing is more expensive than a bank loan…

It also explains why the practice of closing costs and service fees have survived internal industry scrutiny. Some resellers would be operating in the red without them. Organic traffic is in essence free, that is if you don’t consider the salary or fees you pay your SEO team. Hopefully they don’t overdo it and place your site in the Google sandbox. Until then, the rewards outweigh the risks and every day the industry pushes the envelope a little further in the quest to rank on page 1.

If you can earn $200,000 a year from a website or sell one for $75,000 after two months of work, then there is plenty of room for growth. If the industry was saturated, it wouldn’t be that easy. If your mother is getting into the Merchant Cash Advance business, make sure she knows how to market her website. It’s a war out there.

– deBanked

https://debanked.com

Does Your Mom Sell Merchant Cash Advance?

February 4, 2012Five years ago, everyone seemed to add the phrase, “but I also do mortgages on the side” in response to questions about their career.

“I’m a stockbroker, but I also do mortgages on the side.”

“I’m a school teacher, but I also do mortgages on the side.”

“I’m a stay at home mom and a loving wife, but I also do mortgages on the side.”

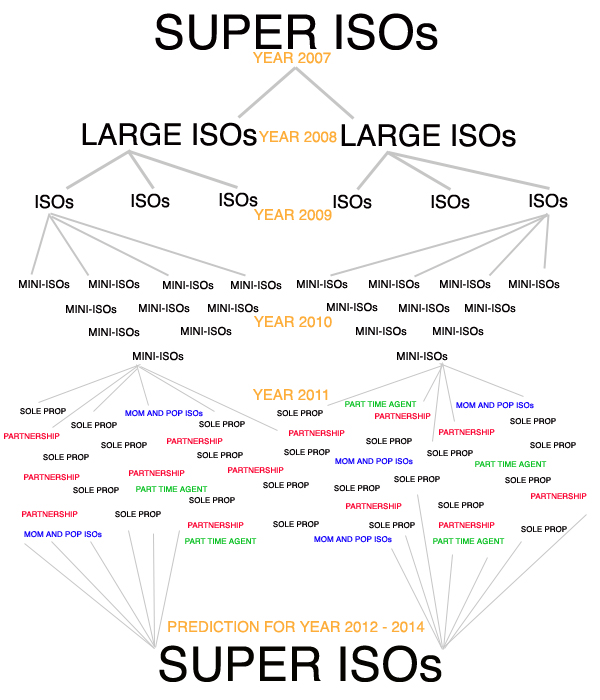

Times have changed and today the new side gig is reselling Merchant Cash Advance (MCA), at least in the New York metropolitan area. The Independent Sales Office (ISO) model is dissipating into a few thousand sole proprietors, all of whom are competing for the same prospects. Most of them started at one of the larger ISOs or funding sources and have over time traded it for the opportunity to work for themselves. Others have pushed it aside as a part time gig while earning a living in another line of work.

It’s encouraging to see that the entrepreneurial spirit is alive and well in the city that never sleeps, but riding solo has its disadvantages. For instance, marketing budgets are more constricted. This inhibits the ability to attract clients, especially when competing against a sizable ISO, who likely has thirty times more to spend on advertising, systems, and service.

It’s encouraging to see that the entrepreneurial spirit is alive and well in the city that never sleeps, but riding solo has its disadvantages. For instance, marketing budgets are more constricted. This inhibits the ability to attract clients, especially when competing against a sizable ISO, who likely has thirty times more to spend on advertising, systems, and service.

And yet, I haven’t heard many complaints from independent agents, which may mean the MCA industry is far from over-saturated. Sixteen of my former co-workers have gone on to start their own MCA ISOs. I even know a pair of twin brothers that run ISOs independent of each other. Some of these newly formed mini-ISOs (less than five people) break apart and each member seems to go on and repeat the cycle.

The Derailing of the Shakeout

In early 2008, it was predicted that low budget marketing would cause a massive shakeout of MCA resellers. David Goldin, the CEO of AmeriMerchant published the following in his blog:

There is another train of thought that is inevitable to fail – those that thought they can sell business cash advances with minimal capital expenditure, meaning hiring unqualified salespeople using inexpensive marketing techniques such as voice broadcasting (with these providers giving the same data to 100s of phone rooms) to dial hundreds of thousands of businessses an hour with a prerecorded message. (Merchants around the country are getting 3 – 5 prerecorded calls a day). The challenge is the quality of anyone that is going to press ‘2’ on their phone for money tends to be “lower hanging fruit” and lower quality deals. With the recent credit crunch and many merchant cash advance funding companies tightening up, some merchant cash advance agents were seeing approval rates as low as 15%-20%. There is no way they can survive and stay in business with that kind of approval rate.

Back then, it was quite popular to have a hundred sales agents in a single room making phone calls. Overhead was the biggest part of the budget, which in places like New York City, could consist of tens of thousands of dollars in rent alone. Add that to all the money that was spent on technology, payroll, dialers, and commissions, and it became really easy to generate a net loss.

With the emergence of mini-ISOs, many are foregoing traditional overhead expenditures such as the renting of a centralized office. Technology costs are also being eliminated since most people already own a personal computer and a cell phone, the only two tools really necessary to interact with prospects. As for state of the art auto dialers? Well, many agents are completely fine using inexpensive resources such as phone books or public UCC filings. Ask around in the MCA industry and you’ll learn just how prevalent this practice is.

There are so few barriers to entry in the MCA industry, that it catches a lot of folks from other financial fields off guard. We receive a dozen e-mails a month from mortgage brokers, stockbrokers, and insurance agents asking what licensing requirements they will need to sell MCA. There are none of course, but they more are shocked to learn that there are no regulations to abide by either. Take your cell phone, throw in your e-mail, spend twenty bucks on a website and you’re an official MCA reseller! It’s just that easy. Thousands of people are getting in on it.

Who is Who?

The flood of resellers and fly-by-night agents is making it increasingly difficult to know where all the MCA money is actually coming from. Here on the Merchant Processing Resource’s website, we’ve created transparency by listing the largest direct funding providers. Need to know if that UCC filing is MCA related? We can help you with that too.

We’re also working on creating an official directory of resellers, for which there will be some requirements for inclusion. That means if you’ve e-mailed us on this topic already and you haven’t heard from us yet, be patient. You will be contacted soon with instructions on how to become an approved MCA reseller.

Consolidation

In the meantime, the increasing fragmentation also presents an incredible buying opportunity. Large ISOs that are looking to add to their portfolios and leverage the brand names that mini-ISOs have created should be able to buy them out at very affordable prices. When this practice starts to happen, it’ll be interesting to see what the market value of mini-ISOs are. Could a business owned by two individuals with a pool of two hundred clients be worth $50,000? $100,000? $300,000? Once someone sets the bar, we should prepare for a year of consolidation, and the little guys will get gobbled up by the big ones. A lot of folks could end up walking away very rich or disappointed. Perhaps now is a good time for your Mother to go into the MCA business for herself and flip the value created for a nice profit a year from now.

ISOs on Steroids

The popularity of co-funding or syndication is also allowing the remaining large ISOs to really flex their muscles in a way they weren’t able to in 2008. Syndication is where an ISO is able to invest their own capital in the MCA deals they close. For instance, on an advance of $20,000, $15,000 of it might come from the MCA funding source, and the remaining $5,000 from the ISO themselves. As long as these accounts perform well, syndicating can create a supernatural rate of growth. This further whets the appetite for opportunities to expand.

So why are mini-ISOs a buying opportunity? Customer loyalty is something big companies can’t always shake, no matter how much is spent courting them. Furthermore, these mini-ISOs tend to have historical performance records on their clients, data that is incredibly valuable. Should a Super ISO invest $20,000 in a small business that has never used MCA before or should they invest it in a business that has responsibly used MCA for two years with no issues, exhibits fierce loyalty, and has a proven record of success? The opportunity to participate in funding that business now and repeated times in the future should be worth a lot.

The Unknown

There are other forces at work that may reshape the industry in a way we can’t predict. The incredible rise of micro-lending is cannibalizing the MCA market, but is also allowing ISOs to offer a variety of financial products to a larger pool of businesses. One New York City MCA funding source privately revealed that micro-loans now make up 80% of their monthly funding volume, a stunning shift from their MCA-only portfolio of 2010.

The growing popularity has also caught the attention of regulators and in some states, the purchase of future credit card receivables is being governed by existing lending laws. The day may come when every agent needs a license to sell, but until then, thousands of people are playing the biggest game in town, helping small businesses get funding to grow. Are you a part of it?

– deBanked

https://debanked.com

The Small Business Lending Climate is Bad, But it’s Not a Disaster

January 27, 2012 We’re proponents of the Merchant Cash Advance (MCA) financial product, but we also believe in objectivity. Over the last several years, MCA providers have collectively rallied the masses by branding themselves as a source of business financing in an economy where financing is scarce.

We’re proponents of the Merchant Cash Advance (MCA) financial product, but we also believe in objectivity. Over the last several years, MCA providers have collectively rallied the masses by branding themselves as a source of business financing in an economy where financing is scarce.

Many people consider the collapse of Lehman Brothers on September 15, 2008 to be the official start of the latest recession. Some will argue that we’re still in that recession. We would probably agree with that. Either way, there hasn’t been much improvement in the financial markets.

Yesterday, on Sean Hannity’s radio show, guest speaker Donald Trump, said “banks aren’t lending.” That’s verbatim and it says a lot, considering that yesterday was January 26th, 2012, a full three years after Lehman’s demise.

A friend of ours that does commercial banking in Philadelphia reiterated the same thing to us a few months ago and even went so far to reveal that restaurants and retail establishments are on their lending blacklist. These revelations paint a grim picture and it’s fortunate that the MCA industry has risen to the challenge to support small business owners.

But there is light at the end of the lending world’s black hole. This morning we had a meeting with a big bank in New York City and of course we asked the question, “Are you lending to small businesses?” They responded, “yes”, and we expected them to follow it with a “but.” Except they didn’t. In fact, they said that small business lending was their biggest market right now.

Intrigued, we demanded to know more. Approximately 50% of applications are being approved and the criteria is as follows:

- Minimum two years in business

- Minimum personal FICO score of 680

- Minimum $250,000 in annual sales

- Must have consistent pattern of sales

- No history of overdrafts or NSFs

- Must prove history of keeping substantial cash reserves in the business account

- Must be current with all vendors and business property landlord

- Collateral may be required

- Maximum approval amount is 20% of annual gross sales

This checklist is challenging. That’s why leveraging your future credit and debit card sales to obtain a large chunk of capital upfront is not only the preferred method of financing for businesses with bad credit, but also for those that are making a serious investment in themselves.

Nonetheless, if a bank IS lending, we’ll be the first ones to admit it. MCAs offer a lot of powerful benefits, but if all banks start lending again one day in the future, quoting Donald Trump might not have the same impact it once did. Fortunately, there are twenty other reasons why MCA is a solid solution, and what banks are doing or aren’t doing is completely irrelevant.

– deBanked

https://debanked.com

Note:

If you are a small business located in the New York City area that is interested in a loan as described above, we would be happy to personally refer you to that bank.

Put Your FUNDED Pants On – It’s Time for Merchant Cash Advance

January 27, 2012 Put your FUNDED pants on because today you’re going to find out just how easy it is to get business financing.

Put your FUNDED pants on because today you’re going to find out just how easy it is to get business financing.

The Merchant Cash Advance industry is expected to surpass $1 Billion in annual funding within the next two years. There are at least thirty two major nationwide providers of capital who want you to be part the revolution. They’ve all got different strengths so you can simply choose the one you believe to be the best fit.

Stop sitting on the sidelines while your competitors are getting funded with less than stellar credit, no collateral, and no fixed payments. The industry average turnaround time from application to funding is approximately seven days.

Do you:

- Accept credit or debit cards as a form of payment?

- Have a copy of your most recent merchant account and bank statements?

- Have a copy of your business property lease or recent mortgage statement?

- Have time to fill out a one page application?

If you answered ‘yes’ to all of these questions and you’ve never considered Merchant Cash Advance financing before, you’re part of a growing minority. There is no cost to apply and no reason not to at least learn about what your options are. Each and every provider in our directory is staffed with experts that can explain exactly how their program works, how much funding you’re eligible for, and how long you can expect the process to take. There are offices and agents all over the country, so whether you prefer to do business in person or over the phone, we’re pretty confident you’ll find what you’re looking for.

If you couldn’t tell, we’re really excited about how Merchant Cash Advance will help rebuild the economy in 2012. So choose a few providers to contact, gather up the documents stated above, and make sure you dress for the occasion. You can never go wrong with FUNDED pants.

Express Working Capital Gives Back

January 21, 2012According to their latest release, Dallas based Merchant Cash Advance Provider, Express Working Capital (EWC) has donated $1,000 to a worthy cause. “The funds went to Dress for Success Dallas, a company striving to empower disadvantaged women with professional attire and a network of support. The donation was made possible by EWC’s recent Facebook campaign.”

Express Working Capital is most known for its business cash advance solution called Convenience Capital™. Money is advanced and repaid through a very simple process so businesses can receive a much-needed merchant cash advance without the snowball effect caused by many other loans that leads to overwhelming debt.

Learn more by visiting EWC’s Facebook page

Rewards: The Next Phase of Merchant Cash Advance Evolution

January 21, 2012 Sky miles and 1% cash back are practically standard benefits of using your credit card, so why shouldn’t you get a little something extra with your Merchant Cash Advance (MCA)? I pay my credit card bill on time every month because I am a responsible customer. As a result, the bank continues to extend me credit when I need it. But that’s not all they do, they also send me a check for 1% of every purchase that I make. That’s pretty nice of them!

Sky miles and 1% cash back are practically standard benefits of using your credit card, so why shouldn’t you get a little something extra with your Merchant Cash Advance (MCA)? I pay my credit card bill on time every month because I am a responsible customer. As a result, the bank continues to extend me credit when I need it. But that’s not all they do, they also send me a check for 1% of every purchase that I make. That’s pretty nice of them!

Sure, it’s a great way to encourage spending but it also promotes loyalty. I get a million credit card offers a year and I have no desire to switch. Isn’t that something?

The Merchant Cash Advance (MCA) industry could learn a thing or two from this. While funding small businesses is practically a blessing in that of itself, there is a lot of fierce competition between MCA providers. Once a business has used MCA, it seems everybody starts fighting over whose going to fund them next. It must be quite an experience for business owners who are by now used to banks tossing them around like an unwanted hot potato. In the MCA industry, everyone wants to fund the potato.

The truth is though, the terms won’t vary much between firms and even if they do, the transaction cost might not be worth it. Switching to a new MCA provider can result in any of the following:

- A termination fee on your existing merchant account

- The purchase or lease of new POS equipment

- The installation of new POS equipment

- An additional service fee on top of the cost of financing

- Unexpected issues with trust or the service

If you have found success with the company that financed you, we can both agree that it’s easier to stay with them. But without additional incentives, you may be feel like your business isn’t appreciated. That’s probably not true and sometimes our sense of entitlement gets the best of us. The thing is though, we believe a little reward is just what you deserve. What makes a great MCA provider great is their ability to become a true partner in your success, instead of just silently collecting their purchased receivables. That’s why we propose the following:

- Cash back for hitting certain monthly sales targets

- Rewards for hitting certain monthly sales targets (gift cards, free advertising, a small business makeover)

- Access to free consulting (consultations from experts on how to best invest the money you receive)

Imagine the motivation you’d feel if your financing not only got approved, but led to a whole bunch of rewards if you invested that money wisely. We don’t have control over the nation’s MCA providers but we can plant the seed and wait for someone to do it first.

Let’s pretend that your business does $8,000 a month in credit card sales on average. One month, you hit $12,000. I think a little reward is in order! Send us an e-mail and tell us what you think.

– deBanked

The point of sale isn’t what it used to be

December 16, 2011 “I’m sorry sir but our credit card machine just went down. Can you wait 11 minutes while I activate a card reader on my iPhone so I can take your payment?”

“I’m sorry sir but our credit card machine just went down. Can you wait 11 minutes while I activate a card reader on my iPhone so I can take your payment?”

11 minutes. That’s how long it took Sean, the founder of the Merchant Processing Resource to set up a merchant account with Square. The point of sale is changing quickly. Dial-up terminals are becoming more and more like their carbon copy imprint predecessors and there’s no way to stop the changing tide. According to Square, 1 out of every 8 merchants in the U.S. uses Square to process credit cards.

The revolution in payments seems to have gone over the heads of Merchant Cash Advance (MCA) providers, a financial industry that purchases future card revenues of small businesses. If the big MCA players have plans in the works to overcome the obstacle of capturing revenues, they certainly haven’t made them public.

We first sounded the warning bell to the industry back in May, 2011, in an article that characterized the modern merchant as having four methods of accepting electronic payments: Desktop POS software, a terminal, PayPal, and mobile payment software. This payment makeup directly leads to rising costs of the MCA product. The ultimate result of our warning was…nothing. MCA providers have for the most part shrugged off the changes in the point of sale, rather than stay ahead of the curve. It’s a shame.

The Electronic Transactions Association (ETA) recently created a certification, a nationally recognized level of excellence for the payment industry employed to become true professionals. A Certified Payment Professional (CPP) will be best equipped to work with business owners and they are required to be knowledgeable on the subject of MCA, as indicated in the CPP handbook. The reverse is unfortunately not required of those employed in the MCA industry, where underwriters mostly hail from the worlds of lending or leasing. Bankcard is certainly not their strong point.

There is a big void of bankcard knowledge in the risk assessment of MCAs. Underwriters are accustomed to reviewing “batch data,” the amount settled out by a merchant, normally once at the end of the day. But press an underwriter for an explanation of where the batch came from, if the technology was PCI compliant, or what would happen to their interchange rates if they delayed settlement for a few days, and you’ll likely catch them scratching their head.

I once personally experienced this firsthand when a relatively new MCA firm sent a 3rd party site inspector to visit a clothing store prior to approval. The inspector’s report and photographs indicated that there was no physical credit card terminal on site but that a USB swiping unit was attached to a desktop computer at the register to accept card payments. The MCA provider declined the deal based on the report since the lack of a credit card machine flew in the face of the processing statements they received. I appealed the case to the CEO, who responded by e-mail with, “The merchant is showing $7,000 a month in credit card sales but when we visited the store, there’s apparently no credit card machine there. The statements we have must be fabricated.” Flabbergasted, I pointed out that the merchant uses desktop POS software and a swiping unit and that it had been verified in the inspector’s report. The last e-mail I received from the CEO was, “I don’t know what you mean by their computer accepting credit cards. Is this PayPal? We don’t do PayPal. We only fund merchants who process on site and they don’t seem to process on site. The deal remains declined.”

Just because I haven’t cited the name of the company, doesn’t mean this exchange wasn’t real. It was and It’s even more embarrassing because their goal was to be in the top three largest funders of MCA in the country. They’re still in business but they’ve suffered some major setbacks.

USB card readers have been in use for a long time and we recently had the pleasure of hearing from Richard Freedkin, the Co-founder of USBSwiper.com. We asked if the mobile pos software revolution was impacting the desktop industry. He shared this, “I don’t think that the USB card readers are being threatened per se… however; I believe that the Mobile Payments industry will make a dent. There will always be people using computers for their POS especially at more fixed locations and Internet access is much cheaper than mobile phone data plans that are required for processing to work.”

And while he’s probably right that the desktop POS experience isn’t going away, they’re not standing on the sidelines either. “We are also about 6 weeks from releasing our new beta version of our software for iPad, iPhone, iPod Touch and Android systems. We will also have a swiper for that platform as well. So we will offer the best of both worlds.”

Great firms innovate so we’re waiting…waiting…waiting for the MCA players to follow suit. If 1 out of 8 merchants are using Square, then the MCA industry is ignoring at least 1 out of every 8 merchants or failing to capture total card revenues from their merchants that use it.

Besides, technology companies like Roam Data are claiming that their mobile payments device has 3x the capabilities of Square. With Text2Pay, you can just SMS text someone funds or better yet, FaceCash allows consumers to make payments using their phone and their FACE!

Capturing payments directly from a merchant account is what made the MCA industry so popular but it could also be their downfall. If a merchant can activate a new account in 11 minutes, then surely there must be an increased focus on the overall banking and financial picture of a small business before purchasing future revenues. That might be where underwriters with lending backgrounds excel but if they don’t know bankcard, then they don’t know squat.

The point of sale isn’t what it used to be…

– The Merchant Cash Advance Resource