marketing

Abe Zeines, Jennie Villano ‘Cook Up’ Buzz

February 13, 2018Abe Zeines, of former MCA infamy, is cooking up something new, according to a video that was posted on LinkedIn earlier today. The 2-and-a-half minute clip was produced by Jennie Villano, a top social media marketer who serves as the VP of Business Development at Kalamata Advisors.

Villano was spotlighted for her notable online marketing acumen in a deBanked story last December.

In this for-fun video, Zeines appears to put spaghetti noodles into an empty pot.

Did he win the cooking challenge?

Dear Funders: Don’t Dial ‘M’ for Marketing

October 7, 2016

Imagine you own a small donut shop in Arizona and receive an email saying, “Hello, I have heard your chocolate donuts are amazing and the most popular item. I work for XX, and we provide small business loans, do reach out to us if you’re looking to take it a step further.”

Versus

Getting yet another envelope in a deluge of mails with a bank-check-like promotional ad for a preposterous amount that startles you for a hot second before it ends up in the paper shredder.

One of these methods is free, personalized and subtle. And no points for guessing which one.

Gone should be the days where funders indiscriminately send out email blasts or cold call merchants offering working capital. But are they?

A year ago, a Wall Street Journal article said,

“A big reason online lenders make heavy use of mail, they said, is that it is still more effective than other types of direct marketing. Across all industries, the overall response rate for direct-mail overtures is 3.7%, compared with 0.1% for both email and social-media marketing campaigns, according to a recent report from the Direct Marketing Association, an industry group.”

Mintel Comperemedia, a database which tracks advertising data highlighted the use of technology as being the paramount shift in marketing for the financial services industry. But is the transition from analog to digital underway?

For some companies, it is. New York-based SOS Capital does not have a sales team and does all of its marketing on social media. The company sends no direct mailers, limits email blasts and instead scouts for small businesses on Facebook, LinkedIn and Yelp.

With more small businesses ramping up their social media presence, discovering leads has not only become easier but also cheaper. “Small business presence on Facebook is growing every day and finding them there can save you a lot of money,” said David Obstfeld, CEO and co-founder of SOS Capital. “Facebook is not explored by most funders but we have had great success.” The company spent $6,500 marketing to SMBs on Facebook and had 120 conversions over a period of two months.

How does that compare with the conventional methods of direct mail campaigns, email blasts and phone calls?

According to Justin Benton, sales director at leads generation firm, Lenders Marketing, it could cost about $100,000 to send out a million emails to active, verified accounts and as much as a dollar for a nice direct mail, including printing and postage.

“Even though it’s cost prohibitive for some folks and some others think that it’s past its prime, direct mail still wins,” said Benton who urges his clients to consider social media marketing which he says can be “virtually free.”

Discovering companies on sites like LinkedIn and Yelp can offer insights into the business and target customers better. “Calling a lead once and saying the words, ‘business loans’ or ‘working capital loans’ does not work, you need to understand the business,” Benton added.

Digital marketing can also help one keep better track of leads and reinvest in the ones that work. “It’s important to have a leads scoring system,” Benton said. The opposite of that, to him, looks like “Making a gumbo from scratch but you have no idea how you did it and cannot recreate it.”

Competition among financial companies will eventually force them to get more creative with their marketing tactics. Like Partners Funding for example, an MCA funder that markets to ISOs, uses incentives as baits. “If the ISOs fund three deals over $50,000, we reward them with extra points or give them marketing dollars,” said Michael Jenssen, ISO sales manager at Partners Funding, which sticks to marketing through email blasts, calls and exhibiting at trade shows.

Ultimately, the road to a lasting relationship with clients is paved with effective marketing. And the line between pushing call to action and being pesky is quite fine. “Funders have been using the same marketing campaigns and it’s making the clients sick,” said Obstfeld. “There are only so many mailers one can receive. They have to be creative about marketing to people without annoying them.”

For Obstfeld, the value in pursuing businesses through channels like Facebook is having more control over deals and interacting with the merchants directly, without any interference from ISOs. “It’s not just about saving money but the control over the deal. When there is no ISO involved, there is no stacking involved.”

The transition to moving all marketing online might be slow but inevitable. Until then, using bank check imagery to promote big pre-approvals will be more than just gags.

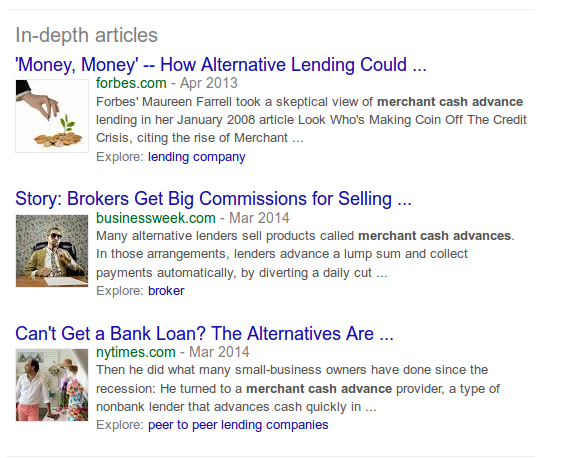

Merchant Cash Advance Now In-Depth

December 1, 2014For quite possibly the first time ever, Google has blessed merchant cash advance with its own array of In-depth articles. What are In-depth articles? Why, they’re featured stories at the bottom of the normal search results. The In-depth feature launched in 2013 and has only worked for certain keywords.

Today it appeared for the very first time for the keyword merchant cash advance

Since Google experiments constantly and shows different results to everyone, it’s possible that you’ve been seeing this for some time already.

I had this to say about the feature 16 months ago:

If you’re wondering how websites can prepare themselves to benefit from such rich snippets, I published Schema.org Markup and Rich Snippets for the Little Guy back in August 2013.

Businessweek, NY Times, and Forbes… I’m not surprised that they’re the chosen publications. Truth be told, there may not have been enough written about merchant cash advance to implement this feature until now. Consider this a milestone.

The Funding Calls That Won’t Stop

November 23, 2014“Your business has been approved for a loan…”

Last week, Chicago Public Radio (WBEZ 95.1 FM) investigated a trend in the small business community, the use of merchant cash advance financing. The station called me in advance to answer some questions about merchant cash advances and I gave my best explanation of the industry and its products.

Of the discussion that lasted more than 30 minutes, only about five of my sentences made it on the air. While I clarify some of my positions below, it was sobering to learn the context of how they were used, as a defense to real life merchant complaints.

The satisfaction rate with merchant cash advances are pretty high and I say that mainly because it’s so rare to hear complaints from anyone other than journalists that can’t believe anyone would accept rates above 6% APR. And while there are indeed bad actors in the industry (as there are in any industry), the gripe one merchant had about phone solicitations that just won’t stop is a recurring theme.

It’s happening to me too.

As an account representative in 2010 calling real time leads sold to five parties at once, I did what anyone would do, I pretended to be a small business myself and inquired through the website that we bought leads from and entered my cell phone as the point of contact

Ring. Ring. Ring…

Within a half hour, representatives from four companies called me, and I learned exactly who my competition was, how they explained the product, and what they would say to win me over. Two of the four were really good and one even referenced my name personally, saying something to the effect of, “If you get a call from Sean Murray, his rates are worse than mine.” Obviously he had already done what I was doing now, which was pretend to be a small business so he could prove to the prospect he was well informed about the alternatives. He had heard my pitch already and was now throwing me under the bus by planting the seed that I was going to offer something more expensive even if it wasn’t the truth.

In the end none of them won because it was all a farce. One never called me again after the first call. Another kept at it for a week and the remaining two followed up for a month.

And then it got quiet…

I had been marked as a dead lead and forgotten about until three months later when one company sent a follow up email. “Smart,” I thought. But then a call came six months later, and then more emails, some from companies I didn’t originally engage with.

And they continued at regular intervals, every couple of months an email or call. Was it interesting? Yes. Annoying? No.

Until this year.

The volume of emails have slowed but I’ve somehow ended up on robo calling lists. “Press 1 to talk to a funding specialist or press 9 to be added to the Do Not Call list”

The volume of emails have slowed but I’ve somehow ended up on robo calling lists. “Press 1 to talk to a funding specialist or press 9 to be added to the Do Not Call list”

The press 9 option doesn’t work for me. Sure, I might be removed from that marketer’s list, but it in no way removes you from anyone else’s list. I knew that already of course because I’ve been on the other end before.

The first time I got one of these calls, I was excited to tell the sales representative who I really was, level with him, and explain that it was a really good idea to take me off the list. But much like other business loan robo call complaints, the representative wouldn’t tell me anything about himself or his company.

I got yelled at.

Every time I tried to ask a question, he’d get louder, insisting I tell him my monthly gross sales volume for the “cash advance I wanted.”

A rogue actor maybe, but I’ve since gotten additional business loan robo calls and have made no progress in getting myself removed. I just hang up now.

Call it sweet irony perhaps. Or maybe a wake up call (pun intended). I applied on a website once four years ago and the rest is history.

My experience with repeat solicitations is marginal compared to somebody that has actually used a merchant cash advance. With the filing of a public UCC-1, anyone in the industry can easily access that data and convert it into a marketing list. And they do.

Brokers that scorn UCC marketing acknowledge that these businesses could be getting called 5-10 times a day. My own clients had reported repetitive calls back when I was an account representative. And while UCC marketing is very cost effective, in today’s market where more than a thousand companies are offering similar financial products, it’s probably safe to say it’s overly saturated.

And if 5-10 calls per day were even remotely accurate, I’d surmise that level of volume is marring the industry’s reputation as a whole.

I could argue though that when customers have a great many options to choose from, they win. With more than a thousand companies offering merchant cash advances and business loans, it’s truly a buyer’s market. Play all the companies against each other and you should end up with the best possible terms. It’s a great time to seek capital.

Except we’ve got to do something about those phone calls, or at least the robo calls.

Every angry robo dial recipient becomes one less person likely to speak positively about the the nonbank financing industry. Aged leads, UCCs and phone calls might be inexpensive, but the cost to undo negative preconceived notions is immeasurable.

Do you want to be known as the company that helped small businesses or the annoying people that won’t stop calling? If merchants are taking to the air waves to complain, it will only be a matter of time before the FTC and FCC become interested.

—

Regarding my comments on the radio about APRs and daily amortization, they were pulled from a conversation that compared daily payment loans to purchases of future sales. I DO believe bad actors exist and every business owner should have an accountant, lawyer, or savvy third party review any contracts they enter into, financial or otherwise.

Why Your Deal Got Stolen

September 16, 2014 Back in April, I presented the idea of trigger leads coming to the alternative lending industry. In subsequent discussions about that blog post, many folks particularly in merchant cash advance questioned whether such a concept could possibly exist or would even be legal.

Back in April, I presented the idea of trigger leads coming to the alternative lending industry. In subsequent discussions about that blog post, many folks particularly in merchant cash advance questioned whether such a concept could possibly exist or would even be legal.

For those not familiar, this is the methodology behind trigger leads using a hypothetical scenario:

- OnDeck runs the personal credit of a merchant using Experian.

- Experian sells the contact information of that merchant to OnDeck’s competitors immediately after credit is pulled.

- Competitors solicit that merchant and convince them to go with them instead.

Again, the reaction I get to the above scenario by most people is, “yeah, right. I don’t believe that could happen.” But if you look at the raw amount of ISOs complaining their deals got stolen, it’s evident that perhaps there is something else brewing than just the usual assortment of rogue underwriters and shady funders.

Most ISOs are convinced that if their client is working with them and only them, that a shady business dealing has taken place if that client is randomly called out of the blue with the knowledge that they’re pursuing funding. To them, the only conclusion is that their deal got backdoored.

And while backdooring does seem to happen out there from time to time, another culprit may very well be trigger leads. Credit bureaus and big data aggregators are selling credit pull data in real time. UCC-1 leads are leads after the funding has taken place. Trigger leads are leads before the funding has taken place. But do they really exist?

And while backdooring does seem to happen out there from time to time, another culprit may very well be trigger leads. Credit bureaus and big data aggregators are selling credit pull data in real time. UCC-1 leads are leads after the funding has taken place. Trigger leads are leads before the funding has taken place. But do they really exist?

Elsewhere in alternative lending, trigger leads are the backbone for how companies tailor their direct mail campaigns. If a consumer’s credit was pulled today by a mortgage lender, companies like Lending Club and Prosper will make sure that consumer receives a mail ad for a home improvement loan tomorrow.

Today at the Apex Lending Exchange conference in New York City, Ron Suber, the president of Prosper, referred to this trigger methodology as “getting to the right borrowers at the right cost.” In their sector, trigger leads are marketing 101. In merchant cash advance, it’s perceived as a pipe dream. Odds are that whoever is taking advantage of trigger leads in this industry would want to keep all the other players in the dark about it.

As much as you might hate to believe it, all of the backdooring paranoia that’s been rampant lately might actually be caused by the credit bureaus, not the funders. The lesson here is that as soon as your merchant’s credit is pulled, the clock is ticking until your competitors find out even if that merchant talks to nobody else.

I know ISOs want to believe that their merchant is only theirs, but in the age of advanced technology and big data, your merchant belongs to the cloud. As soon as your relationship with the merchant interacts with technology, somebody else will find out about it. And that’s why your deal got stolen.

Is Awareness of Alternative Lending Still Low?

July 4, 2014 Prosper’s President Ron Suber and LendingClub’s CEO Renaud Laplanche have previously explained that there is still a large opportunity for growth because most people still don’t know non-bank lending options exist.

Prosper’s President Ron Suber and LendingClub’s CEO Renaud Laplanche have previously explained that there is still a large opportunity for growth because most people still don’t know non-bank lending options exist.

As cited on LendingMemo, Renaud Laplanche admitted the reason they are even considering an IPO is “to use it as an opportunity to raise awareness for the company.” He continued by saying that they don’t need capital so the purpose of their IPO aspirations “is a lot of free advertising.”

In casual conversations with business owners, friends, and new acquaintances I’ve asked if they’ve ever heard of merchant cash advance, p2p lending, or companies like OnDeck Capital and LendingClub. The answer is almost always ‘no’.

That means there is still a lot of work to do.

In this CNBC interview Funding Circle acknowledges that many business owners aren’t aware of alternatives and explains what makes them different.