Loans

The Crazy Lawsuit Against Marcus Lemonis Was Dismissed

November 11, 2021The supposed bombshell lawsuit filed by Nicolas Goureau, Stephanie Menkin, and ML Fashion against Marcus Lemonis has been dismissed. Despite the sensational allegations that enabled Forbes to pen a major story, the Court found the entire lawsuit defective and dismissed it altogether on October 15.

The plaintiffs have advised the Court that they intend to try again by filing a second amended complaint. That would in fact make it their third attempt to try even getting past the opening stage of litigation.

The dismissed lawsuit had been packaged up to make headlines, opening with a monologue about it being the culmination of an “eight-month investigation” carried out with the help of a “former district attorney and a top law school professor, and a world renown psychiatrist that was spurred by the coming forward of no less than seventy (70) family businesses that have been destroyed…”

Despite all this, the judge ordered the suit “dismissed in its entirety.”

Elevate Announces New Financing Facility for Non-Prime Credit Product

October 13, 2021

Elevate Credit, Inc., a top provider for credit solutions marketed for non-prime individuals, announced Wednesday a $50 million financing facility, which may increase to $100 million, according to a company press release. The funding is to grow the Today Card, a credit card designed to expand access to credit while promoting intelligent credit decisions for people with less than perfect credit scores.

Financing for the Today Card will come from Park Cities, an asset management and alternative investment company that provides flexible debt solutions to its customers. The partnership will help reduce the amount of capital required by Elevate for the project.

“The Today Card has seen outsized demand and has been the fastest growing brand over the last 12 months,” said Elevate CEO, Jason Harvison. “To continue that growth, we have announced a new lower cost credit facility. Park Cities has demonstrated a deep understanding of our space. I am pleased to both diversify our financing and promote our platform’s ability to serve non-prime consumers at even lower APRs.”

Backed by Mastercard, Today Card offers all the benefits of a regular credit card to individuals who may not qualify for the same perks through other creditors. Family share, fraud control, and flexible payment options are all packaged into the Today Card product. These options will familiarize cardholders with these types of benefits should their credit improve in the future and they qualify for other cards with different banks.

“Elevate is changing the game for non-prime Americans. We are proud to partner with a mission driven organization and help enable their growth,” said Park Cities Managing Partner, Alex Dunev.

Elevate has originated $9.2 billion in non-prime credit to more than 2.6 million non-prime consumers to date, and has saved its customers more than $8.5 billion versus the cost of payday loans, according to the report. They already offer borrower incentives like reduced interest rates over time, free credit monitoring, and free financial training.

NerdWallet Names its Competition, Reveals Its Web Traffic Figures

October 12, 2021 Personal finance company NerdWallet disclosed who its direct competitors were last week in an S-1 filing.

Personal finance company NerdWallet disclosed who its direct competitors were last week in an S-1 filing.

Those companies include: Bankrate, Credit Karma, LendingTree, and Zillow.

“We currently compete with a number of companies that market financial services online, as well as with more traditional sources of financial information, and with financial institutions offering their products directly, and we expect that competition will intensify,” NerdWallet said.

“… We also face direct or indirect competition from providers of consumer personal finance guidance and online search engines,” the company added.

NerdWallet generated 16 million unique users per month last year, defining that metric as a unique user with at least one session in a given month as determined by unique device identifiers. That was up from the 13 million per month in 2019.

The company had more than 8 million registered users as of December 2020, 2 million of which registered in 2020.

Loans Canada Announces Online Lending Survey Results

August 9, 2021 Loans Canada published their annual online lending survey results on Monday morning. The company polled online personal loan applicants throughout Canada.

Loans Canada published their annual online lending survey results on Monday morning. The company polled online personal loan applicants throughout Canada.

Among the results, several statistics stand out.

40.8% of respondents said that they felt “pressured” to fill their loan application quickly, a compelling counter to the mainstream narrative that borrowers are demanding speed.

44.8% of respondents said they felt “pressured” to accept credit building services even though 85.3% of applicants that had been rejected for an online personal loan said they had been rejected on the basis that their credit score was too low.

Loans Canada noted large swaths of satisfaction and dissatisfaction alike, finding that applicants that have never been able to get approved for an online personal loan were highly likely to rank the online borrowing experience as “very bad” while those that have been approved were highly likely to rank the online borrowing experience as “good” or “very good.”

How to Think About Credit Invisibility

July 29, 2021Authored by:

Lily Cook, Researcher at Canadian Lenders Association

Tal Schwartz, Senior Advisor at Canadian Lenders Association

Recent research by PERC has highlighted the issue of credit invisibility in Canada, defined as “persons with either no account payment history in their credit report (referred to as “no files”) or fewer than three accounts in their credit report (referred to as “thin files);”

Recent research by PERC has highlighted the issue of credit invisibility in Canada, defined as “persons with either no account payment history in their credit report (referred to as “no files”) or fewer than three accounts in their credit report (referred to as “thin files);”

In Canada, credit scores are calculated using payment history, outstanding debt, credit account history, recent inquiries and types of credit. However, according to research from Cornerstone Advisors, the ‘on-ramps’ to being credit visible are limited and come with challenges. The most common paths are:

- Credit cards:

- Collections: Collections as a point of entry into a credit system immediately sets the consumer at a disadvantage, since the first thing to identify them is a negative characteristic.

In general, Canadians under 25 tend to use credit cards at far lower rates. Those in that age group who do have a credit history have the highest percentage of credit scores below 520, according to Equifax Canada.

The rate and impact of credit invisibility in Canada is significant:

- 35.3% of Canadians are credit invisible vs. 19.3% in the US.

- the issue disproportionately affects immigrants, minority communities or younger individuals.

How are fintechs addressing this?

1. Access to alternative data

Canadian data aggregators provide lenders with access to non-traditional credit information that advanced firms can apply ML to in order to better adjudicate credit.

- Open banking data providers like Flinks and Inverite provide consumer transaction history information that allows fintech lenders to underwrite credit invisibles based on their cash flow instead of their credit score.

- Commercial data providers like Forward AI, Boss and Railz pull financial data from accounting systems, payroll, and point of sale terminals in order to give lenders a more fulsome picture of a businesses health.

2. Make alternative data mainstream

PERC Canada recommended that the CFPB explicitly include non-financial institutions in their definition of a ‘creditor’ in order to report positive payment data to credit bureaus. Credit reports that could ‘reward’ customers for paying telecommunications bills on time, for example, could make the credit system more forgiving in the future.

- Billi, for example, a Canadian fintech allows users to integrate on-time payments for their Amazon Prime and Netflix accounts into their credit reports in order to improve them.

Canadian credit bureaus have also taken active steps to being more inclusive of alternative data. A prime (no pun intended) example is Landlord Credit Bureau’s (LCB) and Equifax’s partnership to allow rent payments to count towards credit scores.

- Both as a way to reduce risk for landlords and give tenants a leg up in the market, this shared use of alternative data is “ninety-plus per cent….positive in nature, so overwhelmingly landlords use this to reward tenants,” LCB’s CEO, Zachary Killam said.

3. Create a better on ramp to credit building

Credit building loans can unlock credit for those with minimal histories or challenging track records. These are installment loans that only pay out once the customer has paid them off, and are offered by fintechs like as Spring, Marble and Refresh.

Essentially reverse loans, the reverse structure protects the lender, in the event that the customer doesn’t make all their payments. Over the course of the loan term, the customer’s payments are reported to the credit bureaus. Borrowell, which recently acquired Refresh’s credit building loan portfolio, is now one of the largest providers of this service in Canada.

So what’s the solution?

In order to drive meaningful change on the issue of credit invisibility, fintechs must continue to enable lenders to challenge the limitations of the credit system – by improving access to alternative data, normalizing its use and building better on-ramps to the credit system than collections and credit cards.

Credit invisibility is caused largely by structural issues within Canada’s data markets, but fintechs are starting to fill these gaps.

LendUp Stops Making New Loans

July 10, 2021 LendUp, a fintech lender that hoped to disrupt the payday loan industry, is no longer making new loans. A note posted on its website said “We are currently not offering loans to new customers.”

LendUp, a fintech lender that hoped to disrupt the payday loan industry, is no longer making new loans. A note posted on its website said “We are currently not offering loans to new customers.”

When deBanked sat down with the now former CEO Sasha Orloff in 2017, he said that their product was simply cheaper and more flexible.

“The easiest person to convince that we’re a better product is an existing payday user because it’s slightly cheaper at the beginning, it gets much cheaper over time,” he said then. “It has a lot more flexibility.”

But for all the bells and whistles, their still relatively high rates generated a target on their back with regulators.

In 2016, for example, the CFPB said “[LendUp] did not give consumers the opportunity to build credit and provide access to cheaper loans, as it claimed to consumers it would.”

Balancing the messaging with the reality seemd a difficult task.

Orloff stepped down in January 2019, but in less than two years the CFPB took a second crack at LendUp for allegedly violating the Military Lending Act.

In January of this year, LendUp settled the charges, agreeing to pay $300,000 in redress to consumers and to pay a $950,000 civil money penalty.

As recently as April, LendUp’s website was still offering loans with a promoted APR of 400%.

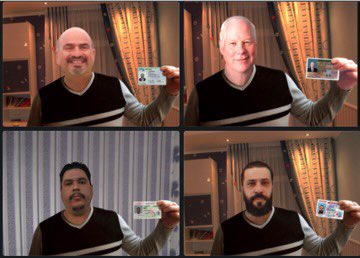

Loan Fraudsters Resorting to AI Generated Faces

April 27, 2021 According to a sneak peek posted by Lendio CEO Brock Blake, fraudsters are stopping at nothing to game the government’s emergency loan system.

According to a sneak peek posted by Lendio CEO Brock Blake, fraudsters are stopping at nothing to game the government’s emergency loan system.

“Wanna glimpse into what lenders are experiencing with attempted fraudulent applications?” Blake wrote in a tweet. “Here are four ‘applicants’ seeking a loan.”

Four pictures showing computer-generated “business owners” all have the same sweater, but different heads. People are using AI tech to create randomized, just barely discernible pics of borrowers holding IDs beside them to beat new compliance measures.

It’s like a techno arms race between an automated scanning system that looks for fakes versus an automated fake ID and person generator that tries to make passable fakes.

After a year of PPP and EIDL success stories and fraud concerns, funders are still beating back scam artists. During a recent U.S. Senate hearing, SBA Inspector General Mike Ware said his office had secured $2.1 billion in fraudulently claimed PPP and EIDL loans.

In related news, the SBA announced the $28.6 billion Restaurant Revitalization Fund applications would open on Monday, May 3. Fraudsters start your fake restaurant owner generators.

Wanna glimpse into what lenders are experiencing with attempted fraudulent applications?

Here are 4 different “applicants” seeking a #ppploan. pic.twitter.com/kdbLmNGlvt

— Brock Blake (@BrockBlake) April 26, 2021

Can’t Wait For An Inheritance? Someone Will Fund You

April 19, 2021 Another twist on purchasing receivables is making its way into the mainstream in the form of an Inheritance Cash Advance.

Another twist on purchasing receivables is making its way into the mainstream in the form of an Inheritance Cash Advance.

For some, the aftermath of losing a loved one can turn into a long drawn out legal process and delay the transfer of rightfully owed inheritance in the process. Probate funders fix the problem, paying cash upfront, purchasing the future receivable of a will. The small industry is remarkably similar to the merchant cash advance world and uses the same terminology. “Inheritance Cash Advances are not loans,” one website says, “with an Inheritance Cash Advance, we send immediate cash to heirs in exchange for an assignment of a fixed dollar amount of their eventual inheritance.”

David Horton, a University of California-Davis law professor who delved into 1,119 probate agreements in the San Francisco area as part of a UPenn Study, said of the product “in almost all cases, with rare exceptions, the lender not only gets their advance back but also gets a huge markup.”

Interestingly, this type of funding is most popular in California, where some of the most complicated estate laws in the country make inheriting a hassle. But a less than flattering industry profile in Consumer Reports says that such companies “earn millions offering cash advances to heirs, with effective interest rates as high as 490 percent.”

And yet, industry advocates say that they are providing a needed service. “We are proud of the service we provide and the highest ethical way we conduct our business at IFC,” said Doug Lloyd, CEO of Inheritance Funding Company to Consumer Reports. “It is easy to understand why banks and other financial institutions are not in this business.”

His company has already advanced more than $200 million to customers. The following video is featured on their website: