Loans

For Marketplace Lending Securitizations, A Bumpy Road But Strong Investor Sentiment

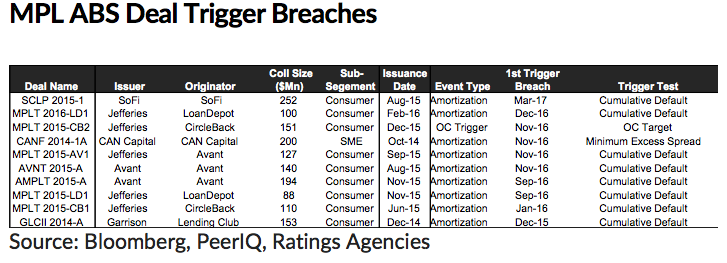

April 3, 2017A new report by published by PeerIQ contains 10 recent examples of trigger breaches in marketplace lending ABS transactions.

“Since the inception of MPL ABS market, we have observed 10% of deals breaching triggers historically,” the report says. It goes on to say that these events are typically manifestations of “unexpected credit performance, poor credit modeling, or unguarded structuring practice.”

“If an early amortization trigger is violated, excess spreads are diverted from equity investors to senior noteholders with the goal of de-risking the senior noteholders as quickly as possible.”

CAN Capital is the lone small business lender on the above list and we reported on their trigger breach back in December. Little public information has come out about the company since they stopped lending late last year.

![]() The most recent trigger breach on the list was SoFi, a company known for courting super prime borrowers.

The most recent trigger breach on the list was SoFi, a company known for courting super prime borrowers.

“Trigger breaching events do not necessarily imply credit deterioration of the collateral pool,” the PeerIQ report states. In another section of the report that addresses increased losses for non-bank lenders, it says that two of the three primary drivers of that are borrowers stacking loans and lenders shifting to riskier borrowers.

Nonetheless, Q1 was a record quarter for marketplace lending securitizations with seven deals priced for $3 billion. That’s a 100% increase over Q12016. “The industry continues to experience strong investor sentiment as evidenced by growing deal size and improved deal execution,” they say.

“We expect higher volatility from rising rates, regulatory uncertainty, and an exit from a period of unusually benign credit conditions. Platforms that can sustain low-cost stable capital access, build investor confidence via 3rd party tools, and embrace strong risk management frameworks will grow and acquire market share.”

In This Online Lender’s Earnings Report, Profits, MCAs and Term Loans

March 22, 2017Limited details were offered when Enova, a publicly traded company, acquired The Business Backer (TBB) in June 2015. For one, the Cincinnati Business Courier had the exclusive, which one might not describe as the typical go-to source for online finance news. But TBB was not typical. Based in Blue Ash, Ohio as opposed to New York City or San Francisco, the company had originally focused on offering merchant cash advances before eventually expanding their suite of solutions to include other products.

According to Enova’s earnings report, TBB had been purchased for $26.4 million with an estimated contingent $5.7 million of that being based on future earn-out opportunities. There was a caveat though. If future operating results exceeded expectations, that contingent amount could increase over time, but not beyond where the total consideration paid for the company exceeded $71 million. As of 2016’s year-end, that contingent amount had increased by $3.3 million.

Enova’s report makes several mentions of their merchant cash advance business or as they call them, receivable purchase agreements (RPAs). For the most part, they obscure the financial metrics of this aspect by lumping it in with installment loans. These installment loans are described as “multi-payment unsecured consumer installment loan products in 17 states in the United States and in the United Kingdom and Brazil” with repayment periods of two to sixty months, so yeah, they’re pretty different.

Their RPA customers, however, “average approximately $1.5 million in annual sales and 10 years of operating history while those who obtain an open line of credit account average approximately $450 thousand in annual sales and 7 years of operating history,” the report says. These lines of credit are primarily offered through a business lending subsidiary called Headway Capital.

While companies like Lending Club and OnDeck grab all the headlines, Enova describes itself as a “leading technology and analytics company focused on providing online financial services.” And in 2016, they extended nearly $2.1 billion in credit to borrowers and had a net income of $34.6 million.

On the company’s Q4 earnings call in February, Company CEO David Fisher said, “There currently seems to be a bit of a shakeout occurring in the non-bank small business lending and financing industry. A number of our competitors have either ceased funding or completely shut down over the past several months. From the intelligence we were able to gather, this is largely due to credit issues and their portfolios. As we mentioned last quarter, we have taken a more methodical approach than some to growth for our small business products. And we’re now seeing the benefits of that approach. Recent advantages of our small business book are performing well and the unit economics continue to improve especially as acquisition costs have dropped following the shakeout I just mentioned.”

Enova’s small business financing portfolio only constituted 12% of their loan portfolio at the end of last year. And at $13.70 a share, the company’s current market cap is larger than OnDeck’s.

SoFi Plays It Safe With Super Bowl Ad – And Kind of Wants to Be Your Bank

February 6, 2017“Here’s to conquering more together in 2017,” SoFi’s Super Bowl ad asserts. The company wants to help you own a home, start a family and see the world. They essentially want to be your bank for life, and now that their acquisition of Zenbanx allows them to offer checking accounts, they pretty much can be. It was no surprise then that their infamous tagline “Don’t Bank” was nowhere to be found in their Super Bowl ad. Watch below:

The ad they ran last year received criticism for labeling people as either great or not great. Maybe it wasn’t the best approach, but it was a very SoFi thing to do at the time.

This year, the only thing missing from their feel-good we-want-to-be-with-you-through-all-your-life-milestones ad is a voice coming on at the end to say “There are some things money can’t buy, for everything else, there’s MasterCard.”

Perhaps SoFi will consider changing their slogan from Don’t Bank to Bank With Us. It’s only a matter of time.

Google Banned Five Million Payday Loan Ads Last Year

February 3, 2017 After Google suspiciously decided to permanently ban payday lending ads from their search results last year, they had to disable more than 5 million payday loan ads, Google’s Sean Spencer wrote in a blog post. They also “took action on 8,000 sites promoting payday loans,” he said.

After Google suspiciously decided to permanently ban payday lending ads from their search results last year, they had to disable more than 5 million payday loan ads, Google’s Sean Spencer wrote in a blog post. They also “took action on 8,000 sites promoting payday loans,” he said.

For years, Google had no problem with payday lending or the advertising revenue it generated for them. In fact, in November 2013, an affiliate company, Google Ventures, even invested in a payday lending company named LendUp. But the harmony was short-lived. Eventually, Google’s search team would ban LendUp and every other payday lender from running ads on their platform after what appears to be government pressure.

- In May 2016, Google announced they would be banning payday loan ads.

- In July, that ban started to go into effect.

- In September, the CFPB announced it had taken action against LendUp, citing deceptive practices and internet ad campaigns that violated federal laws.

Google now reports having banned more than 5 million payday loan ads from that time. Other categories were worse, however. Google also had to ban 17 million ads that promoted illegal gambling and 68 million that offered bad healthcare products such as illegal pharmaceuticals.

Some ads still sneak through or try to sneak through. “Bad actors know that ads for certain products—like weight-loss supplements or payday loans—aren’t allowed by Google’s policies, so they try to trick our systems into letting them through,” Google’s Spencer wrote. “Last year, we took down almost 7 million bad ads for intentionally attempting to trick our detection systems.”

LendUp, the company Google Ventures invested in, is still in business.

Meet the Online Lender That’s Made $100 Billion in Loans

January 31, 2017Here’s a milestone for you, loanDepot has funded more than $100 billion in loans since they were founded in 2010. Mortgage loans may have enabled them to hit such a higher number in a short amount of time, but they also have a robust personal loan business. The two have more in common than you might think.

One trend that loanDepot CEO Anthony Hsieh shared when he spoke at the Marketplace Lending & Investing Conference back in September, is that since the Great Recession, borrowers that would have traditionally sought a home equity line, have instead been applying for personal loans. They know this because the credit and financial profiles between their home loan borrowers and personal loan borrowers is virtually identical, Hsieh said.

loanDepot celebrated making $100 billion in loans by publishing this video. Have a look:

The Leads Are Weak, Court Rules

January 21, 2017 One disagreement that has come out of the Argon Credit bankruptcy case is the value of the consumer loan leads that the company has in its possession. Argon argued that it has 300,000 leads worth $5.5 million based on its alleged cost to acquire them.

One disagreement that has come out of the Argon Credit bankruptcy case is the value of the consumer loan leads that the company has in its possession. Argon argued that it has 300,000 leads worth $5.5 million based on its alleged cost to acquire them.

In a court filing, Fund Recovery Services, LLC (FRS), a creditor, called that valuation “absurd on its face,” explaining that these were prospects that Argon had already declined for a loan and that they had not been able to sell these leads previously. A representative for FRS testified that the leads might be worth somewhere between a 1/2¢ and 1¢ each, giving them a value of only $1,500 on the lower end.

Presented with two completely different valuations for the leads, one for $1,500 and one for $5.5 million, the court ruled that it did not find Argon’s valuation credible and could not attribute any significant value to the leads.

Argon had hoped to use the leads’ value as collateral to keep the creditor at bay so that it could continue to spend its cash while the proceedings play out. The bankruptcy has been changed from Chapter 11 to Chapter 7.

The court has yet to rule on the motion to preclude non-closers from drinking the coffee.

New Industry Group Established to Support Consumers’ Right to Access their Financial Data

January 19, 2017The Consumer Financial Data Rights (CFDR) group defends consumers’ access to their data and fuels new innovation in fintech

REDWOOD CITY, Calif., Jan. 19, 2017 /PRNewswire/ — The Consumer Financial Data Rights (CFDR), a new industry group formed by some of the most recognized companies in the financial sector, officially launched today in support of the consumers’ right to innovative products and services that improve their financial well-being and are powered by unfettered access to their financial data. As fintech companies increasingly collaborate with banks around the world to provide innovative solutions through open application program interfaces (APIs), this right ensures a consumer can continue to give permission to third party companies to use that individual’s data for managing their personal finances, obtaining loans, making payments, and providing investment advice in addition to many other applications.

The CFDR brings together organizations from across the fintech ecosystem and includes some of the most influential and innovative companies in the financial sector, including the following founding members: Affirm, Betterment, Digit, Envestnet | Yodlee, Kabbage, Personal Capital, Ripple, and Varo Money among many other companies.

Section 1033 of Dodd-Frank codified the consumers’ right to access their personal financial data through technology-powered third party platforms. Together with promoting consumer choice and access to these consumer-first financial health tools, the CFDR is also committed to improving dialogue throughout the financial industry, actively engaging the government and working with banks, fintech innovators, and third party platforms. The CFDR aims to be a resource for policymakers, including the Consumer Financial Protection Bureau, as they determine how to best assist consumers in leveraging their own financial data.

“Each consumer’s right to their own financial data is vital in helping to understand their finances and make the best saving and spending decisions,” said Max Levchin, Founder and CEO of Affirm. “As a company we’re committed to helping customers make the best financial decisions and improve their financial lives through technology and improved flexibility, and having a complete picture of a customer’s financial picture is essential to achieving this. As a founding member of the CFDR, we’re committed to ensuring that all consumers have access to data which makes their financial lives better.”

“Consumers and small business owners need to be able to view their entire financial picture to make decisions that are truly in their best interests,” said Rob Frohwein, Co-Founder of Kabbage. “The ability to freely access financial data empowers customers to take actions to improve their financial lives, whether it’s accessing capital to grow a business or better understanding their income streams. Access to financial data is not just vital for customers wanting to enjoy financial health, but it also allows companies to provide better user experiences. Kabbage is thrilled to join other companies also committed to democratizing access to financial data.”

CFDR’s first action will be the submission of a joint comment letter in response to an advanced notice of proposed rulemaking on Enhanced Cyber Risk Management Standards issued by the Federal Reserve, Office of the Comptroller of the Currency, and Federal Deposit Insurance Corporation. The submission will encourage the regulators to establish a risk hierarchy with regard to cybersecurity risk in the fintech industry and will note the importance of continuing to allow consumers to access secure tools that enable their financial well-being.

“Consumers have the right to access financial solutions that allow them to improve their financial well-being,” said Anil Arora, CEO of Envestnet | Yodlee. “The CFDR is committed to initiatives that enable fintech innovation in the United States, much of which has transpired globally including recent open API initiatives in Europe, the Open Banking standard in the UK, and the commitment by the Monetary Authority of Singapore to create an open API economy and promote the secure use of cloud environments. The consumers’ right to unfettered access to their financial data will help enable the continued growth of innovative financial technologies and ultimately help consumers improve their financial health.”

About Consumer Financial Data Rights (CFDR)

The Consumer Financial Data Rights (CFDR) is a new industry group formed by some of the most recognized companies in the financial sector, launched to support the consumers’ right to unfettered access to their financial data. Open data acess is critical to enabling innovative tools that can help consumers improve their financial lives. CFDR members seek to: drive financial innovation in a collaborative ecosystem by bridging the needs of consumers, banks, fintech innovators, and regulators; partner with banks to support unfettered access to consumer and small business data through a secure and open financial system; and promote consumer rights to access and share their financial data with third party companies that provide tools to enable better financial outcomes.

SOURCE Envestnet | Yodlee

+1 for Swift Capital, -1 for Lending Club

December 15, 2016Swift Capital has named Tim Naughton as Chief Legal Officer, according to a company announcement on Thursday. “Prior to joining Swift Capital, Naughton advised Bank of America’s small business lending and deposit services as assistant general counsel and senior vice president,” it says. “He served as external counsel for American Express and Sallie Mae, and was a partner at Hudson Cook specializing in financial and regulatory compliance.”

Hudson Cook law firm coincidentally produced the merchant cash advance industry’s training course.

Meanwhile, Lending Club disclosed in an 8-K Thursday that CTO John MacIlwaine had tendered his resignation “to pursue another opportunity.” MacIlwaine had been with the company for more than 4 years. He is the latest of several C-level execs to depart in 2016. Former CEO Renaud Laplanche resigned in a scandal earlier this year and CFO Carrie Dolan, like MacIlwaine, also resigned “to pursue another opportunity” back in August. Other executives including Jeff Bogan and Adelina Grozdanova, Lending Club’s Head of Investor Group and Vice President, Head of Institutional Investors respectively, also both resigned in May. Lending Club’s stock is down more than 50% since the beginning of the year.