Industry News

OnDeck Funded $591M to Small Businesses in Q1

May 8, 2018 OnDeck’s originations were $591 million in Q1 of this year, according to their earnings report, up 3% year-over-year. 29% of that was generated by funding advisors, OnDeck’s term for brokers.

OnDeck’s originations were $591 million in Q1 of this year, according to their earnings report, up 3% year-over-year. 29% of that was generated by funding advisors, OnDeck’s term for brokers.

They reported a total net loss of $1.9 million.

Compared to the same quarter last year, OnDeck’s Cost of Funds Rate increased from 5.9% to 6.8%, the 15+ Day Delinquency Ratio decreased from 7.8% to 6.7%, the Net Charge-off Rate decreased from 14.9% to 10.9%, and their average APR increased from 44% to 46%.

During the Q&A, OnDeck CEO Noah Breslow said that they had a strong quarter with Chase originations and that their second major bank is on track to be announced later this year.

Elevate’s Net Income Soared in Q1 Year-Over-Year

May 6, 2018 Elevate’s net income increased 459 percent from $1.7 million in Q1 2017 to $9.5 million in Q1 2018, according to the company’s Q1 financial statement released on April 30th.

Elevate’s net income increased 459 percent from $1.7 million in Q1 2017 to $9.5 million in Q1 2018, according to the company’s Q1 financial statement released on April 30th.

“What you are now seeing is a business beginning to leverage its scale in a market that is almost boundless,” said Elevate CEO Ken Rees. “We are gratified by our strong start to 2018 and by the fact that we’ve done it offering what we believe are the most responsible credit products available to non-prime borrowers today.”

Elevate (NYSE: ELVT) provides funding solutions to non-prime consumer customers. They offer three products: RISE, a state-licensed online lender that offers up to $5,000 in unsecured installment loans and lines of credit, Elastic, a bank-issued line of credit, and Sunny, a short-term loan product for customers in the UK. RISE and Elastic serve the US market.

The RISE product has performed well, likely buoyed by the hiring of Tony Leopold a year ago to build on the product. Elevate is still new as a public company. It recently celebrated its one year anniversary on the New York Stock Exchange in April.

According to the Q1 earnings report, the total number of new customer loans for the first quarter of 2018 was approximately 70,000, an increase of 32.1 percent compared to approximately 53,000 new customer loans in the first quarter of 2017.

Founded in 2014, the Fort Worth, TX-based company has originated $5.5 billion to 1.9 million customers. The company also has offices in Dallas, TX, San Diego, CA, and in the UK, in London and Bury St. Edmunds.

Newtek Funds $91 Million in 7(a) loans in Q1

May 3, 2018 Newtek (Nasdaq:NEWT), a provider of business and financial solutions, funded $91.4 million of SBA 7(a) loans in the three months ending March 31, 2018, according to the company’s Q1 2018 earnings report released yesterday. This is an increase of 16.2 percent year-over-year from $78.6 million funded in SBA 7(a) loans in the three months ending March 31, 2017.

Newtek (Nasdaq:NEWT), a provider of business and financial solutions, funded $91.4 million of SBA 7(a) loans in the three months ending March 31, 2018, according to the company’s Q1 2018 earnings report released yesterday. This is an increase of 16.2 percent year-over-year from $78.6 million funded in SBA 7(a) loans in the three months ending March 31, 2017.

On this morning’s phone call, CEO Barry Sloane was particularly pleased to announce Newtek’s loan referral growth of 86.9 percent from Q1 2017 ($2.6 million) to $4.8 million in Q1 2018.

“It gives us the ability to make selection on opportunities that come to us directly from business owners,” Sloane said, “without the use of brokers, and pick the best credits available.”

Newtek also closed on $3.9 million in SBA 504 loans for the three months ending on March 31, 2018. SBA 504 loans provide approved small businesses with long-term, fixed-rate financing used to acquire fixed assets for expansion or modernization.

The New York-based company was founded in 1998, went public in 2000, and has been a BDC (Business Development Company) for three and a half years. BDCs are publicly traded companies that make investments in private companies in the form of loans or equity securities. And the structure provides certain tax advantages, according to Solar Capital.

Newtek acquired United Capital Source in October 2017, which is still led by its original CEO Jared Weitz, who was featured in deBanked’s September/October 2015 issue.

Newtek had a net investment loss of $2.8 million for Q1 2018.

Aside from the company’s headquarters in Lake Success, NY, Newtek also has loan processing offices in Orlando, FL and Boca Raton, FL.

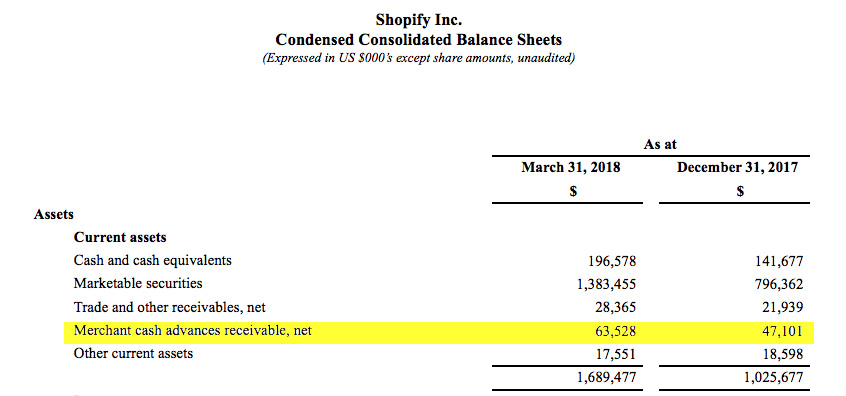

Shopify Capital Issued $60.4M in Merchant Cash Advances in Q1

May 1, 2018 Shopify Capital, Shopify’s small business funding arm, issued $60.4 million in merchant cash advances in Q1, according to the company’s earnings report, an increase of more than 300% year-over-year. The company has advanced $230 million to merchants since April 2016.

Shopify Capital, Shopify’s small business funding arm, issued $60.4 million in merchant cash advances in Q1, according to the company’s earnings report, an increase of more than 300% year-over-year. The company has advanced $230 million to merchants since April 2016.

On the company’s earnings call, Canaccord Genuity equity researcher David Hynes, inquired about the patterns of seasonal demand one could expect for the company’s merchant cash advances.

“So in terms of seasonality on Shopify Capital,” said Shopify COO Harley Finkelstein, “it’s important to note that the use of proceeds for Shopify Capital for most of our merchants tend to be in the realm of inventory or marketing spend, which we quite like, because that leads to more sales, which makes it easier for them to return the capital to us.

“Obviously, there’s the seasonality of capital reflecting the seasonality of retail in general, which is certainly more of a Q4 issue than it is a Q1 issue,” he added.

Canaccord’s Hynes also referred to Shopify’s product as a loan but was corrected by Finkelstein.

“Just keep in mind, these are not loans, these are cash advances, so I want to be very clear about that,” Finkelstein explained.

Shopify is a Canadian e-commerce company headquartered in Ottawa, Ontario. It is also the name of its proprietary e-commerce platform for online stores and retail point-of-sale systems

View the company’s earnings report here

BlueVine Announces $200 Million Credit Facility

May 1, 2018

BlueVine announced today that it has secured a $200 million asset-backed revolving credit facility with Credit Suisse. This will be used to expand its business line of credit product and the company’s customers will now be eligible for a credit line of up to $250,000.

“Capital markets partnerships are critical to our ability to scale and effectively serve our expanding customer base,” said BlueVine CFO Ana Sirbu. “This financing will support our next phase of growth [as] we continue to build a business for the long-term by offering the best working capital financing solutions to business owners.”

The company offers two products – invoice factoring and business lines of credit. The latter was introduced in January 2016 with a maximum credit line of $30,000, Sirbu told deBanked. That maximum soon became $50,000 and has steadily risen. In February, the company increased its business line of credit from $150,000 to $200,000.

Founded in 2013 by CEO Eyal Lifshitz, the company first offered only factoring in March 2014. Now, Sirbu said that the breakdown of its business is about even between its factoring and business line credit offerings.

This is BlueVine’s first facility with Credit Suisse. Not counting this facility, the company had $318 million in funding as of October 2017, according to Crunchbase.

BlueVine is headquartered in Redwood City, CA, with other offices in Jersey City, NJ, New Orleans, LA, and a large office in Tel Aviv, Israel, where most of its Research and Development team is based. Altogether, BlueVine employs about 200 people.

Yellowstone Capital Funded $61 Million in April

May 1, 2018Yellowstone Capital originated $61 million in funding to small businesses in April, according to the company. The year-to-date total now exceeds $200 million.

Yellowstone Capital, which is based in Jersey City, NJ, originated $553 million in 2017.

Kabbage Acquires Orchard

April 26, 2018

Following speculation, Kabbage officially announced today that it has entered into a “definitive agreement” to acquire Orchard, a financial technology and analytics company that provides data to lenders and investors.

“I’m most excited about the people [at Orchard] because, while they’ve built this amazing technology, it takes a long time to get the right people in place,” said Kabbage co-founder Kathryn Petralia. “And they’ve built a great culture and great company of talented individuals who I think really understand the industry…and can help us get to where we’re trying to go.”

Kabbage and Orchard have enjoyed a working relationship for some time already, Petralia told deBanked. (Kabbage has been a client of Orchard).

More than 20 employees from New York-based Orchard will move to Kabbage’s New York office, including two of its founders, Matt Burton and David Snitkof. The company was founded in 2013 by Burton and Snitkof, along with Angela Ceresnie and Phil Rosen.

Burton previously worked at Google and Snitkof previously worked at Citigroup and American Express.

“Like most businesses, we often listened to interesting offers, but never found the best fit. Until Kabbage,” Snitkof said of its decision to be acquired by Kabbage. “Everything from their mission, technology focus and culture is aligned with Orchard. [And] there are really interesting innovations we can do together by combining our data science platforms.”

Orchard has a proprietary technology platform that simplifies mass-data analysis and Kabbage has a forecasting and predictive analytics engine that strengthens its automated underwriting platform. Together, they hope to create an even stronger platform that helps small businesses access capital quickly and efficiently.

“Integrating our two data science platforms will take time, but we’re excited for what’s to come,” said Snitkof.

Almost ten years old, this is Kabbage’s first acquisition. Asked if the company is “on a buying spree,” Petralia said no, but also acknowledged that they are now in a position to make acquisitions, like Orchard, that can help them build their business faster, as long the acquisition makes sense.

Founded in 2009, Kabbage is headquartered in Atlanta and has provided over $4 billion to more than 130,000 businesses.

Ascentium Capital Surpasses $4 Billion in Originations

April 18, 2018 Texas-based lender Ascentium Capital announced last week that it had surpassed $4 billion in origination volume since the company was founded in 2011.

Texas-based lender Ascentium Capital announced last week that it had surpassed $4 billion in origination volume since the company was founded in 2011.

The company has two key channels of business. The vendor channel, in which Ascentium creates custom finance programs for clients like equipment manufacturers, distributors and resellers. It calls these clients its “vendor partners.”

“We do a lot of our business with vendor partners, typically [a company] selling something to a small business,” said Ascentium Capital CEO Tom Depping.

The other business channel is a direct channel where Ascentium makes direct loans to small and medium sized businesses of up to $250,000. Depping told deBanked that the company’s direct channel makes up about 30 to 40 percent of its business. Not an insignificant percentage. But he said that the company’s primary business is equipment finance via vendor partners.

Ascentium gets its leads from an internal sales team of 120 people and Depping said that he anticipates adding 50 additional sales people this year. Why the significant growth?

“Our award-winning finance platform, elevated levels of efficiencies and our personalized service continue to drive demand for our financial products,” said Depping. “Everything with us is very simple and very fast.”

The company currently employs 250 people with headquarters in Kingwood, TX, near Houston, with smaller offices in Dover, NH and Irvine, CA. Depping also counts 30 to 40 locations throughout the country where Ascentium Capital sales people either work from home or in micro-offices of one to two people.