Fintech

Elevate Tests ‘Geofencing’ to Lure Customers Away from Competition

November 1, 2018 During a session at Money 20/20 last week, Elevate CEO Ken Rees mentioned a fairly new marketing technique they have been testing called geofencing. According to a story in CIO, a trade publication for Chief Information / Chief Technology Officers, geofencing is “a service [using GPS technology] that triggers an action when a device enters a set location.” For Elevate, these set locations are payday loan stores and the idea is for the company to detect and then market to prospective customers who may have recently visited a payday loan store. People visiting such stores would likely be good candidates for Elevate’s Rise product.

During a session at Money 20/20 last week, Elevate CEO Ken Rees mentioned a fairly new marketing technique they have been testing called geofencing. According to a story in CIO, a trade publication for Chief Information / Chief Technology Officers, geofencing is “a service [using GPS technology] that triggers an action when a device enters a set location.” For Elevate, these set locations are payday loan stores and the idea is for the company to detect and then market to prospective customers who may have recently visited a payday loan store. People visiting such stores would likely be good candidates for Elevate’s Rise product.

“It can’t be a completely [random person,]” Elevate’s COO Jason Harvison told deBanked. He explained that the prospective customer had to have somehow engaged previously with Elevate, which could mean that they visited Elevate’s website.

Daniel Rhea, Elevate’s Senior Communications Manager, said that they don’t have the ability follow people. Instead, what they can do is tell when someone gets near one of their targets (payday loan stores) and then present them with ads. The mobile ads are not served immediately. Rhea said that ads could be served to someone who entered the target zone up to 90 days later.

“We’re not trying to get you at that exact moment,” Harvison told deBanked. “It’s not something that’s going to interfere with your transaction at a payday loan store, but it’s going to inform you that there is a better option out there.”

According the CIO article, retailers use geofencing to market to people who are in the vicinity of their stores. The technology is also being used for home convenience (to turn on a thermostat when someone arrives at their house) and for security (to alert a someone when others enter or leave their home or business).

Many of these uses of geofencing require that an app is downloaded to the user’s phone. Elevate system does not involve an app, but the individual’s location services on their phone must be turned on. So how can Elevate identify people within its target zones? As an example, Rhea said that if you use the public wifi at a Starbucks, Elevate can identify you. And he said that the same applies for when someone uses bluetooth.

“There’s a lot of people [using] this,” Rhea said. “Politicians are microtargeting around polling stations. It’s not that it’s uncommon. It might be uncommon in our space.”

Rhea said that this program, which started at the beginning of 2018, is still in a pilot phase, but that Elevate hopes to place geo-targets around every payday loan store in the country.

“[If you’re going to a payday loan store,] we want to try to entice you to not take out a product in a storefront and use a more consumer-friendly product that we take to market,” Harvison said.

Prime and Non-prime Lenders Exchange Notes

October 25, 2018 Ken Rees, CEO, Elevate

Ken Rees, CEO, ElevateAt Money 20/20 Ken Rees, CEO of Elevate, a non-prime consumer lender, sat down with David Kimball, CEO of Prosper, a prime consumer lender. As they discussed a number of topics, listeners got insight into how these lenders think, and how they think differently based on the customers they serve.

On Partnering with Banks

Rees said that he is eager to partner with banks and that banks have spoken to him about a gap they have – namely, the fact that they have thousands, if not millions, of checking account customers with low Fico scores for whom they have no other products to offer. Elevate has products for these banks’ non-prime customers.

“Banks have customers and we want to work with them,” Rees said.

Rees said that the very large banks may have the resources to develop new products on their own, but that there are thousands of mid-sized banks to partner with.

Kimball, who was CFO of USAA Federal Savings Bank, had some advice for fintechs on how to approach a potential partnership with a bank.

“Don’t go in thinking they’re stupid,” he said. “Assume that you have a really good partner.”

Furthermore, Kimball said that having worked at a bank during the recession, “when you break things, regulators aren’t so happy to work with you again.” By this, he meant that bankers may have very legitimate concerns about taking on risk by working with a fintech company.

Kimball continued, “You need a good champion at the right level [at a bank] to move you forward.”

David Kimball, CEO, Prosper

David Kimball, CEO, ProsperOn a Looming Recession

Kimball said that Prosper is being more conservative with its underwriting now. On the other hand, Rees said that a recession doesn’t concern him as much.

“Our customers are always living in a recession,” Rees said.

On Speed vs. Rate

“For prime customers, it’s all about rate. For non-prime, it’s all about speed, how fast they can get the money,” Rees said.

On Marketing

Kimball said that direct marketing still works best to get new customers, while Rees mentioned a new geo-marketing tool that alerts Elevate when a potential customer approaches a payday lending shop. Someone visiting a payday lending shop would likely be a good customer for Elevate. Rees conceded that “this could be kind of creepy.” But it’s a new approach.

Heard at Money 20/20

October 24, 2018Shaquille O’Neal, Basketball legend and startup investor

O’Neal appeared at the conference on behalf of Steady, a startup he supports that helps people find work relevant to their skill set and location.

“I like being involved in companies that help people people,” O’Neal said. “With Steady, we want to help people gain income. It shouldn’t be hard to find work.”

When asked about other companies he involved with, he said, “I listed all the companies once and my mom said, ‘It sounds like you’re bragging, so cut it out.’ So I don’t talk about them anymore, because my mom’s out in there in the audience somewhere.”

Basketball Legend and Advisor & Advocate of @thesteadyapp, @SHAQ reveals his new nickname at the final of the Startup Pitch at #money2020 pic.twitter.com/ZhDGbCi9DN

— Money20/20 (@money2020) October 24, 2018

Rob Frohwein, Kabbage Co-founder

Frohwein said his company noticed that its customers were borrowing a little less money after they were issued Kabbage’s card.

“It was because customers were borrowing the exact amount they needed at the point of purchase.”

At first, Frohwein said they were concerned, but that ultimately “customers aren’t over-borrowing…and that’s excellent for customer loyalty.

Anthony Noto, SoFi CEO

Noto said he went to West Point for college, which was completely free for him. He said that he could have gotten student loans to attend other prestigious colleges, but he didn’t know if he could afford to pay it back.

With regard to how higher interest rates are affecting SoFi, he said, “higher interest rates have made our underwriting more conservative [and have forced us] to focus on quality.”

On the topic of potentially becoming an Industrial Loan Company (ILC) bank:

“An ILC could be in our future so that we have the same rates across all states we operate in…We are regulated and we’re comfortable with that.”

Breslow Shows What a Fintech/Bank Partnership Looks Like

October 24, 2018 In the wake of OnDeck’s announcement of ODX, a new subsidiary that will service banks, OnDeck CEO and Money 20/20 veteran Noah Breslow took to the stage for a discussion with his new business partner, Lakhbir Lamba, Head of Retail Lending at PNC Bank. PNC will now be using ODX to originate lines of credit for the bank’s small business customers, while everything will stay on PNC’s balance sheet.

In the wake of OnDeck’s announcement of ODX, a new subsidiary that will service banks, OnDeck CEO and Money 20/20 veteran Noah Breslow took to the stage for a discussion with his new business partner, Lakhbir Lamba, Head of Retail Lending at PNC Bank. PNC will now be using ODX to originate lines of credit for the bank’s small business customers, while everything will stay on PNC’s balance sheet.

“We’re keeping a laser focus on small business lending,” Breslow said, when asked if OnDeck would begin to serve other segments of the market, like student or auto loans.

“The problems that small businesses face are worldwide,” Breslow said, indicating that the company has interest in expanding service to small businesses internationally. Already, OnDeck operates in Canada and Australia.

The moderator asked if an application that is rejected by PNC would become a lead for OnDeck. Breslow and Lamba said that is not currently the arrangement, but that it may be a possibility.

“Our goal [with ODX] is to service banks,” Breslow said, while acknowledging that banks serve a different kind of small business customer than OnDeck.

“We will make sure that we underwrite based on PNC’s risk appetite,” Breslow said.

Digital Mortgage Lender “Better” Goes Where No Fintechs Have Gone

October 8, 2018

One product noticeably absent from fintechs expanding into lending or banking is mortgage loans, but now a fintech startup is looking to disrupt the $13 trillion mortgage industry.

Eric Wilson is co-founder and head of operations at Better Mortgage, a New York-based digital mortgage lender. Wilson explained to deBanked:

“Our industry more than consumer lending is stuck in the pre-internet era and hasn’t been able to leverage the tools to make getting a mortgage feel as simple and as empowering as other products we’re used to consuming online. The industry was waiting for a company like ours to come along with the right skills and engineering staff.”

Better Mortgage is an end-to-end mortgage lender that matches investors interested in giving loans to a subset of consumers. “We take applications and compare with investors for the best price. Underwriting and communication with the borrower happen on the internet,” Wilson said.

The investors are large financial institutions that are in the business of buying mortgage loans.

“We are a direct lender. We originate mortgages. We don’t charge origination fees to customers. We make money when we sell those loans to the secondary market, whether it’s Fannie Mae or any one of our 28 partners,” said Paula Tuffin, Better Mortgage chief compliance officer and general counsel.

In addition to zero origination fees, Better has eliminated commissions. “For us, we believe you should be able to put your storefront online and have consumers find you. We don’t think it’s appropriate or necessary pay one individual to take $6,000 out of a $300,000 loan,” said Wilson.

Instead, Better relies on a team of loan consultants who are “full-time employees or better” who are incentivized to deliver a delightful customer experience,” said Wilson. This differs from the traditional broker model used by much of the industry. “We don’t deal with third-party mortgage brokers. This eliminates a lot of the potential for fraud and harm to investors,” he noted.

Pain Points

The “pain points,” he noted, tied to mortgage lending surpass that of personal or unsecured lending. For instance, greater amounts of data are needed for loans of this size, and there’s the complex and intensive process of risk underwriting, all of which is exacerbated by heavy regulation.

Unlike some of its fintech peers, Better Mortgage has no interest in pursuing an OCC special- purpose national bank charter, or fintech charter.

Wilson is a millennial who had a front-row seat to the mortgage crisis and all of the hardship that fell on consumers. “It was a result of irresponsible lending practices,” said Wilson, “and a failure by regulators to keep lenders in check. So to that end, we are champions of post-crisis Dodd Frank-era consumer protection regulation.”

While operating under a single regulator across all 50 states would streamline the process for Better, it would come at the high price of innovation. “It comes with some pretty hefty strings attached. That regulatory environment is often so challenging to navigate or requirements so onerous … that I would be hesitant to go head-first into a program like this,” said Wilson.

As a result, Better incurs the cost of taking a state-by-state approach, a burden that Wilson says the company is happy to bear: “If we were to pivot and get a bank charter issued by the OCC, we could transact in 50 states overnight. But our ability to innovate evaporates in the process.”

Better is licensed in 19 states and is making an expansion push in which it plans to operate in all 50 states in the first half of 2019. The minimum FICO score for a Better conforming mortgage product is 620.

“By and large, the market is shallow in the application of technology. We’re a tech company first and we acquired a mortgage company as opposed to being a mortgage company learning about tech. This gives us a fundamental advantage in the way we think about problems,” said Wilson.

Congressman Cleaver’s Findings on Fintech Lending Mixed

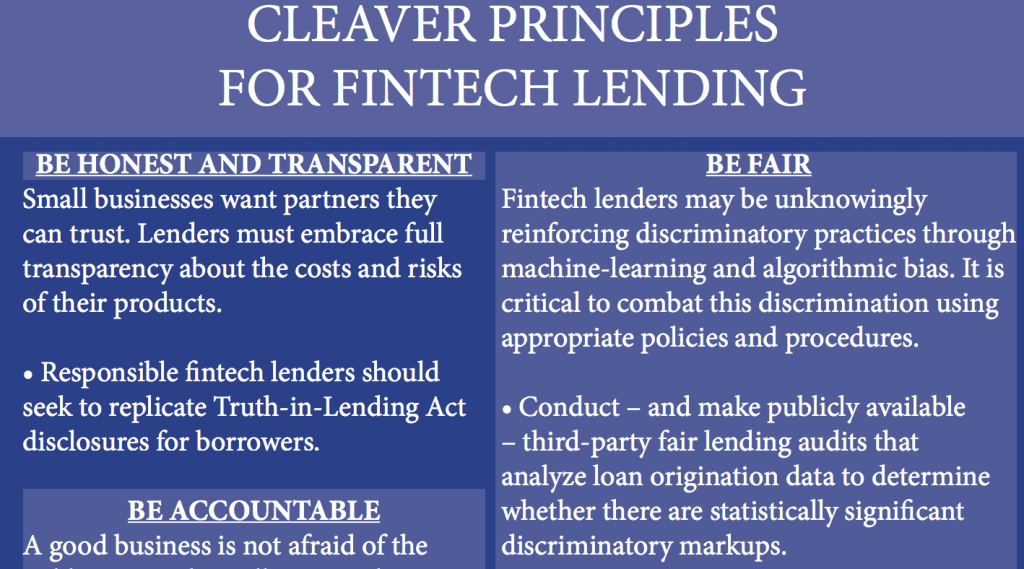

August 30, 2018 Congressman Emanuel Cleaver, II from Missouri announced findings earlier this month from a year-long inquiry he initiated into fintech small business lending practices and minorities. His initial inquiry was to determine if merchant cash advance companies had mechanisms in place to avoid discriminatory lending practices.

Congressman Emanuel Cleaver, II from Missouri announced findings earlier this month from a year-long inquiry he initiated into fintech small business lending practices and minorities. His initial inquiry was to determine if merchant cash advance companies had mechanisms in place to avoid discriminatory lending practices.

Cleaver concluded that some common practices in non-bank underwriting processes lend themselves to discrimination against minority business owners. One such practice is using a merchant’s personal credit score to determine a business’ credit worthiness, which the report maintains is unfair because “a personal credit score has little bearing on a business model or the owner’s business acumen, and using it unfairly punishes minority business owners who may not have had the same opportunities to build credit.” Another complaint is the common practice of having merchants sign forced arbitration clauses that forbid the borrower to take the lender to court.

The companies that he surveyed included OnDeck, Kabbage, Fora Financial, Lending Club, Biz2Credit and LendUp, even though Lendup only does consumer lending. And OnDeck, Kabbage and Lending Club don’t offer a cash advance product. Still, they make non-bank business loans.

The report also mentioned that algorithms used by some of these companies could inadvertently be discriminatory. That’s because they have the ability to incorporate the number of criminal records and bankruptcies in the merchant applicant’s zip code when making a funding decision. And these numbers tend to be higher in minority neighborhoods.

However, the report also highlighted some good practices, such as including a third party in the lending process to protect from engaging in unintentional discriminatory behavior.

“From the responses gathered,” the report reads, “it has become increasingly clear that a majority of the companies have taken some measure to prevent blatant discrimination. Nevertheless, additional protections are very much needed.”

“The initial findings are clear as day, Congressman Cleaver said in a statement about the report. “We need to further understand how lenders may be intentionally or unintentionally offering higher interest rates to minorities and underserved communities, and work to implement industry-wide best practices.”

Investment in Fintech Soars in 2018

August 6, 2018 Fintech investment in the Americas reached a new high of $14.8 billion for the first half of 2018, according a KPMG report. This was spread across 504 deals. The bulk of the investment, $14.2 billion, went to U.S. companies.

Fintech investment in the Americas reached a new high of $14.8 billion for the first half of 2018, according a KPMG report. This was spread across 504 deals. The bulk of the investment, $14.2 billion, went to U.S. companies.

Big fintech deals in the U.S. this year spanned a range of sub-industries, from blockchain (R3, Circle Internet) and Cryptocurrencies (Basis) to Insurtech (Lemonade, Oscar) and wealth management (Robinhood). The largest deal of the year was the acquisition of Boston-based Cayan, a payment technology company, by global payments solutions provider TSYS, for $1.05 billion.

While the U.S. accounted for the majority of fintech investment in the Americas, there was notable fintech investment in other countries. Brazil-based Nubank held the fourth largest VC round in the Americas during the first half of the year with a $150 million Series E raise.

“While an outlier in terms of deal size, the Nubank deal highlights the growing importance VC investors are placing on Brazil as an epicenter for fintech innovation in Latin America,” the report read.

Fintech investment in Canada continued to evolve in the first half of 2018 with $263 million in total. However, this was actually a decrease compared to the second half of 2017 which brought in $510 million for Canadian fintech companies.

The Canadian government is in the process of updating its Bank Act, which is expected to occur in 2019. And Payments Canada, a government organization, is also undertaking a multi-year payments modernization initiative aimed at upgrading critical infrastructure. According to the KPMG report, while both of these initiatives are in the process of happening, VC investors and fintechs recognize that change is coming and are trying to position themselves to take advantage of the changes once they are implemented. San-Francisco based fintech, Plaid Technologies, announced in May of this year that it would be expanding into the Canadian market. The report indicates that other U.S. companies will likely follow suit.

Can Fintech Startups Become Banks? OCC Opens The Gates

August 1, 2018 Yesterday, the U.S. Treasury Department released a report that prompted the Office of the Comptroller of the Currency (OCC) to say that it would start accepting applications from fintech for special purpose national bank charters.

Yesterday, the U.S. Treasury Department released a report that prompted the Office of the Comptroller of the Currency (OCC) to say that it would start accepting applications from fintech for special purpose national bank charters.

This is boon for fintech companies that, until now, have mostly been prevented from applying for national bank charters because of protest from banks and others that they will not be subject to adequate regulations. But now the OCC, a significant regulator, is opening the door for non-depository fintech companies – like OnDeck and Kabbage – to become banks.

“Over the past 150 years banks and the federal banking system have been the source of tremendous innovation that has improved banking services and made them more accessible to millions,” said head of the OCC, Comptroller of the Currency, Joseph M. Otting, in a statement. “The federal banking system must continue to evolve and embrace innovation to meet the changing customer needs and serve as a source of strength for the nation’s economy…Companies that provide banking services in innovative ways deserve the opportunity to pursue that business on a national scale as a federally chartered, regulated bank.”

The main advantage for fintech companies of having the opportunity to get their own bank charter is that they would now be able to operate nationwide under a single licensing and regulatory system, instead of a myriad of state licenses. Currently, fintech companies must adhere to the regulations in each state where they do business, which can be expensive. And some states have regulations that are stricter than others. That is why this news is bad news for states that feel that this development will allow fintech companies to bypass and undermine their regulation designed to protect consumers.

The OCC’s decision is the latest development in a years long, sustained effort by fintechs to become banks. In fact, for the last several years, Fintech companies have tried attaining bank status by getting the Utah Department of Financial Institutions to allow them to become Industrial Loan Company (ILC) banks. So far, Square, SoFi and NelNet have tried, in some capacity, to become an ILC bank.

The New York Department of Financial Service and the Conference of State Bank Supervisors (CSBS) was angered by the OCC’s decision.

“An OCC fintech charter is a regulatory train wreck in the making,” said CSBS President John W. Ryan in a statement. “Such a move exceeds the current authority granted by Congress to the OCC. Fintech charter decisions would place the federal government in the business of picking winners and losers in the marketplace. And taxpayers would be exposed to a new risk: failed fintechs.”

He said that his organization is keeping all options open to stop what he says is regulatory overreach.

The OCC indicated in its announcement that fintech companies that become special purpose national banks will be subject to heightened supervision initially, similar to other banks. But these special purpose banks would not have to abide by the stricter regulations of deposit-taking banks and they would not have to be insured by the Federal Deposit Insurance Corporation (FDIC) either.

“It is hard to conceive that insured national banks will allow the OCC to allow a fintech entity a national bank charter without insisting that all national bank obligations apply—which is what fintech companies want to avoid,” said Joseph Lynyak, partner and regulatory reform specialist at the law firm Dorsey & Whitney.