Business Lending

Can an ISO “Excel” in 2016?

August 26, 2016

Don’t let anyone tell you that it’s too hard for a commercial finance broker to make a buck in exchange for honest work these days. One ISO in lower Manhattan is seeing more opportunity than ever before. Chad Otar, a managing partner of Excel Capital Management, sat down with deBanked to make his case for a bright future.

“As long as there’s small businesses, there’s always going to be opportunity,” Otar said. “Business owners are always going to need money.” Ironically, his own company that he cofounded in 2013 with hometown friend Nathan Abadi, was formed without any outside debt. Bootstrapped even to this day and even as they’re expanding, they’ve seen firsthand what other businesses around the country have to go through to get ahead.

“We’ve always believed in the products that we’ve sold,” said Otar, who brokers merchant cash advances, business loans, SBA loans, factoring products and more. They want every deal to help their clients whether it’s big or small, explaining further that even he himself has to feel comfortable with what the merchant wants. When asked about size, Otar said the largest SBA loan they got done was for $4.9 million.

But when questioned if more merchants were moving towards factoring and other traditional products, he explained that some merchants just don’t want to deal with the hassle of something that might be overly invasive or a process that might take a long time. They just want to get funded quickly, he said. And that’s where they come in.

Otar and Abadi’s optimism is not just anecdotal. The two partners, who previously renewed one year leases for their small office on Maiden Lane, saw enough runway to recently sign a five year lease for a 2,700 sq ft. office on Greenwich Street, staying within the bounds of the city’s financial district. Between full time employees and contractors, they currently house about fifteen people in their new office.

Though the partners live in Brooklyn, they, like many other companies in the industry, believe a Manhattan headquarters makes the most sense. “Everything is here,” Otar said. It’s easier to recruit new hires, he explained. And they indeed have immediate hiring plans now that they’ve got the space for it, both in sales and operationally.

Though the partners live in Brooklyn, they, like many other companies in the industry, believe a Manhattan headquarters makes the most sense. “Everything is here,” Otar said. It’s easier to recruit new hires, he explained. And they indeed have immediate hiring plans now that they’ve got the space for it, both in sales and operationally.

This new up-and-coming generation of business owners is very comfortable with the Internet and technology, Otar added, speeding up the process and allowing they and the funding partners they work with to do more deals together. One example offered was a small business owner who gave a guided tour of his establishment to an underwriter using FaceTime on his phone. Normally, the process would’ve been delayed by a few days because of the time it takes to hire a third party to perform a site inspection.

Some funding partners offer DocuSign so that merchants don’t even have to spend time printing and signing documents anymore, he said, qualifying that however by adding that while some merchants love it, others hate it and feel more comfortable doing things the old fashioned way. He acknowledged that was likely due to the generational gap that still exists.

When asked if the setbacks and gloom that had begun to envelop the consumer lending side of fintech, was also affecting the commercial side, Otar said he didn’t see it. Funders are still very aggressive with approvals and terms, he said. While paperwork required for approval is declining overall, he described one obstacle that he hadn’t really dealt with in previous years, UCC filings that are accidentally left active even when the agreements are satisfied in full.

Underwriters doing due diligence might interpret active UCCs to mean that outstanding obligations still exist. Absent a formal termination of the UCC, an underwriter may request that merchants provide documents from the secured party to support that a termination should’ve been filed. This in itself is not a burdensome task but Otar said he has seen merchants who have used alternative financing products continuously over the last eight years or so, who are then challenged to produce satisfaction letters from dozens of companies, some of whom the merchant may only vaguely remember.

But he is not discouraged when new challenges come up. “We’ve been constantly learning,” he said. And when asked what their secret to success has been up until this point, “It’s hard work and dedication,” he responded.

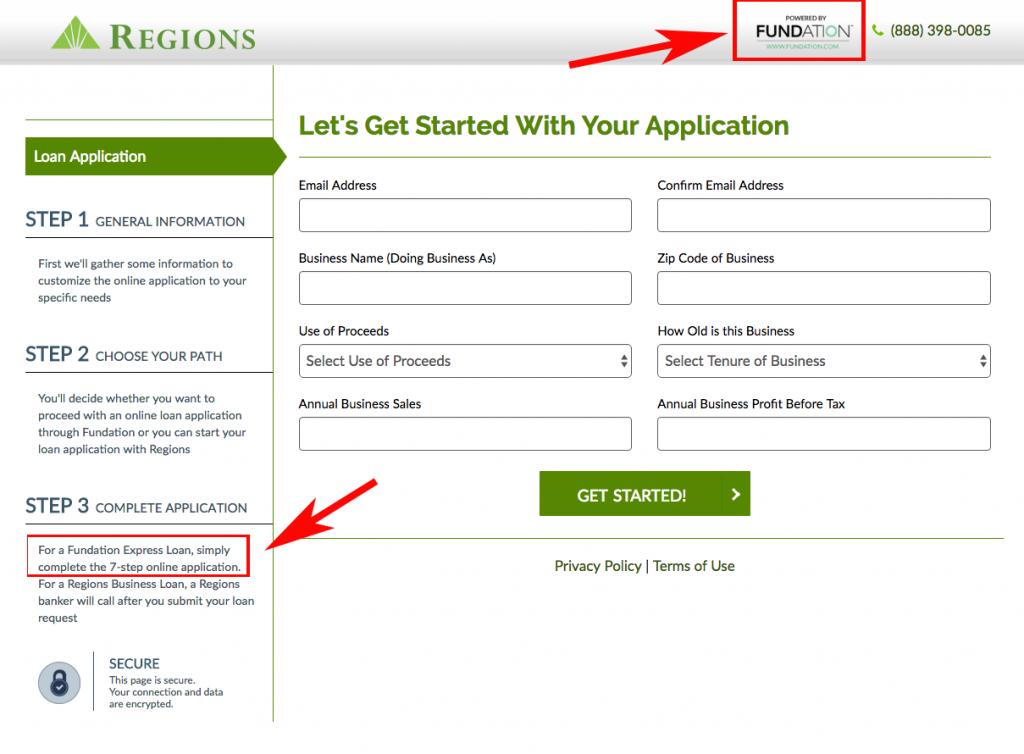

Fundation’s $100 Million Credit Facility From Goldman Sachs Is A Return To Banking

August 23, 2016 The online lending party isn’t over yet. And neither is bank lending…

The online lending party isn’t over yet. And neither is bank lending…

Fundation, which company CEO Sam Graziano described to the WSJ as a credit solutions provider rather than a lender, has secured a $100 million credit facility from Goldman Sachs. But they are a lender, a direct small business lender in fact, that uses their own balance sheet to make loans.

Fundation is different in that they bolt their platform on top of the traditional banking system. Their partnership with Regions Bank for example, allows Regions Bank customers to apply for a Fundation loan right through the Regions.com website.

The sizable credit facility, the system it will help foster, and the name behind it further demonstrates the demise of peer-to-peer lending. “We decided to be an integrated partner of the banking system,” said Fundation’s Graziano to the WSJ in regards to the saturated environment of lending platforms.

The WSJ also reported that the firm will use the funds to make more loans to Regions bank customers as well as other community banks that they have partnered up with.

Bizfi Originates $144 Million in Q2; CAN Capital, Entrepreneur Media Launch Funding Center

August 16, 2016 Online small business loan marketplace, Bizfi said that it originated over $144 million in Q2 this year, a 25 percent increase compared to $116 million in Q2 last year. The New York-based company has facilitated financing for more than 3,580 small businesses through its platform.

Online small business loan marketplace, Bizfi said that it originated over $144 million in Q2 this year, a 25 percent increase compared to $116 million in Q2 last year. The New York-based company has facilitated financing for more than 3,580 small businesses through its platform.

The company forged many partnerships to expand its customer base and access to small businesses. In March of this year, Bizfi announced a partnership with Western Independent Bankers (WIB), a trade association with community and regional banks across the Western United States and in July, it joined hands with the National Directory of Registered Tax Return Preparers & Professionals (PTIN).

Bizfi also secured a $20 million investment from New York-based investment manager Metropolitan Equity Partners in June this year, supplementing the $65 million infusion in December last year to expand and optimize its funding programs and develop an effective marketing campaign to advertise those better.

In other news, small business lender CAN Capital and Entrepreneur Media launched the funding center offering funding products that include term loans — available from $2,500 up to $150,000 for a single location with range of terms from 3 to 36 months. Trak loans which are working capital loans available from $2,500 up to $150,000 and installment Loans provide funding from $50,000 to $100,000 with 2, 3, and 4 year terms and have fixed monthly payments.

Square Capital Outgrows Square

August 11, 2016 You don’t need to process payments through Square anymore to get a loan from Square Capital. Restaurants that use Upserve, a restaurant payments and data analytics system, are now eligible as well.

You don’t need to process payments through Square anymore to get a loan from Square Capital. Restaurants that use Upserve, a restaurant payments and data analytics system, are now eligible as well.

Formerly known as Swipely, Upserve is still relatively small, with only 7,000 restaurants as customers. But it’s a milestone for Square nonetheless, whose loan program within their own ecosystem has become so successful, that they feel comfortable venturing outside of it.

“We are proud to partner with Upserve and offer loans through Square Capital to even more small businesses who traditionally face barriers when seeking access to funds,” said Jacqueline Reses, Head of Square Capital.

The move puts them on a path to truly competing with other alternative lenders such as OnDeck and CAN Capital. Loans are repaid just like they are through Square, through a percentage of each day’s card sales with the option to repay early at no additional fee.

Calling Timeout On Financial Regulations, A Pump For Trump?

August 10, 2016

Only 24% of small business owners say that Hillary Clinton is the presidential candidate that has their best interest at heart, according to a survey conducted by Capify, a business financing company based in New York. 53% selected Donald Trump.

And whatever your opinions about Trump, his proposed moratorium on new financial regulations could entice both small businesses and alternative financial companies to consider a Trump presidency.

“Under my plan, no American company will pay more than 15% of their business income in taxes,” Trump said in Detroit on August 8th.

A report published by the National Federation of Independent Business (NFIB) last month found that 20% of business owners ranked taxes as the single most important problem facing their business. Only 2% reported that financing was their top business problem.

Message received? It appears not

In states like Illinois, some legislators are focusing their efforts on finding ways to make it harder for small businesses to obtain financing, convinced that questionable lending practices are the source of their problems, not taxes. But in a call with Bryan Schneider, secretary of the Illinois Department of Financial and Professional Regulation, he told deBanked that no one has complained of any small-business lending problems in Illinois to state regulators.

Regulators should not indulge in creating solutions in search of problems, Sec. Schneider cautioned. “When you’re a hammer, the world looks like a nail,” he said, suggesting that regulators sometimes base their actions on anecdotal isolated incidents instead of reserving action to correct widespread problems.

And that’s why a moratorium on financial regulations (albeit on the federal level) might also resonate with small businesses. Lawmakers don’t appear to be addressing their grievances and ironically, passing new laws that make it harder to obtain financing could potentially even exacerbate the problems they’re already vocalizing.

Small businesses seemed to have become aware of the government-as-obstructionist role however since 22% of them surveyed in the NFIB study, said that government requirements and red tape were the single most important problem they faced, more than anything else.

The Finance Side

A timeout is not a sure-fire way to woo Wall Street however, since a moratorium on federal regulations could actually serve as a hindrance for some financial companies hoping to reach some legal framework consensus down the road. Last year, Bizfi founder Stephen Sheinbaum, said that a 50-state patchwork of laws would make operating companies like his more challenging. “Personally, I’d be glad to see it on the federal level, we won’t have to deal with 50 individual states, which is more unruly,” Sheinbaum said in regards to potential regulation.

But a timeout on making any moves might indeed be in order anyway, given the questions that are being asked by some federal legislators. Last month during a hearing, Rep. David Scott asked what made business loans different from consumer loans. Parris Sanz, the Chief Legal Officer of CAN Capital, who was there testifying on behalf of the Electronic Transactions Association (ETA), gave his answer.

But there is a fear, just by those questions, that some legislators are still having trouble understanding the fundamentals. And that may be why a dozen trade associations and lobbying groups have formed in the last year to provide educational resources about alternative financing.

In states like Illinois, Scott Talbott, SVP of government affairs for the ETA, said they are encouraging legislators to adopt a “go-slow approach” that affords enough time to understand how the industry operates and what proposed laws or regulations would do to change that.

Keep it Simple?

With Trump, despite all his quirks, it’s possible that his ideas about a moratorium, could be a deciding factor in how small business owners and those employed by alternative financial companies vote. Lower taxes, timeout on regulations, has the potential to resonate far and wide.

60% of small business owners think that the outcome of the presidential election will have a severe impact on small businesses, according to the Capify survey. 29% said it possibly will have a severe impact. With taxes and government red tape at the top of their list of grievances, there might just be a pump for trump on both sides of the alternative finance aisle.

OnDeck is NOT a Marketplace Lender

August 9, 2016

It’s finally time to stop calling OnDeck a marketplace lender.

The company only sold 15.6% of its originated loans through the OnDeck Marketplace, according to their Q2 earnings report. That’s down from 26% in the prior quarter. It’s not hard to see why that might be as the Gain on Sale Rate was only 3.5% in Q2, a significant drop from the 5.7% in Q1 and 7.8% at this time last year.

On the earnings call, OnDeck’s chief officers argued that demand for their loans remained very high but that investors are requiring more return for the same risk. With the profit incentive to sell loans severely diminished, the company plans to continue selling only 15% – 25% of their loans going forward on the basis of keeping institutional relationships and diversification.

But if not a marketplace? Then?

OnDeck is a non-bank commercial balance sheet lender. And as a result, the company’s cash dropped from $160 million on December 31, 2015 to only $78 million at the end of Q2. OnDeck CFO Howard Katzenberg said that this wasn’t a burn, but rather cash being invested into their loans, all part of their plan of moving away from the marketplace. The company still has $300 million in GAAP equity, $100 million available to it from its warehouse lenders, and other debt facilities that it plans to increase for more leverage.

OnDeck funded a whopping $590 million in loans in Q2 but posted a net loss of $17.9 million. Origination figures include the full loan principal amount on renewals even though part of the principal may be used to pay off an existing loan.

Marketing costs remained relatively stable as did loan performance. Little was said about their relationship with JPMorgan Chase other than the fact that it’s still “early days at this point.”

Have You “deBanked” Yet?

August 5, 2016If you’re not already subscribed, you can make sure that you receive the July/August 2016 edition in print by subscribing here.

Among the featured stories and content are:

- The role of MCA/business-loan brokers around the world contrasted with the U.S.

- The continued growth of alternative commercial finance

- How to grow an MCA or business loan brokerage

- Uber’s new finance program

- And much more!

Are you involved in funding businesses outside the bank? It sounds like you’ve de-banked! We hope you enjoy this issue. The digital version will be online later this month.

Square Capital Revs Up, Funds $189M to Small Biz in Q2

August 4, 2016

Square is proving that the business loan sector is still hot, especially since their payment processing ecosystem requires nearly no marketing budget to advertise Square Capital. With $189 million funded in Q2, a growth of 123% year-over-year, their shift from merchant cash advances to loans seems to have had the desired effect since they have attracted even more investors willing to buy them.

“We sell a majority of our loans to third-party investors for an upfront fee and a small ongoing servicing fee. In addition, we continue to have a strong continued pipeline of interested investors,” the company said in its earnings report.

The average loan size remains small, only $6,000, but ranges from $1,000 to $100,000. Square CFO Sarah Friar, said during the earnings call that their data shows an overall increase in the gross payment volume of merchants who use their loans, which indicates that borrowers are indeed using the funds to grow their businesses.

A typical Square Capital loan is close to 10% of a seller’s annual processing sales and the average repayment term is 9 months. Loss rates remained steady at 4%.

Friar also said that PayPal Working Capital and American Express Working Capital were not really competition since they are working directly with their own existing user base.

The company made about 34,000 loans in Q2.