Business Lending

Are You a Loan Broker? You Need to Be Licensed in Vermont

May 12, 2017 Loan broker licensing may have gotten stalled in New York, but in Vermont, it’s the law. Governor Phil Scott made H. 182 official on May 4th, regulating everyone engaged in loan solicitation with prospective Vermont borrowers. Specifically this applies to anyone that:

Loan broker licensing may have gotten stalled in New York, but in Vermont, it’s the law. Governor Phil Scott made H. 182 official on May 4th, regulating everyone engaged in loan solicitation with prospective Vermont borrowers. Specifically this applies to anyone that:

- offers, solicits, brokers, directly or indirectly arranges, places, or finds a loan for a prospective Vermont borrower;

- engages in any activity intended to assist a prospective Vermont borrower in obtaining a loan, including lead generation;

- arranges, in whole or in part, a loan through a third party, regardless of whether approval, acceptance, or ratification by the third party is necessary to create a legal obligation for the third party, through any method, including mail, telephone, Internet, or any electronic means;

- or advertises or causes to be advertised in Vermont a loan or any of the services described in (i) –(iii). This license does not include the authority to engage in the business of making loans.

The loan solicitation law is separate from a Commercial Lender License, which already requires licensing to solicit business loans under $1 million, as it covers:

- Any company or person who engages solely in the business of making commercial loans of money, credit, goods, or things in action and charges, contracts for or receives on any such loan interest, a finance charge, discount, or consideration therefore. Commercial loans do not include a loan or extension of credit secured in whole or in part by an owner occupied one-to-four unit dwelling. [Note: The company’s main office must be licensed as a commercial lender prior to, or simultaneously with, the filing of a branch commercial lender license.]

- Each location, whether located in Vermont or not, desiring to engage in the business of making commercial loans in Vermont must obtain a separate license by filing a Form MU3 through the NMLS.

- A commercial loan solicited or made by mail, telephone or electronic means to a Vermont business is subject to licensing notwithstanding where the loan is legally made. No person may engage in the business of soliciting or making commercial loans by mail, telephone or electronic means in Vermont unless duly licensed.

Brokers and lead generators should take a good hard look at their marketing since it may not matter if the customer ultimately is referred to a non-lender such as an equipment lessor or a merchant cash advance company if loans are even an option among many.

According to the law, each loan solicitation licensee shall include clearly and conspicuously in all advertisements of loans and solicitations of leads, the following statement:

“THIS IS A LOAN SOLICITATION ONLY. [INSERT LICENSEE NAME] IS NOT THE LENDER. INFORMATION RECEIVED WILL BE SHARED WITH ONE OR MORE THIRD PARTIES IN CONNECTION WITH YOUR LOAN INQUIRY. THE LENDER MAY NOT BE SUBJECT TO ALL VERMONT LENDING LAWS. THE LENDER MAY BE SUBJECT TO FEDERAL LENDING LAWS.”

A loan solicitation license cost $1,100.00 (includes a $500.00 Licensing Fee, a $500.00 Investigation Fee; and the $100 NMLS processing fee), according to the government website.

If you’re sending mailers to Vermont businesses, calling them or even marketing to them on the Internet, you should speak with an attorney about both the loan solicitation license and commercial lenders license first.

Kabbage’s Next Growth Phase

May 9, 2017 Victoria Treyger, Chief Revenue Officer, Kabbage

Victoria Treyger, Chief Revenue Officer, KabbageWhen you consider the recent milestones Kabbage has achieved it makes it difficult to think of the fintech lender as a startup. In recent weeks Kabbage surpassed a couple of major milestones comprised of extending $3 billion in funding to 100,000-plus small businesses. More than half of those loans were directed toward existing credit lines. Kabbage also recently priced a $525 million private securitization, which tips the company’s hand on strategy.

After barely letting the paint dry on those achievements, Kabbage already has the next phase of growth in its sights. Victoria Treyger, Kabbage’s chief revenue officer, took some time to discuss those details with deBanked, ranging from serving larger businesses with bigger loans, to expanding its partnerships to providing more niche-based features to customers.

Kabbage is pursuing its growth plans all while performing a confidential search for a new chief technology officer, details for which are expected to unfold in the coming months.

Personal Touch

As chief revenue officer, Treyger oversees the customer experience across both sales and marketing. She describes the Kabbage experience as a cross between a loan and a credit card.

“Ours is a living, breathing product that automatically adjusts for the needs of a business. Once you apply with Kabbage and link your data sources, you never have to do anything again,” said Treyger, pointing to the example of an ad agency. “If you’re an ad agency your highest cash needs are January through March. That’s when the agency’s customers invest their marketing budgets. So the Kabbage credit line automatically adjusts your credit line during your busiest time.”

And while most customers already take out multiple loans per year, with some accessing as many as 10-20, Kabbage is looking to streamline the customer experience even more. “The next stage of Kabbage is about personalization,” said Treyger, pointing to its automated underwriting platform that is connected to over a million live data points about business’ performance and allows the company to understand the cash flow needs of customers across industries.

Kabbage’s sales and customer service teams are also staffed with team members possessing industry vertical expertise ranging from e-commerce to construction.

Partnership Pipeline

At the LendIt USA 2017 event, Kabbage co-founder & CEO Rob Frohwein alluded to the online lender’s plans to reach new territories, details for which were scarce. Treyger shared, however, that Kabbage’s global growth plans are somewhat tied to the company’s pipeline of banking partnerships.

“They are all very large, global banks. I can’t say who they are but there are over half a dozen large relationships that are in the works,” said Treyger, adding that details surrounding those new partnerships will unfold over the next year.

“It’s not that banks don’t want to serve smaller small businesses. But with manual processes they often don’t have the capacity to serve these customers. Kabbage’s automated platform allows them to automate these manual processes and therefore serve more businesses of every size,” said Treyger.

Kabbage already counts as partners household names including Santander, ScotiaBank, and ING, all of which license software from Kabbage. Meanwhile, as big banks are accessing smaller businesses, Kabbage’s growth blueprint includes serving larger ones.

For instance, Kabbage is drawing on its recent $525 million securitization to fund small business loans. The credit facility is larger than previous deals, and for a good reason.

“One reason it is larger is that it was designed to support Kabbage in expanding our product offering to serve larger small businesses, which means two things — larger credit lines of $150,000 to $200,000 and eventually higher; and also longer-term products, not just six-to-12-months but 24, 36 months and different terms. The new larger facilities allows us to expand to serve even more small businesses across all size and funding needs,” said Treyger.

Early Innings

Meanwhile in terms of the small business community’s awareness of fintech and tech-based lenders, Treyger believes the industry is in the early innings. “That’s a great thing. There is a tremendous growth opportunity for the company,” she said.

OnDeck On the Path to Profitability?

May 8, 2017 In their earnings announcement this morning, OnDeck predicted that GAAP profitability would be achieved in the second half of 2017. For now, the GAAP net loss in Q1 was only $11.1 million, down from $36.5 million in Q4. The company originated $573 million worth of loans for the quarter.

In their earnings announcement this morning, OnDeck predicted that GAAP profitability would be achieved in the second half of 2017. For now, the GAAP net loss in Q1 was only $11.1 million, down from $36.5 million in Q4. The company originated $573 million worth of loans for the quarter.

OnDeck has been under pressure from at least one major shareholder to make changes. “We’re talking about a stock that is down 75 percent to 80 percent from its IPO price. You’re not going to find a lot of happy campers in that situation. Shareholders are going to ask tough questions,” Mario Cibelli, Marathon Partners managing member, told deBanked last month.

OnDeck has been underperforming just about all of its peers year-to-date according to the deBanked Tracker. The company’s stock price has been flat on the year, whereas Square, which does payments in addition to business loans, is up 45%.

The Marketplace, once a defining part of the tech-based lender’s strategy, is being almost completely phased out. “Loans sold or designated as held for sale through OnDeck Marketplace represented 9.0% of term loan originations in the first quarter of 2017 compared to 25.9% of term loan originations in the comparable prior year period,” their report said. OnDeck plans to reduce the amount of loans sold through their marketplace to less than 5% for the remainder of 2017.

“The Provision Rate in the first quarter of 2017 was 8.7% compared to 5.8% in the prior year period.”

“The 15+ Day Delinquency Ratio increased to 7.8% in the first quarter of 2017 from 5.7% in the prior year period and from 6.6% in the fourth quarter of 2016 due primarily to the continued seasoning of the portfolio.”

“The Cost of Funds Rate during the first quarter of 2017 increased to 5.9% from 5.5% in the prior year period primarily due to the increase in short-term rates.”

“The Net Charge-off rate increased to 14.9% in the first quarter of 2017 from 11.2% in the prior year period and increased sequentially from 14.2%.”

“Combined with the company’s prior workforce reduction, total headcount at the end of the second quarter of 2017 is expected to be approximately 27% lower than December 31, 2016 levels, due to both involuntary terminations and actual and scheduled attrition.”

Two Small Biz Owners Talk Online Borrowing

May 5, 2017 Katie Basson, President of Birch Tree Promotions

Katie Basson, President of Birch Tree PromotionsDuring National Small Business Week, we wanted to see what we can glean from a couple of small business owners who have taken to the Internet for their capital needs. Entrepreneurs Katie Basson of Birch Tree Promotions and Asha Waterstreet of Tasteful Additions document their experience as first-time online borrowers, and here’s a hint: Both of them would do it again.

And while their stories are unique, there are some parallels in Basson’s and Waterstreet’s online borrowing experience starting with the fact that both women got their capital needs met through SmartBiz Loans. Both raved about customer service. And for both, marketing and the media played a key role in their decision process.

Where their stories diverge, however, is in their response to the amount of financial products targeting women-owned small businesses. While Waterstreet does not give much thought to demo-tailored loans, Basson’s experience is that the number of programs geared toward women small business owners is lacking. This despite the fact that the United States is home to more than 11 million women-owned small businesses who employ millions and produce $1.6 trillion-plus in combined revenue.

Meanwhile SmartBiz Loans seems to buck the banking trend when it comes to extending capital to entrepreneurs like Basson and Waterstreet. “One third of loans [we process] are to women-owned businesses, which is higher than the average for traditional bank loans to small businesses,” Evan Singer, CEO of SmartBiz Loans, told deBanked.

Katie’s Story

Birch Tree Promotions, whose name was inspired by a trip to Basson’s grandparents New England cottage where the moon-lit birch trees shined, was founded in 2006. The Newburyport, Mass.-based business, whose annual revenue hovers at about $1 million, specializes in selling premium promotional items. Similar to the birch tree at that vacation cottage, Basson seeks to make her brand stand out from the rest.

“It’s amazing to do this kind of volume for such a small place. I attribute that to technology, which is why I completely appreciate a company like SmartBiz that leverages that technology to be efficient,” said Basson, who counts among her clients Bain Capital, Philips and Amazon Robotics.

Her need for capital arose with a growth spurt during which time she hired a number of part-time employees.

“Up until [using SmartBiz Loans] we were sort of going along using lines of credit from local banks. I expressed my desire to have a long-term solution help with cash flow so it’s not boom and bust all the time. Instead there would be a significant amount of capital to use for managing the cash flow of the business where making payments each month made sense. None of them were interested. Somehow I didn’t fit their traditional model,” she explained.

The roots of Birch Tree Promotions reside in Basson’s quest to achieve a work/life balance, throughout which she observed financing needs for women-owned home-based business being overlooked.

“There was nothing I could see out there that was targeted to me. I didn’t have a storefront; I’m working out of my home office. That made it seem suspect to them. I wasn’t serious if I didn’t own office space,” she noted.

But Basson, whose business is run 100 percent online, would not take no for an answer. “If I could pay a $20,000 line of credit, why wouldn’t they view me as a viable credit risk?” she quipped. So Basson set out on a journey to find a lender that was more open minded. She read about SmartBiz loans in an article published by a major financial publication, and then it was off to the races.

But Basson, whose business is run 100 percent online, would not take no for an answer. “If I could pay a $20,000 line of credit, why wouldn’t they view me as a viable credit risk?” she quipped. So Basson set out on a journey to find a lender that was more open minded. She read about SmartBiz loans in an article published by a major financial publication, and then it was off to the races.

“I was amazed at how easy it was and how quickly everybody responded to me,” said Basson, adding that she even received a call on a Friday night from a SmartBiz representative to let her know where her loan stood and so that she wouldn’t have to worry over the weekend.

SmartBiz Loans matched her up with First Home Bank in Florida for an SBA-backed loan. Basson borrowed $200,000 over a 10-year term and her monthly payment is $2,274. The loan process took four weeks.

“Managing cash flow was the biggest, most important piece in addition to having funds available should I need them for big orders. We need some resources if we’ve just landed a huge order. We pay for the goods and then wait to get paid by the big company, and we needed more financial flexibility for that,” said Basson.

Perhaps the greatest testament to her online borrowing experience resides in whether or not she would return to the online lender for her capital needs in the future. The answer? “Indeed” she would.

Asha’s Story

Waterstreet launched Tasteful Additions about six years ago in Rochester, New York. The inspiration for her business came from a family vacation to North Carolina where she and her daughter visited a tasting store featuring flavored olive oils and balsamic vinegars. Ten bottles later coupled with frequent requests from her 12-year old for salads at dinner, Waterstreet knew there was something there.

So she opened up her own tasting store featuring flavored olive oils, balsamic vinegars and gourmet salts. And while in recent weeks she brought her small business entirely online doing away with the brick-and-mortar location, Waterstreet came across a need for capital about three years ago.

“I wanted to expand some of my products, and that was primarily the reason I decided to apply for a loan to get more capital. Credit cards were too high interest and I didn’t want to do that,” she said, adding that she initially went to her local banks only to be met with a process that she described as “tedious.”

In fact, after inquiring with a traditional bank for a loan, she was later greeted by her local banker with a pile of paperwork that she immediately rebuffed. “Being a small business and with me running things I didn’t have time, honestly. I’m trying to open the store, run the business and meet with customers, and I was like, ‘forget it,’” she said.

Instead she opted opting to complete an online application, a process she described as “simple.”

“They took care of everything. And when they had questions, they called me. It was so easy. Whenever you think something’s too easy you wonder, ‘What’s the catch?’ I was shocked there really wasn’t a catch,” said Waterstreet reflecting back.

It was while reading a food trade magazine that Waterstreet came across and ad for SmartBiz Loans. The rest is history. “I read about what they do. I called and the process was so easy and quick. And I got a very good interest rate as well. I was not getting raked over the coals or anything like that,” she said.

Waterstreet would not discuss the details surrounding her SBA loan but suffice to say that if she were to find the need to access more capital in the future, she would likely go to SmartBiz first.

Neither Basson nor Waterstreet considered any other online-lenders.

Square Lent $251 Million to Small Businesses in Q1

May 4, 2017It was another big quarter for Square Capital, who originated more than 40,000 business loans for a total of $251 million. That’s an increase of 64% year-over-year but only up 1.2% from the previous quarter. The company had $51 million in loans held for sale on their balance sheet as of March 31st.

Overall, Square, Inc. had a net loss of $15 million for the quarter compared to a $96.7 million loss over the same period last year. Investors took the news in stride, pushing the stock price up from under $18.50 to temporarily over $20.

Of notable interest in the fine print of their 10-Q, is acknowledgement that there have been and could be challenges to the chartered bank model on which they rely to make their loans, to the point where they say it’s possible they could one day have to revert back to the merchant cash advance model.

We have partnered with a Utah-chartered, member FDIC industrial bank to originate the loans. There has been, and may continue to be, regulatory interest in and/or litigation challenging partnered lending arrangements where a bank makes loans and then sells and assigns such loans to a non-bank entity that is engaged in assisting with the origination and servicing of the loan. If our bank partner ceases to partner with us, ceases to abide by the terms of our agreement with them, or cannot partner with us on commercially reasonable terms, and we are not able to find suitable alternatives and/or obtain licenses to make loans ourselves, Square Capital may need to enter into a new partnership with another qualified financial institution, revert to the merchant cash advance (MCA) model, or pursue an alternative model for originating loans, all of which may be time-consuming and costly and/or lead to a loss of institutional third party investors willing to purchase such loans or MCAs, and as a result Square Capital may be materially and adversely affected.

Square originally relied on the merchant cash advance model but switched to making loans after they found it challenging to package them up and sell them to investors.

Alternative Lending Is Dead

April 30, 2017At LendIt, Kabbage co-founder & CEO Rob Frohwein, blew the roof off the house with his presentation. Titled, “Alternative lending is dead, long live data,” he explained what he believes the industry should really be about.

On why the term alternative lending doesn’t make sense:

Think about Uber, when they talk about their business. Their tagline is ‘when you don’t feel like taking a taxi.’ They don’t call it alternative transportation at its best

On how most companies have been answering the wrong question:

The question answered by most online lenders is, ‘can you fill the void left by banks?’ I will tell you right now that the question that should’ve been answered by folks going into online lending would be ‘why aren’t banks filling this void?’ When you ask a different question, you get a different answer.

I’m not trying to prove that small businesses need capital. That is blatantly obvious. I’m trying to prove that there is a better way to do it.

Most online lenders tried to disrupt banks by proving they could grow fast and they could acquire capital, but there is only one problem with that approach. You don’t disrupt banks by focusing on the advantage that banks have over you. Banks have customers and money. That is mostly what they have. They have customers and money. So why disrupt the space with the two items that they actually have? The question that should’ve been asked and answered is, ‘why aren’t banks filling this void?’

The answer to that is, because they can’t profitably, for our industry, they can’t profitably serve small business customers. When you ask that question and you figure out the reason, you start building your business a little bit different

On why an online application doesn’t make you a technology company:

Most online lenders thought that by calling themselves a technology company, that they were one, but that wasn’t the case. The biggest piece of technology that most of them promote, is an online application. That’s it. If you think about it, it’s an online application. Everything else is manual. There is nothing, nothing special about an online application.

And outside the US, we’ve already launched in Australia, Spain, the UK, Canada and Mexico. And we’re going to be announcing two other territories in the next several weeks. And by the way, we have no employees in those markets, because we’re able to operate everything remotely because we’re a technology company.

If your business is scaling really fast, and your opex (operating expense) is doing anything but going down, you’re not operating a technology company. Everyone else is flat or up on opex, but we can continue to go down. If you’re running a technology company, you don’t have to lay people off at the slightest hint of trouble and do you know why? Because you don’t have too many employees. Your business scales. Right?

What IOU Financial Revealed in its Earnings Statement

April 29, 20172016 was a weird year for online lenders and IOU Financial, who lends to small businesses, fared no differently. Loan origination volume for the year was $107.5 million, down 26.5% from 2015. Revenues were up due to the company retaining more of their loans on balance sheet but losses were up as well.

Here are the most interesting statistics we found:

- 93% of their loan volume came from brokers

- 15% of merchants in their portfolio were classified as specialty trade contractors and home building renovation

- 14% of merchants in their portfolio are based in Florida (more than New York and New Jersey combined)

- Their borrowers have been in business for an average of 11.4 years

- Their average loan size is $69,695

- Their average loan term is 12 months

- They sold $60.8 million of loan receivables in 2016, down from $137.3 million in 2015

- The company has loaned $415 million to small businesses since inception

- The company had 53 full-time employees at year-end

IOU Financial is the only lender that deBanked is tracking whose stock is down year-to-date. At close on Friday, company shares were down more than 28% for the year.

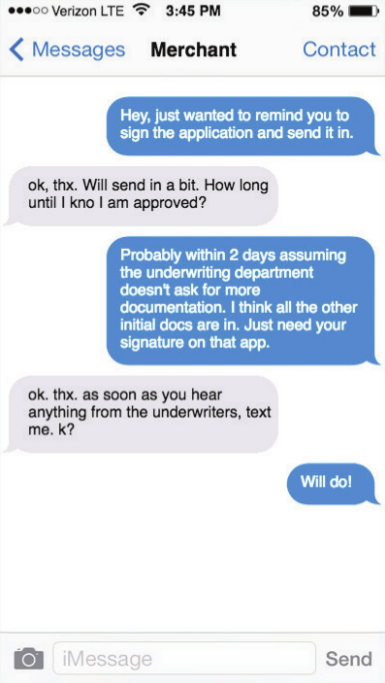

Text The Merchant, Close The Deal

April 15, 2017

About a year ago, Cheryl Tibbs, general manager of Douglasville, Ga.-based One Stop Funding, was having trouble getting in touch with one of her clients. The merchant in question runs a lawn care service and is usually out on the job, so he isn’t quick to return phone calls or respond to email messages.

“I just got the idea to send a text,” Tibbs recalls. She typed a message expressing her regret for intruding but letting her client know that he needed to take certain steps to advance the funding process for his loan application. He texted right back.

After that initial success, the texting continued between Tibbs and the lawn care provider. He’s been a customer for us for a while, and that’s just how we communicate,” she says. “It’s easy for him to stop and shoot me a text as opposed to having a full conversation with me.”

Tibbs isn’t alone in her appreciation for text messaging as a part of the sales process. Quick responses to texts are making the medium increasingly important in the alternative small-business funding business, maintains Gil Zapata, CEO of Miami-based Lendinero. “Text messaging is more powerful than emailing nowadays,” he declares.

One reason for that shift is that texts are easy to use, according to Tibbs. “It’s a matter of convenience for the merchant,” she contends. “In this business, any way you can make it easier for the merchant to facilitate the transaction with you is the method you have to use.”

Besides the convenience, there’s the sense of urgency people feel when they receive a text, asserts Jeb Blount, a sales trainer who’s written eight sales-oriented books, including the bestselling Fanatical Prospecting. “When you send a text message you move to the top of a person’s priority list,” he says. In fact, people who are talking face-to-face often disengage from the conversation to respond to a text message, he notes. “It’s treated as something that’s urgent.”

As texting becomes more commonplace in the alternative-finance business, some industry salespeople are beginning to view the medium in the same way they regard email, telephones and fax machines. “I use them as another tool for follow-up communications,” John Tucker, managing member of 1st Capital Loans in Troy, Mich., says of text messages. “In addition to sending them an email, I’ll shoot them a text.”

As texting becomes more commonplace in the alternative-finance business, some industry salespeople are beginning to view the medium in the same way they regard email, telephones and fax machines. “I use them as another tool for follow-up communications,” John Tucker, managing member of 1st Capital Loans in Troy, Mich., says of text messages. “In addition to sending them an email, I’ll shoot them a text.”

Texting has become almost standard procedure at Florida-based Financial Advantage Group LLC, according to Scott Williams, the firm’s managing member. He prefers that sales associates make the initial contact by phone to get a sense of what the merchant is looking for in a funding deal. After gathering information and getting approval, it’s best to send the offer by email so the merchant has “all the numbers in black and white” and more details than a text message can hold, he notes. After that, text messages can deliver requests for additional documentation and provide updates on the progress of the funding process. “We can tell them, ‘Hey, everything got cleared this morning – we should be able to do the funding this afternoon,’” he says.

Texting expedites communication regarding renewals, too, Williams observes. “If a merchant is 50 percent paid back, you can check in and see if they need some additional capital right now,” he says. “It’s really good for that.”

Clients can use messaging to convey images of documents needed in the funding process, Tibbs says. “I had a merchant yesterday who sent me over her IRS tax agreement through picture message,” Tibbs says by way of example. Often, funders request color images of both sides of an applicant’s driver’s license, she notes. To fulfill such requirements, it’s generally easier to snap a photo with a phone and send it as a picture message than to scan pages of paper into a computer to create an electronic document and then send the resulting file by email. “We do a lot with picture messaging,” she observes.

But as useful as text messaging can become for contacting phone-shy clients or helping clients share an image to document a key cancelled check, companies should exercise care when using the medium for prospecting, warns Zapata. He and just about everyone else deBanked consulted emphasizes that sending unsolicited text messages can violate Federal Trade Commission regulations. “Just because our industry isn’t regulated doesn’t mean there aren’t regulations out there on the side,” he says.

Most say they learned of the regulations from third-party vendors who specialize in sending batches of text messages simultaneously. The key to sending those groups of messages legally is to get permission from the recipients in advance, notes Ted Guggenheim, CEO of TextUs, a Boulder, Colo., company specializing in multiple-texting services. “If you’re (randomly) contacting people you got off a list somewhere, that’s a pretty bad idea,” he maintains.

Most say they learned of the regulations from third-party vendors who specialize in sending batches of text messages simultaneously. The key to sending those groups of messages legally is to get permission from the recipients in advance, notes Ted Guggenheim, CEO of TextUs, a Boulder, Colo., company specializing in multiple-texting services. “If you’re (randomly) contacting people you got off a list somewhere, that’s a pretty bad idea,” he maintains.

The feds heavily regulate five-digit short-code texts but tread lightly with long-code texts – the ones sent from 10-digit phone numbers, Guggenheim says. The latter would apply in alternative finance, and if a text recipient calls back on the phone number associated with a long-code text, someone will answer, he notes.

Citing guidelines from the Cellular Telecommunications Industry Association (CTIA), Guggenheim stipulates that consumers should have the ability to opt out of additional messages after receiving the first one. Members of the industry who want to send groups of text messages can post conditions on their websites that compel users to grant permission to contact them by text if they submit their contact information, he suggests.

After ensuring everything’s legal, Tucker reports 1st Capital Loans nets a good response when he uses a vendor to blast multiple identical text messages to lists of prospective clients who have already granted permission for his company to contact them by text message. The strategy has helped bring in a reasonable number of deals because the prospects were “already in the pipeline,” he notes.

Remember, though, that cell phone numbers change more often than land line numbers, Tucker cautions. That means a call to a number that’s been reassigned could inadvertently fall into the unsolicited text message category that violates federal rules, he says. “You could be texting a 14-year-old,” instead of a small business, he warns.

When mounting a mass text campaign, marketers are wise to avoid lengthy missives, according to Tibbs. “Keep it simple,” she says. A typical message from her might read: “Looking for funding? Looking for capital? Give us a call,” she notes.

In business texts, avoid acronyms like “LOL” and write in complete sentences with proper punctuation and capitalization, Blount suggests. “Begin by typing out the message somewhere other than in the text box, read it, make sure it makes sense and then send it,” he says. Put your name with the word “from” at the top of the message so the recipient knows who sent it, he emphasizes.

Keep messages conceptual rather than marketing-oriented, Guggenheim advises. Messages should directly address the customer’s situation to avoid seeming they were sent by a robot, he says. As with any response a salesperson receives, getting back to customers quickly pays off in better results, he adds. When sending a batch of texts, vendors of the bulk service can ensure every text bears the same phone number that the sales rep uses to call the client, thus avoiding the possible confusion of using more than one number, says Guggenheim. The system he offers can trigger a pop-up on the computer screen of a specified salesperson when a text recipient responds, he says. It also keeps management informed of the volume of texts and the response rate, he says. That helps managers determine which types of text messages are working, he maintains.

Keep messages conceptual rather than marketing-oriented, Guggenheim advises. Messages should directly address the customer’s situation to avoid seeming they were sent by a robot, he says. As with any response a salesperson receives, getting back to customers quickly pays off in better results, he adds. When sending a batch of texts, vendors of the bulk service can ensure every text bears the same phone number that the sales rep uses to call the client, thus avoiding the possible confusion of using more than one number, says Guggenheim. The system he offers can trigger a pop-up on the computer screen of a specified salesperson when a text recipient responds, he says. It also keeps management informed of the volume of texts and the response rate, he says. That helps managers determine which types of text messages are working, he maintains.

Users can also rely on Guggenheim’s TextUs system to schedule messages for delivery in the future to remind clients of meetings. The system detects land-line numbers and informs the user that the phone will not receive text messages, and it integrates with customer-relationship management systems to exchange information, he says.

So used properly, texting can offer benefits for everyone involved. But some unscrupulous players still insist upon using the medium to mislead prospective clients, says Zapata. His customers have shown him texts from competitors who make initial contact or early contact by sending text messages that might look like offers but are really just marketing letters, says Zapata. That approach, which might tout the availability of $50,000, can cause problems when it turns out that the merchant qualifies for only $25,000, he explains. “Trust me, you’re not going to look like the good guy,” he says of the firms that send what he considers objectionable text messages.

Sensitivity comes into play with text messaging, according to Blount. He and other sources say a great number of people regard email as business-oriented and texts as personal. That leads them to nonchalantly delete unwanted email messages but to become angry when they receive a text they didn’t want, he says. “You can’t send text messages to customers if they don’t know you,” he counsels.

Once a relationship is established, however, text messages can nurture it, Blount maintains. Suppose two businesspeople meet at a networking event and exchange business cards, he says. He advises noting the cell number on the card and sending a LinkedIn invitation immediately after meeting the potential client. Twelve hours later he would send a text message mentioning the encounter. If the salesperson can get the potential client to respond to a text message, that prospect is granting permission to receive texts, he says.

Once a relationship is established, however, text messages can nurture it, Blount maintains. Suppose two businesspeople meet at a networking event and exchange business cards, he says. He advises noting the cell number on the card and sending a LinkedIn invitation immediately after meeting the potential client. Twelve hours later he would send a text message mentioning the encounter. If the salesperson can get the potential client to respond to a text message, that prospect is granting permission to receive texts, he says.

Blount’s example seems to suggest the line between business and personal may be blurring when it comes to texting. People often check their email messages on phones these days – instead of on a laptop or desktop computer – which also minimizes the difference between texting and emailing, says Tibbs. “Everybody does everything with their phone these days,” she notes.

Communicating through a more personal channel such as texting has advantages, too, Williams contends. That’s because some merchants consider their financing to be personal and don’t want to broadcast the details to employees, he says. To protect their privacy, merchants often provide financial institutions with their cell phone number instead of their office number or toll-free line, he notes.

Meanwhile, the world continues to become more comfortable with texting. When Williams and his sales associates began messaging clients about four years ago, they found younger customers receptive and older ones reluctant, he remembers. In the intervening years, however, the 50 plus crowd has warmed to the medium, he observes.

An advantage that accrues with text messaging – compared with email – arises from the fact that spam filters and spam folders don’t seem to have a place in the world of texting. Several sources cite that as a big advantage with using texts. “If you send someone a text message, they’re going to see it,” notes Zapata.

Asked about a downside to the proper use of text messaging in business, most sources could not name one. However, Williams has discovered one area where the mode of communication comes up short. “I would not deliver bad news over text-messaging,” he advises. “If the merchant is upset or frustrated by the news, it would be better-handled in a phone call so you could explain the reason for the negative news. A text message leaves too many things unsaid.”