Business Lending

I Got Funded, OMG I’m a Merchant!

March 3, 2017 I’ve read the press releases, interviewed the executives, and written the summaries about the latest and greatest innovations in alternative finance. I’m the guy that’s supposed to know how everything in this industry works, but do I REALLY REALLY know? In the last decade, I’ve worn an underwriter hat, an MCA broker hat, a syndicator hat, a lead generator hat and a reporter hat just to name a few. This diverse array of experiences has surely influenced deBanked’s success. But even as we publish content about the funders, lenders and other Fintech players in the wider industry, deBanked is truly a small business first.

I’ve read the press releases, interviewed the executives, and written the summaries about the latest and greatest innovations in alternative finance. I’m the guy that’s supposed to know how everything in this industry works, but do I REALLY REALLY know? In the last decade, I’ve worn an underwriter hat, an MCA broker hat, a syndicator hat, a lead generator hat and a reporter hat just to name a few. This diverse array of experiences has surely influenced deBanked’s success. But even as we publish content about the funders, lenders and other Fintech players in the wider industry, deBanked is truly a small business first.

Independently owned, there are no investors in the company to turn to for assistance. And that’s not such a bad thing if you know at all what it can be like to have partners. At the end of last year, we did what hundreds of thousands of small businesses around the country have done, we got funded by a marketplace lender. Through that experience, I found myself wearing a brand new hat, one that says “merchant” on it.

On December 1st, my company received a deposit for $35,000. It was a loan from Square Capital and I didn’t pursue it for a story, but rather to facilitate cash flow at the busiest time of the year. I was moving into a larger office on the same floor of our building and the hustle and bustle of the pre-holiday craze was upon us. The circumstances may come off a bit cliché, simulated even, but there it was at the right time and the right place, an email telling me that my business had been “selected.” If you’ve ever wondered if that kind of marketing works, it must, because a half hour after reading through the materials, I made an educated decision and applied for a loan.

The higher-ups at Square Capital, those above the underwriting department, might have no idea that they even funded us (our legal name is different from our trademark publication name). And I haven’t reached out to them for comment because I didn’t want to turn this into a PR stunt or get them riled up about my account. But if you work at Square and you’re reading this now, you don’t need to hold your breath. Everything seemed to work just as the press releases, ads, and executives claim it does. Phew! That’s good for you, but it was also very good for me.

The most pleasant surprise was that our business got approved for the maximum amount advertised in their email. Here’s how it went down:

11/29/16

1:34 PM

Received email offering a business loan up to $35,000 to repay over 12 months

2:01 PM

Applied for $35,000, which consisted of logging into my Square account and tapping a button

8:02 PM

Got approved for $35,000

11/30/16

Square sent out the funds via ACH

12/1/16

Received full loan deposit in my business bank account

All in all, it couldn’t have been any simpler. The deposit was for the full $35,000. And try as you might to hate me for saying this, I never calculated what the APR is. Square explained the cost as a fixed fee, which for me was $3,160. That’s approximately 9% of the principal of which the whole loan and fee would be repaid in equal installments over the next 12 months. To those that work in the industry, I got a 12-month 1.09 deal.

All in all, it couldn’t have been any simpler. The deposit was for the full $35,000. And try as you might to hate me for saying this, I never calculated what the APR is. Square explained the cost as a fixed fee, which for me was $3,160. That’s approximately 9% of the principal of which the whole loan and fee would be repaid in equal installments over the next 12 months. To those that work in the industry, I got a 12-month 1.09 deal.

As a small business owner, I calculated whether or not it made sense to pay a set fee for $35,000 over that time period and determined it did. An APR would not have impacted my decision, nor would I really have found it helpful in determining the supposed true cost. The true cost is already there in black and white, the total dollars I agreed to pay.

Two things guided me, speed and economics. I wasn’t motivated to shop around to try and get the absolute best deal, just one that made economic sense with the least amount of work in the shortest amount of time. It sounds ironic to write that, especially as someone who has a bachelor’s in both Accounting and Finance but if you’re someone who works 7 days a week like I do, well maybe you’d understand my thought process. If I was applying for a million bucks, then yes, I’d shop and think on it pretty hard, but in my circumstances, a few thousand dollars in fees is relatively small stakes for the company. Besides, I was using the money proactively, as a positive tool.

I knew my patience for waiting was thin. For example, an experience with one of my banks earlier in the year had already left me rattled. I had asked to extend the limit of a business credit card and I was told that in order to do so, I’d have to visit the bank branch where I had originally signed up for the card (I don’t even live near that branch anymore) and that I would have to bring financial statements with me to present for review. By the way, this was for a limit increase to an amount that was much less than $35,000.

I learned that day that the rumors about (some) banks are true. They wanted me to visit a branch… and bring paperwork… for some kind of unspecified analysis… in 2016. Lo and behold I never showed up, and was more entrenched in my belief than ever before that the world needed to become de-banked and soon.

My business already processes cards through Square so I’ve got a track record with them. Applying didn’t place any inquiries on my personal credit report nor did anyone at Square ever call me to ask me any questions. I know that most of their competitors conduct what is commonly known as a “merchant interview” prior to full approval or funding, but they didn’t. It wouldn’t have bothered me if they did though since we have a good business and would be using the money for the right reasons.

My business already processes cards through Square so I’ve got a track record with them. Applying didn’t place any inquiries on my personal credit report nor did anyone at Square ever call me to ask me any questions. I know that most of their competitors conduct what is commonly known as a “merchant interview” prior to full approval or funding, but they didn’t. It wouldn’t have bothered me if they did though since we have a good business and would be using the money for the right reasons.

Alas, the entire process really all just came down to clicking a button online. I kept waiting for the catch, for them to let me down, to come up short of all the promises that the Fintech revolution has made about changing the world, but it never happened. A month later, Square withdrew their first payment from our account. Like I said earlier, I was satisfied with the entire process and it was a big help. Had I been given the option however, I might’ve opted to structure the arrangement differently and sold a portion of our future sales proceeds rather than simply borrow money. Allow me to explain.

It’s entirely possible that the next 12 months of business won’t pan out the way I project. If my sales drop, I still have to make the fixed monthly payment in accordance with my loan terms regardless. Not so when selling future sales since the delivery of those funds to the buyer is entirely tied to actual sales activity. A structure like this, what many consider a merchant cash advance, is actually what Square used to offer up until early 2016.

When the pace of sales slow down, delivery of the sales proceeds slows with it. When the pace of sales increases, so too does the delivery to the buyer. And if I went out of business, well then the buyer would get what they purchased, nothing.

Merchant cash advances are harder to bundle up and securitize though because there are no maturity dates nor is there even a guarantee the buyer will get what they purchased in full. They’re investments with loads of uncertainty built in for the buyer, and that’s probably why Square switched to loans and also probably why the cost of my loan was relatively inexpensive. They’ve minimized the uncertainties.

Nonetheless, the loan I ultimately got, is just fine. In the moment that I needed it, the process couldn’t have been any simpler or any faster. The banks have met their match. I got funded and loved it, now it’s your turn.

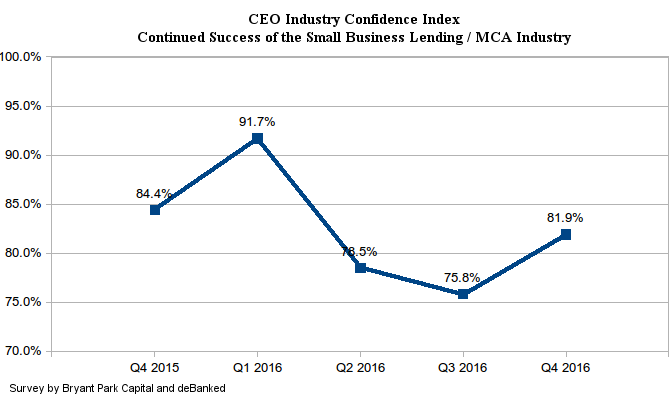

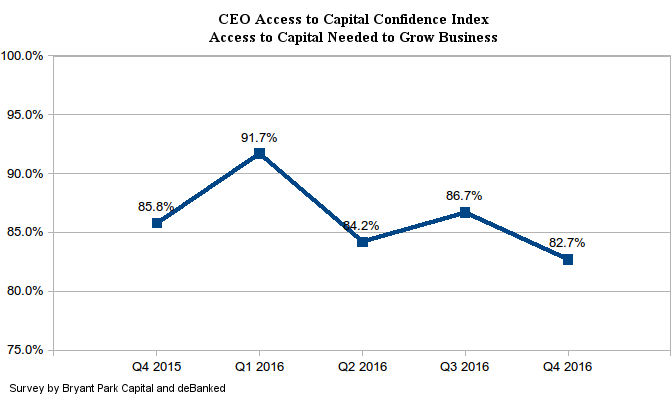

Confidence Stable For Small Business Lenders and MCA Companies

February 26, 2017Recent events may be putting a slight damper on the confidence of industry CEOs in being able to access capital needed to grow their businesses, but continued success of the industry in general is ticking back up. This data is according to the latest survey conducted by Bryant Park Capital and deBanked of small business lending and merchant cash advance company CEOs.

Confidence in the industry’s continued success bumped back up to 81.9% in Q4, while confidence in being able to access capital reached its lowest level since the survey’s inception. Still, at 82.7%, it’s high.

In late November of 2016, CAN Capital, one of the industry’s largest companies, encountered problems that caused the company to suspend funding. Several of their competitors since then have reported a boost in submission volume, which they partially attributed to that event.

Pressure on companies to merge or exit the market may also be kindling optimism for larger players who stand to gain market share.

The Road To Training The Best Sales Reps

February 26, 2017

Alternative-finance industry executives tend to agree on at least two basic rules for building a successful sales team: Hire people who know how to sell and never stop training them. Following the second rule requires knowledge and perseverance. The first one takes a leap of faith.

To obey Rule No. 1, companies have to find ways of determining who possesses that elusive quality known as salesmanship, even among inexperienced job candidates. To that end, most firms make an educated guess based on experience, intuition, common sense, high hopes and the good graces of Lady Luck.

“We look at personality traits,” says Zach Ramirez, a World Business Lenders vice president and manager of the company’s Costa Mesa, Calif., branch. “We’re looking for an outstanding person – the highest-caliber person we can find. They should be hard-working and competitive. You can underline ‘competitive.’ They should have a fire inside them.”

“We want someone who’s hungry for money and is going to be a go-getter, says Chad Otar, CEO and executive funding manager at Excel Capital Management Inc. “It’s a feeling that you get when you talk to them. You can tell when a person is going to sit back and not do anything.” In addition, good candidates aren’t intimidated by the challenge of learning how the industry works, he notes.

“It’s really about how you connect with someone,” according to Amanda Kingsley, who owns Options Capital and also works as a sales training consultant. “Even over the phone, you need to treat people with understanding. You need to inspire the trust that you could provide the advisory help they need.” Small details, like remembering a potential client’s daughter just got married, mean a lot, she says.

“It’s really about how you connect with someone,” according to Amanda Kingsley, who owns Options Capital and also works as a sales training consultant. “Even over the phone, you need to treat people with understanding. You need to inspire the trust that you could provide the advisory help they need.” Small details, like remembering a potential client’s daughter just got married, mean a lot, she says.

“It comes down to drive and personality,” says John Celifarco, sales manager at Sure Funding Solutions. He finds there’s not much room for the thin-skinned and it takes a certain kind of person to succeed. “When you find the right people, it usually clicks pretty quick,” he says. “For the people who don’t work out, it usually falls apart pretty quick.”

“I look for strong personalities,” says Isaac Stern, CEO of Yellowstone Capital. “I don’t believe you can necessarily teach someone to sell,” he asserts. “This isn’t an easy sell, so you have to have a Type A personality. They’re on the phone and they’re confident whether they know the product or not in the beginning.” The interview process can “weed out” candidates who aren’t going to find success, he says.

Don’t expect someone with a background in outside sales to find happiness spending eight hours a day on the phone as an inside salesperson, warns Stephen Halasnik, managing partner at Financing Solutions. As a direct financing company, his firm hires salespeople different from those an ISO or broker employs, he says. His company expects salespeople to act as consultants who are knowledgeable about finance and empathetic to small-business owners.

Nearly every company prefers candidates with selling experience, possibly in telemarketing. Some seek reps with a background in selling financial services, but others prefer prospective employees who are new to the industry. “I don’t want to hire someone else’s problem child,” Stern asserts. “I’d like them to learn the way we do things from start

to finish.”

“Different offices have different cultures, so someone who has worked well in one office might not work well in another,” Celifarco says. People hired from other companies may bring bad habits, he says. They may approach the job in a variety of ways they’ve learned elsewhere and thus prevent the company from presenting a consistent face to the public, he says. “Every company has an identity,” he contends.

“Different offices have different cultures, so someone who has worked well in one office might not work well in another,” Celifarco says. People hired from other companies may bring bad habits, he says. They may approach the job in a variety of ways they’ve learned elsewhere and thus prevent the company from presenting a consistent face to the public, he says. “Every company has an identity,” he contends.

Applicants without a sales background sometimes rise to the occasion and succeed, says Ramirez. In fact, one of his top sales managers joined the company with no sales experience. Former entrepreneurs, even those without a sales background, often have a lot in common with other small-business owners and that helps them do well, he notes.

Excel Capital Management seeks salespeople with differing backgrounds for two different types of roles in its sales force, says Otar. Openers work on salary and should have phone sales experience so they’re comfortable on the telephone. Closers, who work for commissions, should have experience at selling financial services products or something closely

related, such as stocks or mortgages, he says.

While good hiring practices bring good employees into the company, they also guard against inviting bad ones into the fold. World Business Lenders uses several third-party companies to perform background checks and pre-employment screening, but most often calls upon ADP, says Alex Gemici, the company’s chief revenue officer. ADP performs evaluations that comply with the laws of the states where the employees are located, he says.

Eliminating unsavory candidates carries special significance in the alternative-finance business, notes Ramirez. “It’s critically important that they have no background issues,” he says. “In this industry there a lot of bad apples out there. It’s important that they don’t infiltrate our organization.”

“It’s very difficult to find loyal guys,” Otar laments. “They come in and utilize all your systems and then you catch them stealing.” In other words, they pass deals along to other companies. Otar has caught three of his closers doing exactly that. “You’ve got to be very careful,” he warns, adding that it’s difficult to spot bad actors because they’re skilled at selling themselves.

Once a company chooses the best candidates, the training can begin. New salespeople always start on Mondays at World Business Lenders, and the company’s corporate headquarters conducts sales training nationwide that day, says Gemici. The full day of instruction originates at headquarters, and new hires at branch locations participate on Skype. Subjects include the industry in general, specific company products and sales tips.

On Tuesdays, the World Business Lenders branches take over the training for a day or more, Gemici notes. That instruction, which lasts as long as the branches decide, can include having the new employees “shadow” more-experienced workers and having crack salespeople listen in on the phone calls of the new staffers as they make their pitches.

In the World Business Lenders office in California, Ramirez continues the training every day of a new employee’s first two weeks on the job. Tuesday and Wednesday of the first week, he spends the full eight-hour day with them. After that, he sets aside at least two or three hours of instruction each day. “I want to err on the side of over-training,” he explains.

From there, education continues as long as employees work for the company, Ramirez says. That can include spot training that he institutes anytime he sees a problem or an opportunity for improvement. Ongoing training also helps salespeople keep up with changes that occur in the industry, he notes.

The sales staff in the California office of World Business Lenders also assembles in a conference room for regular sales meetings. Ramirez picks a rep who’s outstanding at some aspect of the job to deliver a short lecture on the subject at those meetings. A star at prospecting, for example, could explain tricks of that part of the trade and then field questions on the subject. “That way, everybody can learn what everybody else knows,” he says.

For ongoing training at Financing Solutions, Halasnik calls his staff into a “huddle” for 10 minutes every day. They review what deals are pending so that salespeople know what management is seeking and can use that knowledge when they’re gathering data from customers. “We’re looking for reasons to give someone financing that doesn’t fit the cookie cutter approach a bank would use,” he notes. The team also use the huddle to share information about the industry.

At Sure Funding Solutions the sales staff meets every couple of weeks for ongoing training. They talk about some aspect of the sales process, such as opening, closing, dealing with banks, what’s working and what’s not working, says Celifarco. “I’ve been in this business since ’08, and I’m still learning new things,” he notes, adding that changing one phrase in a pitch could get better results.

Ongoing training at Excel hinges on monitoring phone calls to ensure openers are asking the appropriate questions to qualify leads and that closers are working effectively, Otar emphasizes. “It’s a never-ending process to learn what to say at the right time,” he says of his company’s training policies. Salespeople who have mastered the basics can bring their own personalities into their presentations to avoid sounding as though they’re reading from a script and thus foster an organic conversation, he notes. “That’s perfect – it’s golden,” he exclaims.

Kingsley agrees. “Don’t be too ‘salesy,’” she counsels. “That’s the best sales advice I can give.” Nobody enjoys receiving a telemarketing call, she reminds her trainees. Larger companies probably won’t heed that tip because they’re focused on volume, but smaller companies can avoid the “salesy” trap, she says.

Training should also teach originators to avoid industry jargon on their calls because prospects simply may not know the lingo, Kingsley cautions. Closers should learn from their training that knowledge of the customer’s industry can help build a relationship, she says. And knowing the customer’s industry also helps salespeople convey a deeper understanding of creditworthiness to underwriters, she maintains.

Financing Solutions trains salespeople to reveal information to clients through a string of questions instead of merely throwing out statements about the company’s products, Halasnik says. The questions can include how the customer’s business works and how he’ll use the money. That can allow the client to sell himself, and it can help the salesperson explain the client’s situation to the underwriters, he says.

Salespeople should learn to present themselves as professionals and avoid sounding like used car dealers, Halasnik maintains. “They have to understand business,” he notes, adding that training must convey that sensibility because “they don’t really come in that way.” In fact, he maintains that financing Solutions has to persevere in continuing to help the sales staff understand how small-business owners think.

Even though training never ends, it eventually pays off, Halasnik contends. He looks forward to the time – possibly in six months or so – when the roles reverse because his salespeople are picking up so much information that they’re training him. The fact that sales reps are making contact with customers keeps them in touch with the pulse of the industry, he notes.

But problems can arise even with the most persistent training efforts, so it’s also vital to begin the process with employees who are trainable, Kingsley suggests. “Some people listen to you, but then they don’t act on the advice,” she maintains. Others don’t want to expend the effort necessary to research their customers’ industries. “If you’re going to make $10,000 off of a sale, put in the work for it,” she admonishes.

Some companies are hiring lots of salespeople and putting them to work quickly as part an effort to achieve sheer volume, Kingsley says. Instead, she recommends training a smaller number of reps to conduct themselves in a transparent manner that promotes repeat business.

World Business Lenders allows for a 90-day period to determine whether a new salesperson and the company are a good fit, says Gemici. Turnover occurs during that period, often because the company is growing so quickly that it’s necessary to take on a few inexperienced employees, he says. For salespeople who complete the 90 days, the success rate is high, he notes.

World Business Lenders allows for a 90-day period to determine whether a new salesperson and the company are a good fit, says Gemici. Turnover occurs during that period, often because the company is growing so quickly that it’s necessary to take on a few inexperienced employees, he says. For salespeople who complete the 90 days, the success rate is high, he notes.

“We like to say six weeks,” Otar says of his company’s probationary period. By then, a closer should be making four to seven deals a week, he suggests, noting that openers should generate 15 to 25 leads weekly and five to seven should be getting funded.

Salespeople can require four months to really catch onto their jobs, according to Halasnik. He finds that he can gauge their progress by the quality of the questions they ask, not by what they say. As they learn the business, their questions improve, he notes.

The effort required to find and train salespeople can tempt some companies to steal good employees from their competitors, but the problem’s no more severe in the alternative-finance industry than in other businesses, according to Ramirez. “I never intentionally poach someone else’s employees, although people have tried to recruit mine,” he says. “Most of these people are clients. These competitors of ours send deals to us so I don’t want to do anything to jeopardize that relationship nor do I think that’s a good business tactic.”

So where are those prospective employees hiding? World Business Lenders employs a full-time in-house recruiter to ferret them out. Excel finds candidates on industry blogs or through general employment websites. Kingsley urges companies to contact colleges to seek out finance majors. Stern says he puts up a post and receives “tons of resumes.”

Wherever the employees come from, one of the keys to their success lies in understanding the customer’s business, Halasnik maintains. “If you only think of your business as money, it could be a little bit boring,” he says. “If you think about who the clients are and how they got there and who their customers are, that’s the fun part of the job.”

Square Capital Made More Loans, Maintained Default Percentage, Continued to Show Why They’re A Tough Competitor in Fintech Loan Market

February 22, 2017Square has continued to set itself apart in the fintech lending space. The company announced Wednesday that Square Capital had facilitated 40,000 business loans for a total of $248 million in the fourth quarter of 2016. And they did that while holding their default rate at 4%.

A look at their recent loan volume compared to their competitor OnDeck:

| 2016 | Square | OnDeck |

| Q1 | $153,000,000 | $570,000,000 |

| Q2 | $189,000,000 | $590,000,000 |

| Q3 | $208,000,000 | $613,000,000 |

| Q4 | $248,000,000 | $632,000,000 |

Square Capital’s biggest competitive advantage is that they have practically no acquisition cost for their borrowers. “We’re able to upsell and cross-sell to our base of millions of sellers with minimal incremental cost,” Square’s Q4 earnings presentation says. Their payment’s customers, which they can convert to borrowers, processed around $50 billion in transactions last year.

Square had a net loss of $171.6 million across 2016 however, the bulk of which originated in the first quarter. The net loss for Q4 was only $15 million.

Prospa, Now Valued at $235 Million, is a Major Online Small Business Lender

February 22, 2017 Online small business lending in Australia is taking off, especially for Sydney-based Prospa, who according to the Australian Financial Review, has slightly more than half of the industry’s market share. The company just announced a $25 million (AUD) equity round led by AirTree Ventures that pegged Prospa’s value at $235 million (AUD).

Online small business lending in Australia is taking off, especially for Sydney-based Prospa, who according to the Australian Financial Review, has slightly more than half of the industry’s market share. The company just announced a $25 million (AUD) equity round led by AirTree Ventures that pegged Prospa’s value at $235 million (AUD).

Prospa is significant in that it received early support from US-based Strategic Funding, the same company that just absorbed the US operations of Capify. A 2013 press release said that Strategic would be providing the technology for the electronic servicing, underwriting and cash management of all Prospa Advance accounts in Australia in addition to jointly funding all the merchant cash advances and loans they originated. Sources say however that the arrangement is no longer in effect.

In September 2015, The Carlyle Group, one of the largest private equity firms in the world, participated in a $60 million round for the company. Prospa has now funded more than $250 million to small businesses since inception.

“The market in Australia has been very ripe for alternative finance,” Prospa co-CEO Beau Bertoli said to deBanked about 18 months ago. “We see an opportunity for the alternative finance segment to be more dominant in Australia than it is in America.”

The Australian Financial Review cites Bertoli as more recently saying that the market there could grow to at least $20 billion in the next five years.

Similar to offers in the US, Prospa lends between $5,000 to $250,000 for loans up to one year.

What Shakeout? Breakout Capital Secures $25 Million Credit Facility

February 8, 2017 Put a tally up on the board for small business lenders in 2017. McClean, VA-based Breakout Capital, which just announced a move into a larger office last week, has also secured a $25 million credit facility with Drift Capital Partners. Drift is an alternative asset management company.

Put a tally up on the board for small business lenders in 2017. McClean, VA-based Breakout Capital, which just announced a move into a larger office last week, has also secured a $25 million credit facility with Drift Capital Partners. Drift is an alternative asset management company.

Breakout is young by today’s industry standards, founded only two years ago by former investment banker Carl Fairbank, who is the company’s CEO. And don’t count them out just because they’re not in New York or San Francisco. Washington DC’s Virginia suburbs have become somewhat of a hotspot for fintech lenders. OnDeck, Fundation, StreetShares and QuarterSpot all have offices there, Fairbank points out. “And Capital One is right up the street,” he adds while explaining that the community has a strong talent pool that is familiar with creative lending. Breakout has already grown to about 20 employees and they’re still growing, he says.

Fairbank considers Breakout to be a more upmarket lender, whose repertoire includes serving the near-prime, mid-prime customer. CAN Capital and Dealstruck had focused on this area and both companies stopped funding new business in 2016. As I point this out, I ask if that suggests that segment is perhaps too difficult to make work.

“Candidly, that’s the part of the market that I feel the best about,” he says matter of factly. The company tries to product-fit deals based on the borrower, and will even make monthly-payment based loans. “I think the subprime side with the stacking and the debt settlement companies is a very very difficult place to play right now,” he says, adding that they have worked with subprime borrowers using their original bridge program but that they’ve kind of pulled back from doing those. As with all programs regardless, their goal is to graduate merchants into better or less costly products later on. We have helped merchants move on to get SBA loans, he maintains.

That all sounds very hands on, and part of it is, Fairbank confirms while asserting that technology does indeed do a lot of the legwork. “There’s absolutely a human element to underwriting these deals,” he says. He also agrees with much of what RapidAdvance chairman Jeremy Brown wrote in a deBanked op-ed titled, The New Normal. Both Breakout and RapidAdvance refer to themselves as technology-enabled lenders, an acknowledgement that tech is a component of the company, not the entire company itself.

“I think we will see the beginning of the demise of fully automated, no manual touch funding,” Brown wrote in his article.

Brown also predicted that the legal system will ultimately impose order on some industry practices like stacking or that a state like New York could take a public policy interest in products he believes have legal flaws. As he was writing that, Governor Cuomo’s office published a budget proposal that redefined what it means to make a loan in the state. And it leaves much to be desired, some sources contend. Two attorneys at Hudson Cook, LLP, for example, published an analysis that demonstrates how its wording is ambiguous and far-reaching.

“What they really need to do is take the time to think through the implications and basically do a full study of the market to ensure that what they’re pushing forward is going to have the desired consequences,” Breakout’s Fairbank offers on the matter.

This doesn’t mean he’s anti-regulation. The company already holds itself to high standards and customer suitability and is a founding member of the Coalition for Responsible Business Finance.

“I personally do believe that there’s bad forms of lending or cash advances in the market and I’m sure that’s what Cuomo thinks as well but at the same time, it’s getting pushed very quickly and they really really ought to step back and do the research to understand the broader implications and to understand what exactly they’re trying to accomplish,” he maintains.

His pragmatism extends to the OCC’s proposed limited fintech charter, which he finds intriguing, assuming it gets buttoned up. “I believe it’s a concept worth pursuing,” he says, explaining that regulators will need to get comfortable with unsecured lending.

In the meantime, he’s optimistic about Breakout’s prospects. “In a time when institutional appetite for alternative finance companies has dried up, we believe our ability to raise a credit facility in this market speaks volumes about what we have already accomplished, our position as a leading player in the space, and our prospects for strong, but measured, growth,” Fairbank is quoted as saying in a company announcement. The company was also invited and joined the Task Force for the PLUM Initiative, a collaboration between the U.S. Small Business Administration (SBA) and the Milken Institute to more effectively provide capital to minority-owned businesses throughout the United States. The Task Force consists of a very select group of industry leaders, who are in positions to improve access to capital in underserved markets, according to the announcement.

While other companies are making adjustments or in his opinion, continuing to make questionable underwriting decisions, Fairbank thinks his formula for success works. “I think that we do look at deals differently than most folks because I intentionally built the core of my underwriting team with folks who are not from this space so they take a more traditional approach and mix it with some of the greatest aspects of alternative finance.”

OnDeck’s COO Announces Resignation Prior to Q4 Earnings

February 3, 2017OnDeck COO James Hobson notified the company on Friday that he is resigning to “pursue another opportunity.” According to the 8-K filed with the SEC, it will become effective on March 15, 2017.

Hobson started at OnDeck in 2011 and became the COO in 2012.

The announcement comes weeks before OnDeck is expected to disclose their Q4 and full-year 2016 report. In Q3, the company had shifted to keeping more loans on their own balance sheet, while increasing their reliance on third party brokers for business. They had also reported a GAAP net loss of $16.6 million for the quarter, bringing the 2016 Q1 – Q3 total losses to $47.1 million.

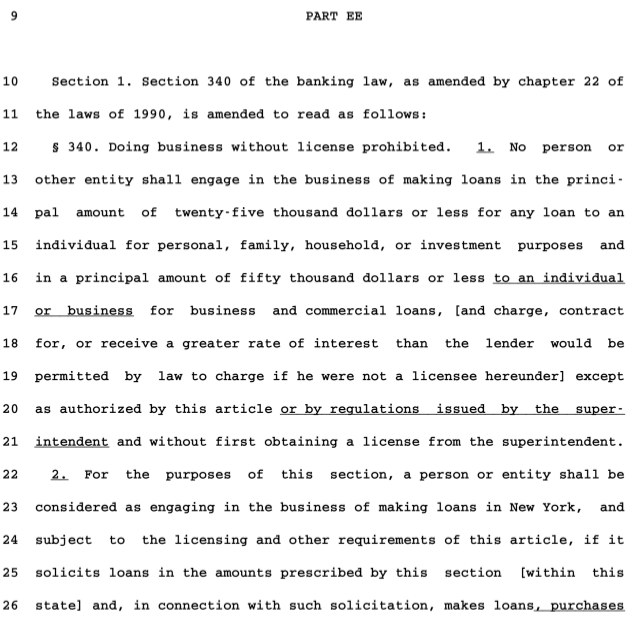

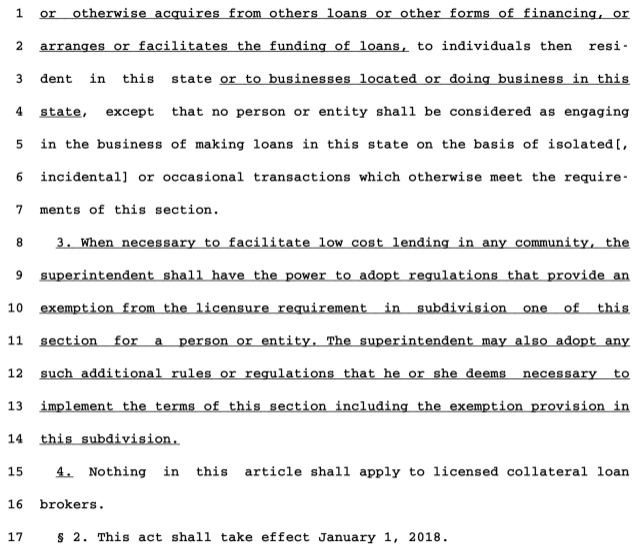

New York’s Proposed Budget Slips In Sweeping Regulation of Non-bank Business Lending and Finance

January 28, 2017In New York, Governor Cuomo’s 309-page budget proposal includes a handful of sentences tucked in towards the end (Part EE) that would revise Section 340 of the state’s banking law. And the implications are broad, given that it calls for any person or entity involved in the soliciting, arranging or facilitation of business and consumer loans or other forms of financing to be licensed in order to engage in such activity. It appears that MCA companies as well as business loan brokers and ISOs would be directly impacted.

If it passes, the regulator tasked with overseeing that would be the New York Department of Financial Services. It would be effective January, 2018.

For consumer loans, it applies to loans $25,000 and under. For business financing, $50,000 and under.