Business Lending

Funding Circle US Originated $800M in 2020, More than 90% of Borrowers Were Making Payments

March 26, 2021 Funding Circle US revealed originations of £581M in 2020, equivalent to about $800M at current exchange rates. More than 90% of the company’s American borrowers were making full regular payments on their loans, Funding Circle reported. Approximately 7% were on a “payment holiday” at year-end or were not paying.

Funding Circle US revealed originations of £581M in 2020, equivalent to about $800M at current exchange rates. More than 90% of the company’s American borrowers were making full regular payments on their loans, Funding Circle reported. Approximately 7% were on a “payment holiday” at year-end or were not paying.

Funding Circle’s US loans generate low annual returns, its highest being a projected return of 4.1% to 4.9% for its 2016 cohort. Its 2020 cohort is projected to generate an annual return of between 1 – 3%.

Overall, Funding Circle reported a total net loss of £108.1M (approx $150M US) on just £103.7M in revenue, a massive loss that stemmed entirely from the first half of the year, attributed mostly to a write-down in “fair value.”

Funding Circle’s primary market is the UK. When comparing the market with the US, the company said that the US is in an earlier stage of development even though the market is 5x larger.

Tune In Tuesday at 10:30 AM EST: deBanked TV Live – With Guests From the Business Funding Industry

March 22, 2021 deBanked is hosting a livestream broadcast tomorrow beginning at 10:30 AM from a venue in Midtown Manhattan with guest speakers from two broker shops and a business funding company. There is no need to register for anything. Anyone can tune in live at deBanked.com/tv to watch it. The broadcast will run for 2.5 hours and end at 1 PM. This is an-person event being broadcast with no Zoom or virtual conversation. The event will also be recorded and made available free.

deBanked is hosting a livestream broadcast tomorrow beginning at 10:30 AM from a venue in Midtown Manhattan with guest speakers from two broker shops and a business funding company. There is no need to register for anything. Anyone can tune in live at deBanked.com/tv to watch it. The broadcast will run for 2.5 hours and end at 1 PM. This is an-person event being broadcast with no Zoom or virtual conversation. The event will also be recorded and made available free.

deBanked’s massive in-person conference, Broker Fair, will return to NYC later in the year on December 6th at Convene at Brookfield Place in lower Manhattan.

Was That Loan Forgiven? The Tax Man Cometh

March 10, 2021 With tax season upon us, the events of 2020 will soon be reviewed and evaluated by everyone’s best friend, the IRS. Lenders that offered debt forgiveness might have done a favor to distressed borrowers in 2020, but a consequence of that courtesy is that the borrowers’ forgiven debt might be taxable.

With tax season upon us, the events of 2020 will soon be reviewed and evaluated by everyone’s best friend, the IRS. Lenders that offered debt forgiveness might have done a favor to distressed borrowers in 2020, but a consequence of that courtesy is that the borrowers’ forgiven debt might be taxable.

This is as good a time as ever to review a report prepared by Grassi Advisors & Accountants whether you are a lender that forgave debt or a borrower that had debt forgiven.

“This issue was noticed early last year,” said deBanked President Sean Murray, “but at the time everyone was so focused on PPP forgiveness, the EIDL program, and government stimulus, that I think the potential consequences of lenders forgiving non-PPP debt for their borrowers were lost in the shuffle. Imagine you’re a borrower that had $100,000 of non-PPP debt forgiven last year and you’re only now about to learn that the IRS may classify that as income. Or worse yet, you don’t even realize it and are told that later on during an audit.”

In May 2020, deBanked labelled this as a hidden tax time bomb that was set to detonate in 2021. And now here we are.

Square Officially Becomes a Bank

March 2, 2021 Square launched its own industrial bank Monday, after receiving a charter from the FDIC. The Salt Lake City, Utah-based bank will begin underwriting business loans under the Square Financial Services title.

Square launched its own industrial bank Monday, after receiving a charter from the FDIC. The Salt Lake City, Utah-based bank will begin underwriting business loans under the Square Financial Services title.

“Bringing banking capability in-house enables us to operate more nimbly,” CFO and Chair of the new bank Amrita Ahuja said, “which will serve Square and our customers as we continue the work to create financial tools that serve the underserved.”

Square had previously offered credit products through a partnership with Utah-based Celtic bank. The move answers the questions “buy or build” when it comes to fintech banking. Many fintech firms, some of who even claimed to be anti-bank alternatives, have made the switch to either partnering with a nationally chartered bank or outright becoming a bank themselves.

“We thank the FDIC and Utah DFI for their partnership enabling us to reach this milestone, and look forward to continuing to expand access to financial services at this critical time for small businesses,” Ahuja said.

ODX Merges with Fundation

February 25, 2021 The ODX brand from OnDeck is splitting off to combine with Fundation, forming a new SMB digital banking company called Linear Financial Technologies.

The ODX brand from OnDeck is splitting off to combine with Fundation, forming a new SMB digital banking company called Linear Financial Technologies.

The news follows the recent disclosure from Enova that it was looking to divest ODX in addition to OnDeck Canada and OnDeck Australia.

The new firm, headed by the current CEO of Fundation, Sam Graziano, will be an online banking service provider. Linear will take on Fundation’s service of processing loans for big and small banks, reportedly processing a total of $13 billion.

“Over the years, our combined platforms have served hundreds of thousands of business customers through many of the leading business banking providers in the market, deploying modern banking experiences that their customers and front-line colleagues expect in the digital era,” said Graziano in the published announcement. “Together as Linear, we’ll have the resources to more rapidly expand the breadth of our solutions to bring more value to our clients.”

Enova will retain a minority stake in the new firm.

Square Originated $254M in Loans in Q4, Nearly a Billion For the Year

February 23, 2021 Square released its Q4 earnings on Tuesday, disclosing that the Square Capital division originated 57,000 loans for $254 million.That brings them to $957 million on the year.

Square released its Q4 earnings on Tuesday, disclosing that the Square Capital division originated 57,000 loans for $254 million.That brings them to $957 million on the year.

Just before the earnings release, Square reported they had also bought $170 million worth of additional bitcoin. After purchasing $50 million in October, no wonder the firm doubled down. Reportedly 48% of Square’s total revenue in 2020 was from bitcoin and bitcoin trading. 85% of all value added in 2020 was bitcoin-related.

Overall, Square added $9 billion in net revenue in 2020. $4.5 billion of which was Bitcoin revenue.

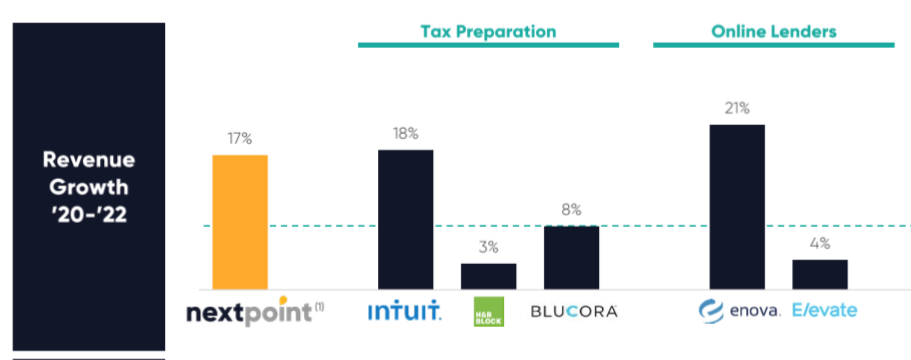

LoanMe, Liberty Tax Merger to Take on Intuit, Enova

February 22, 2021NextPoint Financial will combine LoanMe’s business, consumer, and mortgage lending with Liberty Tax’s tax preparation business, according to merger announced on Monday. Liberty’s “2,700+ locations in the US and Canada” will become consumer and SMB loan shops.

The new firm will also offer Merchant Cash Advances; LoanMe launched MCA funding in January and expects to fund $15 million in MCAs in 2021. Based on the acquisition prospectus, NextPoint will be a tax readiness firm, with the added suite of financial products as a value and growth builder.

Ramping up consumer, installment, and MCA lending, paired with the third-largest tax-prep business in the U.S, NextPoint expects to compete directly with Intuit, H&R Block, Enova, and Elevate.

Fintech firms are setting themselves apart from the competition as one-stop shops for everything a business needs, including MCA products. Why branch into financial services now? NextPoint found that this year alt lenders have outperformed the S&P500 three times over.

“We are a one-stop financial services destination empowering hardworking and credit-challenged consumers and small businesses,” the investor presentation reads. “To get to the next point in their financial futures.”

Intuit offers a variety of financial products, like business loans through Quickbooks Capital, alongside their popular, 60%+ market share of tax prep software. H&R began offering small $1,000 lines of credit this year, but not much more.

The team leading the new company, NextPoint Financial, will feature execs like Brent Turner as CEO, Mike Piper CFO, both keeping their previous Liberty Tax positions. Jonathan Williams, former president and founding shareholder of LoanMe, will become president of lending.

LoanMe Has Been Acquired Along With Liberty Tax By Canadian Listed SPAC

February 22, 2021 LoanMe has been acquired. The announcement was made by Nextpoint, a SPAC listed on the Toronto Stock Exchange that simultaneously acquired Liberty Tax.

LoanMe has been acquired. The announcement was made by Nextpoint, a SPAC listed on the Toronto Stock Exchange that simultaneously acquired Liberty Tax.

The combined company will be called NextPoint Financial.

NextPoint will acquire LoanMe at an enterprise value of approximately US$102 million, US$18 million of which is payable in cash, approximately US$49 million of which is payable in NextPoint common stock equivalents and with the balance of which reflects the assumption of existing corporate net debt at LoanMe.

“We are a one-stop financial services destination empowering hardworking and credit-challenged consumers and small businesses to get to the NextPoint in the financial futures,” the company said of its newly formed self.

The company says that LoanMe had originated $2 billion since inception, 340,000+ borrowers since inception, and has a $200 million loan portfolio. Liberty Tax, meanwhile, processes 185,000+ SME tax returns, 1 million+ US consumer tax returns, and 400k+ Canadian tax returns.

Combined, the company projects $317M in revenue in 2021.

“NextPoint has obtained a commitment for a new US$200 million revolving credit facility, advances under which may be used for NextPoint’s general corporate purposes, including to fund the Liberty Tax and LoanMe cash purchase prices, and to fund potential future acquisitions,” the company said in a public release.