Business Lending

LendingTree: SMB Lending Cools Slightly

May 7, 2026“When the war started in March and gas prices went way up, that was a shock to the system in that month specifically,” said LendingTree CEO Scott Peyree. “Now, on the small business lending side, I would say we are seeing a little bit of both—fewer small merchants looking for loans and smaller loan sizes than normal. On the lender side, credit is still available, but they are typically offering lower loan amounts at higher interest rates.”

Peyree believes this will correct on its own.

“When you have a cautious merchant to begin with, and then they are not getting the exact loan they want and at a higher interest rate, the sense we are getting is they are just not as urgently looking for money right now because of macro geopolitical stuff that is going on,” Peyree said. “I still think this is a short-term thing that will go away. Once consumer sentiment comes back up and, hopefully, things settle down geopolitically, I think we will be right back off to the races.”

Revenue from the small business segment of its business, however, was still up 49% YoY and they’ve brought on more people to help these businesses choose a solution.

“We have selectively added to our SMB concierge team to help more customers find the right financing options, while increasing the speed of application submission, approval, and funding,” the Q1 shareholder letter states.

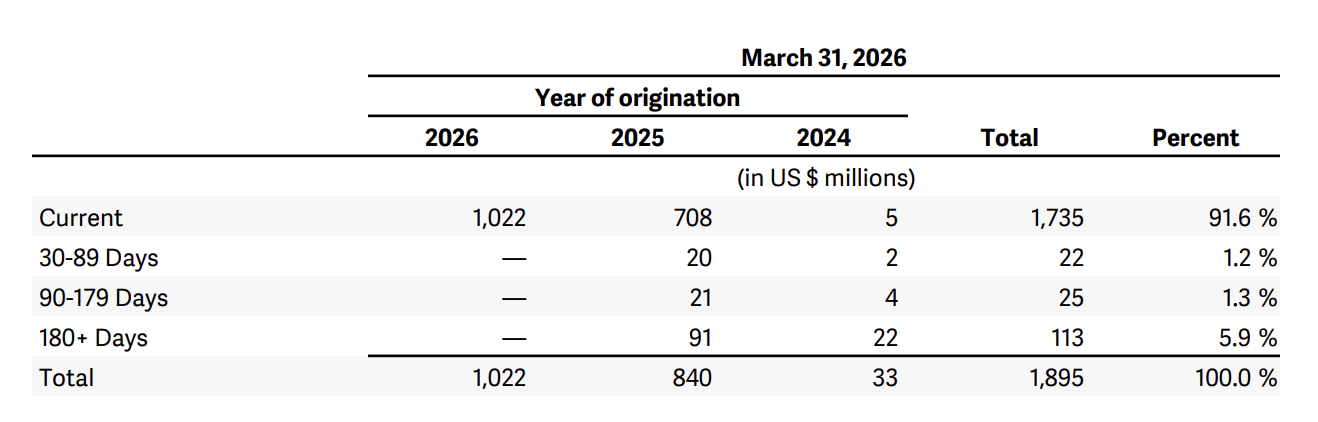

Shopify Capital: $1.4B in Business Loans and MCAs in Q1

May 5, 2026 Shopify’s business loan and merchant cash advance offerings continue to increase. This follows a consistent decade-long rise with no down years. In Q1, the company originated $1.4 billion in business loans and merchant cash advances, up from $821 million YoY. Based on the weight of the respective receivables, the product mix is roughly 82% loan-based and 18% MCA.

Shopify’s business loan and merchant cash advance offerings continue to increase. This follows a consistent decade-long rise with no down years. In Q1, the company originated $1.4 billion in business loans and merchant cash advances, up from $821 million YoY. Based on the weight of the respective receivables, the product mix is roughly 82% loan-based and 18% MCA.

Of the loans it originated in 2025 that still have an outstanding balance, 10.8% were more than 6 months behind on their original payment schedule as of March 31, 2026.

Delinquency chart in in the Q1 docs:

Enova: $1.7B in Business Loans in Q1, New Record, Competition Hasn’t Changed

April 28, 2026“Our SMB business continued to deliver remarkable growth and stable credit as our leading brand presence, scale, and strong competitive position drove 42% year-over-year growth in originations to a record 1.7 billion dollars,” said Enova CEO Steve Cunningham during the Q1 earnings call. “Our SMB portfolio has grown 37% over the past year and remains intentionally well diversified across geographies and industries. In addition, the SMB net charge-off ratio remained in a tight range consistent with the past two years.”

The company indicated that economic signals look strong despite rising gas prices and that they expect the growth in SMB lending to continue.

When Kyle Joseph at Stephens asked Cunningham to size up the competitive environment they face in their sector, Cunningham said that they have the advantages.

Cunningham:

“The SMB market is large, and new business formation over the past five or six years has been really strong if you look at new business applications. Those companies that are a couple of years into their life and have shown staying ability become potential customers. So the market is growing, probably a little faster than the overall consumer market. Regarding our presence, brand, scale, and capabilities, our set of competitors has not really changed much over time, and we believe we have a lot of advantages. It is a great setup: a large, growing market and competitive advantages that allow us to be selective and generate growth that creates strong returns for us and our shareholders.”

Just the Facts With LendFax

April 1, 2026More than 76% of small business owners who apply for financing through their system do it from a mobile device. That’s the fax from LendFax, a one-stop shop for business owners (and consumers) to be paired with the most appropriate service provider for their needs. The information they submit through the curated intake process is pushed to their partners via API, and then LendFax continues to communicate with those customers to make sure they complete the process with them.

Nick De Jesus, LendFax’s Chief Marketing Officer, says that the process relies on enterprise-grade infrastructure to make it all work and is the culmination of years of in-house development and an obsessive desire to achieve the most optimal outcomes for all parties in the process.

“I’m working non-stop, 12 hours, 13 hours a day on this, 100% passion, I couldn’t see myself doing anything else,” De Jesus says of his time spent at LendFax.

That he’s there doing this at all is due to a chance intersection in his life. For example, De Jesus had been on an accelerated track in college and was bound for medical school at an extremely young age. His special area of study as a nineteen-year-old was heterotopic ossification and involved researching bone formation from trauma and soft stem cell tissues. And that was the path he had surrendered himself to until one night, a few acquaintances asked for his input on a tech project involving small business financing, thinking his broad knowledge could be insightful. But what De Jesus learned from them had him hooked immediately, and he dropped everything to be a part of it.

“I finished my cell biology exam and the next Monday I was in [their] office,” De Jesus said.

De Jesus says that they’re aware that LendFax isn’t the only operator of their kind in the space, but that by being lean and running efficiently, partners on their platform can get “enterprise infrastucture without the enterprise pricing.” Depending on the relationship setup, partners can get as little as a merchant’s qualified and completed application or as much as the entire deal with full docs, all managed by LendFax and ported into the partner’s CRM in real time.

De Jesus is a regular at the big trade shows and stressed just how important in-person relationships are in this field, but noted that the merchant side is different, that merchants looking for financing have trended toward solutions that produce the least amount of friction and interaction along the way.

“…things are moving definitely more to the digital landscape where people just want to go online, submit information, without even texting or talking or emailing anybody and get an answer,” De Jesus said. “So that’s kind of what we’re trying to do with LendFax, is we’re kind of just trying to bring them the offers based on the answer that they select.”

Eddie DeAngelis to Speak at Broker Fair 2026

March 31, 2026

Eddie DeAngelis will be speaking at Broker Fair 2026 in New York City on June 1. DeAngelis owns a high-performing small business finance brokerage.

About QualiFi

QualiFi’s journey is just getting underway and will be extraordinary. We get to push the reset button one more time and apply what we’ve learned from our many successes and failures. Our current mission with QualiFi is two-fold, and we’re inspired to make it happen. We’re determined to take the hassle out of small business financing by building an accessible, affordable #1 client experience for business financing, one client at a time.

California Bill Asserts Businesses Generating Up to $18 Million/Year in Sales Need Consumer Protections

March 10, 2026California’s AB2116 is proposing to amend the state’s Consumer Financial Protection Law and declare that small businesses generating less than $18 million a year in revenue be considered a consumer for the purpose of consumer financial protections.

“Small business” means a business entity organized for profit with annual gross receipts of no more than sixteen million dollars ($16,000,000) or the annual gross receipt level as biennially adjusted by the Department of General Services in accordance with Section 14837 of the Government Code, whichever is greater.-AB2116

The DGS alternative, when applied to the “whichever is greater” test, currently sits at $18 million, making that the current applicable baseline for what is small.

“Small business owners are often similarly situated as consumers with regards to their sophistication and bargaining power relative to providers of financial services and products,” the bill says. “Many of the rationales supporting legal protections for consumers apply also to small business owners. Small businesses have a better chance to survive and grow if they are able to access safe and effective financial products and are protected from unfair, deceptive, or abusive practices when accessing financial products and services.”

For comparison’s sake, deBanked tracked one online small business lender that originated $200 million in business loans that generated just $14.3M in revenue. Per the bill, this lender would also be presumed an unsophisticated consumer that is unable to bargain on financial service products without consumer protections.

Lending Tree: “The merchant cash advance market is a strong market that is growing”

March 3, 2026 “The merchant cash advance market is a strong market that is growing,” said Lending Tree CFO Jason Bengel during the company’s Q4 earnings call.

“The merchant cash advance market is a strong market that is growing,” said Lending Tree CFO Jason Bengel during the company’s Q4 earnings call.

Small business financing has become an increasing priority for the financial services referral platform.

“…we have continually invested in additions to our small business concierge sales force, allowing us as well as lenders on the network, to help a greater number of business owners find the best loan options for them while guiding them through the often complex process of completing their application through to funding,” said Lending Tree CEO Scott Peyree.

Though Lending Tree is considered a platform, they describe themselves as a business loan broker, one with a name that helps lenders reach merchants they would otherwise never be able to connect with.

“A lot of our small business lenders, for example, they do not even write direct to merchant,” Peyree said. “They write loans through brokers like us. Deep API logged-in access for us to get their loan information, these consumers do not even know that these companies exist, outside of talking to us to get a loan.”

NerdWallet: LLM Referrals Convert Much Better, Licensing Regulations A Barrier to AI Shopping Takeover

March 3, 2026“…in terms of what we’re seeing on our side, the conversion rates on that LLM referral traffic are much higher and growing rapidly,” said NerdWallet CEO Tim Chen during the Q4 earnings call. “People, I think, are searching more both on traditional search engines as well as LLMs.”

NerdWallet had taken a hit on organic search traffic throughout 2025 due to search engines like Google adjusting organic search layouts and rankings but they’ve made up for the lost business by a combination of paid marketing and referrals coming in from AI. Although the AI LLM traffic isn’t enough to replace the loss in organic search traffic, those referrals are said to have a much better conversion rate. The LLMs themselves aren’t a threat to replace the entire shopping experience, however, because of existing regulations.

“I mean I think if you think about the scenario where you’re trying to do some form of agentic shopping or LLMs are trying to get more integrated, there’s kind of 2 obstacles you really need to think about,” said Chen.

So the first is regulatory. For example, you can’t get an insurance quote from someone without an insurance license. And so if you look across, for example, credit, insurance, mortgages and investing, they require licensing where institutions need deterministic and compliant outputs, not probabilistic answers.”

NerdWallet is a platform that connects consumers and SMBs with financial products.