Business Lending

Building a High-Trust Lending Platform in a Low-Trust Environment

July 7, 2026Richard Henderson is the Chief Executive Officer of BriteCap Financial, a technology-enabled small business capital platform that has deployed over $1 billion to support American small businesses. He brings more than two decades of leadership experience in financial services and small business lending, with a track record of driving growth, strengthening operational discipline, and leading strategic transformation. Prior to BriteCap, Richard served as Chief Revenue Officer at CAN Capital and held senior leadership roles at Marlin Capital Solutions and CIT Bank.. Learn more at https://www.britecap.com

Let’s start with something most people in this industry understand but don’t always say clearly: The barrier to entry into the revenue-based financing space is relatively low. That’s true for brokers. It’s also true for funders.

And that matters. Because when barriers are low, standards tend to vary. A lot.

There are exceptional operators in this space—on both sides. I’ve met and worked with many who actually care about their customers, about building real relationships, and about seeing their businesses and customers thrive long term. There are also aggressive players. Some cross lines; some don’t even realize they’re crossing them.

Over time, the market reflects all of it: Borrowers come in skeptical. Good brokers feel like they have to defend themselves, funders feel the same, and an entire industry gets lumped together. And when viewed as a whole that way? The industry doesn’t look that great.

That’s the environment.

The Scaling Problem

In my experience, most businesses in this industry don’t break because of bad intentions. They break when they scale.

A great broker or funder can run a clean, high-integrity operation as an individual or small team. But what works at 1–5 people doesn’t automatically work at 25, 50, or 100.

Why? Because standards that live in someone’s head don’t scale. They have to be explicit, operationalized, and enforced. If they’re not, small decisions start to drift:

• Deals are framed a little too aggressively.

• Details are left out because they “probably won’t matter.”

• Customers are pushed a bit further than they should be.

Nothing dramatic. Until it compounds.

Where Things Actually Go Wrong

Let’s talk about something real.

There are cases where a business owner takes a loan, then quickly gets stacked—sometimes multiple times—with compounded payments outstripping cash flow. In the worst cases, that same customer ends up being referred into a debt settlement situation by the same bad actor who just keeps getting paid. This happens at the expense of the customer we’re all supposed to be trying to help, not harm.

They’re over-leveraged, their credit is damaged, and their access to capital is effectively shut down for a long time—if not permanently. Or worse, it turns a business owner into a former business owner.

That’s not a one-off issue. It’s a structural vulnerability. And here’s the uncomfortable part: Without the right controls, well-meaning organizations can participate in that outcome without even realizing it. It just takes one bad actor within your organization.

Intent isn’t enough.

The Foundation: The Big Three

If you want to build a high-trust platform, you have to start with alignment. At BriteCap, we’ve distilled our model into three non-negotiables:

• A strong business model that delights customers profitably.

• A sales system that ensures customers are delighted consistently and predictably.

• A high-performing talent environment that drives excellence and ownership.

If your business model depends on outcomes that hurt the customer, it will fail in the long run. If your sales system isn’t consistent, the experience will drift. If your talent environment doesn’t reinforce awareness of your vision and accountability, none of it holds.

Then You Build the Controls

Trust doesn’t scale without structure. We’ve invested heavily in making sure ours does:

• Achieving SOC 2 Type II certification.

• Participating in the Secure Funder program.

• Implementing continuous inspection of vulnerabilities across our systems and processes.

And just as important: ownership. Our Chief Administrative Officer & General Counsel and our Chief Technology Officer actually own governance, compliance, and operational controls as mission-critical mandates. This is not a back-office function. It’s core to the business.

You Also Decide Who You Work With

This is where I’ve seen many platforms compromise. We don’t. And neither should you.

We run a highly selective, by-invitation-only broker and overall partner acquisition strategy. We set a very high bar for whom we’ll invite into (and allow to stay in) our ecosystem. When that standard isn’t met, we act quickly.

We walk away from brokers delivering or promising to deliver million-plus per month origination volume. That’s not theoretical; we’ve done it. Because once you let standards slip, they don’t come back.

That includes a clear stance on something that’s become increasingly common: We do not work with brokers who sell debt settlement services. Not because we don’t understand the economics, but because we understand them too well. It creates a structural conflict that almost always ends the same way for the customer. That’s not a system we’re willing to be part of.

Culture and Incentives Drive Everything

You don’t get high-trust outcomes from low-trust incentives. If your organization is purely volume-driven, behavior will follow.

We focus heavily on alignment: what we reward, what we tolerate, and what we reinforce. Our Guiding Principles act as absolute operating constraints:

• Truth-Seeking and Radical Transparency: We deal in reality.

• Ethical Decision-Making: No shortcuts, no cutting corners.

• Building a Culture of Purpose and Connection: People perform at their best when they understand what they’re building, why it matters, and how their actions impact others.

That alignment is what keeps standards high as you scale. And underneath all of it: Trust is our most valuable asset.

Technology Is Necessary—But Not Sufficient

We believe the borrowing experience should be ridiculously fast, smooth, and predictable. Technology gets us there, but technology doesn’t create trust. It amplifies whatever is already there.

If your system is disciplined, technology scales discipline. If it’s not, it simply scales problems faster.

What This Means for Brokers and Funders

If you’re building in this space, the challenge is simple—and hard: Can you maintain your standards as you scale?

That means making expectations explicit, aligning incentives with outcomes, building real oversight, and acting quickly when something isn’t right. The operators who figure that out will stand out.

The Long Game

At BriteCap, we’re building for the long term with an epic journey to number one. That’s not about being the biggest. It’s about building something that holds together at scale, delivers consistently, always keeps our customers’ best interest at the center, and earns trust over time.

In a low-trust environment, that’s the opportunity. Not to move faster than everyone else, but to build something better.

Bottom Line

Trust doesn’t break all at once. It erodes—through small decisions, unclear standards, and misaligned incentives.

The inverse is also true. Trust is built the exact same way: clear expectations, disciplined systems, aligned people, and consistent decisions. Every single day.

Do that long enough, and you’ll have built yourself a high-trust lending platform in a low-trust environment. And if enough of us do it long enough, we’ll create a high-trust, mainstream funding mechanism for small businesses. That is good for all of us.

SoFi’s Small Business Loan Product Details

July 2, 2026SoFi is now a small business lender, according to their most recent announcement.

But they’ve been in this market for a while. They first flirted with the idea in February 2023 and then launched a marketplace in January 2024 to warm up to it. As a marketplace, they referred their own customers to other direct providers of capital, including MCA companies. Under this new program, applicants will be evaluated for a SoFi business loan first and then referred to their marketplace if they don’t qualify, second. Fundbox is referenced by name as one of the possible destinations for these applicants.

SoFi’s in-house business loan comes with a max APR of 36% and dollar ranges of $2,500 – $250,000. They’re personally guaranteed and have max terms of 2 years. Applicants need not be a SoFi customer to apply and funding can take place in as little as 24 hours.

Parafin Has Funded 50,000 Businesses, How Does That Compare?

June 25, 2026Parafin’s new credit facility with Goldman Sachs was complemented by the disclosure that the company had funded more than 50,000 businesses since inception. Founded in 2020, Parafin typically markets how much it has extended in “offers” to small businesses rather than how much it has actually funded. This bucks the prevailing industry trend.

To put Parafin’s 50,000 deals funded over the last 5 years into perspective, the industry leading online lender, Square Loans, funded approximately 700,000 loans last year alone.

Parafin disclosed revenue in 2025 as $90M, which is approximately double that of Lightspeed Capital over the same time period. Lightspeed originated $340M in MCAs in 2025.

Parafin says that the majority of its fundings go to repeat borrowers. The company powers platforms such as Amazon, Walmart, DoorDash, Gusto.

Big Deals, Big Consequences: How some deals went very wrong

June 18, 2026In November 2018, a conglomerate of car dealerships went out of business in California. Within three weeks, a merchant cash advance company, 1 Global Capital, was discovered to have filed bankruptcy as a result. They had lost more than $40 million in that dealership deal alone. Over the ensuing weeks, additional funding companies revealed that they had also been in it and gotten burned, some so badly that they also closed their doors. It was a moment of reckoning for the industry as deals got bigger and the stakes got higher. At the time, it was considered the largest deal (and then the largest default) in history.

Less than two years later, an even bigger deal was revealed, a $91M MCA made by Par Funding. Par also became a rather infamous failed business.

And some time in between the two, a $1B hedge fund that provided credit facilities to small business lenders, also failed and took some lenders down with it.

In each case there was a lesson learned.

1 Global Capital

In 1 Global Capital, internal emails revealed that the company knew the dealerships were on the brink of collapse, but were compelled to keep funding them to avoid taking the loss.

“…if they were to become insolvent, everyone loses,” said 1 Global’s Director of Accounting. The result was they dug a deeper and deeper hole until they were on the hook for tens of millions and their exposure became existential.

1 Global was not forthcoming about the performance of its portfolio to its investors and by the time the dealerships went bust, regulators and prosecutors moved in to deal with the fallout.

Par Funding

In the Par Funding case, foul play appears to have been the defining issue. The large funding amounts and low defaults looked good to the investing public because the books were not being accurately reported. Par was adamant that the power of “compounding” could make up for any losses they incurred, but regulators said they had not even properly disclosed their losses to begin with and investors were not aware of them. The $91M deal was just the tip of the iceberg. Another customer purportedly owed $35M, for example. And then those combined with the next eight largest deals on their books added up to $228M, which made up 54% of their entire portfolio. Par had very severe concentration risk and compounding probably could not save it on other deals if these went bust.

Direct Lending Investments

In the Direct Lending Investments hedge fund case, the CEO had famously proclaimed that small businesses were overpaying for credit and that was how their investors stood to profit. But over time, it became evident that some of the small business lenders they backed actually had customers underpaying for credit and the losses overwhelmed the hedge fund. Unfortunately, the CEO was unwilling to concede the losses and told investors they were actually profitable instead. To try and cover it up and make it back, the hedge fund loaned nearly $200M to telecom companies at high interest rates. And because they made these loans during a state of distress and probably were not underwriting them carefully, the borrowers scammed them and disappeared with the funds. There was no longer a way out and the CEO resigned. The receiver in the case initially estimated that portfolio was then worth $500M less than what they had last reported to investors.

Ironically, the CEOs of all three companies were convicted of crimes for their roles in the lies and the losses.

Concentration risk, misleading investors, and falling victim to the sunk cost fallacy ultimately were their undoing. For some, the deals got larger to try and keep a dead deal from failing. For others, it was a Hail Mary play to try and generate a return to make up for losses elsewhere.

Soon, You’ll Be Able to Lend Against Credibly Small Business Loan Pools

May 23, 2026For most people in the small business lending and revenue-based financing industry, news of a billion-dollar securitization barely resonates. It’s too big, too abstract, especially if you’re used to the ground game of syndicating a couple million bucks in deals you handpicked with funders you personally know. Wall Street-level capital markets has always felt like a mysterious private club, where a hundred million here and a billion there changes hands through an old-fashioned system outsiders hardly ever get to see, aside from the press release that later announces a deal happened.

But something recently changed. Capital markets, at least a corner of it, is being democratized. That became obvious when someone told me I could lend a hundred bucks toward a warehouse line of credit for Credibly just to see it for myself.

Me? Somehow involved in a warehouse line for Credibly???

On May 5, Credibly announced a strategic partnership with Figure to “modernize SMB capital markets via blockchain rails.” It sounds like a buzzwordy headline from the 2010s. Not AI, blockchain. In 2026. Though there are certainly AI technologies involved.

Figure is a familiar name, not only because it is publicly traded, but also because I had the honor of sharing a stage with Figure CEO Michael Tannenbaum last fall at the B2B Finance Expo in Las Vegas for a fireside chat. While I mainly asked him about how small business owners could leverage their home equity to obtain capital, Tannenbaum pivoted at moments to explain how the company was reshaping capital markets by using blockchain. At the time, some of it went over my head.

“Everybody else is trying to use an origination system, and then on the back end figure out where to sell the loan,” said Tannenbaum on Peter Renton’s recently released Fintech One-on-One podcast, “and that figuring out process creates all this back and forth between the lender, the borrower, and the ultimate buyer, and we eliminated that, and we eliminated the people-based approach and standardized it.”

In a nutshell, Figure being in the mortgage game meant it was inevitably tied up in the capital markets game. And they found the capital markets game very old-fashioned. So they made their own capital markets marketplace, with one segment called Democratized Prime, and built it on blockchain rails.

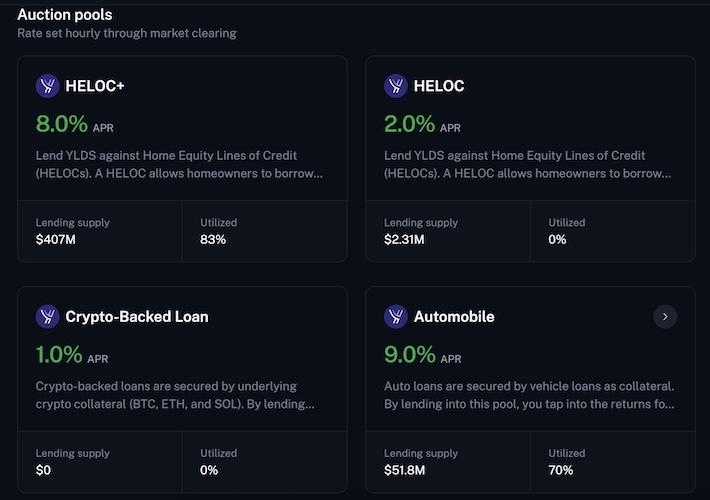

Democratized Prime is essentially like a universal warehouse line, one that is “much easier to borrow and lend against than the arduous process of getting a warehouse line with lots of third-party diligence and legal fees,” Tannenbaum told Renton. It has rapidly become popular for mortgages. If you signed up for the platform today, you would see HELOC pools and their corresponding credit profiles that you could lend against.

Mortgages were just the start. You can also lend against an auto loan pool brought on by Agora. That deal was announced this past February as a landmark moment that kicked off the democratization of new asset classes. Credibly will bring SMBs into the mix next, where the company’s small business loans and revenue-based financing deals will be pooled up and available to lend against with as little as $10 at a time. That means this opportunity is open to just about anybody.

The yield can be determined in one of two ways. One is a Dutch auction, where participants compete to lend into the pool by offering lower rates, which is good for Credibly as the number goes down. If you bid too high or the pool is full, you may have to wait until the next hourly auction to try again. The process resets each hour, with the lowest acceptable bids getting priority, meaning lenders are not just deciding whether they want exposure to the pool, they are also competing on price for the right to put their money to work. The other is a live-rate system where rates change automatically based on utilization. You can exit an auction pool if your funds are not in use or if someone else’s funds are ready to replace yours. For live rates, you can request an exit up to the available liquidity at the time. Credibly is not on the Democratized Prime system just yet. That is supposed to happen this quarter. But HELOC and auto loan pools are already there.

I first tried the platform myself with just a couple hundred bucks. I entered digits into an auction-pool form indicating that I’d be willing to lend at 7.9% APR all-in to a HELOC pool. The pool wasn’t taking any offers for higher than 8% so that’s how I came up with my figure. My funds were accepted, and they’re now earning a return. Not in some magic back room, but visibly on the blockchain.

While you can obviously fund your account with dollars, I dusted off an old stockpile of ETH and sent funds using MetaMask to Figure Markets. Therein lies the only caveat. To lend against the pools, you have to use Figure’s stablecoin, YLDS.

YLDS is an SEC-registered security. It is pegged 1:1 with the U.S. dollar and also earns a return on its own just for holding it, a little over 3% at the time of this writing. Users use their YLDS to lend against the pools and are paid their interest in YLDS (hourly!). This can be swapped back into dollars, Bitcoin, or whatever else one is comfortable with.

YLDS is an SEC-registered security. It is pegged 1:1 with the U.S. dollar and also earns a return on its own just for holding it, a little over 3% at the time of this writing. Users use their YLDS to lend against the pools and are paid their interest in YLDS (hourly!). This can be swapped back into dollars, Bitcoin, or whatever else one is comfortable with.

YLDS exists on the Provenance blockchain. You’re assigned a wallet address, and you can trace where your funds went using Provenance’s main block explorer, ZoneScan. That also lets you see a bit of what other users are doing, as well as what Figure is doing. By being on blockchain rails, everything is kind of out there for audit and inspection. I saw my ETH get swapped for YLDS on the block explorer and then saw my funds interact with a corresponding HELOC pool smart contract.

If you think this blockchain stuff is still niche, consider that in 2025, stablecoins processed $28 trillion in real economic volume, according to Chainalysis. By 2035, that number could reach $1.5 quadrillion, surpassing today’s entire cross-border payments market. Those are eye-popping numbers, but even if one discounts the forecast, the broader point is hard to ignore: stablecoins are no longer a fringe experiment.

Of course, this is not risk-free just because it is transparent. Pool performance still matters. Borrower credit quality still matters. Liquidity may depend on whether other participants are ready to replace your funds. And because YLDS is itself a security, participants need to understand what they are holding, how it works, and what risks come with using it. The blockchain may make the mechanics easier to inspect, but it does not make credit risk disappear.

While Democratized Prime can make it easier for lenders to tap into capital, this also is not a solution for everyone. Credibly, for example, has provided access to over $3 billion in working capital to more than 61,000 small businesses, with four completed KBRA-rated securitizations, its most recent one completed in the first quarter of 2026 for $124 million, expandable up to $225 million. That is sort of the baseline quality: true institutional-level assets from an institutional-tier lender. A small funder looking to graduate away from syndication is not going to be an immediate candidate for something like this. One of the HELOC loan pools, for example, has taken in $340M from parties looking to lend their YLDS.

One benefit for Credibly in challenging traditional finance ABS markets and adopting this technology is that greater efficiency and reduced friction should ultimately enable the company to pass savings on to its small business customers.

Would you lend a million dollars against a Credibly business loan and revenue-based financing pool? Before now, you probably wouldn’t ever have had that opportunity. Now Figure is making that possible.

QuickBooks Capital: ~$1.7B Funded Last Quarter, Repeats that AI is Not a Threat, But Rather an Advantage

May 21, 2026 Intuit’s QuickBooks’s capital originated about $1.7B in small business loans in Q3 FY 2026. That brings the total for the trailing nine month period ending April 30 to $4.3B. During the earnings call, Intuit CEO Sasan Goodarzi said “We are growing our line of credit offerings with buy now, pay later, directly embedded within QuickBooks, and the launch of Intuit business credit card.”

Intuit’s QuickBooks’s capital originated about $1.7B in small business loans in Q3 FY 2026. That brings the total for the trailing nine month period ending April 30 to $4.3B. During the earnings call, Intuit CEO Sasan Goodarzi said “We are growing our line of credit offerings with buy now, pay later, directly embedded within QuickBooks, and the launch of Intuit business credit card.”

Like other software companies, analysts have been questioning the sustainability of their product offerings as AI looms large as a threat. Like the previous quarter, Goodarzi offered a rebuttal on this subject, expressing that they are effectively the AI solution customers would seek.

“It is important to recognize that businesses, while they use Google, they use LLMs to do searches, do queries, you cannot run your business with an LLM because you are managing your books, you are managing your money, you are managing your payroll, and accuracy and compliance of doing that matters,” Goodarzi said. “And running a business is mission critical. And so psyche of businesses is such that and accountants is that they need us to be their AI platform to provide expertise so they can run and grow their business.” Goodarzi cited Anthropic and OpenAI as partners they are already working with, for example.

Goodarzi also said that winning customers is not necessarily about the best software anyway, but rather about the confidence the assistance with the work instills in the customer. And given the integrations they have, the reputation they have, the AI power that they use, and ability to assist customers, this is where they are actually structurally advantaged.

Barney Frank Once Answered My Question About Business Loans

May 20, 2026 Former Congressman Barney Frank has died. He was 86 years-old. While he left Congress in January 2013, his legacy has lived on through the Dodd-Frank Act of 2010. Readers may recall that’s the law that gave birth to the Consumer Financial Protection Bureau and with that a debate that has spanned more than 15 years over how to implement its small business loan data collection mandate.

Former Congressman Barney Frank has died. He was 86 years-old. While he left Congress in January 2013, his legacy has lived on through the Dodd-Frank Act of 2010. Readers may recall that’s the law that gave birth to the Consumer Financial Protection Bureau and with that a debate that has spanned more than 15 years over how to implement its small business loan data collection mandate.

In any case, I once personally crossed paths with Congressman Frank in a hallway at the Exponential Finance Conference presented by Singularity University and CNBC. It was in 2014 and I had official press credentials. I had limited time so I fired away the first question I could think of and that was “would you be in favor of a federal maximum cap on business loan interest rates?” He said that he would not be.

Talking further about this subject, Frank went on to say that he supported transparency in business loan transactions, such that the borrower should be easily able to identify the terms, but that the premise behind consumer loan protections was that consumers were less sophisticated.

In a second question, I brought up overdraft fees and their tendency to be characterized by critics as short-term loans. Should a loan term of just a single day be required to disclose an annual percentage rate? He believed that they should.

This exchange and a summary of topics discussed at the conference appeared in the July/August 2014 issue of DailyFunder’s periodic trade journal. RIP Congressman Frank.

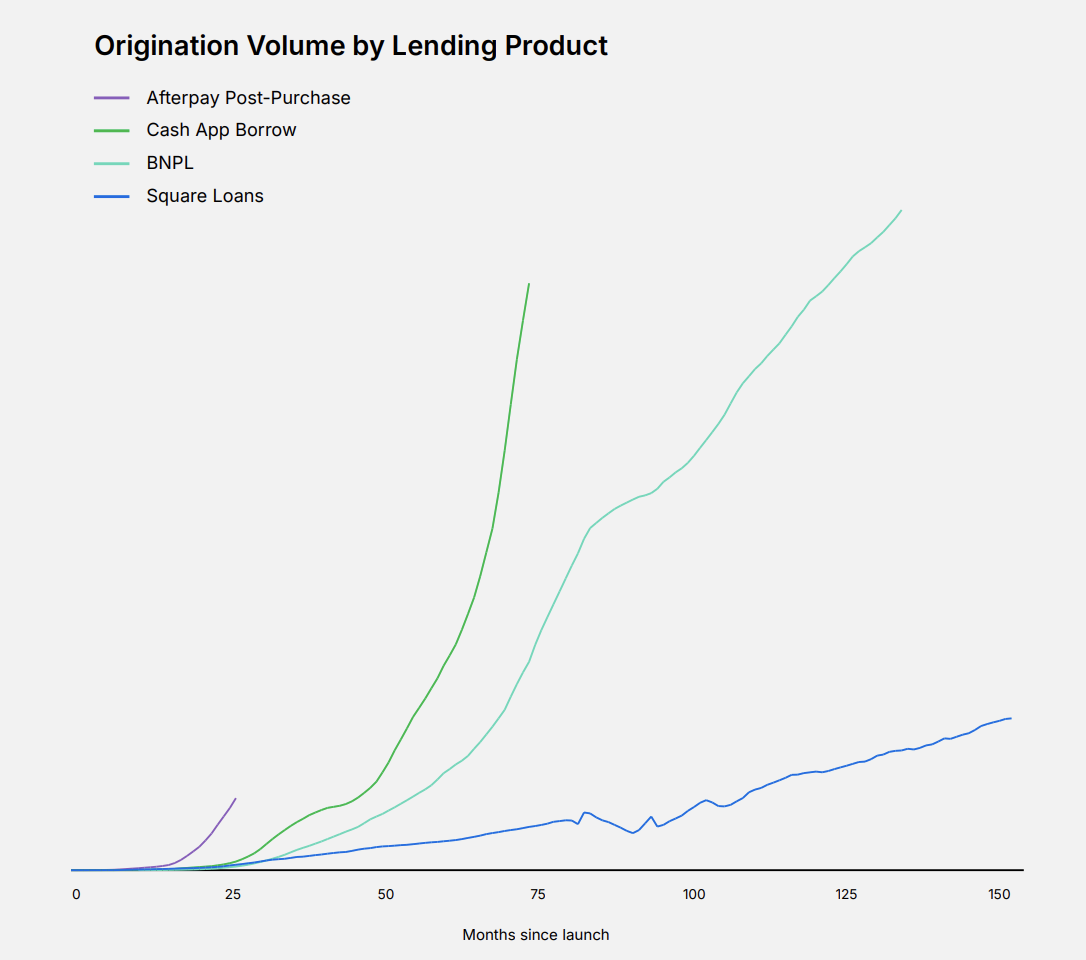

Square’s Q1 Gross Profit Growth Driven by Square Loans

May 12, 2026Block didn’t divulge the precise number of business loans it originated in Q1 2026 but did say that it grew. deBanked, which tracks online small business lender originations, estimates the number to be ~$1.9B.

“Square gross profit grew 9% year over year in the first quarter, driven primarily by Financial Solutions, most notably Square Loans,” the company said.

Lending has become a significant business for the company across all of its verticals. Consumer lending origination volume growth accelerated to 82% YoY, for example. Its “Borrow” product grew by 300% over that time period.

“Each new Block lending product has scaled originations at a faster rate than the last one,” the company revealed in its earnings presentation. A snapshot from that presentation is below: