|  |  |

Related Videos

Episode 25 - The Roosevelt Hotel | Deal or No Deal: What's Ahead For Brokers |

deBanked TV Live 3/23 - Full | Jared Weitz Talks SMB Finance |

Stories

United Capital Source CEO Jared Weitz Discusses The State of Small Business Finance

September 24, 2020Jared Weitz, the CEO of United Capital Source, recently sat down (virtually) for an interview with me to discuss the state of small business finance. During it, Weitz makes an alarming prediction, that pandemic related events will lead to 50% of all restaurants permanently closing. You can watch our full talk below:

United Capital Source CEO Jared Weitz Appeared on Fox News

April 21, 2020This week, Jared Weitz, CEO of United Capital Source, appeared on Fox News to talk about the PPP, EIDL, and small business lending. Video below:

Bizfi Alum Jared Weitz Reflects on Demise of Former Employer and Rise of UCS

October 9, 2017Jared Weitz has come a long way since his earlier days as one of the original Bizfi employees. Today he’s at the helm of online funding marketplace United Capital Source (UCS), which has been on a tear since deBanked last spoke with Weitz a couple of years ago. The UCS founder and chief executive took some time to revisit with us about having to painfully watch the demise of his former employer, which is where he cut his teeth in this business, and the rise of his own company UCS as a funding marketplace.

In some ways, the more things change the more they stay the same. Since the last time Weitz spoke with us, the company’s location remains in the heart of Times Square in New York, and UCS has grown its staff by only four people including two sales reps. What has changed, however, is the amount of funding that the company has done and the size of the average transaction, all of which have blossomed.

“When we first spoke a few years ago we were doing $8 million to $10 million a month in funding volume. Now we are doing between $14 million and $16 million per month,” said Weitz.

He added that where the company differentiates itself is that while a few years ago the products they were selling were predominately in the sub-prime space now they sell other products, which allows merchants to “swim upstream” when they qualify for that.

The result has been bolstered partnerships and product offerings and an average loan size that has jumped from $30,000 to $40,000 per deal to a range of $500,000 to $2 million.

“We opened up the funnel to the kind of relationships we’re able to broker and the kinds of financings we’re able to offer. We’re playing in the field of SBAs, account receivables financing, lines of credit and asset backed loans. By offering these products our volume has jumped significantly and allowed us to talk to different referral partners.”

UCS does all of its own marketing and generates leads for their in-house sales reps. Those sales reps take a file from open to close and they analyze the small business owner’s needs on a consultative call.

“We understand their business and their pain points. The first question we ask isn’t how much do you need but what’s paining you in your business today that we can help you with?”

One such business owner recounted his experience with UCS to deBanked, saying that traditional banks were “an absolute pain” to secure funding. He spoke of the “very stressful” and time-consuming process of applying for a loan, saying he doesn’t have time to “jump through a million hoops to get a loan.”

“When I was initially looking to curb my temporary cash flow problem, I searched online for the best alternatives to traditional bank loans. I read all the reviews on companies and decided to call UCS,” the business owner told deBanked, adding that he’s been a UCS repeat customer for a number of years and is especially fond of the ease at which the process is completed.

“I could literally call Jared today and have six figures in my account tomorrow. The best part is the pay back process. They only take funds when I run credit card transactions. So, in my slow months, I don’t have to stress and worry about repaying the loan. UCS is a perfect fit for me,” the business owner said.

Eye Opener

As the seventh or eighth employee of Bizfi, Weitz really has been part of the evolution of online funding. He says the rise and fall of Bizfi has been an “eye opener” for him.

“It caused a bunch of funding companies to be a little gun shy when it comes to funding. I told my guys this too shall pass. People are shaken and wondering if it’s a larger global issue. Thankfully it’s not a global issue. There are plenty of funding companies that are well backed that are still funding. My group is well able to pick it back up. We have signed up with more funding companies to increase our offerings and make sure we have no concentration issues,” said Weitz.

And although he left the company to eventually launch UCS, which has proven to be a prudent move, he has nothing but respect for his former employer.

“My history there is very deep and I’ve got a genuine love for the founders of the company. It’s where I cut my teeth. I was really sad the day I heard they’re not funding anymore.”

In fact, Bizfi was one of the funders that UCS counted among its partners.

“We had a good book there. We started to see problems and began to shift where our new business was going. Thankfully it didn’t affect me. But it showed me that you should sign up with more funding companies. If you think the mix should be X go 50% more and be super cautious. This approach has worked out for us,” he said.

Weitz has advice for other funders that might be looking to grow at lightning speed.

“Someone that’s growing so fast while they’re also innovating and looking to close larger transactions that bring them to a bigger place – that’s hard to do all at once. Driving at 200 MPH either works out well and takes you to the finish line or it doesn’t work out really well. It’s really unfortunate that it didn’t work out for them.”

Deal Competition

Deal Competition

For its part, UCS competes with the likes of LendingTree and other online marketplaces, but that seems only to add an ounce of perspective to Weitz and the UCS team, driving them to adjust and remain nimble so that they can get the next deal.

“Healthy competition is good for us. We welcome anything like that. Some of my best learning experiences have been when we were beat out on a deal. I call the merchant personally and say hey, who gave you the deal? Honestly, I want to sign up with them and offer those rates to my clients. We form a friendship with both the funder and the small businesses,” he said.

UCS also counts some high-profile funders among its partners.

“We’ve worked with some funders forever and it’s been great. But we really had to also find folks that offer certain products but at a cheaper rate,” said Weitz, pointing to the scenario of a merchant having a few of those loans under their belt and improved credit as a result. “They are being solicited by depository banks and can qualify for that rate. We don’t want to lose the relationship. My thought process is sign up with similar folks with that product and when the time comes we can swim the merchant upstream.”

For instance, not all funders offer SBA loans but UCS has been doing so for the past two years. “It’s really kind of taken off for us over the last year. The same thing with accounts receivable and future order financing.”

UCS acts as both a broker and investor in their own deals, so they have a vested interest in the underwriting standards. “Investing with some of our funding partners on the syndication side allows us to have buying power and to take an actual interest in the merchant we’re dealing with,” said Weitz, adding that UCS takes a hybrid approach offering both a fully automated underwriting process for those merchants who want it but also having the capability to talk to the business owners, which is what the large majority of business owners prefer.

Meet the Source: How Jared Weitz and United Capital Source became one of the industry’s fastest growing shops

October 23, 2015Jared Weitz came from humble beginnings and nearly settled for a humble fate. But associates say an ordinary, uneventful life wouldn’t have suited him – he works too hard and figures things out too quickly.

Almost ten years ago Weitz, 33, was parking cars to earn money for community college. After finishing at St. Johns University, he almost made plumbing his career. But now he’s CEO of United Capital Source LLC, an alternative-finance brokerage with deal flow of between $9 million and $10 million a month and an annual growth rate of over 65 percent.

Business associates, former bosses and his small cadre of employees all seem to revere Weitz for his honesty and straightforwardness. They consider him a personal friend. They say he continues to grow as a businessman and as a human being while taking pleasure in helping others do the same.

Geographically, Weitz has the good fortune to know where he belongs – the city of New York is in his DNA. “Every time I fly back,” he said, “I’m so happy to land.”

His love affair with the city began in Brooklyn. He was born there and raised in a Brighton Beach apartment in the shadow of Coney Island. When he was 16, the family moved to Oceanside on Long Island.

As the second of six children, Weitz had to come up with the money for college on his own. “My older sister and I had to pay our way,” he said. “Everybody else, my dad was able to cover.” He started school at Nassau Community College, selling cell phones and parking cars at night.

But then came an abrupt change. Once Weitz saved enough money, he transferred to Tulane University in New Orleans to pursue a relationship with a woman who was finishing her studies there. He attended classes part-time, worked as the athletic director at the Jewish Community Center, tended bar in a Mexican restaurant and served summonses for a law firm.

But then came an abrupt change. Once Weitz saved enough money, he transferred to Tulane University in New Orleans to pursue a relationship with a woman who was finishing her studies there. He attended classes part-time, worked as the athletic director at the Jewish Community Center, tended bar in a Mexican restaurant and served summonses for a law firm.

The relationship with the woman fizzled, but Weitz made lasting friendships during his days down south. His old roommate in New Orleans, who now practices law in Atlanta, serves as counsel for United Capital Source.

When Weitz had been in New Orleans for two years, Hurricane Katrina struck. He evacuated to Houston, where he stayed in a Holiday Inn for two weeks before realizing he wouldn’t be able to return to southern Louisiana anytime soon. The magnitude of the devastation was just too great.

Shouldering the duffel bag of belongings he had managed to pack on his back during the evacuation, he returned to New York, enrolled in St. John’s University and began working in sales for Honda Financial Services and parking cars.

Weitz had started school expecting to become a teacher. He had grown up with younger siblings and liked leadership roles, which convinced him teaching would be a good fit.

Still, many of his college jobs had required him to sell. As a bartender, for example, he promoted drink specials. As an athletic director he convinced people to sign up for classes. “Everything that I took to naturally wound up being in the sales, marketing and finance arena,” Weitz observed.

When he was nearly finished at St. John’s, Weitz was parking a car for an acquaintance who offered him a job as a union plumber. Suddenly, he was making $27 an hour and had health benefits. “It was a big breather for me,” Weitz recalled.

He quit his three jobs and labored as a plumber from 7 a.m. to 3 p.m. School started at 3:30 p.m. for him and stretched into the evening. But when he finished his degree, working as a teacher for $35,000 to $40,000 a year no longer seemed attractive.

Besides, his plumbing work didn’t center on toilets. On typical commercial plumbing jobs he did things like install air, medical and gas lines in hospitals. He was reading blueprints and bidding for jobs. A promotion to foreman didn’t seem that far off.

At about the same time, near the end of 2006, a friend, Mike Caronna, landed a job at Bizfi, formerly known as Merchant Cash and Capital (MCC), The company, which had just started and had only a few employees, was looking for underwriters.

As fate would have it, Weitz fell into a conversation with a fellow union plumber, one who had been on the job for 30 years. The older man reminded him that his wages would never climb much higher than they were right now. The veteran plumber then showed the younger man his hands, bent from decades of holding tools. “That got me thinking,” Weitz said.

He asked his friend Caronna to arrange a job interview at MCC. He got an offer and took a 90-day leave from his plumbing job to give the world of finance a try. “After about two weeks, I knew it was for me,” he said of the alternative-finance industry. It was by then the beginning of 2007.

Weitz excelled as an underwriter, and the company CEO, Stephen Sheinbaum, picked him and four others for a sales contest. Sheinbaum gave them some leads and turned them loose. Weitz won the competition but asked his boss to help him gain experience in business development and operations before taking on a sales position.

Sheinbaum was happy to comply. “He is one of the best and the brightest in the space,” he said of Weitz.

So, at age 25, Weitz found himself building a business development department by cultivating relationships with ISOs and persuading them to send business to MCC. “It was amazing,” he said of those days. “That was a big opportunity.”

Weitz learned the mechanics of the business. He found that the right ISO can originate good deals and a bad ISO can ruin deals. He learned the politics of when to talk, when to remain silent and when to let someone vent.

Then Weitz and a good friend at MCC, Anthony Giuliano – who’s now managing partner of Sure Payment Solutions – worked out how they could improve the MCC sales effort. They pitched Sheinbaum on the idea of having a second internal sale force, and that led to the birth of Next Level Funding (NLF), a division of MCC.

Weitz and Giuliano each owned 10 percent of NLF, and MCC owned 80 percent. “I’m 26, about to be 27, and I’m like, ‘You did it, Man,’” Weitz said as he looked back.

After about four months, NLF absorbed MCC’s original sales division. Next, Giuliano and another executive, Paul Giuffrida, decided to leave MCC. Weitz felt torn. He felt an allegiance to Giuliano and respected Giuliano’s knowledge of programming – a subject that was alien to him. Yet Sheinbaum had provided Weitz a series of opportunities.

Weitz stayed at MCC but felt he deserved to become chief sales officer. When that didn’t happen, he sold his shares back to the company at a dramatically reduced price to extricate himself from a non-compete clause and set off to start United Capital Source (UCS).

With a five-figure investment, Weitz and his then partner, started UCS in January of 2011 in a 250-square-foot office in Long Beach, L.I. Weitz invested about 90 percent of the money he had saved while working at MCC.

Jon Baum left NLF with Weitz and became the first UCS employee. Within a week or two, Danielle Rivelli, left NLF to join UCS, and Weitz put the remaining 10 percent of his savings into the business to meet the expanded payroll. Today, Baum and Rivelli are UCS sales managers.

The first month UCS was open, it funded $240,000 in deals. “It just felt good to be on my own and start funding deals,” Weitz said. From the beginning of UCS, he won praise from funders for bringing them the right kind of deals with merchants who were likely to repay.

“He really has the pulse of the marketplace and what a lender is looking for,” said Todd Sherer, who handles business development for Entrepreneur Growth Capital. “He doesn’t waste time giving you transactions that don’t fit in your box.”

That’s because doing things right means a lot to Weitz. “He is one of the most straightforward, honest, high-integrity people I have met in the industry,” said Steven Mandis, adjunct associate professor at the Columbia University Business School and chairman of Kalamata Capital LLC.

He’s won the OnDeck seal of approval. “OnDeck has a rigorous and extensive background check process as part of our broker certification process,” said Paul Rosen, OnDeck’s chief sales officer. “Jared Weitz and United Capital have passed our screens and process and are currently active brokers for OnDeck.”

And with time, Weitz has learned patience. He was sometimes short with funders when he started his company but has matured into a pleasant person to deal with, said Heather Francis, CEO of Elevate Funding. “I’ve seen that growth with him,” she said.

All of those good qualities soon came together to help UCS succeed. Within four months of its launch, the company rented a 1,500-square-foot office in Garden City and hired two more people. Next came a 3,200-square-foot office in Rockville Centre and three more employees.

“The company was growing and gaining traction,” Weitz recalled. “I bought out my original partner.” Since then, Vincent Pappalardo has invested in UCS and become a minority partner.

Meanwhile, the lease was expiring on Long Island, and Weitz felt the time had come to move to Manhattan. That would enable the company to draw employees from throughout the region and not just Long Island.

“We decided to bite the bullet and pay the excess money to move to the city because we believed it would be better for the business,” Weitz said. He added two people and rented a 5,500-square-foot space near Penn Station in the Garment District in September of 2014.

Within three months of making the move to Manhattan, business doubled. “Being in a faster-paced environment caused the business to go through another growth phase,” he said. After nine months in the city, UCS is now taking over a whole 8,500-square-foot floor of the same building.

Within three months of making the move to Manhattan, business doubled. “Being in a faster-paced environment caused the business to go through another growth phase,” he said. After nine months in the city, UCS is now taking over a whole 8,500-square-foot floor of the same building.

UCS remains a small shop in terms of headcount with 21 people, but the company’s funding numbers equal the output of many brokerages five times its size. Twelve of the UCS employees work in sales, with the others engaged mainly in underwriting, operations and customer service.

Less than 2 percent of UCS’s funding volume comes from broker business. “We self-generate all of our business,” Weitz said, declining to elaborate too much on his company’s marketing efforts.

“My salespeople – bar none – are the best in the industry,” he claimed. “Much like the Navy has the SEALS and the Army has the Rangers, there are groups in the industry that can do triple or quadruple what other people do because that’s just the way they are.” His people fund an average of $750,000 per month per person in new business, while his renewals reps fund well into the 7-figure range per person.

UCS salespeople achieve their results because they have detailed knowledge of the industry, Weitz said. The staff’s understanding of alternative finance doesn’t end with sales but also includes underwriting and finance, he noted. “That’s what makes you a very good and knowledgeable sales rep,” he maintained.

His salespeople don’t just tell a client what he or she wants to hear. They take the time to understand the client’s financial situation. “They know how to read a profit and loss statement, a balance sheet and tax returns,” Weitz said.

ARE THE BEST IN THE INDUSTRY”

While 90% of Weitz’s sales team has a college degree, most of the salespeople have come from outside the industry, he said, noting that one was with Sleepy’s, the mattress company. Another was selling memberships at a gym, one worked for a credit card processing company, two were barbers and one had just graduated from college.

UCS doesn’t make double-digit commissions because the company isn’t over-charging merchants, Weitz maintained. The company does not obtain excess funding that a customer can’t afford or increase the factor rate to dangerous levels, he noted.

“You’re not really helping the merchant” by providing too much capital, Weitz asserted. “You’re sucking the blood out of him before he goes away. That’s not why I’m in business.”

A clean record will also prove beneficial when federal regulation comes to the industry, he said. Integrity in the workplace can also spill over into other parts of a person’s life, Weitz believes.

As UCS grew larger and Weitz grew older, he saw his employees rent their first apartments and then buy their first homes. He learned then that he had taken on more responsibility than was apparent to him at first.

As UCS grew larger and Weitz grew older, he saw his employees rent their first apartments and then buy their first homes. He learned then that he had taken on more responsibility than was apparent to him at first.

To accommodate the employees he added a human relations department and commissioned a company handbook. He’s also started marketing, finance, operations and other departments.

He’s lost only four employees because he pays them well, respects their time and doesn’t view their youth as a liability.

Meanwhile, talking daily to merchants and hearing about their heartaches and triumphs has humbled and matured Weitz. Seeing how the merchants’ choices panned out or fell short also shaped him and helped him grow up a little, he said.

Weitz has found time in his 70-hour workweek to meet his future bride. They’re planning to wed next year, and he plans to invite his entire staff. “It wouldn’t feel right without them,” he said.

Weitz has skipped the Ferrari, Rolls Royce and mansion because he didn’t feel he needed them. But even without those status symbols, it’s clear that Weitz has avoided settling for a humble fate.

As for what comes next, UCS is said to be developing an online marketplace to take their business to the next level, though Weitz declined to provide specific details about how it will work. “We’re on pace to do more than $100 million worth of deals a year,” Weitz said. “And as far as we’ve come, I feel like this is still just the beginning.”

United Capital Source CEO Jared Weitz is deBanked’s September / October Cover

October 10, 2015Jared Weitz came from humble beginnings and nearly settled for a humble fate. But associates say an ordinary, uneventful life wouldn’t have suited him – he works too hard and figures things out too quickly.

Almost ten years ago Weitz, 33, was parking cars to earn money for community college. After finishing at St. Johns University, he almost made plumbing his career. But now he’s CEO of United Capital Source LLC, an alternative-finance brokerage with deal flow of between $9 million and $10 million a month and an annual growth rate of over 65 percent.

Business associates, former bosses and his small cadre of employees all seem to revere Weitz for his honesty and straightforwardness. They consider him a personal friend. They say he continues to grow as a businessman and as a human being while taking pleasure in helping others do the same.

Geographically, Weitz has the good fortune to know where he belongs – the city of New York is in his DNA. “Every time I fly back,” he said, “I’m so happy to land.” His love affair with the city began in Brooklyn. He was born there and raised in a Brighton Beach apartment in the shadow of Coney Island. When he was 16, the family moved to Oceanside on Long Island.

As the second of six children, Weitz had to come up with the money for college on his own…

To read the FULL 4-page exclusive, you’ll need to subscribe to deBanked!

In this September/October issue, payments and finance journalist Ed McKinley explored the story behind United Capital Source, one of the industry’s fastest growing shops and what it took for its 33-year old CEO to get there.

—

For current subscribers, this edition will be dropped in the mail on Tuesday the 13th. deBanked’s Sean Murray will have a limited amount of extra copies with him at Lend360 in Atlanta and Money2020 in Las Vegas if you’re interested to get your hands on one in person.

Navigating SBA Lending at B2B Finance Expo

August 21, 2024Looking to do more in SBA lending? Make sure you attend this panel of SBA lending professionals at B2B Finance Expo, taking place on Day 1 of the conference on September 23!

Moderated by Bob Coleman of the Coleman Report, this discussion will feature Carissa Sousa, Adam Seery, Jared Weitz, and Ryan Baderian.

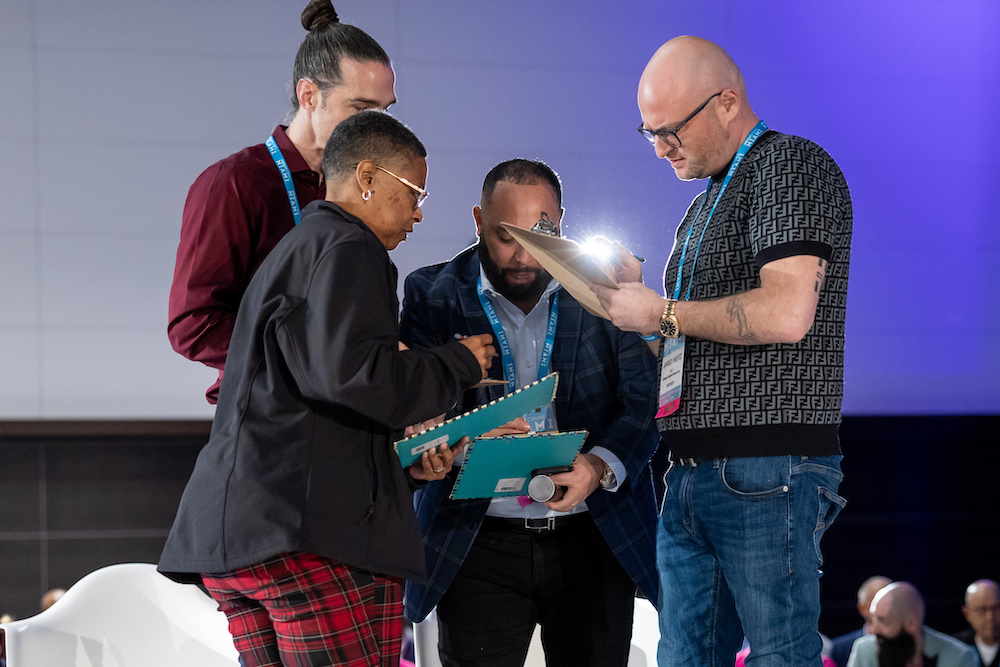

Broker Battle Finds a Champion

January 14, 2024At the Miami Beach Convention Center in Miami Beach, Florida, thousands of viewers packed a hall to witness the first ever Broker Battle™ at deBanked CONNECT. After the rules of the competition were explained, six broker contestants waited eagerly for their turn to face four judges and with that a chance to win a grand prize of $5,000. Their goal? Choose from one of three pre-defined sales scenarios and show off their knowledge and abilities to the judges. Here’s what happened:

The Broker Battle was introduced

Broker Battle judge Daniel Dames (Bitty Advance) held up a Title belt

Irving Betesh (Advance Funds Network) had the distinction of going first. He came prepared!

The contestants continued one by one alphabetically by last name

The conversational role playing on the stage covered the gamut, ranging from explaining APRs and contract terminology to diagnosing customer needs or trying to earn a customer’s business. Below, judges Jared Weitz (United Capital Source) and Cheryl Tibbs (Equipment LeaseCo Inc) listen in to a contestant’s pitch.

Mike Brooks (Best Connect Capital) came in with his own style

Corey Digi (Lexington Capital Group) put up a strong showing

Stanley Mitchell (CLM Financial) goes to work

Danielle Rivelli (United Capital Source) showed off her experience

Anthony Truglia (CapFront) made it known the competition wasn’t over yet

The judges had to add up their scores for each contestant to find out which TWO would make it into the final championship battle

Second from the right is judge Leo Vargas (Triton Recovery Group).

Anthony Truglia and Danielle Rivelli are declared the two finalists after racking up the highest scores

The final sales scenario is revealed!

Both contestants have to compete on stage at the same time! Oh my!

The contestants are sent offstage so the judges can deliberate

And the winner is…

Anthony Truglia!

All photos from the Broker Battle here

All photos from the rest of deBanked CONNECT MIAMI here

deBanked would like to thank all of the amazing broker contestants for participating in something bold and brand new. Thank you to Anthony Truglia, Danielle Rivelli, Corey Digi, Irving Betesh, Stanley Mitchell, and Mike Brooks. Gratitude is also directed towards the judges for their efforts, Cheryl Tibbs, Daniel Dames, Jared Weitz, and Leo Vargas.

deBanked hopes that this competition inspires all brokers to become better, to further master their knowledge of available products, legal compliance, style, and confidence. A video highlight reel of the competition is in post-production.

Interested in more from deBanked? Contact us at info@debanked.com or call 212-220-9084.

ERC And The Broker Relationship

January 11, 2023 Like many business loan brokerage CEOs across the US, Jared Weitz is familiar with the Employee Retention Credit (ERC). His company, United Capital Source (UCS), which in 2021 surpassed $1B in small business financing volume, regularly speaks to thousands of small business owners. Weitz told deBanked that through his own experience most business owners have become sufficiently aware of the ERC as well. That in turn raises the question of what role a company like UCS can play in the ERC process.

Like many business loan brokerage CEOs across the US, Jared Weitz is familiar with the Employee Retention Credit (ERC). His company, United Capital Source (UCS), which in 2021 surpassed $1B in small business financing volume, regularly speaks to thousands of small business owners. Weitz told deBanked that through his own experience most business owners have become sufficiently aware of the ERC as well. That in turn raises the question of what role a company like UCS can play in the ERC process.

“We have a few different referral partners that are lending against those credits,” Weitz said. “And that’s what we’re doing.”

In that regard, UCS is doing what it is already used to doing, connecting the business owner with a compatible source of funding. While other brokers may attempt to generate fees by assisting businesses with filing for the tax credits themselves, Weitz said he prefers to avoid the headache and/or potential liability that can come along with doing that.

“We’re able to get 100% of what a client is owed right up front,” Weitz said. “They can either have an interest-only program or a no-payments program for 12 months, and then after 12 months there would be a factor rate attached to the program that would be paid back weekly.”

UCS earns a commission when a deal goes through but ERC has not by any means become a primary driver of business, according to Weitz. Rather, it’s something that could come up during a customer consultation.

“When we’re peeling back the layers and chatting with the client on why they need funds, if they say ‘well, actually I’m falling short here and I also just filed for [the ERC] and I’m still waiting for that,’ it can be one of the options that we offer them […] and we’ll just see what they qualify for and if they’re interested in it.”

It’s the waiting part that is creating a cottage industry around ERC. Weitz says he hasn’t heard of any business getting an ERC refund in less than 7 or 8 months and he is aware of at least one business that is still waiting for it 2 years later since filing. But just because most businesses are aware of the ERC doesn’t mean they’ve all actively pursued it. On this, UCS simply offers free helpful advice.

It’s the waiting part that is creating a cottage industry around ERC. Weitz says he hasn’t heard of any business getting an ERC refund in less than 7 or 8 months and he is aware of at least one business that is still waiting for it 2 years later since filing. But just because most businesses are aware of the ERC doesn’t mean they’ve all actively pursued it. On this, UCS simply offers free helpful advice.

“What I would say to them is ‘hey, heads up, you should probably look into this with your local accountant and payroll company, make sure you get your tax attorney or your accounting firm’s attorney involved just to make sure you’re doing it the right way.'”

Putting business owners on that path of pursuit, informing them of its existence and advising them to seek out qualified counsel to assist with it, generates no revenue to UCS, but Weitz thinks it’s important to help business owners in any way possible.

“I think it does build a bridge of trust a bit more between you and your clients because you’re showing them that you’re not solely looking at products that are beneficial to you, and you shouldn’t be doing that anyway,” Weitz said. “But I think when you’re dealing with someone there’s always that thought in their head, right? And so this has helped solidify that you’re not.”

The Way of the Funding Pro... jared weitz in the article., , , , its all about the customer experience., , , , what does that really mean?, , , , hubspots 2016 sales experience survey found these results when asking what can sales reps do to make their experience positive?, , , , 69% listens to my needs, , , , 61% is not pushy, , , , 61% provides relevant information, , , , 51% responds or gives information in a timely manner, , , , 49% provides a range of options even byond his/her business offering, , , , 45% cares about the success of my business project, , , , 37% details the ways s/he can help me succeed, , , , what have you found to be effective for being that trusted advisor to your clients?, , , , -fundingstrategist, , https://fundingstrat.com, , https://fundingstrat.com/the-way-of-the-funding-pro/... |

See Post... jared weitz is not only the chairman of the small business finance council (sbfc), but has also been an active participant within nearly every industry tradeshow and event. he is a known and respected figure within the space, with a firm producing around $2... |

See Post... jared weitz is not only the chairman of the small business finance council (sbfc), but has also been an active participant within nearly every industry tradeshow and event. he is a known and respected figure within the space, with a firm producing around $2... |