Business Lending

Are Your Sales Agents or ISOs Up to Snuff? (Take Our Research Survey)

August 12, 2015If you enjoy reading deBanked’s articles, please take the time to take our short survey:

Some background:

What started as a few sensational articles about practices in small business lending and merchant cash advance is now turning into a cry for a governmental crackdown by not only observers outside the industry but lenders from inside the industry itself.

Stories that look like they’ve been written by consumer activist groups are being penned by your peers. Just recently, Fundera’s Brayden McCarthy submitted his thoughts to American Banker and the Huffington Post.

Stories that look like they’ve been written by consumer activist groups are being penned by your peers. Just recently, Fundera’s Brayden McCarthy submitted his thoughts to American Banker and the Huffington Post.

“As evidence,” he wrote. “One need only look to some lenders’ triple-digit interest rates, the proliferation of shady loan brokers and inadequate or nonexistent disclosure of price and terms. Some practices, such as brokers that brand themselves as impartial but take incentives to market certain lenders over others, resemble behavior seen in the run-up to the financial crisis.”

Along with the Treasury’s RFI, there is a mass lobbying effort to regulate the industry as fast possible. As Patrick Siegfried, Esq pointed out recently, former SBA Administrator Karen Mills recently urged the the CFPB to implement the Small Business Data Collection Rule of the Dodd-Frank Act, a law which could potentially outlaw the underwriting practices of the entire business lending and merchant cash advance industries.

There’s also been the publication of a Small Business Borrowers’ Bill of Rights and the formation of the Responsible Business Lending Coalition. And on Forbes, an interview with loan broker Ami Kassar described the industry as the wild, wild west.

As a long time participant and observer in the industry, (this is my 10th year now) I want nothing more than a bright and prosperous future for both my peers and America’s small businesses. I hope you’ll take two minutes to take our survey above.

Thanks!

OnDeck vs. IOU Financial: Are one of these lenders mispriced?

August 12, 2015 Has OnDeck’s stock price dropped so much that it’s now a buying opportunity? You’ll probably want to read this before you decide.

Has OnDeck’s stock price dropped so much that it’s now a buying opportunity? You’ll probably want to read this before you decide.

OnDeck’s IPO market cap was $1.3 billion. They funded $1.2 billion worth of loans in 2014. OnDeck’s stock has since dropped though, bringing its market cap down to around $650 million. The company is often compared to Lending Club despite their business models being completely different. But since there has been seemingly no one else to make comparisons with, the two have become star crossed lovers in a new FinTech Lending category of the market.

Everyone seems to have ignored the fact that one of OnDeck’s direct competitors is also a public company and I don’t mean a subsidiary of a giant conglomerate for which no individual comparison would be logical, but a standalone entity that is a serious player.

Kennesaw, GA-based IOU Financial (formerly IOU Central) is actually a public company in Canada, even though its only operational activities are small business loans in the U.S. The company is not a fly-by-night me-too business lender, as they funded more than $100 million in 2014 and earned a spot on the deBanked leaderboard for being one of the biggest in the industry.

OnDeck out-loaned IOU in 2014 at a ratio of 12 to 1, but here’s the kicker, OnDeck’s market cap is more than 34x the size of IOU. When converting to USD, IOU’s market cap is only slightly above $18 million.

$18 million…

That for a company that loaned $100 million last year. It’s no wonder that the perceived low market value has invited a hostile takeover bid from Russian venture capitalists. The tender offer of $15 million, presumably in Canadian dollars, would’ve acquired 55.9% of the company’s outstanding shares. The company is currently waiting for its shareholders to vote on the offer.

Meanwhile, another competitor, Kabbage, was recently valued at $875 million on loan volume last year of $400 million.

Ignoring all other factors that comprise a lender’s worth

- Kabbage was valued at more than twice its annual loan volume

- OnDeck’s IPO value was about equal to its annual loan volume, but their current market cap is almost half its annual loan volume

- IOU Financial’s current market cap is less than 20% its annual loan volume.

On these stats alone, IOU Financial seems to be incredibly undervalued, especially for a company whose spokesperson is celebrity investor and TV personality Kevin O’Leary.

OnDeck touts OnDeck marketplace as a way to sell off loans and generate income but IOU also regularly sells off its loan receivables while retaining the servicing rights just like OnDeck does.

Kabbage out-loaned IOU last year by a ratio of only 4 to 1, yet is valued almost 50x higher than IOU.

Every company has strengths, weaknesses, and reasons why they stand apart from their peers even if they look very much like them. However, given the mind blowing disparity in valuations for lenders that compete for the same customer with similar products, there surely has to be a buying or selling opportunity in here somewhere.

I think the Russian nuclear scientists are on to something…

Former SBA Administrator Karen Mills Urges CFPB to Enact Small Business Data Collection Rule

August 11, 2015 Last week a handful of small business lenders announced the formation of the Responsible Business Lending Coalition. The announcement was made at an event held at the National Press Club in Washington, DC. The event’s Keynote speaker was former SBA Administrator Karen Mills.

Last week a handful of small business lenders announced the formation of the Responsible Business Lending Coalition. The announcement was made at an event held at the National Press Club in Washington, DC. The event’s Keynote speaker was former SBA Administrator Karen Mills.

During her presentation, Ms. Mills called on the CFPB to implement the Small Business Data Collection Rule of the Dodd-Frank Act. Ms. Mills’ request echoes the recent letter signed by 19 US senators urging the Bureau to issue the regulations contemplated by section 1071 of the Act. Ms. Mills argued that the data collection rule will be critical to understanding small business credit availability, especially for women and minority owned businesses.

Ms. Mills’ statements are the most recent in a series of requests to the CFPB to implement 1071. In addition to the 19 senators, multiple community activist groups along with the National Community Reinvestment Coalition have demanded that the Bureau take action.

The White House has remained silent on the issue so far. If the Bureau does decide to act, the new rule could be added to its list of action items as early as this winter.

The Importance Of A Profitable Business Model And Creative Financing For Your Broker Office

August 10, 2015 Continuing The Year Of The Broker Discussion, I wanted to touch on another aspect that isn’t discussed too often in our space (Independent Broker or Independent Agent space), and that’s the importance of creating a profitable business model and rounding up creative debt financing for our Office.

Continuing The Year Of The Broker Discussion, I wanted to touch on another aspect that isn’t discussed too often in our space (Independent Broker or Independent Agent space), and that’s the importance of creating a profitable business model and rounding up creative debt financing for our Office.

I believe it was the Roman Playwright, Plautus, that said, You must spend money to make money. This is certainly true for Independent Brokers and Agents, as we are entrepreneurs in every sense of the word, or if you operate a one man show like I do, then you would be more along the lines of a solopreneur which is new terminology floating around that refers to certain special entrepreneurs who run their business solo with full responsibility over the day-to-day operations.

However, despite the fact that one must spend money in order to make it, it begs the question as to why many new Brokers have very little networks, resources and other sources for financing?

Not only do they lack these resources, but many new Brokers also have not truly developed a scientific business model for their office based on: If I invest XYZ in data, marketing and all other aspects in association of producing 1 new closed deal, I would receive XYZ back into terms of the revenue off the initial closed deal as well as XYZ back in terms of recurring revenues on the renewals of said merchant.

Many new brokers lack both a scientific and profitable business model, along with efficient financing for said business model, which threatens their survival going forward.

Your Profitable Business Model

I argue with investors across the Investment Community all of the time in relation to which is better in terms of building the most Wealth, is it investing in Stocks or operating your own Profitable Business Model? I have always believed creating your own Profitable Business Model was the fastest way to Wealth due to the lack of control one has over the returns you can generate through the Stock Market. Commentators like James Altucher tend to agree with my mentality as he says: The best way to take advantage of a booming stock market is to invest in your own ideas. If you have an extra $50,000 don’t put it into stocks. Put it into yourself. You’ll make 10,000% on that instead of 5% per year.

I’ve always used a model of at least a 400% return within 24 months for operating my office because, not only did I have to cover business expenses and taxes, but I also had to cover my personal expenses, the funding of my emergency funds/savings, and the funding of my retirement accounts which includes SEP IRAs, Social Security, and Health Saving Accounts.

So for example, my model might have it to where if I invest $30,000 into my office, that should produce revenues of around $180,000 within 24 months, revenues include commissions from new deals, renewal deals, side processing residuals and other valued added products. This would leave a profit before taxes of $150,000 or a 500% return. Now the 500% range is just the benchmark used, in terms of actual returns, they have been at least double this amount due to my focus on maintaining clients for the long term as with recurring clients, there are no investment dollars spent on the acquisition of those additional revenues but they do continue to add to the overall “profitability” measurement of the original investment.

Utilizing this predictable model allows for the use of creative financing for leverage, cashflow management, along with the preservation of savings, and other investment portfolios. One of the tools I have been using for creative financing have been Credit Card No Interest Promotional Offers.

Using Credit Card Promotional Offers To Finance Your Office

I’m a Dave Ramsey fan like many Americans, but I’m totally against Mr. Ramsey’s consistent hammering of the use of “debt,” specifically the use of Credit Cards. Credit Cards are just like hand guns, if you put the gun in the hands of a solider, police officer, hunter, or a responsible home owner, then you protect human life, build nations and protect communities. If you put the gun in the hands of the common Chicago inner city street thug, then you get crime and homicide. If you put a Credit Card in the hands of a responsible person, the Credit Card is used to bring a variety of additional benefits to said user. But in the hands of an irresponsible person, the Credit Card just adds to their financial woes.

If you strive to keep your personal credit profile clean and with high efficiency, you should qualify for a number of Credit Cards that not just provide cashback rewards, but they provide short term financing in the form of 0% interest for 12 – 18 months, with a 1% – 3% upfront fee. This means you can receive an up to 18 month loan for only 1% – 3% in borrowing costs. These offers are not presented just when the card is opened, but they are generated usually on a monthly or quarterly basis.

So coming back to my business model, I might put that entire $30,000 on a credit card promo deal for 18 months with an upfront fee of 3%, which means the borrowing costs are $900. I would continue paying the minimum payment every month which is usually calculated as no more than 0.5% – 1% of the outstanding balance. I would invest the $30,000 into my business model and would have obtained the break-even return and profit measurement in a relatively short period of time (usually 3 – 5 months) and then be profitable on the investment. I would eventually end up paying off the outstanding balance on the Credit Card well before the promo period ends, which further increases my positive credit history allowing for larger credit limits to be requested.

Other Benefits Of Credit Cards Over Other Payment Options

Credit Cards also provide a host of other benefits including cashback rewards of anywhere from 1% – 45% depending on the reward category, these rewards and savings are not available through any other form of payment option. If you seek out cards with no monthly fees, setup fees or annual fees, you could run up balances, pay them off before the grace period ends, and obtain a stream of free income.

Credit Cards also include Chargeback Protection that can save you a significant amount of headaches down the line should you run into an unscrupulous vendor, or if you are the unfortunate victim of theft such as a robbery, identity theft, strong-arm theft, etc. For example:

- If someone steals your wallet and goes on a “card swiping spree”, once you report your Credit Card stolen then you aren’t responsible for any of those transactions. This isn’t as efficient if you carried a Debit Card, as the money would be gone from your Checking Account until the Bank recovers the funds in 30 – 90 days, which might cause you some cashflow issues. If you carried Cash, the money might never be recovered.

- If you ordered something from a vendor and didn’t receive it, you are protected with the use of Credit Cards. With a Debit Card or Check, it will again take 30 – 90 days for the dispute to complete with the Bank, however, throughout this period of time the money is still gone from your account until the dispute is over, which might cause some cashflow issues. If you used Cash for the order, the money might never be recovered in this case as even though you are likely to obtain a judgment by suing the vendor, the Courts do not assist you with collections.

To Wrap

In order to survive going forward as an Independent Broker or Agent, remember the importance of developing a profitable business model as well as having low cost sources of financing for said model. Credit Cards are one of the ways you can creatively finance your business model.

I’m on track to end the year with near or over $200,000 in total credit limit availability. This credit limit availability is spread out over a number of different accounts, but some of my favorite Credit Card Accounts include: The Double Cash Card ™ from CitiBank, The Discover IT Card ™ from Discover Bank, The BankAmericard Cash Rewards Card ™ from Bank of America, The Chase Freedom Card ™ from Chase Bank, The Upromise Mastercard ™ from Barclay’s Bank, The QuickSilver Rewards Card ™ from Capital One Bank, and The Blue Cash Everyday Card ™ from American Express.

Funding Circle Breeds Bean Bags

August 7, 2015Yogibo CEO Eyal Levy saw a business loan ad for Funding Circle and applied. “The process was very smooth,” Levy said, who made a point to say that he was interviewed by an underwriter. Today, Yogibo has around 25 retail store locations and their bean bag business is booming.

Bloomberg’s Eric Schatzker expressed surprise that it wasn’t an instantaneous automated algorithmic approval that online lending has a reputation for these days. Video below:

Just like Lending Club, whose CEO appeared on Bloomberg earlier today, Funding Circle is one of the original founders of the Responsible Business Lending Coalition. They announced a “borrowers bill of rights” yesterday.

Is This OnDeck Class Action Lawsuit a Sham?

August 7, 2015Update: The lawsuit was withdrawn on September 28, 2016

If you haven’t actually read the class action complaint filed against On Deck Capital on August 4th for an alleged violation of securities laws, you can download it here. Reactions throughout the industry are generally mixed, but the big surprise is that anyone would actually be surprised about who OnDeck is or what they are doing.

If you haven’t actually read the class action complaint filed against On Deck Capital on August 4th for an alleged violation of securities laws, you can download it here. Reactions throughout the industry are generally mixed, but the big surprise is that anyone would actually be surprised about who OnDeck is or what they are doing.

The company sourced 68.5% of its loans from commercial finance brokers in 2012 and 45.6% of its loans from them in 2013. By the second quarter of this year, that percentage had drifted down to 20.6%.

To OnDeck, this gradual shift has been part of an overall strategy to control their sales process, costs, and reputation. While it might impede origination growth in the short term, it would be a heck of a lot harder to explain to investors in the future that the company’s fate was in the hands of unknown salespeople who may or may not be swayed to work with their competitors at any moment.

Understandably, many brokers were not happy when OnDeck suddenly terminated them. Angry feelings spilled out on to DailyFunder, an online message board, and were eventually cited in a Seeking Alpha article, the very same article the lawsuit opens up with to make its case.

“THE TRUTH BEGINS TO EMERGE,” the complaint states. “On February 11, 2015, less than two months after the IPO, SeekingAlpha.com published an article entitled “On-Deck Capital: Bad Loans, Bad Interest Rates, Bad Business Plan.”

But the author of the article, TheStreetSweeper, which describes itself as as “a publisher of news and opinion,” placed a disclaimer that they held a short position in OnDeck’s stock. And notably, TheStreetSweeper website is run by Hunter Adams, a convicted felon who makes no effort to hide his past. His website bio says, “his career ended in 2001, when government investigators accused him of manipulating worthless penny stocks.” And continues, “he pled guilty to two conspiracy charges — for securities fraud and money laundering — and served time in prison for his crimes. Years later, he pled guilty to racketeering charges, fully cooperated with the government and accepted full responsibility for his actions.”

Today, his opinion on a stock for which he holds a short position in, has somehow become credible enough for lawyers to make the case that the “truth” had come out about OnDeck. But it’s no small oversight by the Pomerantz law firm, the attorneys that brought the suit on behalf of plaintiff Carl A. Stitt. A cursory glance at the law firm’s past press releases and filed complaints show that the firm regularly relies on TheStreetSweeper’s stories to solicit plaintiffs as well as to bolster class action complaints.

Notably, TheStreetSweeper’s analysis (overseen by convicted mob associate pumper dumper Hunter Adams), which Pomerantz accepts at face value and offers as evidence of misleading default rates, calculates a loan loss rate 24.8%. That formula is unfortunately incorrect. $26.7 million in charge offs divided by $107.6 million in gross revenue might return 24.8% but that’s not how one assesses a loan loss rate. $107.6 million is the interest income, not the aggregate loan principal.

OnDeck had an aggregate unpaid principal balance on loans outstanding of $422.1 million for the nine months ending September 30, 2014. $26.7 million was charged off during that time period.

Some quick math: $26.7 million/$422.1 million = 6.3% lost.

This is decent considering the company generated $107.6 million worth of interest income, not to mention consistent with what company management has both said and reported. TheStreetSweeper’s math and the plaintiff’s reliance on it is unsurprisingly wrong.

Reading through the rest of the suit, the plaintiff’s complaint hinges almost entirely on the phony calculation.

OnDeck might not be popular with the commercial finance brokers these days, and I myself have published several posts about their progress (good and bad), but if anything is garbage, it’s probably this lawsuit.

—-

Note: I do not and have never had a financial position in OnDeck.

Do Borrowers of a Feather Flock Together?

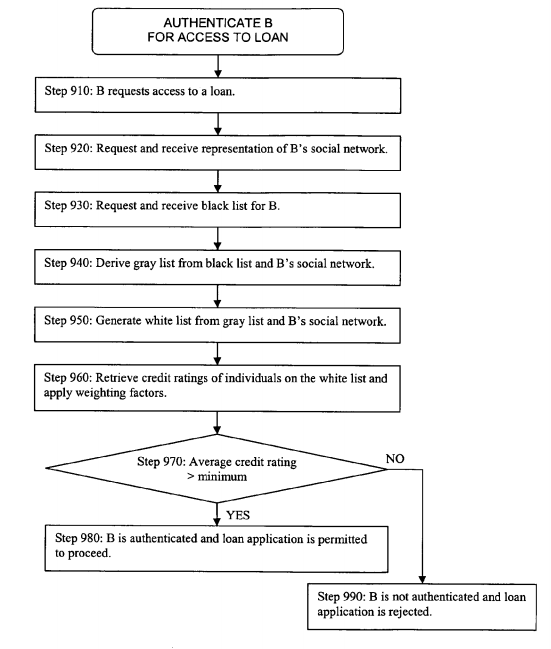

August 6, 2015Facebook believes that you might be the company you keep, at least according to a patent it has.

“When an individual applies for a loan, the lender examines the credit ratings of members of the individual’s social network who are connected to the individual through authorized nodes,” reads an explanation of the technology. “If the average credit rating of these members is at least a minimum credit score, the lender continues to process the loan application. Otherwise, the loan application is rejected.”

Diagram below:

This is one of those concepts that if ever used, is likely to end up prohibited under an amendment to the Equal Credit Opportunity Act or similar.

What are your thoughts on this?

And also, you might want to check out similar patents that Kabbage has in its arsenal.

MCC and BizFi Founder Stephen Sheinbaum on Bloomberg

August 4, 2015Earlier today on Bloomberg TV:

“Automation doesn’t mean no underwriting,” said Stephen Sheinbaum, the founder of Merchant Cash and Capital and BizFi.

Sheinbaum also said that they have never raised an equity round from an institution.

“We do want to go public,” he added. If they can obtain an equity investor, he put their timeline to go public at 12 to 18 months.

Watch the video below: