Business Lending

Underwriting Canadian SMB Loans and MCAs? You Still Need to Watch Out for Fraud

August 4, 2026 Back in February, Trust Science acquired Lenders API, a real-time fraud-prevention and consortium-data platform developed in collaboration with the Canadian Lenders Association and its small business, consumer, and automotive finance members. The platform is designed to address bust-out fraud, synthetic identity fraud, and loan stacking. Not all “stacking” is fraud, of course, but a recent deBanked feature reported that stacking business loans and MCAs is certainly on the rise.

Back in February, Trust Science acquired Lenders API, a real-time fraud-prevention and consortium-data platform developed in collaboration with the Canadian Lenders Association and its small business, consumer, and automotive finance members. The platform is designed to address bust-out fraud, synthetic identity fraud, and loan stacking. Not all “stacking” is fraud, of course, but a recent deBanked feature reported that stacking business loans and MCAs is certainly on the rise.

“No single lender can solve this problem alone,” said Tal Schwartz, co-founder of Lenders API, when the acquisition was announced. “Loan stacking and organized fraud thrive in the gaps between institutions. The only effective response is shared intelligence delivered through a compliant, trusted infrastructure.”

But wait—fraud? In Canada? According to a 2022 BBC feature, one of Canada’s defining characteristics is its “deep reservoir of niceness.” Those on the front lines in finance, however, say fraud happens there just as it does anywhere else.

“It’s quite a wild west,” said YaMing of Xuper Funding, a small business finance company that operates in both the United States and Canada. “…compared to the United States I would say it’s almost the same level of fraudulent files.”

“…my gut is going to be that it’s probably on par, relatively speaking [with the US],” said Jodi Levy, Head of Sales and Business Development for BizFund in Canada. Levy added that underwriting applications in Canada involves many of the same checks conducted by American companies regardless.

“I think the general idea is literally the same,” said Alex Xu, CEO of Xuper Funding, who works with YaMing. “It’s still against the revenue, it’s still about checking the fundamentals, checking the anti-fraud, so the procedures are literally the same.” The challenge, according to Xu, is that Canada’s credit-reporting infrastructure is not as mature as that of the United States. Data sources and access can also vary by province.

And it can be even more difficult to make a proper evaluation when a business owner has recently emigrated to Canada and has not had the same opportunity as a native-born citizen to build a public credit footprint over time. Twenty-three percent of Canadians are immigrants, for example, and that figure could rise to 34% by 2041. The total population of Canada today numbers around 41 million people.

Levy of BizFund said one advantage of operating in a smaller market is that news about fraud travels quickly, especially when a broker is involved. Discussing a hypothetical case involving an altered financial document, she said “It just wouldn’t fly. You’d be blacklisted so fast.”

In a sense, Lenders API was founded on that principle of sharing: The industry took fraud prevention into its own hands by creating a system through which participants could identify and report suspicious activity to one another. The company that acquired it, Trust Science, “is Canada’s third and most modern credit bureau,” according to its website.

Similarly, bad deals, like fraud, can also be reported through DataMerch, a U.S.-founded platform that also relies on members to report negative business dealings. Launched in 2015, DataMerch accumulated 100,000 records of unsatisfactory U.S. MCA deals by January 2023 and is still growing. Today, its database also includes Canadian businesses as well.

“Our Canadian search/merchant upload is based off the 9-digit Business Number,” said Scott Williams, co-founder of DataMerch. “Canadian funders can search by Business Number or legal name.”

Several companies that spoke with deBanked said defaults on Canadian business loans and MCAs can occur for many reasons, some fraudulent and some not. Certain forms of fraud can be nearly impossible to detect because the paperwork is authentic, the business is legitimate, and the only hidden element is the applicant’s intent to disappear as soon as the deal is completed. The fraud, in those cases, is in their mind.

But the Canadian market is not defined solely by fraud, nor is any market. There is plenty of good business and plenty of good deals, often beginning with strong broker relationships.

“If you have a good ISO partner to work with, they’re going to be transparent with you,” said Xu of Xuper Funding. “They’re going to work with you, they’re going to be very collaborative with you, and they’re going to syndicate with you. And that’s the ISO we really cherish and value.”

For Levy of BizFund, transparent communication begins at the outset.

“When I’m onboarding people, I kind of like to do the work upfront to make sure I understand,” she said. Although BizFund remains mindful of fraud and the warning signs that accompany it, Levy said that ultimately “the market is a lot of fun, there’s a lot of room to have an impact.”

LendingTree: “Using AI as a Communications Tool With the Consumer is Very Exciting.”

August 3, 2026“I think using AI as a communication tool with the consumer is very exciting,” said LendingTree CEO Scott Peyree during the Q2 earnings call. “For example, we develop a lead. Instead of sending that lead out five times and having five different brokers call the consumer a bunch, it’s like first have that—whether it’s voice or text or email—have that AI agent engage and communicate with the consumer a little bit first to get a little further detail on it.”

The substance of that conversation would be to clarify what type of factors are the most important, and then directing them to one or two companies that are best suited for that rather than to five.

“That’s a dramatically better consumer experience, and it’s a really useful way to use AI from a consumer-facing perspective,” said Peyree.

LendingTree: SMB Lending Business Softened in Q2, Merchant Sentiment Shifted

August 3, 2026“Performance in July gives us confidence that Q2 was our trough and we have entered the recovery period,” said LendingTree CEO Scott Peyree during the Q2 earnings call.

LendingTree’s SMB business underperformed in the quarter, driven by “both merchant sentiment and lender pullback.” It attributed this to tension in the Middle East, energy price spikes, and more, but concluded that the merchant sentiment issues, which have been slower to recover, were macro-driven and temporary.

“I will say the lenders have largely come back and are writing and offering loans at similar levels to early Q1. Merchant sentiment does remain soft,” said Peyree. “The long-term macro outlook for the SMB industry remains very strong, in our opinion. We’re seeing some encouraging signs already; Improving closing rates, larger loan requests, favorable underwriting shifts. July will be our best sales month since Q1.”

LendingTree does not make loans itself, it connects prospective borrowers with the proper partners that can do that. This business has been very lucrative and had been growing 40% year-over-year on average until now.

“This was our growth engine,” said LendingTree CFO Jason Bengel. “Like I said, it was growing 40% a year on average. Now for this year it’s looking like we might be flat to down. The good news is that should really be temporary. There’s nothing structurally wrong with that business. We operate very well in that business, and the market opportunity is really strong. That will recover. Once merchant sentiment returns, that will return to being a very strong growth driver for us. We’re very optimistic with small business.”

SoFi: We Think We Can Take Significant SMB Lending Marketshare

July 29, 2026“We’ve expanded our offering to include our new SMB loan product and have agreed to terms on a three-year, $3 billion agreement with BasePoint Capital,” said Chris Lapointe, CFO of SoFi during the company’s Q2 earnings call, who later added that there was also another undisclosed party working with them on this for several hundred million dollars. SoFi’s foray into direct business loan origination was announced a month ago after spending years referring customers to other parties using a platform it built.

“The SMB business is one that we think we can be incredibly competitive on, similar to personal loans and credit cards,” said Anthony Noto, CEO of SoFi during the Q&A session. “Most SMB lenders are charging exorbitant rates of over 30%. We think we can operate meaningfully below that and take significant market share.”

Small business lending was a recurring theme and question during the call so Noto explained the genesis for how they even first started thinking about it.

“SMB really was born out of the fact that a large percentage of our members actually are small business operators,” Noto said. “Back during COVID, when the government provided PPP loans, we got a significant amount of demand for applications on PPP loans, even though we were not in the SMB business. We actually stood up an application process that met the government’s application criteria and helped pass on that demand to lenders. Then on the back of that, we built a marketplace so that we actually get paid for that referral process that we’re doing. The SMB business is very much synergistic to the rest of our business. I would think of it as just another use case for an individual to satisfy the needs they have from a borrowing standpoint. We’ll obviously follow this up with checking and savings in SMB, and other products that are ancillary to that. It will add to the flywheel.”

Need Capital for Your Funding or Lending Company? 3Jane Does it On Blockchain

July 27, 2026“I’m a big believer in agentic capital markets. I think we’re going to see a Cambrian explosion of novel primitives, driven largely by two pieces. Today, it’s just very easy to construct arbitrary financial building blocks using smart contracts,” said Jacob Chudnovsky, Founder of 3Jane, to deBanked.

3Jane provides credit facilities and forward flow arrangements across a range of products, including consumer loans, small business loans, and even merchant cash advances. The company previously provided a $10 million senior warehouse facility to consumer lender LendSwift, for example, and followed that with an inaugural $8.5 million purchase of small business loans from Slope, an embedded credit infrastructure provider that powers business lending programs for major players across the US, including Amazon. According to Chudnovsky, 3Jane would like to do even more deals in the small business lending and MCA space.

But with a twist.

3Jane has built an entire protocol on the blockchain. It offers a credit-backed “yieldcoin” that earns its yield “from warehouse facilities, forward-flow programs, and credit-lines.” Investors can mint the coin on Ethereum, and it earns a yield backed by the performance of 3Jane’s credit assets. Minting is not open to US investors, but the company’s capital markets offerings are focused exclusively on North America. So, if you’re a small business funder seeking a credit facility or forward flow arrangement, 3Jane wants to speak with you.

3Jane has built an entire protocol on the blockchain. It offers a credit-backed “yieldcoin” that earns its yield “from warehouse facilities, forward-flow programs, and credit-lines.” Investors can mint the coin on Ethereum, and it earns a yield backed by the performance of 3Jane’s credit assets. Minting is not open to US investors, but the company’s capital markets offerings are focused exclusively on North America. So, if you’re a small business funder seeking a credit facility or forward flow arrangement, 3Jane wants to speak with you.

Chudnovsky is a software engineer by trade and entered the DeFi space in 2020.

“…around 2024, I basically came to the realization that credit is still an extremely underdeveloped vertical in crypto and particularly both the capital aggregation and the capital distribution side of it,” he said. “My initial focus was ‘can we get the best of crypto to distribute capital in a better way?’ and so I founded 3Jane, and we started off by doing unsecured lines of credit for crypto users in the United States who had a bunch of these different assets and could not really borrow against it in a streamlined way.”

That effort eventually led to 3Jane’s current business model. If the name 3Jane sounds familiar, it’s because Chudnovsky drew it from the 1984 novel Neuromancer, the famous William Gibson book that coined the phrases “cyberspace” and “the matrix.” By pure coincidence, Apple TV is releasing a 10-episode series based on the book in January 2027.

That effort eventually led to 3Jane’s current business model. If the name 3Jane sounds familiar, it’s because Chudnovsky drew it from the 1984 novel Neuromancer, the famous William Gibson book that coined the phrases “cyberspace” and “the matrix.” By pure coincidence, Apple TV is releasing a 10-episode series based on the book in January 2027.

“I just think we’re going to enter this complete renaissance of new different financial primitives and I think it’s going to drive a lot of adoption, new ways of thinking about our financial system and that sort of really resonated with me with the book,” Chudnovsky said.

And that new way of thinking is starting to take root. The capital markets utilizing blockchain to create efficiencies is already cropping up around the industry. Since 3Jane last spoke with deBanked, its purchase of embedded finance products from Slope has increased to a total of $60 million.

3Jane’s customers do not need to be crypto experts. The company handles that side of the transaction while underwriting the risk and executing what is otherwise a conventional capital markets deal, but one in which the infrastructure is robust enough that this can be a lender’s first and last facility. On 3Jane’s part, doing this requires a strong understanding of the various financial products it evaluates, including MCA.

“…there are a number of MCA operators in the United States that are doing things right, they’re growing significantly and they need leverage to scale their business,” Chudnovsky said. “and so warehouse facilities and to a lesser extent forward-flows for MCAs sort of equally make sense for them as long as you are cognizant of the risks.”

Enova Originated $1.6B in Small Business Loans in Q2

July 27, 2026Enova’s small business loan originations increased 29% year-over-year, coming in at $1.6 billion for Q2. Enova owns OnDeck and Headway Capital.

During the Q&A session of the company’s quarterly earnings call, Enova CEO Steve Cunningham was asked about the performance of their small business loan portfolio.

“I think on the SMB side, it’s been remarkably stable,” Cunningham said. “You can see quarter-to-quarter, we can have some growth variations, but we’ve been very healthy growth. Our net charge-off ratio has been hanging within the 4%-5% range that we would expect every quarter for quite some time.”

It’s Live, You Can Now Invest in a Credibly Warehouse Line Through Figure

July 21, 2026 IT’S LIVE. Less than two months after Credibly announced a strategic partnership with Figure to “modernize SMB capital markets via blockchain rails,” investors big and small are now able to share in the earnings of a Credibly business loan warehouse line.

IT’S LIVE. Less than two months after Credibly announced a strategic partnership with Figure to “modernize SMB capital markets via blockchain rails,” investors big and small are now able to share in the earnings of a Credibly business loan warehouse line.

Specifically, Credibly boarded a business loan portfolio on July 21 and can already borrow against it using Figure’s Democratized Prime. Investors can now effectively participate in the earnings of that line by lending their own money into the pool. The amount of capital contributed to the pool and the utilization rate of it play a big role in the yield generated from that. Investors can pull out of the pool at any time assuming there is liquidity available to do so.

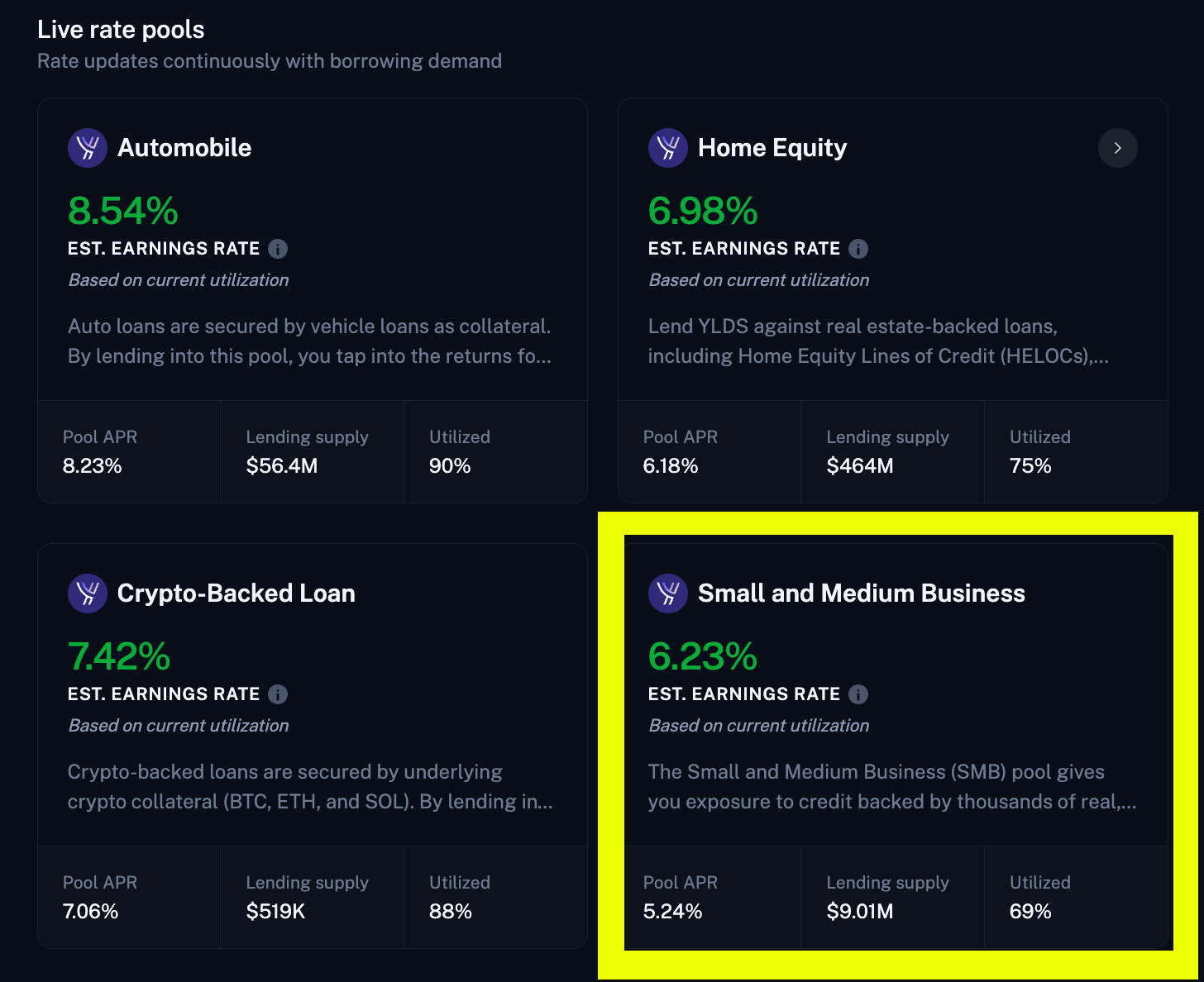

Unlike most investing platforms, investors can only participate in this one using blockchain rails (as was explained in deBanked’s May 23 story). Investors fund their accounts using dollars, crypto, or stablecoins, convert them into Figure YLDS tokens, and then lend those tokens into any number of available pools. As of the time of this writing investors can participate in HELOCs, auto loans, crypto loans, and now “small and medium business loans” which at present is sourced from Credibly. This all takes place on the Provenance blockchain and can all be easily conducted through the Figure Markets mobile app. deBanked was able to execute this process with no issues while using the investor side of the platform.

The investing opportunities on Figure’s Democratized Prime are warehouse lines for institutional-grade portfolios so investors are likely to see returns that resemble warehouse line rates (versus what one might expect if they do direct syndication with mom & pop lenders/funders). Credibly stands to benefit in the long run by the likelihood of lower borrowing rates and costs versus other capital market options and then being able to pass those savings onto their customers.

Investors will see some stats for the inaugural small and medium business loan pool which looked like this at the time of this writing:

The page also offers this information:

The Small and Medium Business (SMB) pool gives you exposure to credit backed by thousands of real, vetted American small businesses. The receivables represent payments owed by operating U.S. businesses. By lending into the pool, you earn from the cash flows those businesses generate as they repay their financing obligations. Backed by institutional-grade small-business credit, the SMB pool provides yield generated by a tangible, collateralized asset class, and a new way to diversify your portfolio.

Risk parameters

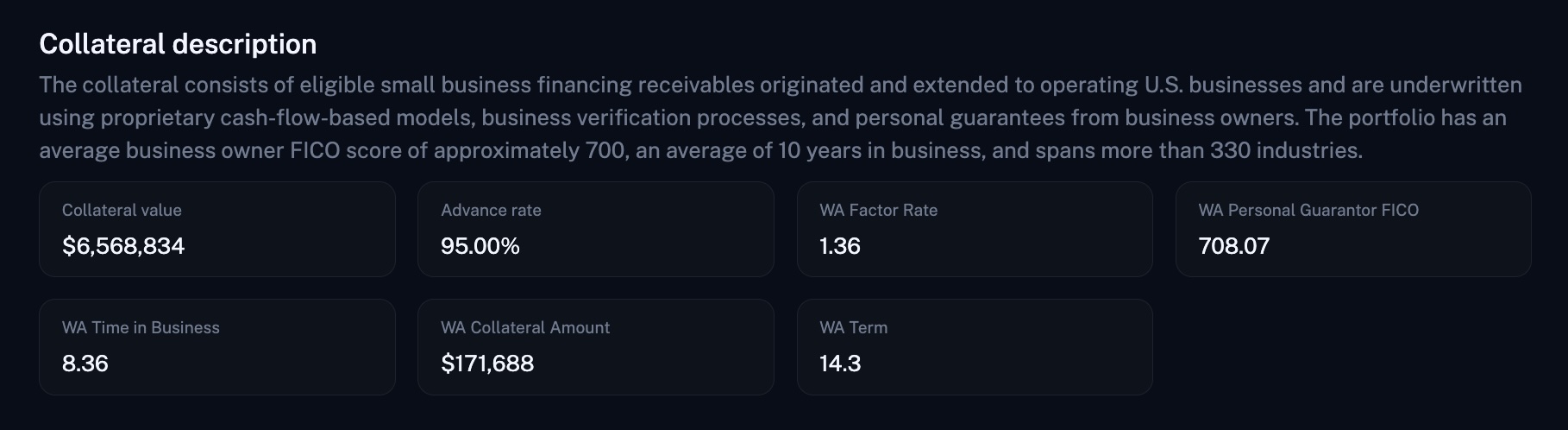

Democratized Prime manages risk through a structured financing facility backed by a diversified pool of prime small business financing receivables. The facility benefits from multiple layers of credit enhancement ensuring the pool can absorb a variety of adverse conditions before depositor yield is affected. This is enabled by a variety of mechanisms, including a 95% advance rate cap, reserve account funding, overcollateralization, originator repurchase obligations, and full recourse provisions. All receivables included in Democratized Prime must satisfy established eligibility requirements and be performing at the time of inclusion.Collateral description

The collateral consists of eligible small business financing receivables originated and extended to operating U.S. businesses and are underwritten using proprietary cash-flow-based models, business verification processes, and personal guarantees from business owners. The portfolio has an average business owner FICO score of approximately 700, an average of 10 years in business, and spans more than 330 industries.

The author contributed $5,000 in YLDS tokens into the Small and Medium Business loan pool on his own volition prior to the publication of this article for test purposes.

Stripe Capital, PayPal Working Capital Could Merge If Acquisition Offer is Accepted

July 19, 2026The old rumor that Stripe was interested in acquiring PayPal was apparently true. Partially anyway. This past April, Stripe, along with Block and Advent (a private equity firm), let PayPal know they were jointly interested in acquiring it. But Block dropped out of the deal and the newest acquisition offer, now public, comes from just Stripe and Advent together. While Stripe and PayPal are obviously known as payment processing companies, the two originate more than $3 billion a year in MCAs and short term business loans a year combined.

PayPal is one of the few online payment platforms to struggle with bad debt in its merchant funding program and the company had never weaponized its lending offerings to grow PayPal’s business. Nevertheless, its origination volume outpaced Stripe’s in 2025. Stripe and Advent offered $53 billion to acquire PayPal. It remains to be seen if a deal will actually happen.