Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

IT’S A BROKER’S WORLD

August 31, 2016

From east to west, small businesses are getting funded. But how they’re found and who they work with depends on where they are. In the US, where brokers tend to have a love/hate relationship with the funding companies they work with, they are no doubt a driving force in the market. In other countries, they might not even exist, are just starting to bloom or they add balance to a mature market. Is the world built for brokers? deBanked traveled far and wide to find the answers.

Down under in Australia where American-based merchant cash advance and lending companies have expanded, the ISO (which stands for Independent Sales Office and is synonymous with broker) model has not really followed. David Goldin, CEO of Capify, an international company headquartered in New York, told deBanked that there’s very few ISOs in Australia.

He believes that’s because there’s next to no payment processing ISO market there, a foundation that was a major precursor in the US towards the development of ISOs reselling merchant cash advances and business loans.

He believes that’s because there’s next to no payment processing ISO market there, a foundation that was a major precursor in the US towards the development of ISOs reselling merchant cash advances and business loans.

Luke Schmille, President of CapRock Services, echoed same. The Dallas-based company founded Sprout Funding in Australia earlier this summer as part of a joint venture with Sydney-based family office Huntwick Holdings. “Direct marketing is the primary method [of acquiring deal flow],” he said. “The credit card processing space is controlled by several large banks, so you don’t see ISO efforts in the acquiring space either.”

Big bank dominance was only one reason why another country’s emerging alternative small business funding market developed slowly. In Hong Kong, non-bank alternatives like merchant cash advances faced legal uncertainty for a long time. For example, Global Merchant Funding (GMF), once the only merchant cash advance company in the Chinese special administrative region, had been relentlessly pursued for years by the Secretary for Justice for conducting business as a money lender without a license. GMF fought it. And won.

In May of this year, the legality of merchant cash advances ultimately prevailed after the highest court ruled the agreements were not loans. Emboldened, several companies have stepped up their marketing of the product. But whether they’re doing daily debit loans or split-processing merchant cash advances (both of which exist there), marketing tends to be directed at merchants, not a middle market of brokers.

Gabriel Chung of Hong Kong-based Advanced Express Capital said that there are a handful of large brokers typically comprised of former bankers, but the rest of the broker market is highly fragmented, mostly made up of individual freelancers.

Gabriel Chung of Hong Kong-based Advanced Express Capital said that there are a handful of large brokers typically comprised of former bankers, but the rest of the broker market is highly fragmented, mostly made up of individual freelancers.

Adrian Cook, the Founder and CEO of Hong Kong-based Asia Capital Advance, agreed that marketing is usually aimed at merchants directly but that it’s changing. “Since the market is still very new and MCA is only beginning to gain popularity, brokers on the market are only starting to recognize MCA,” he said. “There is a lot of room for the brokerage market to grow.”

In the UK, where Capify also operates, CEO David Goldin explained that the UK doesn’t have a lot of credit card processing ISOs so there wasn’t a major migration from that business to MCA like there was in the US. But that doesn’t mean there is no middleman market at all.

Paul Mildenstein, executive director of London-based Liberis, said that brokers are an important channel, but not as dominant as they are in the US. “Our brokers are usually members of the NACFB, an organisation in the UK that actively supports and provides operating principles to the furtherance of the commercial finance broker community,” he wrote. The National Association of Commercial Finance Brokers claims to have 1600 members, one among them is Liberis.

Paul Mildenstein, executive director of London-based Liberis, said that brokers are an important channel, but not as dominant as they are in the US. “Our brokers are usually members of the NACFB, an organisation in the UK that actively supports and provides operating principles to the furtherance of the commercial finance broker community,” he wrote. The National Association of Commercial Finance Brokers claims to have 1600 members, one among them is Liberis.

“Many clients want the support of an experienced professional who can discuss the financial options available to them in their specific circumstances,” said Liberis’ CEO, Rob Straathof. “Given relatively low awareness of the Business Cash Advance product in the UK, this means that brokers have a key role to play in educating potential customers on when this is the right option for them,” he added.

Straathof stressed a robust criteria for the brokers they work with and explained that brokers are their eyes and ears in the market. “The relationships we have with them are not transactional, but transformational for our business,” he said.

The NACFB was also praised by Alexander Littner, Managing Director of Chelmsford, Essex-based Boost Capital. The company, which is actually a subsidiary of Coral Springs, FL-based BFS Capital in the US, sees a balance between their use of brokers and their efforts to acquire customers directly.

“As the alternative finance market is still relatively new here in the UK these brokers are important for this independent advice, and to help educate the market and establish trust,” Littner said. “At Boost Capital we work very closely with brokers across the UK, they are a critical part of our growth and fundamental to our ongoing success.”

In the US, brokers play such a dominant role in customer acquisition that some MCA funding companies rely on them to source the entirety of their business. Back in February, Jordan Feinstein of NY-based Nulook Capital told deBanked, “We decided that the best way to grow is to build relationships to avoid the overhead, compliance, training and manpower that a sales team would require.” Nulook markets its broker-only approach as a strength.

Others take a more blended approach, like Justin Bakes, CEO of Forward Financing, for example. “While our priority is to self originate, it is essential to create and maintain partnerships in this business,” he said earlier this year.

Notably, no such guiding authority like the UK’s NACFB exists for brokers in the US so it’s not easy to track exactly how many there are or how they operate, but their role in the industry cannot be understated. deBanked actually labeled 2015 The Year Of The Broker, when it published an article in its March/April 2015 issue that tried to capture the essence of the industry at the time. Tom McGovern, who was then a VP at Cypress Associates LLC, said of brokers, “They’re like the missionaries of the industry going out to untapped areas of the market.”

But preaching the gospel of alternative funding exists at different stages across the world. And Goldin, whose company Capify operates in four countries including the US, thinks that many middlemen here at home may not ultimately survive. In an interview, he predicted that the stronger ones over time will be acquired by funding companies and that direct marketing will only increase. “I think more and more companies are going to start building their own internal sales forces,” he said.

Other brokers are not convinced that acquisition costs will lead to the death of their businesses, especially if they’ve already found ways to reduce overhead costs. Several brokers have discreetly mentioned running operations from Costa Rica, Nicaragua or elsewhere as a way to keep things profitable. Still more, like Excel Capital Management based in Manhattan, have found that offering a suite of products allows them to monetize more customers. Chad Otar, a managing partner for Excel, said that they recently brokered a $4.9 million SBA loan. MCA is just one of their options these days. “As long as there’s small businesses, there’s always going to be opportunity,” he said.

In the US, the brokers have certainly seized it, but that’s because most funding companies offer big bucks and quick payment to those that are capable of sourcing customers. In other countries, compensation for services rendered might be the responsibility of the broker to arrange with the merchant since it may not be customary for funding providers to pay commissions. That would mean more work and more risk for the broker.

In the US, the brokers have certainly seized it, but that’s because most funding companies offer big bucks and quick payment to those that are capable of sourcing customers. In other countries, compensation for services rendered might be the responsibility of the broker to arrange with the merchant since it may not be customary for funding providers to pay commissions. That would mean more work and more risk for the broker.

Ironically, some brokers in the US will tap into both sides, earning a commission from the funder and charging a fee to the merchant for services rendered. And if the broker has payment processing roots, they can go a step further and earn merchant account residuals as well.

Brokers can’t exist without funding companies willing to support their endeavors, of course. While their prevalence around the world varies, most of the funding companies deBanked spoke to, appear eager to nurture the middleman’s role, so long as they act responsibly.

“Brokers in the UK are incredibly important as independent advisors to small businesses on the various sources of finance to suit their needs,” said Littner.

And as long as those customers, wherever they may be, are getting the value they want from a broker, that role, so long as it can continue to be done profitably, will likely have a place in the world for the foreseeable future.

Can an ISO “Excel” in 2016?

August 26, 2016

Don’t let anyone tell you that it’s too hard for a commercial finance broker to make a buck in exchange for honest work these days. One ISO in lower Manhattan is seeing more opportunity than ever before. Chad Otar, a managing partner of Excel Capital Management, sat down with deBanked to make his case for a bright future.

“As long as there’s small businesses, there’s always going to be opportunity,” Otar said. “Business owners are always going to need money.” Ironically, his own company that he cofounded in 2013 with hometown friend Nathan Abadi, was formed without any outside debt. Bootstrapped even to this day and even as they’re expanding, they’ve seen firsthand what other businesses around the country have to go through to get ahead.

“We’ve always believed in the products that we’ve sold,” said Otar, who brokers merchant cash advances, business loans, SBA loans, factoring products and more. They want every deal to help their clients whether it’s big or small, explaining further that even he himself has to feel comfortable with what the merchant wants. When asked about size, Otar said the largest SBA loan they got done was for $4.9 million.

But when questioned if more merchants were moving towards factoring and other traditional products, he explained that some merchants just don’t want to deal with the hassle of something that might be overly invasive or a process that might take a long time. They just want to get funded quickly, he said. And that’s where they come in.

Otar and Abadi’s optimism is not just anecdotal. The two partners, who previously renewed one year leases for their small office on Maiden Lane, saw enough runway to recently sign a five year lease for a 2,700 sq ft. office on Greenwich Street, staying within the bounds of the city’s financial district. Between full time employees and contractors, they currently house about fifteen people in their new office.

Though the partners live in Brooklyn, they, like many other companies in the industry, believe a Manhattan headquarters makes the most sense. “Everything is here,” Otar said. It’s easier to recruit new hires, he explained. And they indeed have immediate hiring plans now that they’ve got the space for it, both in sales and operationally.

Though the partners live in Brooklyn, they, like many other companies in the industry, believe a Manhattan headquarters makes the most sense. “Everything is here,” Otar said. It’s easier to recruit new hires, he explained. And they indeed have immediate hiring plans now that they’ve got the space for it, both in sales and operationally.

This new up-and-coming generation of business owners is very comfortable with the Internet and technology, Otar added, speeding up the process and allowing they and the funding partners they work with to do more deals together. One example offered was a small business owner who gave a guided tour of his establishment to an underwriter using FaceTime on his phone. Normally, the process would’ve been delayed by a few days because of the time it takes to hire a third party to perform a site inspection.

Some funding partners offer DocuSign so that merchants don’t even have to spend time printing and signing documents anymore, he said, qualifying that however by adding that while some merchants love it, others hate it and feel more comfortable doing things the old fashioned way. He acknowledged that was likely due to the generational gap that still exists.

When asked if the setbacks and gloom that had begun to envelop the consumer lending side of fintech, was also affecting the commercial side, Otar said he didn’t see it. Funders are still very aggressive with approvals and terms, he said. While paperwork required for approval is declining overall, he described one obstacle that he hadn’t really dealt with in previous years, UCC filings that are accidentally left active even when the agreements are satisfied in full.

Underwriters doing due diligence might interpret active UCCs to mean that outstanding obligations still exist. Absent a formal termination of the UCC, an underwriter may request that merchants provide documents from the secured party to support that a termination should’ve been filed. This in itself is not a burdensome task but Otar said he has seen merchants who have used alternative financing products continuously over the last eight years or so, who are then challenged to produce satisfaction letters from dozens of companies, some of whom the merchant may only vaguely remember.

But he is not discouraged when new challenges come up. “We’ve been constantly learning,” he said. And when asked what their secret to success has been up until this point, “It’s hard work and dedication,” he responded.

LendIt’s Peter Renton is Still Earning 8.72%

August 25, 2016

LendIt, speaking to LendIt USA 2016 conference in San Francisco, California, USA on April 11, 2016. (photo by Gabe Palacio)

LendIt Conference founder Peter Renton made more from his marketplace lending investments in the last twelve months than some people earn in a year just from their nine-to-five job. $54,936 to be exact, according to his latest blog post detailing his performance. That’s a result of investments on the Lending Club platform, Prosper, P2Binvestor (which requires you to be an accredited investor), the LendAcademy P2P Fund (which includes Funding Circle, Upstart, Lending Club and Prosper), and the Direct Lending Income Fund managed by Brendan Ross (which invests with lenders such as Quarterspot and IOU Financial).

Unsurprisingly, his business loan performance through the Direct Lending Income Fund has earned the highest yield, a TTM return of 12.77%.

While reporters and critics seem to be planning the funeral for several lending platforms, Renton remains steadfast in his optimism. “Eventually, I plan to have a diversified seven-figure portfolio made up of consumer, small business and real estate loans,” he wrote on his Lend Academy website.

Though Renton is reaping the benefits of being a platform investor, it’s the platforms themselves that may be in trouble, according to a recent op-ed by Todd Baker, a senior fellow at the Mossavar-Rahmani Center for Business and Government at Harvard University’s John F. Kennedy School of Government. On American Banker, Baker wrote, “Almost all [Marketplace Lending] revenue is generated from ‘gain on sale’ fees earned from new loan sales. This dependence on origination volume and gain-on-sale margins makes MPL results exquisitely sensitive to macro and micro trends in investor demand and risk appetite.”

And if a platform isn’t sustainable, the theory is that future investment opportunities may not be as available as they have been historically.

“MPLs need to shift to a more sustainable mode — either as banks or as nonbank balance-sheet lenders — before the end of the current credit cycle brings on a real shakeout and the MPL experiment becomes a financial failure,” Baker wrote.

Renton himself acknowledged a downward trend in his yield, conceding that it may never return to previous levels. “While I would love to be earning more than 10% again I don’t expect to get back there any time soon,” Renton wrote.

He also recently rebutted a Bloomberg article that argued Lending Club was being shady with repeat borrowers.

Hillary Clinton Wants to Harness the Potential of “Online Lending Platforms”

August 24, 2016 Presidential candidate Hillary Clinton acknowledged online lending on Tuesday when she published her plan to help small businesses. “Small businesses owners cite insufficient access to capital as a primary inhibitor to starting, growing, and sustaining a small business,” she asserted in a fact sheet posted to her website.

Presidential candidate Hillary Clinton acknowledged online lending on Tuesday when she published her plan to help small businesses. “Small businesses owners cite insufficient access to capital as a primary inhibitor to starting, growing, and sustaining a small business,” she asserted in a fact sheet posted to her website.

To solve that dilemma, she wants to:

- Harness the potential of online lending platforms and work to safeguard against unfair and deceptive lending practices.

- Streamline regulation and cut red tape for community banks and credit unions while defending the new rules on Wall Street.

- Give the SBA administrator the authority to continue providing 7(a) loan guarantees to small businesses if demand is higher than the yearly cap, helping even more small businesses get affordable bank loans.

- Etc.

The WSJ and other media outlets have claimed Clinton’s reference to online lending means “marketplace lending” but that appears to be an exaggeration. The two are not synonymous. One company for example that just secured a $100 million credit facility from Goldman Sachs to make more loans online is not a marketplace, but rather a balance sheet lender that helps banks make loans to their clients.

Hillary Clinton’s plan for small business growth is focused on community banks, the SBA and tax incentives. Fintech and marketplaces were not mentioned. You can read it here.

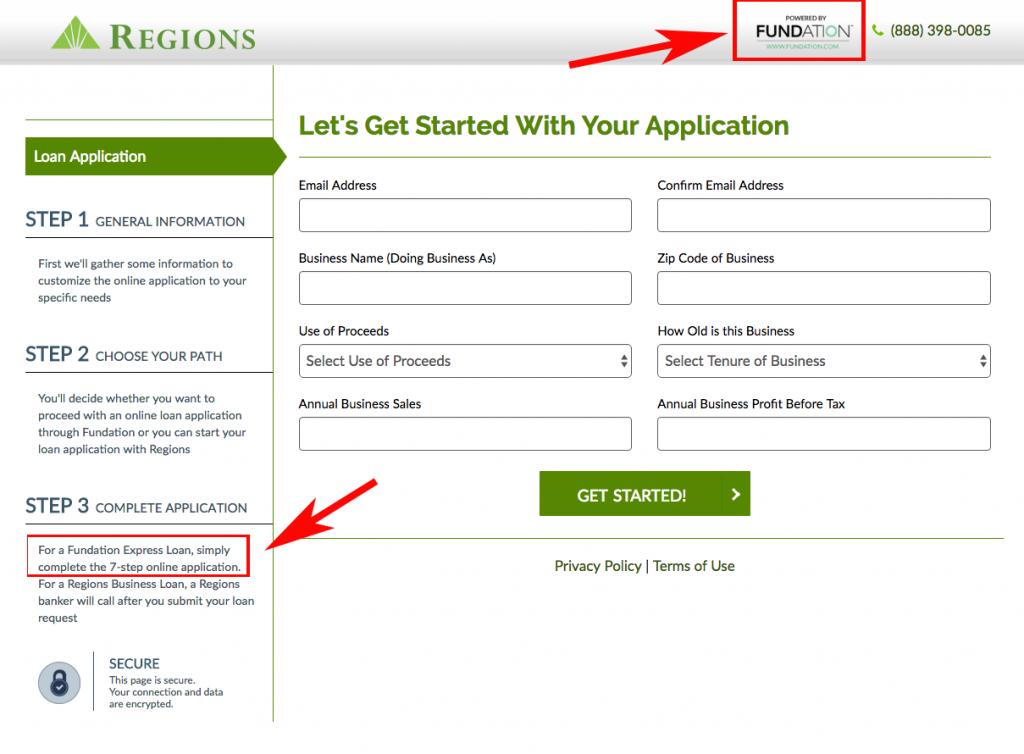

Fundation’s $100 Million Credit Facility From Goldman Sachs Is A Return To Banking

August 23, 2016 The online lending party isn’t over yet. And neither is bank lending…

The online lending party isn’t over yet. And neither is bank lending…

Fundation, which company CEO Sam Graziano described to the WSJ as a credit solutions provider rather than a lender, has secured a $100 million credit facility from Goldman Sachs. But they are a lender, a direct small business lender in fact, that uses their own balance sheet to make loans.

Fundation is different in that they bolt their platform on top of the traditional banking system. Their partnership with Regions Bank for example, allows Regions Bank customers to apply for a Fundation loan right through the Regions.com website.

The sizable credit facility, the system it will help foster, and the name behind it further demonstrates the demise of peer-to-peer lending. “We decided to be an integrated partner of the banking system,” said Fundation’s Graziano to the WSJ in regards to the saturated environment of lending platforms.

The WSJ also reported that the firm will use the funds to make more loans to Regions bank customers as well as other community banks that they have partnered up with.

Prosper Marketplace Bitten in Q2 With Major Loss

August 17, 2016Prosper Marketplace Inc. reported a Q2 2016 loss of $35.5 million, down from a loss of only $6 million over the same period last year. While not publicly traded, the company is still required to file its results. Originations for the quarter totaled $445 million.

For comparison purposes, rival Lending Club posted an $81 million loss on $1.96 billion in originations.

Prosper incurred $14 million in expenses just from restructuring related to their downsizing and layoffs which includes the closing of their Salt Lake City office and the termination of 167 employees.

The company also used a lot of cash, finishing Q2 with only $29 million in the bank, down from $66 million at the beginning of the year. Lending Club by comparison had $573 million in the bank at the end of Q2.

According to their 10Q, “Prosper Funding saw reduced listings on the marketplace as Prosper slowed down marketing efforts to reduce demand from Borrowers and maintain marketplace equilibrium. As a result, Prosper Funding experienced a decline in administration fee revenue-related party during this period and expects a decrease in administration fee revenue-related party in the third quarter of 2016 from the third quarter of 2015.”

Meanwhile, the performance of their actual loans has remained steady. View their latest performance update HERE.

Google’s Payday Loan Ad Ban References The Truth in Lending Act (TILA)

August 15, 2016 Did the government pressure Google?

Did the government pressure Google?

Payday loan ads have mostly disappeared from Google’s search results after they banned ads for personal loans where the Annual Percentage Rate (APR) is 36% or higher. In a May 12th post, shortly after the proposed ban was announced, I speculated that the sudden change was likely due to government intimidation, rather than the come-to-Jesus moral reckoning claimed by Google’s Director of Global Product Policy, David Graff.

Google’s official Adwords policy regarding personal loans now cites the Truth in Lending Act, hinting that compliance with the policy is really about compliance with federal law.

Advertisers for personal loans in the United States must display their maximum APR, calculated consistently with the Truth in Lending Act (TILA).

This policy applies to advertisers who make loans directly, lead generators, and those who connect consumers with third-party lenders.

The TILA regulations can be found at 12 CFR Part 1026. The description of which charges are included and excluded from the calculation of “Finance Charge” is found in Section 1026.4. The APR calculation for “Open-End Credit” is found in Section 1026.14. The APR calculation for “Closed-End Credit” is found in Section 1026.22.

The timing of this change is suspicious since just one month before Google announced the ban, the owners of an online payday loan lead aggregator were hit with a lawsuit by the Consumer Financial Protection Bureau (CFPB). Among the allegations is that the defendants ran a lead aggregation business that did not attempt to match consumers with the best loan for their needs, as consumers were led to believe by some lead generators.

“In particular, consumers are likely to be steered to lenders that charge higher interest rates than lenders that comply with state laws, that do not adhere to state usury limits, or that claim immunity from state regulation and jurisdiction,” the complaint says.

The company the defendants ran, T3Leads, was also sued by the CFPB in a separate action.

Google too, as master aggregator, arguably does not attempt to match consumers with the best loan for their needs, nor have they likely been continuously vetting their lending advertisers for legal compliance. While Google has not been sued or accused of any wrongdoing, the CFPB seemed to be laying the groundwork for such a challenge in the future. And as a blanket hedge or perhaps after a direct threat, they’re now applying certain federal loan laws as if they were already subject to them.

You can see an example of the before-and-after of Google’s search results HERE.

Square Capital Outgrows Square

August 11, 2016 You don’t need to process payments through Square anymore to get a loan from Square Capital. Restaurants that use Upserve, a restaurant payments and data analytics system, are now eligible as well.

You don’t need to process payments through Square anymore to get a loan from Square Capital. Restaurants that use Upserve, a restaurant payments and data analytics system, are now eligible as well.

Formerly known as Swipely, Upserve is still relatively small, with only 7,000 restaurants as customers. But it’s a milestone for Square nonetheless, whose loan program within their own ecosystem has become so successful, that they feel comfortable venturing outside of it.

“We are proud to partner with Upserve and offer loans through Square Capital to even more small businesses who traditionally face barriers when seeking access to funds,” said Jacqueline Reses, Head of Square Capital.

The move puts them on a path to truly competing with other alternative lenders such as OnDeck and CAN Capital. Loans are repaid just like they are through Square, through a percentage of each day’s card sales with the option to repay early at no additional fee.