Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

That Awkward Moment in Alternative Lending When…

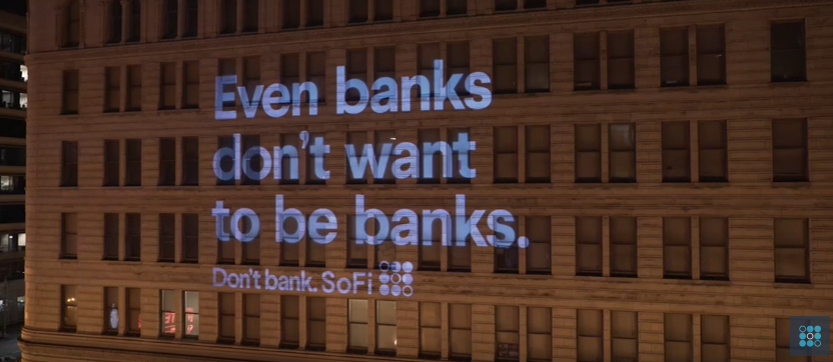

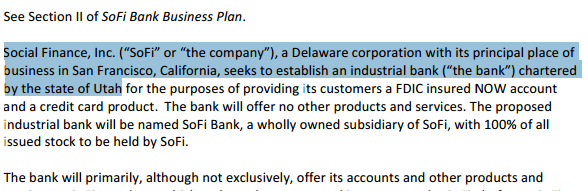

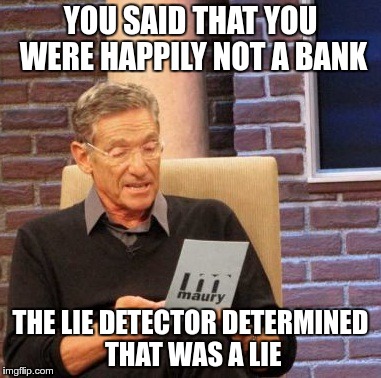

June 13, 2017That awkward moment when you apply for a bank charter (::cough:: SoFi ::cough::) and you realize your company’s motto has literally been #dontbank all along…

Just, don't do it. #DontBank pic.twitter.com/lnxKJHH3QJ

— SoFi (@SoFi) February 11, 2016

Banks send you statements. Our statement is we don’t like banks. Check us out at https://t.co/B5YXtHWKL0. #DontBank pic.twitter.com/RshfsAhdYR

— SoFi (@SoFi) January 26, 2016

Happily not a bank. http://t.co/bDN6i1Fd5W #SoFiSoFun

— SoFi (@SoFi) August 25, 2015

You can view the full bank charter application of the anti-bank whose slogan was #dontbank, here. You can also read an article about it on TechCrunch.

Another NY Supreme Court Judge Casts Doubt On The MFS – Volunteer Pharmacy Case

June 10, 2017Just as an Orange County, NY judge found in Merchant Funding Services, LLC v. Micromanos Corporation d/b/a Micromanos and Astsumassa Tochisako that a uniquely structured merchant cash advance was not a criminally usurious loan, so too did the Honorable Maria S. Vazquez-Doles on June 8th, court records reveal. Vazquez-Doles, who also presides in Orange County, concurred that the attorney representing defendants in Yellowstone Capital LLC v M N B Waterford LLC d/b/a MAC N’ Brewz! Mac N.Cheez! LLC d/b/a Mac N’Cheez! Somerset and Gary E Sussman, misquoted the contract’s language in their motion papers to suit their argument that the agreement was in fact a loan. In her decision, she referred to defendants’ attempt to twist the words as “incomplete and palpably misleading.”

“The Agreement is not on its face and as a matter of law a criminally usurious loan,” she held.

This is the second judge to opine that the decision in Merchant Funding Services, LLC v. Volunteer Pharmacy Inc. was premised on the opposition palpably misquoting an addendum to the contract in their motion papers. The first was the Honorable Catherine M. Bartlett last month.

The weight of the Volunteer Pharmacy case to a cottage industry of attorneys hoping to argue that merchant cash advances are disguised loans, is rapidly declining. The actual language of the these particular contracts has now twice exonerated the merchant cash advance companies.

The Yellowstone case decided on June 8th is filed under Index Number: EF001264-2017.

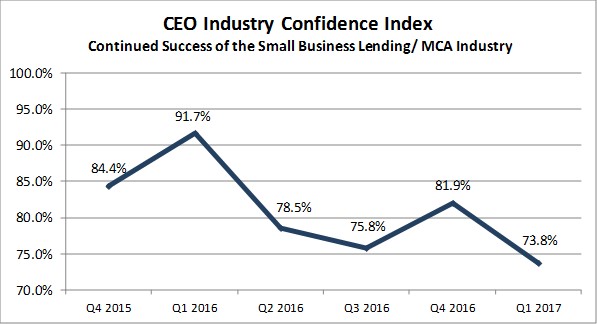

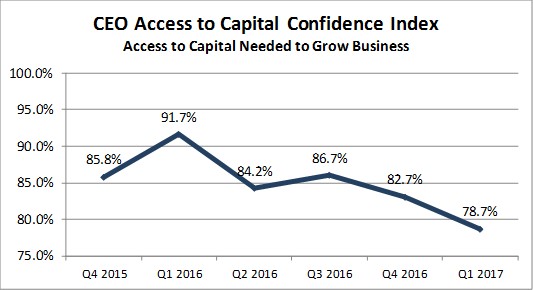

Industry CEOs Were Less Confident in Q1

June 6, 2017According to the latest quarterly Bryant Park Capital/deBanked survey of industry CEOs, confidence dropped to the lowest levels since the survey first began in Q4 2015. Specifically, confidence in being able to access capital needed to grow dipped down to 78.7% from 82.7% in the prior quarter. Confidence in the continued success of the Small Business Lending & MCA Industry shrank from 81.9% in Q4 to 73.8% in Q1.

See the trends below:

The survey does not ask participants to offer a reason for their confidence but the drop could probably be partially attributed to the events that occurred at CAN Capital, OnDeck’s struggles, and a general correction that took place at several other competing firms.

Sneak Peek of Our May/June 2017 Magazine Issue

June 5, 2017

Move over New York, California and Florida because Texas has become a strong incubator for alternative small business finance. In this newest deBanked magazine issue, we went to Dallas-Fort Worth, Austin and Corpus Christi to find out how and why non-bank financing products are flourishing. We were impressed by what we found and inspired just enough to dub Texas The ‘Loan‘ Star State.

And we went bigger than Texas (if that can be believed) by exploring how alternative lenders are spreading their wings beyond the states into other countries like the UK, Australia and Canada. But does it make sense to go abroad before you’ve cornered the market domestically? Industry captains share their thoughts.

There’s more of course, like how new tweaks to automated processes are actually making manual underwriting exercises easier. That itself has re-opened a debate that won’t seem to go away, humans vs computers in underwriting. In 2017, the humans aren’t out of the game yet and some think they never will be, but there are new tools available to increase speed and efficiency.

There’s legal decisions you’ll want to read and details about a new small business lending regulator you’ll want to know about. It’s all in the May/June 2017 issue that subscribers will be receiving in the mail soon and if you’re not subscribed, you should sign up FREE right now!

Commercial Finance Coalition Continues to Engage

June 1, 2017

A sign of a mature industry? The Commercial Finance Coalition is becoming a major liaison between the merchant cash advance industry and Washington. Just as peer-to-peer lenders and electronic payment companies have their own trade associations, the CFC is regularly engaging with legislators to offer their input where needed. And that requires a concerted effort, as evidenced by the group’s most recent trip that included meetings with 26 Members of Congress and senior staff. Those are typically separate individual meetings so you can imagine the amount of time and preparation involved.

“The Commercial Finance Coalition (CFC) conducted our third Washington, DC legislative fly-in last week,” Dan Gans, the CFC’s executive director, said to deBanked. “Fifteen members of the organization attended as well as a few prospective members. The CFC continues to establish itself as the premier trade group in the MCA and alternative small business finance space.”

The CFC also gets involved at the state level and played a role in preventing harmful legislation in New York a few months back. Most importantly, their mission is to simply tell their story.

“Studies show that traditional banks cannot meet the overwhelming demand for small business capital in the United States and we be believe that CFC members help thousands of entrepreneurs grow and sustain their businesses,” Gans explained. “We believe it is critical to educate policy makers in Washington and in state capitals like Albany and Sacramento about the vital role our industry plays in helping small businesses achieve success.”

The CFC is not the only trade association in the industry, but they have made political engagement a focal point of their mission since they were founded 18 months ago.

Gans elaborated on this. “Since its establishment in January of 2016, the CFC has been educating Members of Congress and state legislators about MCA and non-bank small business finance. We give our members a needed voice with elected officials and regulators. I would encourage anyone in the MCA space that is not a CFC member to inquire about membership. The industry is facing many threats and it is important that groups like the CFC stand in the gap to educate government leaders about the thousands of jobs advances from our members create across the country.”

To inquire about CFC membership, they advise to please contact Mary Donohue at mdonohue@polariswdc.com or call (202) 368-9758.

Full disclosure: I have accompanied the CFC on their DC fly-ins and the engagement is every bit as real and consequential as it sounds.

Why OnDeck is Underperforming its Peers

May 29, 2017![]() Small business lending company OnDeck was down nearly 23% on the year when the market closed on Friday. One of their closest rivals, Square, a company that makes business loans in addition to offering payment processing services, was up almost 64% this year so far. The disparity can be partially attributed to the market’s changing perception of OnDeck, originally viewed as a disruptive technology company, to what they’re seen as now, a niche commercial lender. Their tech multiple is gone, putting their market capitalization near book value.

Small business lending company OnDeck was down nearly 23% on the year when the market closed on Friday. One of their closest rivals, Square, a company that makes business loans in addition to offering payment processing services, was up almost 64% this year so far. The disparity can be partially attributed to the market’s changing perception of OnDeck, originally viewed as a disruptive technology company, to what they’re seen as now, a niche commercial lender. Their tech multiple is gone, putting their market capitalization near book value.

Square is faring differently since they have virtually no borrower acquisition costs (whereas OnDeck has high acquisition costs) and a strong revenue stream outside of loans. Square’s strategy is to turn its existing payment processing customers into borrowers.

Meanwhile, Lending Club, an online lender that makes both consumer loans and business loans, is up 6.48% on the year. Despite being down 63% from their IPO price, Lending Club is different in that they generate fee income off of originated loans rather than book loans on balance sheet like OnDeck.

What ties them all together is that OnDeck, Square and Lending Club all rely on chartered banks to make the loans they advertise, a model that is coming under scrutiny by states such as New York. OnDeck and Square both depend on Celtic Bank, a Utah-chartered industrial bank.

Among its peers, OnDeck arguably has the riskiest makeup. They’re concentrated in only one type of lending, they have high acquisition costs, and they retain direct exposure to the loans they generate. Combine that with a lack of profits, lack of growth, and future regulatory challenges ahead, and it’s easy to understand why they’re so significantly underperforming the pack.

Lending Club Raises Minimum Deposit Amount for New Investors

May 18, 2017The micro retail investor can no longer experiment with peer-to-peer lending through just a handful of loans, according to a recent announcement made by Lending Club. Going forward, new users must deposit at least $1,000 to get started. Those investors can still allocate $25 per loan, however. The reason for the deposit increase? Forced diversification.

A Lending Club blog post explained that “data shows that Lending Club investors who are able to diversify their accounts have generally experienced less volatility than investors with more concentrated holdings. This is in part because investors are able to purchase multiple Notes, reducing their exposure to any single Note.” 98% of accounts with more than 100 notes have experienced positive returns, they claim.

On the LendAcademy blog, Peter Renton advocated for an even higher minimum, $2,500, so that investors could at least start off with 100 notes.

It’s an acknowledgment that the type of investing actually carries the risk of loss and is not actually for everyone. I would not be surprised if they eventually set a minimum deposit amount of $10,000 or simply phased out retail investors altogether in favor of accredited ones at a minimum instead. Time will tell.

Federal Court Agrees, Merchant Cash Advances Not Loans or Usurious

May 13, 2017 By now, numerous judges in the New York Supreme Court have concurred that purchases of future receivables are not loans nor usurious, yet challenges to these contracts continue. In the latest landmark ruling, defendants/counterclaim plaintiffs Epazz, Inc., Cynergy Corporation, and Shaun Passley a/k/a Shaun A. Passley, moved to have the original action involving their merchant cash advance dispute transferred from state court to federal court, perhaps hoping for a different opinion on whether such agreements are usurious.

By now, numerous judges in the New York Supreme Court have concurred that purchases of future receivables are not loans nor usurious, yet challenges to these contracts continue. In the latest landmark ruling, defendants/counterclaim plaintiffs Epazz, Inc., Cynergy Corporation, and Shaun Passley a/k/a Shaun A. Passley, moved to have the original action involving their merchant cash advance dispute transferred from state court to federal court, perhaps hoping for a different opinion on whether such agreements are usurious.

The law was not on their side. In the Southern District of New York, a federal court, the Honorable Louis L. Stanton echoed on May 9th, 2017, what state judges have been saying all along, that a purchase is not a loan because the purchased receipts are not payable absolutely.

In this case, the “receipts purchased amounts” are not payable absolutely. Payment depends upon a crucial contingency: the continued collection of receipts by Epazz from its customers. TVT [TVT Capital] is only entitled to recover 15% of Epazz’s daily receipts, and if Epazz’s sales decline or cease the receipts purchased amounts might never be paid in full. See counterclaims, Exhs. A-C at 1. The agreements specifically provide that “Payments made to FUNDER in respect to the full amount of the Receipts shall be conditioned upon Merchant’s sale of products and services and the payment therefore by Merchant’s customers in the manner provided in Section 1.1.” Id. at 3 § 1.9.

Defendants’ argument that the actual daily payments ensure that TVT will be paid the full receipts purchased amounts within approximately 61 to 180 business days, id. ¶¶ 33-47, is contradicted by the reconciliation provisions which provide if the daily payments are greater than 15% of Epazz’s daily receipts, TVT must credit the difference to Epazz, thus limiting Epazz’s obligation to 15% of daily receipts. No allegation is made that TVT ever denied Epazz’s request to reconcile the daily payments. TVT’s right to collect the receipts purchased amounts from Epazz is in fact contingent on Epazz’s continued collection of receipts. See Kardovich v. Pfizer, Inc., 97 F. Supp. 3d 131, 140 (E.D.N.Y. 2015), quoting Amidax Trading Grp. v. S.W.I.F.T. SCRL, 671 F.3d 140, 147 (2d Cir. 2011) (“Where a conclusory allegation in the complaint is contradicted by a document attached to the complaint, the document controls and the allegation is not accepted as true”).

None of the defendants’ arguments, Counterclaims ¶¶ 51-109, change the fact that whether the receipts purchased amounts will be paid in full, or when they will be paid, cannot be known because payment is contingent on Epazz generating sufficient receipts from its customers; and Epazz, rather than TVT, controls whether daily payments will be reconciled.

The decision relies heavily on the reconciliation clause common to merchant cash advance agreements, whereby merchants can adjust their daily ACH amounts to correlate with their actual sales activity. This concept is explained at length in the Merchant Cash Advance Basics training course.

Furthermore, the court was incredulous over the defendants’ claim that they actually wanted loans but were instead fraudulently induced into purchase agreements.

Defendants do not claim that they were misled with regard to the amount of their payment obligation, only that they were misled into believing that their repayment obligation would be absolute when it actually is contingent. Their injury from that is unclear.

In short, the judge suggests that entering into a loan would’ve been worse because it was absolutely repayable, whereas the purchase agreement was not. So how could they have been damaged?

The entire decision surrounding all the claims can be downloaded here.

The case is Colonial Funding Network, Inc. as servicing provider for TVT Capital, LLC v. Epazz, Inc. Cynergy Corporation, and Shaun Passley a/k/a Shaun A. Passley in the United States District Court’s Southern District of New York. Case: 1:16-cv-05948-LLS.

Defendants Shaun Passley and Epazz also lost challenges in another merchant cash advance case in the New York Supreme Court.